Das könnte Ihnen auch gefallen

- Accounting Level 3/series 3 2008 (Code 3012)Dokument15 SeitenAccounting Level 3/series 3 2008 (Code 3012)Hein Linn Kyaw100% (1)

- Accounting Level 3/series 4 2008 (3012)Dokument13 SeitenAccounting Level 3/series 4 2008 (3012)Hein Linn Kyaw100% (1)

- Cost Accounting Level 3/series 4 2008 (3016)Dokument20 SeitenCost Accounting Level 3/series 4 2008 (3016)Hein Linn Kyaw0% (1)

- Book Keeping & Accounts/Series-3-2007 (Code2006)Dokument11 SeitenBook Keeping & Accounts/Series-3-2007 (Code2006)Hein Linn Kyaw100% (3)

- Accounting Level 3/series 2 2008 (Code 3012)Dokument16 SeitenAccounting Level 3/series 2 2008 (Code 3012)Hein Linn Kyaw100% (2)

- Accounting Level 3: LCCI International QualificationsDokument17 SeitenAccounting Level 3: LCCI International QualificationsHein Linn Kyaw100% (4)

- 2008 LCCI Level 2 (2507) Series 3 Model AnswersDokument17 Seiten2008 LCCI Level 2 (2507) Series 3 Model AnswersTracy Chan0% (1)

- Certificate in Management Accounting Level 3/series 3-2009Dokument15 SeitenCertificate in Management Accounting Level 3/series 3-2009Hein Linn Kyaw100% (2)

- Accounting (IAS) Level 3/series 2 2008 (Code 3902)Dokument17 SeitenAccounting (IAS) Level 3/series 2 2008 (Code 3902)Hein Linn Kyaw100% (6)

- Cost Accounting/Series-3-2007 (Code3016)Dokument18 SeitenCost Accounting/Series-3-2007 (Code3016)Hein Linn Kyaw50% (6)

- Cost Accounting Level 3/series 2 2008 (Code 3016)Dokument18 SeitenCost Accounting Level 3/series 2 2008 (Code 3016)Hein Linn Kyaw67% (3)

- 2010 LCCI Level 3 Series 2 Model Answers (Code 3012)Dokument9 Seiten2010 LCCI Level 3 Series 2 Model Answers (Code 3012)mappymappymappyNoch keine Bewertungen

- Cost Accounting Level 3/series 4 2008 (3017)Dokument17 SeitenCost Accounting Level 3/series 4 2008 (3017)Hein Linn Kyaw100% (1)

- Accounting Level 3/ Series 4 2008 (3001)Dokument19 SeitenAccounting Level 3/ Series 4 2008 (3001)Hein Linn Kyaw100% (1)

- Cost Accounting Level 3/series 2-2009Dokument17 SeitenCost Accounting Level 3/series 2-2009Hein Linn Kyaw100% (5)

- Management Accounting/Series-3-2007 (Code3023)Dokument15 SeitenManagement Accounting/Series-3-2007 (Code3023)Hein Linn Kyaw100% (1)

- Cost Accounting/Series-4-2011 (Code3017)Dokument17 SeitenCost Accounting/Series-4-2011 (Code3017)Hein Linn Kyaw100% (2)

- Management Accounting Level 3/series 3 2008 (Code 3023)Dokument14 SeitenManagement Accounting Level 3/series 3 2008 (Code 3023)Hein Linn Kyaw100% (2)

- Certificate in Advanced Business Calculations Level 3/series 3-2009Dokument18 SeitenCertificate in Advanced Business Calculations Level 3/series 3-2009Hein Linn Kyaw100% (10)

- Accounting/Series 2 2007 (Code3001)Dokument16 SeitenAccounting/Series 2 2007 (Code3001)Hein Linn Kyaw100% (3)

- Cost Accounting Level 3/series 3-2009Dokument19 SeitenCost Accounting Level 3/series 3-2009Hein Linn Kyaw100% (2)

- Examiner Report ASE20104 January 2018Dokument22 SeitenExaminer Report ASE20104 January 2018Aung Zaw HtweNoch keine Bewertungen

