Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- DTL Sec 10Dokument14 SeitenDTL Sec 10Nikhil KasatNoch keine Bewertungen

- Sale DeedDokument5 SeitenSale DeedNitin GoyalNoch keine Bewertungen

- Types of Stamps and Some Concepts of Stamp DutyDokument5 SeitenTypes of Stamps and Some Concepts of Stamp DutyNikhil Kasat100% (3)

- Derivatives Markets in Interest Rate & Foreign Exchange RateDokument20 SeitenDerivatives Markets in Interest Rate & Foreign Exchange RatehdjfhsjfhwjfNoch keine Bewertungen

- Income Declaration Scheme Rules, 2016: Form 1Dokument9 SeitenIncome Declaration Scheme Rules, 2016: Form 1Nikhil KasatNoch keine Bewertungen

- Hedging With Financial DerivativesDokument30 SeitenHedging With Financial DerivativesNikhil KasatNoch keine Bewertungen

- Some Confusing & Debatable CSR Issues: Learning Series Vol.-I Issue - 2 2015-16Dokument21 SeitenSome Confusing & Debatable CSR Issues: Learning Series Vol.-I Issue - 2 2015-16Nikhil KasatNoch keine Bewertungen

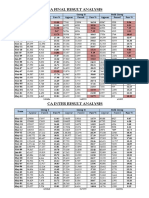

- CA Result AnalysisDokument1 SeiteCA Result AnalysisNikhil KasatNoch keine Bewertungen

- BLack Money RulesDokument23 SeitenBLack Money RulesLive LawNoch keine Bewertungen

- Banca SuranceDokument32 SeitenBanca SuranceNikhil KasatNoch keine Bewertungen

- August Month CompliancesDokument1 SeiteAugust Month CompliancesNikhil KasatNoch keine Bewertungen

- Black Money BillDokument30 SeitenBlack Money BillNikhil KasatNoch keine Bewertungen

- Delhi Dvat Registration InformationDokument4 SeitenDelhi Dvat Registration InformationNikhil KasatNoch keine Bewertungen

- Valuation of InventoriesDokument4 SeitenValuation of InventoriesNikhil KasatNoch keine Bewertungen

- Fees Calculation For Increase in Authorised Share Capital Form SH 7, Only For GujaratDokument10 SeitenFees Calculation For Increase in Authorised Share Capital Form SH 7, Only For GujaratNikhil KasatNoch keine Bewertungen

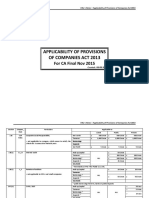

- ApplicabiliTY of ProvisionsDokument3 SeitenApplicabiliTY of ProvisionsNikhil KasatNoch keine Bewertungen

- Directors Report As Per StatusDokument5 SeitenDirectors Report As Per StatusNikhil KasatNoch keine Bewertungen

- List of Indian As Convergence With IfrsDokument1 SeiteList of Indian As Convergence With IfrsNikhil KasatNoch keine Bewertungen

- Agricultural Income: Agricultural Income: - As Per Sec 10 (1) Agricultural Income Earned by TheDokument9 SeitenAgricultural Income: Agricultural Income: - As Per Sec 10 (1) Agricultural Income Earned by TheNikhil KasatNoch keine Bewertungen

- Anf 4dDokument3 SeitenAnf 4dNikhil KasatNoch keine Bewertungen

- Tds On SalariesDokument55 SeitenTds On SalariespunitNoch keine Bewertungen

- Curriculum VitaeDokument13 SeitenCurriculum VitaeNikhil KasatNoch keine Bewertungen

- CA Final Writing Professional Ethics AnswersDokument2 SeitenCA Final Writing Professional Ethics AnswersNikhil KasatNoch keine Bewertungen

- Web Base Timesheet ApplicationDokument4 SeitenWeb Base Timesheet ApplicationNikhil KasatNoch keine Bewertungen

- Importance of ArticleshipDokument6 SeitenImportance of ArticleshipNikhil KasatNoch keine Bewertungen

- Privileges To Small CompaniesDokument2 SeitenPrivileges To Small CompaniesNikhil KasatNoch keine Bewertungen

- C01Dokument23 SeitenC01Silvery DoeNoch keine Bewertungen

- Ind As 2015Dokument2 SeitenInd As 2015Nikhil KasatNoch keine Bewertungen

- Cusoms Valuation MaterialDokument8 SeitenCusoms Valuation MaterialNikhil KasatNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (120)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Ez 14Dokument2 SeitenEz 14yes yesnoNoch keine Bewertungen

- Ia Prompt 12 Theme: Knowledge and Knower "Is Bias Inevitable in The Production of Knowledge?"Dokument2 SeitenIa Prompt 12 Theme: Knowledge and Knower "Is Bias Inevitable in The Production of Knowledge?"Arham ShahNoch keine Bewertungen

