Das könnte Ihnen auch gefallen

- Corporate Social Responsibility in IndiaDokument5 SeitenCorporate Social Responsibility in IndiaAnonymous CwJeBCAXpNoch keine Bewertungen

- Green Products A Complete Guide - 2020 EditionVon EverandGreen Products A Complete Guide - 2020 EditionBewertung: 5 von 5 Sternen5/5 (1)

- Project Report: New Trends in CSR and Its Advantage Towards SocietyDokument31 SeitenProject Report: New Trends in CSR and Its Advantage Towards SocietyHarsh Vijay0% (1)

- Going for Broke: Insolvency Tools to Support Cross-Border Asset Recovery in Corruption CasesVon EverandGoing for Broke: Insolvency Tools to Support Cross-Border Asset Recovery in Corruption CasesNoch keine Bewertungen

- A Study of Corporate Social Responsibility in Indian Organization: An-IntrospectionDokument11 SeitenA Study of Corporate Social Responsibility in Indian Organization: An-IntrospectionSamrat ChowdhuryNoch keine Bewertungen

- Tata Motors CSR positively impacts communitiesDokument25 SeitenTata Motors CSR positively impacts communitiesjasdeepNoch keine Bewertungen

- CSR Perspectives and BenefitsDokument7 SeitenCSR Perspectives and BenefitsNageeta BaiNoch keine Bewertungen

- Corporate Social Responsibility in IndiaDokument17 SeitenCorporate Social Responsibility in Indiarefayet.khanNoch keine Bewertungen

- Role of Corporate Social Responsibilty (CSR)Dokument29 SeitenRole of Corporate Social Responsibilty (CSR)Akash RaiNoch keine Bewertungen

- Corporate Social Responsibility in IndiaDokument22 SeitenCorporate Social Responsibility in IndiaVijiSriragghavan100% (1)

- ProjectDokument19 SeitenProjectrashmi sahu100% (1)

- CSR in India GuideDokument22 SeitenCSR in India GuideankitaNoch keine Bewertungen

- Corporate Governance ProjectDokument13 SeitenCorporate Governance ProjectDhruv AghiNoch keine Bewertungen

- Lee vs. Lee Air Framing LTD 1961Dokument9 SeitenLee vs. Lee Air Framing LTD 1961Rajat Kaushik100% (1)

- Chapter Evolution of CSR in India FinalDokument19 SeitenChapter Evolution of CSR in India Finalsadhubaba100Noch keine Bewertungen

- Introduction To Corporate Social ResponsibilityDokument46 SeitenIntroduction To Corporate Social Responsibilityikjot5430Noch keine Bewertungen

- Corporate Governance Project On Gas Authority India Limited (GAIL)Dokument3 SeitenCorporate Governance Project On Gas Authority India Limited (GAIL)TinaPSNoch keine Bewertungen

- Corporate Governance Assignment On CSR by Mayank RajpootDokument13 SeitenCorporate Governance Assignment On CSR by Mayank RajpootMayank Rajpoot100% (1)

- Central University of South Bihar Project Analyzes India and USA Capital MarketsDokument21 SeitenCentral University of South Bihar Project Analyzes India and USA Capital MarketsRajeev RajNoch keine Bewertungen

- Literature On CSRDokument23 SeitenLiterature On CSRrehanbtariqNoch keine Bewertungen

- Critical Analysis of Corporate Social Responsibility by Top Organizations For CSR & Sustainability in IndiaDokument56 SeitenCritical Analysis of Corporate Social Responsibility by Top Organizations For CSR & Sustainability in Indiaanon_1081786300% (1)

- Corporate Social ResponsibilityDokument18 SeitenCorporate Social ResponsibilityPrashant RampuriaNoch keine Bewertungen

- Hero HondaDokument30 SeitenHero HondaMathews IndiaNoch keine Bewertungen

- Infosys CSR ReportDokument27 SeitenInfosys CSR ReportSaday Chhabra100% (1)

- CSR Study of Janavhi Charitable NGODokument32 SeitenCSR Study of Janavhi Charitable NGOpooja pawarNoch keine Bewertungen