- ASE20104 Examiner Report - March 2018Dokument20 SeitenASE20104 Examiner Report - March 2018Aung Zaw HtweNoch keine Bewertungen

- LCCI Level 3 Certificate in Accounting ASE20104 ASE20104 Dec-2017Dokument16 SeitenLCCI Level 3 Certificate in Accounting ASE20104 ASE20104 Dec-2017Aung Zaw HtweNoch keine Bewertungen

- Management Accounting: Level 3Dokument18 SeitenManagement Accounting: Level 3Hein Linn KyawNoch keine Bewertungen

- Management Accounting Level 3/series 4 2008 (3023)Dokument14 SeitenManagement Accounting Level 3/series 4 2008 (3023)Hein Linn KyawNoch keine Bewertungen

- Management Accounting/Series-4-2011 (Code3024)Dokument18 SeitenManagement Accounting/Series-4-2011 (Code3024)Hein Linn Kyaw100% (2)

- 2011 LCCI Accounting IAS Level-3 Series 2 (Code 3902)Dokument17 Seiten2011 LCCI Accounting IAS Level-3 Series 2 (Code 3902)Hon Loon Seum100% (6)

- Management Accounting Level 3/series 2 2008 (Code 3023)Dokument17 SeitenManagement Accounting Level 3/series 2 2008 (Code 3023)Hein Linn Kyaw100% (1)

- Accounting (IAS) /series 4 2007 (Code3901)Dokument17 SeitenAccounting (IAS) /series 4 2007 (Code3901)Hein Linn Kyaw0% (1)

- Management Accounting: Level 3Dokument18 SeitenManagement Accounting: Level 3Hein Linn Kyaw100% (3)

- Book Keeping and Accounts Model Answer Series 3 2014Dokument13 SeitenBook Keeping and Accounts Model Answer Series 3 2014cheah_chinNoch keine Bewertungen

- Accounting Level 3/series 4-2009Dokument16 SeitenAccounting Level 3/series 4-2009Hein Linn Kyaw100% (5)

- Management Accounting Level 3/series 2 2008 (Code 3024)Dokument14 SeitenManagement Accounting Level 3/series 2 2008 (Code 3024)Hein Linn Kyaw67% (3)

- Code 2006 Accounting Level 2 2001 Series 2Dokument22 SeitenCode 2006 Accounting Level 2 2001 Series 2apple_syih100% (3)

- Management Accounting Level 3: LCCI International QualificationsDokument17 SeitenManagement Accounting Level 3: LCCI International QualificationsHein Linn Kyaw100% (2)

- Business Statistics Level 3/series 2 2008 (Code 3009)Dokument22 SeitenBusiness Statistics Level 3/series 2 2008 (Code 3009)Hein Linn KyawNoch keine Bewertungen

- Management Accounting Level 3/series 4 2008 (3024)Dokument14 SeitenManagement Accounting Level 3/series 4 2008 (3024)Hein Linn Kyaw50% (2)

- Management Accounting Level 3/series 3 2008 (Code 3024)Dokument12 SeitenManagement Accounting Level 3/series 3 2008 (Code 3024)Hein Linn Kyaw100% (1)

- Cost Accounting Level 3/series 2 2008 (Code 3017)Dokument18 SeitenCost Accounting Level 3/series 2 2008 (Code 3017)Hein Linn Kyaw50% (2)

- Tut 05 SolnDokument4 SeitenTut 05 Soln张婧姝Noch keine Bewertungen

- ACFrOgCQb6wa8qC80YIgWx nX6TZBAv20t36Y6v4IINI tRrVqMKoatALM-RVzRoSlFJ3q DBWgUS7WKpaLaGx4C85SucFsMtbhmcAs-y6GE5Sgvzh4F49OEvpet2gphKgF6qFglhWYwVwKMmoJDokument3 SeitenACFrOgCQb6wa8qC80YIgWx nX6TZBAv20t36Y6v4IINI tRrVqMKoatALM-RVzRoSlFJ3q DBWgUS7WKpaLaGx4C85SucFsMtbhmcAs-y6GE5Sgvzh4F49OEvpet2gphKgF6qFglhWYwVwKMmoJDarlene Bacatan AmancioNoch keine Bewertungen

