Das könnte Ihnen auch gefallen

- Bank Secrecy ExceptionsDokument1 SeiteBank Secrecy ExceptionsLeah Marie SiosonNoch keine Bewertungen

- NMAT Sample Paper With Answer KeyDokument4 SeitenNMAT Sample Paper With Answer KeyBATHULA MURALIKRISHNA CSE-2018 BATCHNoch keine Bewertungen

- Labor Law Bar TipsDokument17 SeitenLabor Law Bar TipsMelissaRoseMolinaNoch keine Bewertungen

- Characteristics and Elements of Negotiable InstrumentsDokument13 SeitenCharacteristics and Elements of Negotiable InstrumentsLorenz Reyes100% (2)

- PAras Vs Kimwa ConstructionDokument6 SeitenPAras Vs Kimwa ConstructionVince Llamazares LupangoNoch keine Bewertungen

- Cases For Digest in Commercial LawDokument1 SeiteCases For Digest in Commercial LawLizzette GuiuntabNoch keine Bewertungen

- Maderada vs. MediodeaDokument8 SeitenMaderada vs. MediodeaBea CapeNoch keine Bewertungen

- Case DigestDokument15 SeitenCase DigestFritz Jared P. AfableNoch keine Bewertungen

- Law On Public Officers Set 2 CasesDokument10 SeitenLaw On Public Officers Set 2 CasesPrincess DarimbangNoch keine Bewertungen

- NIL Finals Samplex AnswerDokument5 SeitenNIL Finals Samplex AnswerMark De JesusNoch keine Bewertungen

- Bar Examination Questionnaire On Mercantile Law MCQ (50 Items)Dokument14 SeitenBar Examination Questionnaire On Mercantile Law MCQ (50 Items)Aries MatibagNoch keine Bewertungen

- Limited Partnership - Grp. 4Dokument29 SeitenLimited Partnership - Grp. 4Steven Kyle PeregrinoNoch keine Bewertungen

- Republic Vs BagtasDokument1 SeiteRepublic Vs BagtasCareyssa MaeNoch keine Bewertungen

- Art. 1785-1809 CasesDokument98 SeitenArt. 1785-1809 CasesTokie TokiNoch keine Bewertungen

- Cases On Vawc9262Dokument3 SeitenCases On Vawc9262Maris Joy BartolomeNoch keine Bewertungen

- Election Law: By: Dean Hilario Justino F. MoralesDokument19 SeitenElection Law: By: Dean Hilario Justino F. MoralesmarkbulloNoch keine Bewertungen

- LAW1103 Reflective EssayDokument2 SeitenLAW1103 Reflective Essay뿅아리Noch keine Bewertungen

- 24 Camp John Hay Development Corp. v. CBAA, 706 SCRA 547Dokument2 Seiten24 Camp John Hay Development Corp. v. CBAA, 706 SCRA 547Raymond MedinaNoch keine Bewertungen

- DO 174 Series of 2017Dokument2 SeitenDO 174 Series of 2017jearnaezNoch keine Bewertungen

- FINAL-QUESTIONS-WITH-ANSWERS-legal ClashDokument37 SeitenFINAL-QUESTIONS-WITH-ANSWERS-legal ClashMaureen AdriaticoNoch keine Bewertungen

- BELTRAN Vs Samson - AubreyDokument1 SeiteBELTRAN Vs Samson - AubreyNanz JermaeNoch keine Bewertungen

- 19-Mondano Vs Silvosa 97 Phil 143Dokument3 Seiten19-Mondano Vs Silvosa 97 Phil 143enan_intonNoch keine Bewertungen

- Acme Shoe, Rubber & Plastic Corp. v. CADokument2 SeitenAcme Shoe, Rubber & Plastic Corp. v. CAAgee Romero-ValdesNoch keine Bewertungen

- Green Valley Poultry v. SquibbDokument2 SeitenGreen Valley Poultry v. SquibbMike Zaccahry MilcaNoch keine Bewertungen

