Das könnte Ihnen auch gefallen

- Esm 1Dokument8 SeitenEsm 1Economy 365Noch keine Bewertungen

- MSCI-NACUSIP v. National Wages and Productivity CommissionDokument3 SeitenMSCI-NACUSIP v. National Wages and Productivity CommissionbearzhugNoch keine Bewertungen

- Cayman Islands Funds Update Q1 2020 OgierDokument12 SeitenCayman Islands Funds Update Q1 2020 OgierR TNoch keine Bewertungen

- Common Draft Terms of Merger ExampleDokument50 SeitenCommon Draft Terms of Merger ExamplesalarconhNoch keine Bewertungen

- Covered Bond Base Prospectus PDFDokument255 SeitenCovered Bond Base Prospectus PDFFidelis BeryNoch keine Bewertungen

- Corporate Bond GuidelinesDokument12 SeitenCorporate Bond GuidelinesnuhubinadamNoch keine Bewertungen

- MSCI-NACUSIP vs. NWPC and MONOMER SUGAR DIGESTDokument4 SeitenMSCI-NACUSIP vs. NWPC and MONOMER SUGAR DIGESTruelNoch keine Bewertungen

- U.S.$1,154,923,000 Lima Metro Line 2 Finance Limited: 5.875% Series 2015-1 Senior Secured NotesDokument183 SeitenU.S.$1,154,923,000 Lima Metro Line 2 Finance Limited: 5.875% Series 2015-1 Senior Secured NotesHo Chuen Brian KongNoch keine Bewertungen

- IFRS 16 Leases: Application GuidanceDokument34 SeitenIFRS 16 Leases: Application Guidancehisham emamNoch keine Bewertungen

- Visa Inc. To Acquire Visa Europe: Foster City, Ca., and London, UK, November 2, 2015Dokument3 SeitenVisa Inc. To Acquire Visa Europe: Foster City, Ca., and London, UK, November 2, 2015srx devNoch keine Bewertungen

- Weekly UpdateDokument3 SeitenWeekly UpdateKoko FerminNoch keine Bewertungen

- Eac Query 1Dokument6 SeitenEac Query 1ratiNoch keine Bewertungen

- Msci-Nacusip V National Wages and Productivity CommissionDokument3 SeitenMsci-Nacusip V National Wages and Productivity CommissionanailabucaNoch keine Bewertungen

- Financial Institutions' (Recovery of Finances) Rules, 2018Dokument4 SeitenFinancial Institutions' (Recovery of Finances) Rules, 2018Syed AzharNoch keine Bewertungen

- Informe NRSRODokument32 SeitenInforme NRSROSEBASTIAN AGUDELO ECHEVERRINoch keine Bewertungen

- Oh5 Ptblmioe0018 Final Terms - 2012Dokument8 SeitenOh5 Ptblmioe0018 Final Terms - 2012Paulo Jorge OliveiraNoch keine Bewertungen

- Stat Doc 2 Finance - Version 19.0Dokument35 SeitenStat Doc 2 Finance - Version 19.0Phillip kerry-smithNoch keine Bewertungen

- Disclaimer Opinion (Attachment) - FinalDokument2 SeitenDisclaimer Opinion (Attachment) - FinalFierDaus MfmmNoch keine Bewertungen

- Philippine Veterans Bank v. CallanganDokument4 SeitenPhilippine Veterans Bank v. CallanganLDNoch keine Bewertungen

- DSAIDokument11 SeitenDSAIkipkarNoch keine Bewertungen

- Ic 33142Dokument68 SeitenIc 33142Aleksa RancicNoch keine Bewertungen

- Boletín 9 Feb 2009 EnglishDokument8 SeitenBoletín 9 Feb 2009 EnglishRodriguez-Azuero AbogadosNoch keine Bewertungen

- CMBS ProspectusDokument211 SeitenCMBS Prospectussh_chandraNoch keine Bewertungen

- Management?s Proposal To The Extraordinary Shareholders? MeetingDokument8 SeitenManagement?s Proposal To The Extraordinary Shareholders? MeetingUsiminas_RINoch keine Bewertungen