- Tutorial Questions - Trimester - 2210.Dokument26 SeitenTutorial Questions - Trimester - 2210.premsuwaatiiNoch keine Bewertungen

- Accounting IAS (Malaysia) Model Answers Series 2 2005 Old SyllabusDokument20 SeitenAccounting IAS (Malaysia) Model Answers Series 2 2005 Old SyllabusAung Zaw HtweNoch keine Bewertungen

- Financial Statements ForecastingDokument5 SeitenFinancial Statements ForecastingRimpy Sondh0% (1)

- This Assessment Is in Three Parts, Please Answer All ElementsDokument5 SeitenThis Assessment Is in Three Parts, Please Answer All ElementsAyesha SheheryarNoch keine Bewertungen

- Practice Questions For Ratio Analysis2Dokument13 SeitenPractice Questions For Ratio Analysis2Crazy FootballNoch keine Bewertungen

- HKICPA QP Exam (Module A) Feb2006 Question PaperDokument7 SeitenHKICPA QP Exam (Module A) Feb2006 Question Papercynthia tsuiNoch keine Bewertungen

- CeresDokument9 SeitenCeresDebangana BaruahNoch keine Bewertungen

- IMT CeresDokument7 SeitenIMT Ceresraman.joshi751Noch keine Bewertungen

- SudhakarDokument6 SeitenSudhakarSudhakar Keshav100% (1)

- FIn 201 AnswersDokument5 SeitenFIn 201 AnswersShahinNoch keine Bewertungen

- Individual/Group Assignments (Optional) Assignment 1Dokument3 SeitenIndividual/Group Assignments (Optional) Assignment 1Robin GhotiaNoch keine Bewertungen

- Part A Answer ALL Questions.: Confidential AC/APR 2010/FAR360 2Dokument4 SeitenPart A Answer ALL Questions.: Confidential AC/APR 2010/FAR360 2Syazliana KasimNoch keine Bewertungen

- Quiz MKDokument3 SeitenQuiz MKvano aldiNoch keine Bewertungen

- IMT CeresDokument11 SeitenIMT CeresShivam GuptaNoch keine Bewertungen

- Chapter 8Dokument6 SeitenChapter 8ديـنـا عادلNoch keine Bewertungen

- Aifs I SMNR QDokument4 SeitenAifs I SMNR QChapo madzivaNoch keine Bewertungen

- Financial Accounting Cat 1 JonathanDokument14 SeitenFinancial Accounting Cat 1 JonathanjonathanNoch keine Bewertungen

- Heriot-Watt University Accounting - December 2016 Section II Case Studies Case Study 1Dokument6 SeitenHeriot-Watt University Accounting - December 2016 Section II Case Studies Case Study 1sanosyNoch keine Bewertungen

- Order Summary PDFDokument4 SeitenOrder Summary PDFAlyaa Syafika NadiraNoch keine Bewertungen

- Avaya Vs Cisco ComparisonDokument29 SeitenAvaya Vs Cisco ComparisonkaleemNoch keine Bewertungen

- (2023-06) Quotation MGD - Maslaha NiqabDokument3 Seiten(2023-06) Quotation MGD - Maslaha NiqabRiva RinaldyNoch keine Bewertungen

- Refer To The Exhibit.: Ape3: Key Server - Customer 2 Ces: Group MembersDokument57 SeitenRefer To The Exhibit.: Ape3: Key Server - Customer 2 Ces: Group Membersdany sayedNoch keine Bewertungen

- Quiz - Chapter 1 - The Accounting ProcessDokument4 SeitenQuiz - Chapter 1 - The Accounting ProcessJoseph Docto100% (2)

- Market PlaceDokument2 SeitenMarket PlaceKurumiNoch keine Bewertungen

- System-Generated Excel File For January 2022 SalesDokument120 SeitenSystem-Generated Excel File For January 2022 SalesGiomar BasalNoch keine Bewertungen