- AgPart 925 - PartDokument270 SeitenAgPart 925 - Partcezar delailaniNoch keine Bewertungen

- Canon 20 - A Lawyer Shall Charge Only Fair and Reasonable FeesDokument3 SeitenCanon 20 - A Lawyer Shall Charge Only Fair and Reasonable FeesMalagant EscuderoNoch keine Bewertungen

- 2 Solidbank Vs MinfancoDokument1 Seite2 Solidbank Vs MinfancoraizaNoch keine Bewertungen

- Makati Leasing V Wearever Textile G.R. No. L-58469Dokument10 SeitenMakati Leasing V Wearever Textile G.R. No. L-58469Gillian Caye Geniza BrionesNoch keine Bewertungen

- Classification of LandsDokument3 SeitenClassification of LandsKaren Maechelle EdullantesNoch keine Bewertungen

- Persons Case Digests 4Dokument16 SeitenPersons Case Digests 4Burt Ezra Lequigan PiolNoch keine Bewertungen

- Corporation Cannot Invoke Right Against Self-IncriminationDokument3 SeitenCorporation Cannot Invoke Right Against Self-IncriminationAQAANoch keine Bewertungen

- 2 Fold Aspects of Religious Profession and Worship NamelyDokument1 Seite2 Fold Aspects of Religious Profession and Worship NamelyJennica Gyrl G. DelfinNoch keine Bewertungen

- Admin Digest 2Dokument10 SeitenAdmin Digest 2rheyneNoch keine Bewertungen

- LEX LEONUM FRATERNITAS MEMORY AIDDokument5 SeitenLEX LEONUM FRATERNITAS MEMORY AIDHappy SunshineNoch keine Bewertungen

- Liability of Industrial Partners to Third PartiesDokument1 SeiteLiability of Industrial Partners to Third PartiesLeyCodes LeyCodesNoch keine Bewertungen

- Article 1409 - PPDokument3 SeitenArticle 1409 - PPrheaNoch keine Bewertungen

- 16 Martinez Vs CADokument17 Seiten16 Martinez Vs CAMariel D. PortilloNoch keine Bewertungen

- OFFICE OF THE COURT ADMINISTRATOR v. RODELIO E. MARCELO and MA. CORAZON D. ESPAÑOLADokument1 SeiteOFFICE OF THE COURT ADMINISTRATOR v. RODELIO E. MARCELO and MA. CORAZON D. ESPAÑOLAm_oailNoch keine Bewertungen

- Spouses GuevaraDokument9 SeitenSpouses GuevaraShariqah Hanimai Indol Macumbal-YusophNoch keine Bewertungen

- Case11 Dalisay Vs Atty Batas Mauricio AC No. 5655Dokument6 SeitenCase11 Dalisay Vs Atty Batas Mauricio AC No. 5655ColenNoch keine Bewertungen

- The Family Code of The PhilippinesDokument26 SeitenThe Family Code of The PhilippinesEricka Jane CeballosNoch keine Bewertungen

- Incorporation FacilitatedDokument5 SeitenIncorporation FacilitatedMarc Aderades LaureanoNoch keine Bewertungen

- Modes of Acquiring OwnershipDokument2 SeitenModes of Acquiring OwnershipRengie GaloNoch keine Bewertungen

- Supreme Court declares Pork Barrel System unconstitutionalDokument3 SeitenSupreme Court declares Pork Barrel System unconstitutionalDom Robinson BaggayanNoch keine Bewertungen

- Labor Standards: Atty. Nelson T. Bandoles, LPTDokument374 SeitenLabor Standards: Atty. Nelson T. Bandoles, LPTLeo Carlo CahanapNoch keine Bewertungen

- FRIVALDO Vs COMELECDokument2 SeitenFRIVALDO Vs COMELECJeralynNoch keine Bewertungen

- Transfer TaxesDokument8 SeitenTransfer TaxesMikee TanNoch keine Bewertungen

- Nicolas Vs ComelecDokument1 SeiteNicolas Vs ComelecGem S. AlegadoNoch keine Bewertungen

