Das könnte Ihnen auch gefallen

- Federal Income Tax: a QuickStudy Digital Law ReferenceVon EverandFederal Income Tax: a QuickStudy Digital Law ReferenceNoch keine Bewertungen

- Introduction To TaxDokument18 SeitenIntroduction To TaxVenniah MusundaNoch keine Bewertungen

- 2011 - ITR2 - r6Dokument33 Seiten2011 - ITR2 - r6Bathina Srinivasa RaoNoch keine Bewertungen

- Income TaxDokument6 SeitenIncome TaxKuldeep HoodaNoch keine Bewertungen

- ITR-4S: Assessment Year (Presumptive Business Income Tax Return) Indian Income Tax Return SugamDokument11 SeitenITR-4S: Assessment Year (Presumptive Business Income Tax Return) Indian Income Tax Return SugamcachandhiranNoch keine Bewertungen

- IT Return 2011 2012Dokument3 SeitenIT Return 2011 2012swapnil6121986Noch keine Bewertungen

- Assessment Year Indian Income Tax Return: I - IndividualDokument6 SeitenAssessment Year Indian Income Tax Return: I - IndividualManjunath YvNoch keine Bewertungen

- SARS Tax Tables: Download This Report and Save It On Your Desktop For Quick Tax Table Access 24/7Dokument6 SeitenSARS Tax Tables: Download This Report and Save It On Your Desktop For Quick Tax Table Access 24/7dannyboy738Noch keine Bewertungen

- 2016 Itr4 PR3Dokument165 Seiten2016 Itr4 PR3TejasNoch keine Bewertungen

- Indian Income Tax Return Assessment Year SahajDokument7 SeitenIndian Income Tax Return Assessment Year SahajSubrata BiswasNoch keine Bewertungen

- Financial StatementDokument21 SeitenFinancial StatementBiancaDoloNoch keine Bewertungen

- Gross Total Income (1+2c) 4: System CalculatedDokument3 SeitenGross Total Income (1+2c) 4: System CalculatedDHARAMSONINoch keine Bewertungen

- Income Tax CalculatorDokument4 SeitenIncome Tax CalculatorKarthick NNoch keine Bewertungen

- Assessment Year Sahaj Indian Income Tax ReturnDokument7 SeitenAssessment Year Sahaj Indian Income Tax Returnrajshri58Noch keine Bewertungen

- Return of Total Income/Statement of Final TaxationDokument1 SeiteReturn of Total Income/Statement of Final TaxationJazzy BadshahNoch keine Bewertungen

- Bir Form 1701Dokument12 SeitenBir Form 1701miles1280Noch keine Bewertungen

- Assessment Year Indian Income Tax Return SahajDokument7 SeitenAssessment Year Indian Income Tax Return SahajallipraNoch keine Bewertungen

- UntitledDokument21 SeitenUntitleddhirajpironNoch keine Bewertungen

- TAX228 - Individuals 2023Dokument42 SeitenTAX228 - Individuals 2023edwardsyaameenNoch keine Bewertungen

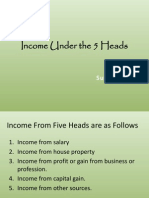

- Income Under The 5 Heads: Sudhir YadavDokument21 SeitenIncome Under The 5 Heads: Sudhir YadavpreetkaurrandhawaNoch keine Bewertungen

- Sachin4kumar@yahoo - Co.in: Gross Total Income (1+2c) 4Dokument3 SeitenSachin4kumar@yahoo - Co.in: Gross Total Income (1+2c) 4Sachin KumarNoch keine Bewertungen

- 2012 Itr1 Pr21Dokument5 Seiten2012 Itr1 Pr21MRLogan123Noch keine Bewertungen

- Computation Format PDFDokument2 SeitenComputation Format PDFRajesh Jaiswal100% (1)

- Assessment Year Indian Income Tax Return Year Sahaj: Seal and Signature of Receiving Official Receipt No/ DateDokument3 SeitenAssessment Year Indian Income Tax Return Year Sahaj: Seal and Signature of Receiving Official Receipt No/ DatethakurrobinNoch keine Bewertungen

- Accounting For Income TaxDokument18 SeitenAccounting For Income TaxChirag PatelNoch keine Bewertungen

- Macroeconomics-1 by Prof. N.C.nayakDokument7 SeitenMacroeconomics-1 by Prof. N.C.nayakSomasish GhoshNoch keine Bewertungen