- Tourism Answers PDFDokument41 SeitenTourism Answers PDFĐạt VươngNoch keine Bewertungen

- 1554798217883X3i7uxTcJ6ABw7aK PDFDokument3 Seiten1554798217883X3i7uxTcJ6ABw7aK PDFAkshaya pNoch keine Bewertungen

- User's Manual: WHG & HSG Series Secure WLAN Controller / Wireless Hotspot GatewayDokument374 SeitenUser's Manual: WHG & HSG Series Secure WLAN Controller / Wireless Hotspot GatewayKleng KlengNoch keine Bewertungen

- Performance Audit Report of The Auditor-General Implementation of National Optic Fibre Backbone Infrastructure Project (NOFBI)Dokument52 SeitenPerformance Audit Report of The Auditor-General Implementation of National Optic Fibre Backbone Infrastructure Project (NOFBI)Marvin nduko bosireNoch keine Bewertungen

- PB Fees and ChargesDokument32 SeitenPB Fees and ChargesechipbkNoch keine Bewertungen

- Resume Kai-Uwe ..Dokument5 SeitenResume Kai-Uwe ..iqbal1439988Noch keine Bewertungen

- State of Market Feb 2008Dokument42 SeitenState of Market Feb 2008azharaqNoch keine Bewertungen

- Direct and Indirect Distribution Channels of Airline Products and Services An OverviewDokument29 SeitenDirect and Indirect Distribution Channels of Airline Products and Services An OverviewShijoNoch keine Bewertungen

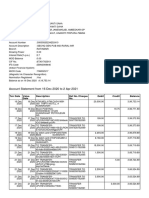

- Account Statement From 16 Dec 2020 To 2 Apr 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokument7 SeitenAccount Statement From 16 Dec 2020 To 2 Apr 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceSuhan SahaNoch keine Bewertungen

- Topic 1 Philippine Financial SystemDokument19 SeitenTopic 1 Philippine Financial SystemJulie Anne DanteNoch keine Bewertungen

- 27-Full Manuscript-489-1-10-20220328Dokument7 Seiten27-Full Manuscript-489-1-10-20220328TychiqueNoch keine Bewertungen

- Blockchain SyllabusDokument2 SeitenBlockchain SyllabusM B ReddyNoch keine Bewertungen

- Telemedicine According To WHO, Telemedicine Is Defined Advantages of Telemedicine Model of Telehealth SystemDokument2 SeitenTelemedicine According To WHO, Telemedicine Is Defined Advantages of Telemedicine Model of Telehealth SystemAmanda ScarletNoch keine Bewertungen

- River Jordan Laundry FSDokument6 SeitenRiver Jordan Laundry FSFiel Marie SateraNoch keine Bewertungen

- HDFC Life Guaranteed Income Insurance ( 8 - 16 )Dokument2 SeitenHDFC Life Guaranteed Income Insurance ( 8 - 16 )AbhishekNoch keine Bewertungen

- SAP DSN Value Prop SlidesDokument8 SeitenSAP DSN Value Prop Slidessmail mahjoubiNoch keine Bewertungen

- 01EB7ADokument1 Seite01EB7ALuka MilojevicNoch keine Bewertungen

- GRC RulesetDokument6 SeitenGRC RulesetDAVIDNoch keine Bewertungen

- Nevada Contracts of InsuranceDokument23 SeitenNevada Contracts of InsurancecrosscomplaintNoch keine Bewertungen

- The Revenue Cycle: Sales To Cash CollectionsDokument12 SeitenThe Revenue Cycle: Sales To Cash CollectionsChrohimeNoch keine Bewertungen

- PartnershipDokument10 SeitenPartnershipJasmine Marie Ng Cheong50% (2)

- Bank Management System: ModulesDokument2 SeitenBank Management System: ModulesSumod SundarNoch keine Bewertungen

- Dbs Group Fact Sheet: Corporate InformationDokument10 SeitenDbs Group Fact Sheet: Corporate InformationleekosalNoch keine Bewertungen