- 15-SPAC - New Trends in France and Europe - Corporate - Commercial Law - European UnionDokument4 Seiten15-SPAC - New Trends in France and Europe - Corporate - Commercial Law - European Unionpayal chaudhariNoch keine Bewertungen

- BDO V Republic (MR - 2016)Dokument67 SeitenBDO V Republic (MR - 2016)MarrielDeTorresNoch keine Bewertungen

- Ibc 2016 MDokument11 SeitenIbc 2016 MMayank SenNoch keine Bewertungen

- Msci-Nacusip vs. NWPC and Monomer Sugar DigestDokument3 SeitenMsci-Nacusip vs. NWPC and Monomer Sugar DigestBruce WayneNoch keine Bewertungen

- Debt Buyback Aug 23 2016Dokument5 SeitenDebt Buyback Aug 23 2016red cornerNoch keine Bewertungen

- 2009 Kaupthing Heads of Terms REDACTEDDokument14 Seiten2009 Kaupthing Heads of Terms REDACTEDHagsmunasamtök heimilannaNoch keine Bewertungen

- Corporate Financial Accounting Project Roll No KSPMCAA012 Dev Shah Mcom Part 2 Sem 4 2022-2023 CARO 2016Dokument5 SeitenCorporate Financial Accounting Project Roll No KSPMCAA012 Dev Shah Mcom Part 2 Sem 4 2022-2023 CARO 2016Dev ShahNoch keine Bewertungen

- Unconventional CDS Credit Events - Hovnanian EnterprisesDokument8 SeitenUnconventional CDS Credit Events - Hovnanian Enterprisesphoennie2512Noch keine Bewertungen

- Notes of VG SIR For Case Law 2016Dokument18 SeitenNotes of VG SIR For Case Law 2016chanduNoch keine Bewertungen

- Understanding The Corporate Insolvency and Resolution ProcessDokument6 SeitenUnderstanding The Corporate Insolvency and Resolution ProcessGourav GhoshNoch keine Bewertungen

- Initial Margin Implementation Under EMIR and The ISDA 2018 Credit Support Deed (For IM) AshurstDokument1 SeiteInitial Margin Implementation Under EMIR and The ISDA 2018 Credit Support Deed (For IM) AshurstRodrigo MellaNoch keine Bewertungen

- MSCI-NACUSIP Local Chapter, Petitioner, vs. NATIONAL WAGES and Productivity Commission and Monomer Sugar CENTRAL, INC., Respondents. G.R. No. 125198. March 3, 1997 FactsDokument3 SeitenMSCI-NACUSIP Local Chapter, Petitioner, vs. NATIONAL WAGES and Productivity Commission and Monomer Sugar CENTRAL, INC., Respondents. G.R. No. 125198. March 3, 1997 FactsAngelaNoch keine Bewertungen

- Credit Cards Order - Final DecisionDokument14 SeitenCredit Cards Order - Final DecisionMohammed Adnane OuzzineNoch keine Bewertungen

- Addendum MB ToolDokument3 SeitenAddendum MB ToolCarol LeónNoch keine Bewertungen

- Atwood Oceanics Inc - Form 8-K (Mar-29-2016)Dokument33 SeitenAtwood Oceanics Inc - Form 8-K (Mar-29-2016)elles1201Noch keine Bewertungen

- FMO Amended and Restated Loan Agreement (EXECUTION)Dokument37 SeitenFMO Amended and Restated Loan Agreement (EXECUTION)Carlo PlasenciaNoch keine Bewertungen

- The Tier 4 Microfinance Institutions and Money Lenders Act, 2016Dokument75 SeitenThe Tier 4 Microfinance Institutions and Money Lenders Act, 2016Paul SitaNoch keine Bewertungen

- Presbe2012 9eDokument2 SeitenPresbe2012 9eChrisBeckerNoch keine Bewertungen

- xs2046736919 Final TermsDokument9 Seitenxs2046736919 Final TermsRajendra AvinashNoch keine Bewertungen