- Corporate Social Responsibility (CSR) To Corporate Environmental Responsibility (CER) :an India PerspectiveDokument14 SeitenCorporate Social Responsibility (CSR) To Corporate Environmental Responsibility (CER) :an India PerspectiveLAW MANTRA100% (1)

- Project ReportDokument49 SeitenProject ReportShivani Bansal50% (4)

- Synopsis PDFDokument22 SeitenSynopsis PDFShivin Sancheti100% (1)

- CSR ProjectDokument25 SeitenCSR ProjectRAHUL UKEYNoch keine Bewertungen

- Recent Trends in CSR in IndiaDokument50 SeitenRecent Trends in CSR in IndiaFlorence BidariNoch keine Bewertungen

- Corporate Social Responsibility in IndiaDokument24 SeitenCorporate Social Responsibility in IndiaHarman PreetNoch keine Bewertungen

- Critical Analysis of CSRDokument14 SeitenCritical Analysis of CSRsaif aliNoch keine Bewertungen

- Dr. Ram Manohar Lohia National Law University, LucknowDokument18 SeitenDr. Ram Manohar Lohia National Law University, LucknowAbhishek PratapNoch keine Bewertungen

- Role of institutional investors in improving Indian corporate governanceDokument47 SeitenRole of institutional investors in improving Indian corporate governanceSaritaMeenaNoch keine Bewertungen

- Corporate Social Responsibility in IndiaDokument22 SeitenCorporate Social Responsibility in IndiaFaizKazi140% (1)

- India CSR Reporting Survey 2018Dokument80 SeitenIndia CSR Reporting Survey 2018Teres SajeevNoch keine Bewertungen

- Corporate Governance in Public Sector Undertakings in India: Project Report OnDokument43 SeitenCorporate Governance in Public Sector Undertakings in India: Project Report OnAdarsh JosephNoch keine Bewertungen

- Tata Institute of Social ScienceDokument45 SeitenTata Institute of Social ScienceWaseem KhanNoch keine Bewertungen

- Corporate Social Responsibility - A Case Study of Microsoft Corporation (India) Pvt. LTDDokument16 SeitenCorporate Social Responsibility - A Case Study of Microsoft Corporation (India) Pvt. LTDGaurav ChauhanNoch keine Bewertungen

- Evolution of Corporate Social Responsibility in India - Wikipedia, The Free EncyclopediaDokument4 SeitenEvolution of Corporate Social Responsibility in India - Wikipedia, The Free Encyclopediapoojamud100% (1)

- Blackbook-Csr in Insurance SectorsDokument43 SeitenBlackbook-Csr in Insurance Sectorsforum67% (3)

- Project Corporate Governance 6semDokument71 SeitenProject Corporate Governance 6semRohit RaiNoch keine Bewertungen

- Assignment Report (2) : Title-Corporate Social ResponsibilityDokument17 SeitenAssignment Report (2) : Title-Corporate Social ResponsibilitykanikaNoch keine Bewertungen

- Social Relevance Project-2Dokument62 SeitenSocial Relevance Project-2DivyeshNoch keine Bewertungen

- Corporate Social Responsibility: An Analysis of Top Performers in IndiaDokument19 SeitenCorporate Social Responsibility: An Analysis of Top Performers in IndiaZaid AnsariNoch keine Bewertungen

- Development of Corporate Social Responsibility in Indian Family BusinessDokument27 SeitenDevelopment of Corporate Social Responsibility in Indian Family Businesskandarp_singh_1Noch keine Bewertungen

- Project Work On: Object ClauseDokument19 SeitenProject Work On: Object ClauseShashi RanjanNoch keine Bewertungen

- A Project On Labour in Unorganised SectorDokument17 SeitenA Project On Labour in Unorganised SectorRishabh SinghNoch keine Bewertungen

- Green MarketingDokument73 SeitenGreen Marketingnitin0010Noch keine Bewertungen

- Corporate Social Responsibility and Stakeholder Approach A Conceptual ReviewDokument26 SeitenCorporate Social Responsibility and Stakeholder Approach A Conceptual ReviewMeenakshi ChumunNoch keine Bewertungen