- 2013 Itr1 PR11Dokument9 Seiten2013 Itr1 PR11Akshay Kumar SahooNoch keine Bewertungen

- How Does It Work?: Train Law Vs Nirc What Is NIRC?Dokument7 SeitenHow Does It Work?: Train Law Vs Nirc What Is NIRC?Bryant R. CanasaNoch keine Bewertungen

- Introduction To Regular Income TaxDokument44 SeitenIntroduction To Regular Income TaxGabriel Trinidad Soniel0% (1)

- Income Under The 5 Heads: Sudhir YadavDokument21 SeitenIncome Under The 5 Heads: Sudhir YadavJankiTrivediNoch keine Bewertungen

- 1701 Bir FormDokument12 Seiten1701 Bir Formbertlaxina0% (1)

- 2011 ITR1 r2Dokument3 Seiten2011 ITR1 r2Zafar IqbalNoch keine Bewertungen

- Bir Forms PDFDokument4 SeitenBir Forms PDFgaryNoch keine Bewertungen

- Law of TaxationDokument9 SeitenLaw of TaxationSikandar KhalilNoch keine Bewertungen

- Income Tax CalculationDokument1 SeiteIncome Tax Calculationsoumyadeep1947Noch keine Bewertungen

- ITR-3 Indian Income Tax Return: Part A-GENDokument12 SeitenITR-3 Indian Income Tax Return: Part A-GENmehtakvijayNoch keine Bewertungen

- Presentation On TaxationDokument12 SeitenPresentation On Taxationpraveenjoshi554Noch keine Bewertungen

- 2023 Slides On Exempt IncomeDokument31 Seiten2023 Slides On Exempt IncomeSiphesihleNoch keine Bewertungen

- ITR Form 1Dokument7 SeitenITR Form 1gj29hereNoch keine Bewertungen

- Gross Total Income (1+2+3) 4: System CalculatedDokument8 SeitenGross Total Income (1+2+3) 4: System CalculatedShunmuga ThangamNoch keine Bewertungen

- National Income Formula and NumericalsDokument17 SeitenNational Income Formula and Numericalsbhaskarvishal100% (6)

- Gross Total Income (1+2c) 4: Import Previous VersionDokument4 SeitenGross Total Income (1+2c) 4: Import Previous Versionbalajiv_mailNoch keine Bewertungen

- Section TWO 2024Dokument5 SeitenSection TWO 2024basuonyshowNoch keine Bewertungen

- TAX4862 TL107 - 2019 Slides 1 Per PGDokument139 SeitenTAX4862 TL107 - 2019 Slides 1 Per PGMagda100% (1)

- Macroeconomics National Income AccountingDokument62 SeitenMacroeconomics National Income AccountingCikgu Poli0% (1)

- MG 3027 TAXATION - Week 2 Introduction To Income TaxDokument39 SeitenMG 3027 TAXATION - Week 2 Introduction To Income TaxSyed SafdarNoch keine Bewertungen

- Sales Tax Return 16353854Dokument1 SeiteSales Tax Return 163538547799349Noch keine Bewertungen

- 201111320114552152IT-2 2011withSurchargeWithoutformulawithPEFDokument7 Seiten201111320114552152IT-2 2011withSurchargeWithoutformulawithPEFOmer PashaNoch keine Bewertungen

- Taxation of IncomeDokument43 SeitenTaxation of IncomeWqas AhmedNoch keine Bewertungen

- Topic-2-INTRODUCTION TO DIFFERENT TAXATION LAWS OF PAKISTANDokument18 SeitenTopic-2-INTRODUCTION TO DIFFERENT TAXATION LAWS OF PAKISTANJaved AnwarNoch keine Bewertungen

- Taxppt 130202121230 Phpapp01Dokument11 SeitenTaxppt 130202121230 Phpapp01Deep S MandeepNoch keine Bewertungen

- V. N. Hari,: Sudhakar & Kumar AssociatesDokument79 SeitenV. N. Hari,: Sudhakar & Kumar AssociatesvnharicaNoch keine Bewertungen

- 82255BIR Form 1701Dokument12 Seiten82255BIR Form 1701Leowell John G. RapaconNoch keine Bewertungen

- Monthly Value-Added Tax DeclarationDokument17 SeitenMonthly Value-Added Tax DeclarationMIRAHNELNoch keine Bewertungen

