Das könnte Ihnen auch gefallen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Your Account Summary: Airtel Number MR Bucha Reddy ADokument8 SeitenYour Account Summary: Airtel Number MR Bucha Reddy AKothamasu PrasadNoch keine Bewertungen

- Tutorial Letter 201/2/2018: Business Management 1ADokument18 SeitenTutorial Letter 201/2/2018: Business Management 1ABen BenNoch keine Bewertungen

- Unified DCR 37 (1 AA) DT 08 03 2019..Dokument6 SeitenUnified DCR 37 (1 AA) DT 08 03 2019..GokulNoch keine Bewertungen

- PRC Ready ReckonerDokument2 SeitenPRC Ready Reckonersparthan300Noch keine Bewertungen

- Monopoly: Principles of Microeconomics Douglas Curtis & Ian IrvineDokument36 SeitenMonopoly: Principles of Microeconomics Douglas Curtis & Ian IrvineNameNoch keine Bewertungen

- Dairy TemplateDokument3 SeitenDairy TemplateSK FoodnBeveragesNoch keine Bewertungen

- Aviation Industry in India - Challenges For The Low Cost CarriersDokument11 SeitenAviation Industry in India - Challenges For The Low Cost Carrierstake3Noch keine Bewertungen

- Preparing The Philippines For The 4th Industrial Revo PIDS Report 2017-2018Dokument120 SeitenPreparing The Philippines For The 4th Industrial Revo PIDS Report 2017-2018Rico EstarasNoch keine Bewertungen

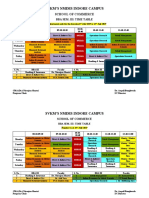

- Time-Table - BBA 3rd SemesterDokument2 SeitenTime-Table - BBA 3rd SemesterSunny GoyalNoch keine Bewertungen

- Prime HR & Security Solutions PVT LTD: SUB: Appointment As HR ExecutiveDokument3 SeitenPrime HR & Security Solutions PVT LTD: SUB: Appointment As HR ExecutivesayalikNoch keine Bewertungen

- Customer Perception of Service Quality at Indian Overseas BankDokument96 SeitenCustomer Perception of Service Quality at Indian Overseas BankRenjith K PushpanNoch keine Bewertungen

- Nepal's 2072 Trade Policy GoalsDokument11 SeitenNepal's 2072 Trade Policy GoalsBinay AcharyaNoch keine Bewertungen

- Akpk SlideDokument13 SeitenAkpk SlideizzatiNoch keine Bewertungen

- List of Maharashtra Pharrma CompaniesDokument6 SeitenList of Maharashtra Pharrma CompaniesrajnayakpawarNoch keine Bewertungen

- List of Philippine AcronymsDokument4 SeitenList of Philippine AcronymsLenniel MinaNoch keine Bewertungen

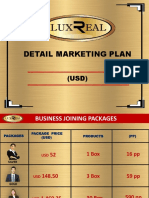

- Luxreal Detail Marketing Plan (2019) UsdDokument32 SeitenLuxreal Detail Marketing Plan (2019) UsdTawanda Tirivangani100% (2)

- Proposal HydrologyDokument4 SeitenProposal HydrologyClint Sunako FlorentinoNoch keine Bewertungen

- GIDB3647341-Money WorksheetDokument6 SeitenGIDB3647341-Money WorksheetAnonymous GxsqKv85GNoch keine Bewertungen

- Data Prep - Homogeneity (Excel)Dokument5 SeitenData Prep - Homogeneity (Excel)NumXL ProNoch keine Bewertungen

- Pre Test of Bahasa Inggris 21 - 9 - 2020Dokument5 SeitenPre Test of Bahasa Inggris 21 - 9 - 2020magdalena sriNoch keine Bewertungen

- PUGEL 'Scale Economies Imperfect Competition and Trade' INTERNATIONAL ECONOMICS 6ED - Thomas Pugel - 001 PDFDokument29 SeitenPUGEL 'Scale Economies Imperfect Competition and Trade' INTERNATIONAL ECONOMICS 6ED - Thomas Pugel - 001 PDFPraba Vettrivelu100% (1)

- Training Manual PPDokument26 SeitenTraining Manual PPKingsmond EhimareNoch keine Bewertungen

- LLP NotesDokument8 SeitenLLP NotesRajaNoch keine Bewertungen

- IBT-REVIEWERDokument10 SeitenIBT-REVIEWERBrenda CastilloNoch keine Bewertungen

- Mcom Cbcs LatestDokument45 SeitenMcom Cbcs Latestanoopsingh19992010Noch keine Bewertungen

- Machu Picchu ToursDokument14 SeitenMachu Picchu ToursCarmen RosasNoch keine Bewertungen

- Can China Keep Rising Despite US PushbackDokument9 SeitenCan China Keep Rising Despite US PushbackVidas ŽūkasNoch keine Bewertungen

- Comparative Analysis of Public & Private Bank (Icici &sbi) - 1Dokument108 SeitenComparative Analysis of Public & Private Bank (Icici &sbi) - 1Sami Zama100% (1)

- FAR1 ASN01 Balance Sheet and Income Statement PDFDokument1 SeiteFAR1 ASN01 Balance Sheet and Income Statement PDFira concepcionNoch keine Bewertungen

- Duncan Hallas - The Meaning of MarxismDokument69 SeitenDuncan Hallas - The Meaning of MarxismROWLAND PASARIBUNoch keine Bewertungen