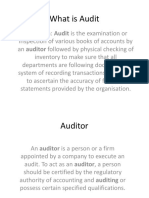

- What is an AuditDokument8 SeitenWhat is an AuditRahul KhandelwalNoch keine Bewertungen

- Yes Bank Corp Govn.Dokument24 SeitenYes Bank Corp Govn.choco_pie_952Noch keine Bewertungen

- Corporate Social ResponsibilityDokument18 SeitenCorporate Social ResponsibilityAravinda A100% (5)

- Corporate Social ResponsibilityDokument8 SeitenCorporate Social Responsibilitysanjay shamnaniNoch keine Bewertungen

- Corporate Law ProjectDokument12 SeitenCorporate Law ProjectAmbir KhanNoch keine Bewertungen

- What Is Corporate Social Responsibility or CSRDokument3 SeitenWhat Is Corporate Social Responsibility or CSRAbrar HussainNoch keine Bewertungen

- CSR - VarshiniDokument37 SeitenCSR - VarshinivarshiniNoch keine Bewertungen

- Final Project of CSR Activity of Tata Capital-ShubhamDokument70 SeitenFinal Project of CSR Activity of Tata Capital-ShubhamShubham JadhavNoch keine Bewertungen

- Gautam & Singh, 2010Dokument16 SeitenGautam & Singh, 2010Preeti SadhwaniNoch keine Bewertungen

- CAIIB Bank Financial Management Sample QuestionsDokument290 SeitenCAIIB Bank Financial Management Sample QuestionsVarun Shastry100% (3)

- Module D-Balance Sheet Management PDFDokument14 SeitenModule D-Balance Sheet Management PDFvarun_bathulaNoch keine Bewertungen

- Chapter 1: The Investment Industry: A Top Down ViewDokument18 SeitenChapter 1: The Investment Industry: A Top Down ViewApratim BhaskarNoch keine Bewertungen

- Six HatsDokument8 SeitenSix Hatsapi-26046446Noch keine Bewertungen

- 2017 FRM StudyChangesDokument12 Seiten2017 FRM StudyChangesSriharsha ReddyNoch keine Bewertungen

- Info Sec Awareness@Dec7th12-FinalDokument53 SeitenInfo Sec Awareness@Dec7th12-FinalApratim BhaskarNoch keine Bewertungen

- Thinking Out of The BoxDokument3 SeitenThinking Out of The Boxapi-3767746Noch keine Bewertungen

- January 2016Dokument80 SeitenJanuary 2016Apratim BhaskarNoch keine Bewertungen

- FMfinancial Statement AnalysisDokument29 SeitenFMfinancial Statement AnalysisApratim BhaskarNoch keine Bewertungen

- CAIIB Bank Financial Management Sample QuestionsDokument290 SeitenCAIIB Bank Financial Management Sample QuestionsVarun Shastry100% (3)

- Bond Holders ChecklistDokument1 SeiteBond Holders ChecklistApratim BhaskarNoch keine Bewertungen

- Inference Practice Questions and Solutions PDFDokument29 SeitenInference Practice Questions and Solutions PDFApratim BhaskarNoch keine Bewertungen

- View Signatory Details for BHARAT AND BHUVAN EXIM PRIVATE LIMITEDDokument1 SeiteView Signatory Details for BHARAT AND BHUVAN EXIM PRIVATE LIMITEDApratim BhaskarNoch keine Bewertungen

- FMfinancial Statement AnalysisDokument29 SeitenFMfinancial Statement AnalysisApratim BhaskarNoch keine Bewertungen

- Sample RLDokument2 SeitenSample RLApratim BhaskarNoch keine Bewertungen

- FMfinancial Statement AnalysisDokument29 SeitenFMfinancial Statement AnalysisApratim BhaskarNoch keine Bewertungen

- Bidding For Representative Allocations For Display AdvertisingDokument12 SeitenBidding For Representative Allocations For Display AdvertisingApratim BhaskarNoch keine Bewertungen