- The Message of Malachi 4Dokument7 SeitenThe Message of Malachi 4Ayeah GodloveNoch keine Bewertungen

- Three VignettesDokument3 SeitenThree VignettesIsham IbrahimNoch keine Bewertungen

- IMTG-PGPM Student Manual - Google DocsDokument12 SeitenIMTG-PGPM Student Manual - Google DocsNADExOoGGYNoch keine Bewertungen

- Memorandum1 PDFDokument65 SeitenMemorandum1 PDFGilbert Gabrillo JoyosaNoch keine Bewertungen

- Construction Design Guidelines For Working Within and or Near Occupied BuildingsDokument7 SeitenConstruction Design Guidelines For Working Within and or Near Occupied BuildingsAthirahNoch keine Bewertungen

- The State of Iowa Resists Anna Richter Motion To Expunge Search Warrant and Review Evidence in ChambersDokument259 SeitenThe State of Iowa Resists Anna Richter Motion To Expunge Search Warrant and Review Evidence in ChambersthesacnewsNoch keine Bewertungen

- BÀI TẬP TRẮC NGHIỆM CHUYÊN ĐỀ CÂU BỊ ĐỘNGDokument11 SeitenBÀI TẬP TRẮC NGHIỆM CHUYÊN ĐỀ CÂU BỊ ĐỘNGTuyet VuNoch keine Bewertungen

- If I Was The President of Uganda by Isaac Christopher LubogoDokument69 SeitenIf I Was The President of Uganda by Isaac Christopher LubogolubogoNoch keine Bewertungen

- DAP-1160 A1 Manual 1.20Dokument71 SeitenDAP-1160 A1 Manual 1.20Cecilia FerronNoch keine Bewertungen

- Balkan Languages - Victor FriedmanDokument12 SeitenBalkan Languages - Victor FriedmanBasiol Chulev100% (1)

- Evening Street Review Number 1, Summer 2009Dokument100 SeitenEvening Street Review Number 1, Summer 2009Barbara BergmannNoch keine Bewertungen

- Parent Leaflet Child Death Review v2Dokument24 SeitenParent Leaflet Child Death Review v2InJailOutSoonNoch keine Bewertungen

- Assets Misappropriation in The Malaysian Public AnDokument5 SeitenAssets Misappropriation in The Malaysian Public AnRamadona SimbolonNoch keine Bewertungen

- A Brief Introduction of The OperaDokument3 SeitenA Brief Introduction of The OperaYawen DengNoch keine Bewertungen

- Equilibrium Is A 2002 American: The Flag of Libria. The Four Ts On The Flag Represent The Tetragrammaton CouncilDokument5 SeitenEquilibrium Is A 2002 American: The Flag of Libria. The Four Ts On The Flag Represent The Tetragrammaton CouncilmuhammadismailNoch keine Bewertungen

- Ashish TPR AssignmentDokument12 SeitenAshish TPR Assignmentpriyesh20087913Noch keine Bewertungen

- To The Lighthouse To The SelfDokument36 SeitenTo The Lighthouse To The SelfSubham GuptaNoch keine Bewertungen

- Unit 1 PDFDokument5 SeitenUnit 1 PDFaadhithiyan nsNoch keine Bewertungen

- CSC Leave Form 6 BlankDokument3 SeitenCSC Leave Form 6 BlankARMANDO NABASANoch keine Bewertungen

- Lec 15. National Income Accounting V3 REVISEDDokument33 SeitenLec 15. National Income Accounting V3 REVISEDAbhijeet SinghNoch keine Bewertungen

- NRes1 Work Activity 1 - LEGARTEDokument4 SeitenNRes1 Work Activity 1 - LEGARTEJuliana LegarteNoch keine Bewertungen

- Chapter 06 v0Dokument43 SeitenChapter 06 v0Diệp Diệu ĐồngNoch keine Bewertungen

- Adobe Scan 04 Feb 2024Dokument1 SeiteAdobe Scan 04 Feb 2024biswajitrout13112003Noch keine Bewertungen

- Eve Berlin PDFDokument2 SeitenEve Berlin PDFJeffNoch keine Bewertungen

- Role of The Govt in HealthDokument7 SeitenRole of The Govt in HealthSharad MusaleNoch keine Bewertungen

- IntroductionDokument37 SeitenIntroductionA ChowdhuryNoch keine Bewertungen

- 2 Secuya V de SelmaDokument3 Seiten2 Secuya V de SelmaAndrew GallardoNoch keine Bewertungen

- Customer Service Observation Report ExampleDokument20 SeitenCustomer Service Observation Report ExamplesamNoch keine Bewertungen