- G.R. No. 208566 November 19, 2013 BELGICA vs. HONORABLE EXECUTIVE SECRETARY PAQUITO N. OCHOA JR, Et Al, RespondentsDokument2 SeitenG.R. No. 208566 November 19, 2013 BELGICA vs. HONORABLE EXECUTIVE SECRETARY PAQUITO N. OCHOA JR, Et Al, RespondentsPrincess Paida Disangcopan ModasirNoch keine Bewertungen

- Law On Corporations Test Bank With Revised Corporate Code References - CompressDokument62 SeitenLaw On Corporations Test Bank With Revised Corporate Code References - CompressCharles MateoNoch keine Bewertungen

- Res judicata bars second case on membership statusDokument37 SeitenRes judicata bars second case on membership statusDonna PhoebeNoch keine Bewertungen

- CredTrans ChartDokument2 SeitenCredTrans ChartElsha DamoloNoch keine Bewertungen

- Taxation Ii Atty. Shirley Tuazon I. Taxation Under The NircDokument5 SeitenTaxation Ii Atty. Shirley Tuazon I. Taxation Under The NircRonnel DeinlaNoch keine Bewertungen

- Periquet vs. NLRCDokument5 SeitenPeriquet vs. NLRCJasper PelayoNoch keine Bewertungen

- CorpLaw 2014 Outline and CodalDokument73 SeitenCorpLaw 2014 Outline and CodalNori LolaNoch keine Bewertungen

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDokument5 SeitenBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledAnie Guiling-Hadji GaffarNoch keine Bewertungen

- Updates On TaxDokument57 SeitenUpdates On TaxSamuel CrawfordNoch keine Bewertungen

- Ra 10021Dokument2 SeitenRa 10021nikkadavidNoch keine Bewertungen

- 11 RR 10-2010 PDFDokument4 Seiten11 RR 10-2010 PDFJoyceNoch keine Bewertungen

- Be It Enacted by The Senate and House of Representatives of The Philippine Congress AssembledDokument3 SeitenBe It Enacted by The Senate and House of Representatives of The Philippine Congress AssembledCyruss Xavier Maronilla NepomucenoNoch keine Bewertungen

- Guerrero vs. BihisDokument9 SeitenGuerrero vs. BihisDeus DulayNoch keine Bewertungen

- RR No. 30-02Dokument1 SeiteRR No. 30-02Joanna MandapNoch keine Bewertungen

- Supreme Court of the Philippines rules on consolidated petitions regarding termination of employmentDokument14 SeitenSupreme Court of the Philippines rules on consolidated petitions regarding termination of employmentJoanna MandapNoch keine Bewertungen

- Vitug vs. CA FullDokument6 SeitenVitug vs. CA FullJoanna MandapNoch keine Bewertungen

- Cebu Country Club Vs Elizagaque 2008Dokument5 SeitenCebu Country Club Vs Elizagaque 2008Joanna MandapNoch keine Bewertungen

- Revenue Regulation 2-99Dokument5 SeitenRevenue Regulation 2-99Joanna MandapNoch keine Bewertungen

- Valle Verde Country Club vs. Africa Sept 2009Dokument4 SeitenValle Verde Country Club vs. Africa Sept 2009Joanna MandapNoch keine Bewertungen

- CIR vs. Pascor Realty 1999Dokument11 SeitenCIR vs. Pascor Realty 1999Joanna MandapNoch keine Bewertungen

- Vitug vs. CA FullDokument6 SeitenVitug vs. CA FullJoanna MandapNoch keine Bewertungen

- CIR vs. Sony Phils 2010Dokument16 SeitenCIR vs. Sony Phils 2010Joanna MandapNoch keine Bewertungen

- IPL DigestsDokument14 SeitenIPL DigestsJoanna MandapNoch keine Bewertungen

- 2010 BIR RegulationsDokument1 Seite2010 BIR RegulationsJoanna MandapNoch keine Bewertungen