- Annexure BDokument1 SeiteAnnexure BDEEPAK2502Noch keine Bewertungen

- FMfinancial Statement AnalysisDokument29 SeitenFMfinancial Statement AnalysisApratim BhaskarNoch keine Bewertungen

- Cferm Prospectus 2013-14 RevisedDokument13 SeitenCferm Prospectus 2013-14 RevisedApratim BhaskarNoch keine Bewertungen

- Bond Holders ChecklistDokument1 SeiteBond Holders ChecklistApratim BhaskarNoch keine Bewertungen

- Current Issues in Quant Market Investment OperationsDokument1 SeiteCurrent Issues in Quant Market Investment OperationsApratim BhaskarNoch keine Bewertungen

- Bidding For Representative Allocations For Display AdvertisingDokument12 SeitenBidding For Representative Allocations For Display AdvertisingApratim BhaskarNoch keine Bewertungen

- Bond Holders ChecklistDokument1 SeiteBond Holders ChecklistApratim BhaskarNoch keine Bewertungen

- LeverageDokument3 SeitenLeverageloversheritageNoch keine Bewertungen

- UntitledDokument1 SeiteUntitledApratim BhaskarNoch keine Bewertungen

- C&C Projects bonds and debenturesDokument462 SeitenC&C Projects bonds and debenturesApratim BhaskarNoch keine Bewertungen

- Adapting CRM Processes With Enterprise SOADokument8 SeitenAdapting CRM Processes With Enterprise SOAApratim BhaskarNoch keine Bewertungen

- Basics of Share Market TradingDokument47 SeitenBasics of Share Market Tradingavijitcu2007Noch keine Bewertungen

- Kalyanamastu Pathakam - Guidelines - Final - 11jan19Dokument3 SeitenKalyanamastu Pathakam - Guidelines - Final - 11jan19KrishnaveniNoch keine Bewertungen

- Complementary Questionnaire SampleDokument4 SeitenComplementary Questionnaire SampleOyelakin Gbolahan PearlNoch keine Bewertungen

- Module in Rinconada Literatur. RevisedDokument14 SeitenModule in Rinconada Literatur. RevisedchongperryboyNoch keine Bewertungen

- Toronto's Segregated Immigrant Population, 2016Dokument1 SeiteToronto's Segregated Immigrant Population, 2016Toronto StarNoch keine Bewertungen

- LGBT Rights FAQ Sheet Explains Key Terms and IssuesDokument2 SeitenLGBT Rights FAQ Sheet Explains Key Terms and Issuesnurul ulfaNoch keine Bewertungen

- Open Letter Exposes Sibling Abuse EnablingDokument4 SeitenOpen Letter Exposes Sibling Abuse EnablingJohn Bowen BrownNoch keine Bewertungen

- Succession (Homework) - Matrix of LegitimeDokument4 SeitenSuccession (Homework) - Matrix of Legitimejsanbusta0% (1)

- Zainab RISBDokument8 SeitenZainab RISBZe Sheikh50% (4)

- Monique Bazile MSW Pis2013Dokument4 SeitenMonique Bazile MSW Pis2013api-251022973Noch keine Bewertungen

- Hortatory Exposition TextDokument1 SeiteHortatory Exposition TextfirasyafriyaniNoch keine Bewertungen

- Slave ContractDokument3 SeitenSlave ContractMANU SHANKAR75% (4)

- Enloe High School: Administrative PresentationDokument17 SeitenEnloe High School: Administrative PresentationSarita ShawNoch keine Bewertungen

- Sample Trial Memo Psychological IncapacityDokument7 SeitenSample Trial Memo Psychological IncapacityEdgar Joshua TimbangNoch keine Bewertungen

- 2 Parental ResponsibilityDokument18 Seiten2 Parental ResponsibilityczarinaNoch keine Bewertungen

- Gender at SexualityDokument56 SeitenGender at SexualityLaura Andrea Dela CruzNoch keine Bewertungen

- Maine's Child Abuse Prevention ProgramsDokument3 SeitenMaine's Child Abuse Prevention ProgramsNEWS CENTER MaineNoch keine Bewertungen

- REHABILITATIONDokument27 SeitenREHABILITATIONBiswajeet MaharanaNoch keine Bewertungen

