Das könnte Ihnen auch gefallen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Computer APPRECIATIONDokument50 SeitenComputer APPRECIATIONSmart AkpabioNoch keine Bewertungen

- Grade 6 ICT NotesDokument101 SeitenGrade 6 ICT NotesAnonymous ZONOvdZqln100% (7)

- Mrs. Sumalathas bank account statementDokument2 SeitenMrs. Sumalathas bank account statementSumalatha VanapalliNoch keine Bewertungen

- To All Promotees CongrtulationsDokument5 SeitenTo All Promotees CongrtulationsambujchinuNoch keine Bewertungen

- The Great Indian Bank Day Light Robbery Chor Machaye Chor ! 5,275 Wilful Defaulters (+ Mallya) Owe Banks Rs 56,621 CroreDokument11 SeitenThe Great Indian Bank Day Light Robbery Chor Machaye Chor ! 5,275 Wilful Defaulters (+ Mallya) Owe Banks Rs 56,621 Croreambujchinu100% (1)

- If History Is A GuideDokument21 SeitenIf History Is A GuideambujchinuNoch keine Bewertungen

- Is History Repeating Itself CHINUDokument7 SeitenIs History Repeating Itself CHINUambujchinuNoch keine Bewertungen

- Dasha Hara - Updation Pension Is Our RightDokument17 SeitenDasha Hara - Updation Pension Is Our Rightambujchinu100% (1)

- Kashmir - Part IIDokument11 SeitenKashmir - Part IIambujchinuNoch keine Bewertungen

- Victory of Good Over EvilDokument13 SeitenVictory of Good Over EvilambujchinuNoch keine Bewertungen

- The Tip of Indian Banking Part I To Part 26my ScribdDokument144 SeitenThe Tip of Indian Banking Part I To Part 26my ScribdambujchinuNoch keine Bewertungen

- Retriement Retirement - The Conclusion of A Long Journey in LifeDokument34 SeitenRetriement Retirement - The Conclusion of A Long Journey in Lifeambujchinu100% (1)

- Updation of Pension - UpdateDokument17 SeitenUpdation of Pension - Updateambujchinu100% (7)

- Notes On Indian Foreign Exchange MarketDokument89 SeitenNotes On Indian Foreign Exchange MarketambujchinuNoch keine Bewertungen

- Kashmir Issue Facts & Myths Part 1 & 2 Kashmir - Part IDokument8 SeitenKashmir Issue Facts & Myths Part 1 & 2 Kashmir - Part IambujchinuNoch keine Bewertungen

- The Tip of Indian Banking - Part 4Dokument424 SeitenThe Tip of Indian Banking - Part 4ambujchinuNoch keine Bewertungen

- The Tip of Indian Banking Part IIDokument66 SeitenThe Tip of Indian Banking Part IIambujchinuNoch keine Bewertungen

- The Tip of Indian Banking - Part3Dokument56 SeitenThe Tip of Indian Banking - Part3ambujchinuNoch keine Bewertungen

- Golden and Noble ThoughtsDokument28 SeitenGolden and Noble Thoughtsambujchinu100% (1)

- LordLord Hanuman and His Worship - Docx Hanuman and His WorshipDokument12 SeitenLordLord Hanuman and His Worship - Docx Hanuman and His WorshipambujchinuNoch keine Bewertungen

- Trade Unions Are All The More Relevant TodayDokument10 SeitenTrade Unions Are All The More Relevant TodayambujchinuNoch keine Bewertungen

- S STRATEGIES FOR EFFECTIVE NPA RECOVERIEStrategies For Effective Npa RecoveriesDokument12 SeitenS STRATEGIES FOR EFFECTIVE NPA RECOVERIEStrategies For Effective Npa RecoveriesambujchinuNoch keine Bewertungen

- Functionalities of A Computer: High SpeedDokument55 SeitenFunctionalities of A Computer: High Speedajay1989sNoch keine Bewertungen

- JBL Full - S. M. Abdul MukitDokument50 SeitenJBL Full - S. M. Abdul MukithabibNoch keine Bewertungen

- TFLTW IZzp 0 Wqja 6 HDokument5 SeitenTFLTW IZzp 0 Wqja 6 HveersainikNoch keine Bewertungen