- Exemptions 2024Dokument9 SeitenExemptions 2024mthandazomathNoch keine Bewertungen

- 1040 Exam Prep: Module I: The Form 1040 FormulaVon Everand1040 Exam Prep: Module I: The Form 1040 FormulaBewertung: 1 von 5 Sternen1/5 (3)

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionVon EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNoch keine Bewertungen

- Appreciation of Evidence CriminalDokument18 SeitenAppreciation of Evidence CriminalAbhishek SharmaNoch keine Bewertungen

- Circumstantial EvidenceDokument12 SeitenCircumstantial EvidenceAbhishek SharmaNoch keine Bewertungen

- SC-UoI Panel 11.12.14Dokument29 SeitenSC-UoI Panel 11.12.14Abhishek SharmaNoch keine Bewertungen

- Signature Not VerifiedDokument28 SeitenSignature Not VerifiedAbhishek SharmaNoch keine Bewertungen

- Section Article 14 Bench Strength 8............................................. This Article Corresponds To The EqualDokument34 SeitenSection Article 14 Bench Strength 8............................................. This Article Corresponds To The EqualAbhishek SharmaNoch keine Bewertungen

- Bail & Anticipatory BailDokument76 SeitenBail & Anticipatory BailAbhishek SharmaNoch keine Bewertungen

- Advanced Rulings - Income Tax PDFDokument222 SeitenAdvanced Rulings - Income Tax PDFAbhishek Sharma0% (1)

- Sl. No. S.173, Code of Criminal Procedure Bench Streng TH 11. When A Report Forwarded by The Police To The MagistrateDokument9 SeitenSl. No. S.173, Code of Criminal Procedure Bench Streng TH 11. When A Report Forwarded by The Police To The MagistrateAbhishek SharmaNoch keine Bewertungen

- Sl. No. Legislative Power Bench StrengthDokument6 SeitenSl. No. Legislative Power Bench StrengthAbhishek SharmaNoch keine Bewertungen

- Principle of ParityDokument4 SeitenPrinciple of ParityAbhishek SharmaNoch keine Bewertungen

- 320 - 482Dokument35 Seiten320 - 482Abhishek SharmaNoch keine Bewertungen

- Excise BookDokument70 SeitenExcise BookAbhishek SharmaNoch keine Bewertungen

- Proforma For Mentioning1Dokument1 SeiteProforma For Mentioning1Abhishek SharmaNoch keine Bewertungen

- 227 239 251Dokument55 Seiten227 239 251Abhishek SharmaNoch keine Bewertungen

- Supreme Court Rules 2013Dokument106 SeitenSupreme Court Rules 2013Abhishek SharmaNoch keine Bewertungen

- Foreign Exchange Management Act The RestrictionDokument2 SeitenForeign Exchange Management Act The RestrictionAbhishek SharmaNoch keine Bewertungen

- Punjab and Haryana High Court Rules Volume IVDokument483 SeitenPunjab and Haryana High Court Rules Volume IVAbhishek SharmaNoch keine Bewertungen

- Bar Council of India Rules, Part V OnwardsDokument102 SeitenBar Council of India Rules, Part V OnwardsAbhishek Sharma100% (1)

- Gauhati High Court Judgement - CBI UnconstitutionalDokument89 SeitenGauhati High Court Judgement - CBI UnconstitutionalSuresh NakhuaNoch keine Bewertungen

- IPO ProcedureDokument2 SeitenIPO ProcedureAbhishek SharmaNoch keine Bewertungen

- Bombay High Court Appellate Side RulesDokument198 SeitenBombay High Court Appellate Side RulesAbhishek Sharma50% (4)

- Delhi High Court RulesDokument1.468 SeitenDelhi High Court RulesAbhishek SharmaNoch keine Bewertungen

- Advocate-on-Record Name Lending Judgment.Dokument18 SeitenAdvocate-on-Record Name Lending Judgment.Abhishek SharmaNoch keine Bewertungen

- General Elections 2014 Detailed NotificationDokument85 SeitenGeneral Elections 2014 Detailed NotificationAbhishek SharmaNoch keine Bewertungen

- Bombay High Court Original Side RulesDokument308 SeitenBombay High Court Original Side RulesAbhishek Sharma92% (12)

- Bombay High Court Original Side FormsDokument147 SeitenBombay High Court Original Side FormsAbhishek Sharma100% (2)