- Timeline Aus MigrationDokument1 SeiteTimeline Aus Migrationapi-282545429Noch keine Bewertungen

- Empowerment of Self-Help Group Members: Dr. K Kavitha Maheswari, C PriyankaDokument3 SeitenEmpowerment of Self-Help Group Members: Dr. K Kavitha Maheswari, C PriyankaAnonymous nveZK61CNoch keine Bewertungen

- Workplace BullyingDokument4 SeitenWorkplace BullyingChristina PerezNoch keine Bewertungen

- Hotter WomenDokument73 SeitenHotter WomenXera Buraco100% (1)

- The Science of Getting Love by Wallace WattlesDokument12 SeitenThe Science of Getting Love by Wallace Wattlesaktoja100% (1)

- Brand Identity Ben and JerryDokument44 SeitenBrand Identity Ben and Jerryjamiebowerman100% (1)

- Berlin, Ira - Reseña, Ira Berlin Many Thousands GoneDokument3 SeitenBerlin, Ira - Reseña, Ira Berlin Many Thousands GoneMontserrat A. MarfullNoch keine Bewertungen

- Female Body and Sexuality in SalmaDokument10 SeitenFemale Body and Sexuality in Salmaanon_972175365Noch keine Bewertungen

- The New EnquiryDokument80 SeitenThe New EnquiryEloisa FranchiNoch keine Bewertungen

- Dast20 PDFDokument3 SeitenDast20 PDFMarchnuelNoch keine Bewertungen

- Manuvo Literatures 101Dokument14 SeitenManuvo Literatures 101angelito peraNoch keine Bewertungen

- As Virtual Theatre: Performing Gender, Race, and Class in 21st-Century ColombiaDokument34 SeitenAs Virtual Theatre: Performing Gender, Race, and Class in 21st-Century ColombiaDiego IgnacioNoch keine Bewertungen

- Child Wellbeing in Kachin StateDokument4 SeitenChild Wellbeing in Kachin Statemarcmyomyint1663100% (1)

- Obviously Awesome: How to Nail Product Positioning so Customers Get It, Buy It, Love ItVon EverandObviously Awesome: How to Nail Product Positioning so Customers Get It, Buy It, Love ItBewertung: 4.5 von 5 Sternen4.5/5 (150)

- $100M Leads: How to Get Strangers to Want to Buy Your StuffVon Everand$100M Leads: How to Get Strangers to Want to Buy Your StuffBewertung: 5 von 5 Sternen5/5 (11)

- Dealers of Lightning: Xerox PARC and the Dawn of the Computer AgeVon EverandDealers of Lightning: Xerox PARC and the Dawn of the Computer AgeBewertung: 4 von 5 Sternen4/5 (88)

- Fascinate: How to Make Your Brand Impossible to ResistVon EverandFascinate: How to Make Your Brand Impossible to ResistBewertung: 5 von 5 Sternen5/5 (1)

- How to Get a Meeting with Anyone: The Untapped Selling Power of Contact MarketingVon EverandHow to Get a Meeting with Anyone: The Untapped Selling Power of Contact MarketingBewertung: 4.5 von 5 Sternen4.5/5 (28)

- Yes!: 50 Scientifically Proven Ways to Be PersuasiveVon EverandYes!: 50 Scientifically Proven Ways to Be PersuasiveBewertung: 4 von 5 Sternen4/5 (153)

- Ca$hvertising: How to Use More than 100 Secrets of Ad-Agency Psychology to Make Big Money Selling Anything to AnyoneVon EverandCa$hvertising: How to Use More than 100 Secrets of Ad-Agency Psychology to Make Big Money Selling Anything to AnyoneBewertung: 5 von 5 Sternen5/5 (114)

- ChatGPT Millionaire 2024 - Bot-Driven Side Hustles, Prompt Engineering Shortcut Secrets, and Automated Income Streams that Print Money While You Sleep. The Ultimate Beginner’s Guide for AI BusinessVon EverandChatGPT Millionaire 2024 - Bot-Driven Side Hustles, Prompt Engineering Shortcut Secrets, and Automated Income Streams that Print Money While You Sleep. The Ultimate Beginner’s Guide for AI BusinessNoch keine Bewertungen