- The Local Government Code of The Philippines Book IiDokument58 SeitenThe Local Government Code of The Philippines Book IiXavier Hawkins Lopez ZamoraNoch keine Bewertungen

- RMO 10-2013 Revised SDT GuidelinesDokument8 SeitenRMO 10-2013 Revised SDT GuidelinesJoanna MandapNoch keine Bewertungen

- 1.in The Matter of James Joseph HammDokument12 Seiten1.in The Matter of James Joseph HammJoanna Mandap100% (1)

- Remedies of The Govt SummaryDokument10 SeitenRemedies of The Govt SummaryJoanna MandapNoch keine Bewertungen

- RR No. 30-02Dokument1 SeiteRR No. 30-02Joanna MandapNoch keine Bewertungen

- Tax II Assignment 19 Jul 2013 II PDFDokument147 SeitenTax II Assignment 19 Jul 2013 II PDFJoanna MandapNoch keine Bewertungen

- Corfin Cases Jul10Dokument81 SeitenCorfin Cases Jul10Joanna MandapNoch keine Bewertungen

- 09-3243-RTJ DQ of JudgeDokument7 Seiten09-3243-RTJ DQ of JudgeJoanna MandapNoch keine Bewertungen

- CIR v. Far EAst BackDokument11 SeitenCIR v. Far EAst BackJoanna MandapNoch keine Bewertungen

- CIR v. SmartDokument13 SeitenCIR v. SmartJoanna MandapNoch keine Bewertungen

- IRS 2-Year Refund Period for Quarterly TaxesDokument7 SeitenIRS 2-Year Refund Period for Quarterly TaxesJoanna MandapNoch keine Bewertungen

- 11 CIR Vs American Express 2005Dokument17 Seiten11 CIR Vs American Express 2005Joanna MandapNoch keine Bewertungen

- 6 Mindanao II Vs CIR 2013Dokument30 Seiten6 Mindanao II Vs CIR 2013Joanna MandapNoch keine Bewertungen

- The Local Government Code of The Philippines Book IiDokument58 SeitenThe Local Government Code of The Philippines Book IiXavier Hawkins Lopez ZamoraNoch keine Bewertungen

- Hotels in Florence, Tuscany Aug-SeptDokument1 SeiteHotels in Florence, Tuscany Aug-SeptJoanna MandapNoch keine Bewertungen

- ACCRA v. CADokument5 SeitenACCRA v. CAJoanna MandapNoch keine Bewertungen

- AMENDMENTS of RA 8293 (IP Code) PDFDokument15 SeitenAMENDMENTS of RA 8293 (IP Code) PDFNikki MendozaNoch keine Bewertungen

- SC upholds constitutionality of tax under Sugar Adjustment ActDokument14 SeitenSC upholds constitutionality of tax under Sugar Adjustment ActMirafelNoch keine Bewertungen

- Instructions for filling Schedule TDS 1Dokument2 SeitenInstructions for filling Schedule TDS 1AbhishekNoch keine Bewertungen

- Business Taxation Chapter 7 - Business Taxes (Group 5) : A. Gross Selling PriceDokument25 SeitenBusiness Taxation Chapter 7 - Business Taxes (Group 5) : A. Gross Selling PriceDizon Ropalito P.Noch keine Bewertungen

- April 23, 2021 Strathmore TimesDokument12 SeitenApril 23, 2021 Strathmore TimesStrathmore TimesNoch keine Bewertungen

- (4525) Rashtriya Ispat Nigam Limited (211101006626)Dokument1 Seite(4525) Rashtriya Ispat Nigam Limited (211101006626)Dontha VenkateshNoch keine Bewertungen

- Fiscal Policy of IndiaDokument18 SeitenFiscal Policy of IndiaRahulNoch keine Bewertungen

- Measures of Economic Activity and GDP ComponentsDokument72 SeitenMeasures of Economic Activity and GDP ComponentsGhassan AlMahalNoch keine Bewertungen

- 1Dokument2 Seiten1Anonymous Hig1tC2h67% (6)