- Form 5 & 6 Notes PDFDokument264 SeitenForm 5 & 6 Notes PDFYuyun FrancisNoch keine Bewertungen

- Account Statement From 1 Feb 2023 To 1 Aug 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokument3 SeitenAccount Statement From 1 Feb 2023 To 1 Aug 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDina ChatterjeeNoch keine Bewertungen

- Cognitive TPG A760 Two-Color Thermal/Impact Hybrid Printer BrochureDokument2 SeitenCognitive TPG A760 Two-Color Thermal/Impact Hybrid Printer BrochureJohnny BarcodeNoch keine Bewertungen

- Mrs. Kiran Gurjar bank account statementDokument2 SeitenMrs. Kiran Gurjar bank account statementUtkarsh GurjarNoch keine Bewertungen

- Account Statement From 6 Apr 2023 To 22 Jun 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokument11 SeitenAccount Statement From 6 Apr 2023 To 22 Jun 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceNishant Sagar DewanganNoch keine Bewertungen

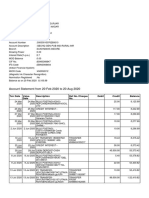

- Account Statement From 1 Apr 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokument14 SeitenAccount Statement From 1 Apr 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceHyper GamingNoch keine Bewertungen

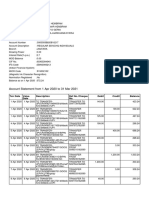

- Account Statement From 1 Mar 2023 To 31 Mar 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokument3 SeitenAccount Statement From 1 Mar 2023 To 31 Mar 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalancePrashant ShuklaNoch keine Bewertungen

- GMJP 4 Puilq 3 WvynoDokument13 SeitenGMJP 4 Puilq 3 Wvynosuresh kumar sainiNoch keine Bewertungen

- Input Devices Explained: Keyboards, Mice, Scanners and MoreDokument34 SeitenInput Devices Explained: Keyboards, Mice, Scanners and MoreBibin JoseNoch keine Bewertungen

- Albert Kahn in The Second Industrial RevolutionDokument25 SeitenAlbert Kahn in The Second Industrial RevolutionlittlewormlwNoch keine Bewertungen

- A CK BWNQ LBsy PWwhyDokument15 SeitenA CK BWNQ LBsy PWwhyPavan Kumãr GannevaramNoch keine Bewertungen

- Mr. Lakkaneni Janardan's bank account statementDokument2 SeitenMr. Lakkaneni Janardan's bank account statementL JanardanaNoch keine Bewertungen

- PneumaticDokument15 SeitenPneumaticDesign ErNoch keine Bewertungen

- Computer QuestDokument10 SeitenComputer QuestXavier MundattilNoch keine Bewertungen

- IT Application in BusinessDokument24 SeitenIT Application in Businesskodnya.meenuNoch keine Bewertungen

- FB6 VV 2 KV SKCQZACdDokument14 SeitenFB6 VV 2 KV SKCQZACdpranablahon42Noch keine Bewertungen

- Computer ConceptDokument127 SeitenComputer ConceptKpsmurugesan KpsmNoch keine Bewertungen

- Customers' Perception Towards Internet Banking in Twin City of OdishaDokument62 SeitenCustomers' Perception Towards Internet Banking in Twin City of OdishaRajesh Kumar Sahoo100% (1)

- Ict Project Mundher Abdu Ali Alyemeni Grade 8-DDokument7 SeitenIct Project Mundher Abdu Ali Alyemeni Grade 8-DMundher AlyemeniNoch keine Bewertungen

- Input and Output DevicesDokument77 SeitenInput and Output DevicesjoanNoch keine Bewertungen

- Full Mock 3 Answer SheetDokument22 SeitenFull Mock 3 Answer SheetlakshmikanthsrNoch keine Bewertungen

- GPPT ZWZG RF 6 JIQq VDokument14 SeitenGPPT ZWZG RF 6 JIQq VKrishna Reddy SvvsNoch keine Bewertungen

- How computers work and their types in 40 charactersDokument30 SeitenHow computers work and their types in 40 charactersVidhya GNoch keine Bewertungen

- UTI - Change of Bank FormDokument2 SeitenUTI - Change of Bank FormSameer apteNoch keine Bewertungen