- Cadbury Schweppes PLC, Cadbury Schweppes Overseas LTDDokument6 SeitenCadbury Schweppes PLC, Cadbury Schweppes Overseas LTDDoinița BourNoch keine Bewertungen

- BDO Vs PhilDokument27 SeitenBDO Vs PhilERNIL L BAWANoch keine Bewertungen

- Prs In1402nonhhmarketDokument4 SeitenPrs In1402nonhhmarketgenid.ssNoch keine Bewertungen

- Spanish Market InfrastructureDokument13 SeitenSpanish Market InfrastructureIra IdroesNoch keine Bewertungen

- Notice To MarketDokument4 SeitenNotice To MarketUsiminas_RINoch keine Bewertungen

- The Risk Clearing Settlement and Management Regulation 01.09.2020Dokument21 SeitenThe Risk Clearing Settlement and Management Regulation 01.09.2020griguta99Noch keine Bewertungen

- Tax 1-A Case 40, 80, 120Dokument2 SeitenTax 1-A Case 40, 80, 120Alan GultiaNoch keine Bewertungen

- IBC 2016 and IBC Amendment Bill, 2021Dokument5 SeitenIBC 2016 and IBC Amendment Bill, 2021Keshav GuptaNoch keine Bewertungen

- Notice Rules 68&68.1 2005Dokument9 SeitenNotice Rules 68&68.1 2005alo_nyanya14Noch keine Bewertungen

- Sec-Ogc Opinion No. 01-20: CD Technologies Asia, Inc. 2020Dokument3 SeitenSec-Ogc Opinion No. 01-20: CD Technologies Asia, Inc. 2020Nadine Anne EscalonaNoch keine Bewertungen

- Reforms in Insolvency Law Across The World Due To COVID-19 PandemicDokument13 SeitenReforms in Insolvency Law Across The World Due To COVID-19 PandemicFarha RahmanNoch keine Bewertungen

- Detailed TCSDokument52 SeitenDetailed TCSlegendry007Noch keine Bewertungen

- Estacio Comunicado Encerramento Oferta Publica 20141023 Eng PDFDokument1 SeiteEstacio Comunicado Encerramento Oferta Publica 20141023 Eng PDFEstacio Investor RelationsNoch keine Bewertungen

- Irs 07 July 1999Dokument9 SeitenIrs 07 July 1999ucoNoch keine Bewertungen

- New Decree 1277-12Dokument4 SeitenNew Decree 1277-12Sebastian MaggioNoch keine Bewertungen

- RETRAK and the Ministry of Trade Advocacy PartnershipVon EverandRETRAK and the Ministry of Trade Advocacy PartnershipNoch keine Bewertungen

- Carta Del President Torra Al President SánchezDokument2 SeitenCarta Del President Torra Al President SánchezModerador Noticies WebNoch keine Bewertungen

- Redacted US House Report On Russian Active MeasuresDokument253 SeitenRedacted US House Report On Russian Active MeasuresRT America100% (1)

- A Day For Water and Water For: Sustainable DevelopmentDokument1 SeiteA Day For Water and Water For: Sustainable DevelopmentEpinternetNoch keine Bewertungen

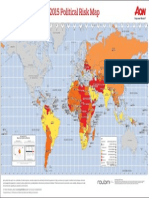

- Mapa Del Riesgo Político en 2015Dokument1 SeiteMapa Del Riesgo Político en 2015EpinternetNoch keine Bewertungen

- Tutorial QN LAWS 3320 OCT 22Dokument5 SeitenTutorial QN LAWS 3320 OCT 22Nur AthirahNoch keine Bewertungen

- Digested CaseDokument1 SeiteDigested CaseEhem DrpNoch keine Bewertungen

- LABOR LAW 1 (Reviewer Based On Codal)Dokument11 SeitenLABOR LAW 1 (Reviewer Based On Codal)Jesse Myl MarciaNoch keine Bewertungen

- Case Study A First Time Expatriate S Controls Inc Experience in A Joint Venture in ChinaDokument21 SeitenCase Study A First Time Expatriate S Controls Inc Experience in A Joint Venture in Chinayk00767% (3)