- Taco 200717DF00065129Dokument1 SeiteTaco 200717DF00065129Frank Edwin VedamNoch keine Bewertungen

- The Multiplier Model ExplainedDokument35 SeitenThe Multiplier Model ExplainedannsaralondeNoch keine Bewertungen

- A Logical Approach to Regulating AirbnbDokument35 SeitenA Logical Approach to Regulating AirbnbMelinda Rahma ArulliaNoch keine Bewertungen

- Gas Station Plaridel BypassDokument19 SeitenGas Station Plaridel BypassEladio AbquinaNoch keine Bewertungen

- Bir Ruling Da 013 08Dokument5 SeitenBir Ruling Da 013 08Nash Ortiz LuisNoch keine Bewertungen

- Tax Bulletin - January 2023Dokument23 SeitenTax Bulletin - January 2023AliNoch keine Bewertungen

- Gepco Online BillDokument2 SeitenGepco Online BillHafiz RizwanNoch keine Bewertungen

- Theories of Poverty and Community DevelopmentDokument13 SeitenTheories of Poverty and Community DevelopmentOm Prakash100% (2)

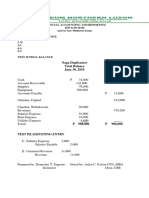

- Financial Accounting and Reporting Midterm Exam KeyDokument4 SeitenFinancial Accounting and Reporting Midterm Exam KeyDonita Joy T. EugenioNoch keine Bewertungen

- Submitted To: Sir Haris Group Name: Moshin Raza 26 Bilal Asif 29 Saira Ishtiaq 03 Maria Farooqi 02Dokument30 SeitenSubmitted To: Sir Haris Group Name: Moshin Raza 26 Bilal Asif 29 Saira Ishtiaq 03 Maria Farooqi 02daniyalNoch keine Bewertungen

- Sindh Sales Tax On Services Rules 2011 (Amendede Upto 30 Nov 2012) PDFDokument64 SeitenSindh Sales Tax On Services Rules 2011 (Amendede Upto 30 Nov 2012) PDFrohail51Noch keine Bewertungen

- A Study On The Impact of Demonetization and GST On The Indian Banking SectorDokument8 SeitenA Study On The Impact of Demonetization and GST On The Indian Banking SectorAnonymous izrFWiQNoch keine Bewertungen

- Bears in The City Big Screen To Ipad Outfoxed: France Warns Cameron Over Push For City Veto in Eu NegotiationsDokument57 SeitenBears in The City Big Screen To Ipad Outfoxed: France Warns Cameron Over Push For City Veto in Eu NegotiationsstefanoNoch keine Bewertungen

- GMIDC B1 Tender Survey Design Estimates Repairs CanalsDokument164 SeitenGMIDC B1 Tender Survey Design Estimates Repairs CanalskkodgeNoch keine Bewertungen

- 06 Philex Mining vs. CIRDokument1 Seite06 Philex Mining vs. CIRJoshua Erik Madria100% (1)

- By Graham HoltDokument5 SeitenBy Graham Holtwhosnext886Noch keine Bewertungen

- Uganda's National 4IR StrategyDokument15 SeitenUganda's National 4IR StrategyThe Independent Magazine100% (1)

- PNOC v. CA (G.R. No. 109976. April 26, 2005.)Dokument2 SeitenPNOC v. CA (G.R. No. 109976. April 26, 2005.)Emmanuel Yrreverre100% (1)

- Request A Distribution - Hardship Guidelines: More ResourcesDokument2 SeitenRequest A Distribution - Hardship Guidelines: More ResourcesJason ChanNoch keine Bewertungen

- Assignment Module 3Dokument2 SeitenAssignment Module 3Drew BanlutaNoch keine Bewertungen

- AccountingDokument9 SeitenAccountingButternut23Noch keine Bewertungen

- Solution Manual For Managerial Economics Froeb Mccann Ward Shor 3rd EditionDokument6 SeitenSolution Manual For Managerial Economics Froeb Mccann Ward Shor 3rd EditionDavid RigdonNoch keine Bewertungen