- Sundiang & Aquino, Reviewer 2014Dokument3 SeitenSundiang & Aquino, Reviewer 2014박은하Noch keine Bewertungen

- Sample FPSB Financial Plan Copyright SAWANTDokument19 SeitenSample FPSB Financial Plan Copyright SAWANTsanket yelaweNoch keine Bewertungen

- Three Models of Corporate Governance From Developed Capital MarketsDokument34 SeitenThree Models of Corporate Governance From Developed Capital MarketsSaahiel SharrmaNoch keine Bewertungen

- Starboard-Presentation PDFDokument294 SeitenStarboard-Presentation PDFArun KumarNoch keine Bewertungen

- Holding Hands Holdings Corporation: By-Laws OFDokument12 SeitenHolding Hands Holdings Corporation: By-Laws OFNorman Kenneth SantosNoch keine Bewertungen

- Official Gazette of The Republic of The Philippines (HTTPS://WWW - Officialgazette.gov - PH/)Dokument46 SeitenOfficial Gazette of The Republic of The Philippines (HTTPS://WWW - Officialgazette.gov - PH/)Gerard TayaoNoch keine Bewertungen

- PNCC 2010 Management LetterDokument95 SeitenPNCC 2010 Management LetterAlyssa ValerioNoch keine Bewertungen

- KyivstarDokument6 SeitenKyivstarТатьяна ПередерийNoch keine Bewertungen

- Đầu tư QT - metroDokument66 SeitenĐầu tư QT - metroMaiNoch keine Bewertungen

- Information Systems Engineering Coursework Assignment - UK University BSC Final YearDokument14 SeitenInformation Systems Engineering Coursework Assignment - UK University BSC Final YearTDiscoverNoch keine Bewertungen

- First Mockbar in RFBT With AnswersDokument18 SeitenFirst Mockbar in RFBT With AnswersMichaelJayCuturaMatolNoch keine Bewertungen

- Order in The Matter of Vanishing CompaniesDokument20 SeitenOrder in The Matter of Vanishing CompaniesShyam SunderNoch keine Bewertungen

- COO Vice President Operations in Southwest US Resume John FogartyDokument4 SeitenCOO Vice President Operations in Southwest US Resume John FogartyjohnfogartyNoch keine Bewertungen

- 1 Shareholders' Agreement - Object Software Ltd. and The9 LTDDokument28 Seiten1 Shareholders' Agreement - Object Software Ltd. and The9 LTDSudeep SharmaNoch keine Bewertungen

- Main Part 1 TranningDokument23 SeitenMain Part 1 TranningRaju100% (2)

- Annual Report 2017 PDFDokument216 SeitenAnnual Report 2017 PDFemmanuelNoch keine Bewertungen

- Meeting, ResolutionDokument21 SeitenMeeting, ResolutionMonica BBANoch keine Bewertungen

- Quiz 2 QuestionDokument3 SeitenQuiz 2 QuestionFatin NajihahNoch keine Bewertungen

- Corporate Governance, Business Ethics, Risk Management and Internal ControlDokument43 SeitenCorporate Governance, Business Ethics, Risk Management and Internal ControlRohanne Garcia AbrigoNoch keine Bewertungen

- Jun 2004 - Qns Mod ADokument12 SeitenJun 2004 - Qns Mod AHubbak KhanNoch keine Bewertungen

- Cadbury 2010Dokument76 SeitenCadbury 2010Faraz Sayed100% (2)

- Blair V Bethel School DistDokument7 SeitenBlair V Bethel School DistJoe EskenaziNoch keine Bewertungen

- Cgbe Bba LecturenotesDokument85 SeitenCgbe Bba Lecturenotesr.ghosh2029Noch keine Bewertungen

- Anti Dummy Law of The PhilippineDokument2 SeitenAnti Dummy Law of The PhilippineJeremy Ryan ChuaNoch keine Bewertungen

- Requirements of AEP 2018Dokument1 SeiteRequirements of AEP 2018Allan Ydia100% (1)

- Board Resolution Initial Issuance-Template-1Dokument2 SeitenBoard Resolution Initial Issuance-Template-1David Jay MorNoch keine Bewertungen