- $100M Offers: How to Make Offers So Good People Feel Stupid Saying NoVon Everand$100M Offers: How to Make Offers So Good People Feel Stupid Saying NoBewertung: 5 von 5 Sternen5/5 (20)

- The Tipping Point by Malcolm Gladwell - Book Summary: How Little Things Can Make a Big DifferenceVon EverandThe Tipping Point by Malcolm Gladwell - Book Summary: How Little Things Can Make a Big DifferenceBewertung: 4.5 von 5 Sternen4.5/5 (120)

- Pre-Suasion: Channeling Attention for ChangeVon EverandPre-Suasion: Channeling Attention for ChangeBewertung: 4.5 von 5 Sternen4.5/5 (276)

- Scientific Advertising: "Master of Effective Advertising"Von EverandScientific Advertising: "Master of Effective Advertising"Bewertung: 4.5 von 5 Sternen4.5/5 (163)

- Launch: An Internet Millionaire's Secret Formula to Sell Almost Anything Online, Build a Business You Love, and Live the Life of Your DreamsVon EverandLaunch: An Internet Millionaire's Secret Formula to Sell Almost Anything Online, Build a Business You Love, and Live the Life of Your DreamsBewertung: 4.5 von 5 Sternen4.5/5 (123)

- Jab, Jab, Jab, Right Hook: How to Tell Your Story in a Noisy Social WorldVon EverandJab, Jab, Jab, Right Hook: How to Tell Your Story in a Noisy Social WorldBewertung: 4.5 von 5 Sternen4.5/5 (18)

- Summary: Range: Why Generalists Triumph in a Specialized World by David Epstein: Key Takeaways, Summary & Analysis IncludedVon EverandSummary: Range: Why Generalists Triumph in a Specialized World by David Epstein: Key Takeaways, Summary & Analysis IncludedBewertung: 4.5 von 5 Sternen4.5/5 (6)

- Fanatical Prospecting: The Ultimate Guide to Opening Sales Conversations and Filling the Pipeline by Leveraging Social Selling, Telephone, Email, Text, and Cold CallingVon EverandFanatical Prospecting: The Ultimate Guide to Opening Sales Conversations and Filling the Pipeline by Leveraging Social Selling, Telephone, Email, Text, and Cold CallingBewertung: 4 von 5 Sternen4/5 (12)

- Summary: Traction: Get a Grip on Your Business: by Gino Wickman: Key Takeaways, Summary, and AnalysisVon EverandSummary: Traction: Get a Grip on Your Business: by Gino Wickman: Key Takeaways, Summary, and AnalysisBewertung: 5 von 5 Sternen5/5 (10)

- Permission Marketing: Turning Strangers into Friends, and Friends into CustomersVon EverandPermission Marketing: Turning Strangers into Friends, and Friends into CustomersBewertung: 4 von 5 Sternen4/5 (329)

- Summary: Dotcom Secrets: The Underground Playbook for Growing Your Company Online with Sales Funnels by Russell Brunson: Key Takeaways, Summary & Analysis IncludedVon EverandSummary: Dotcom Secrets: The Underground Playbook for Growing Your Company Online with Sales Funnels by Russell Brunson: Key Takeaways, Summary & Analysis IncludedBewertung: 5 von 5 Sternen5/5 (1)

- Understanding Digital Marketing: Marketing Strategies for Engaging the Digital GenerationVon EverandUnderstanding Digital Marketing: Marketing Strategies for Engaging the Digital GenerationBewertung: 4 von 5 Sternen4/5 (22)

- How to Prospect, Sell and Build Your Network Marketing Business with StoriesVon EverandHow to Prospect, Sell and Build Your Network Marketing Business with StoriesBewertung: 5 von 5 Sternen5/5 (21)

- Marketing Made Simple: A Step-by-Step StoryBrand Guide for Any BusinessVon EverandMarketing Made Simple: A Step-by-Step StoryBrand Guide for Any BusinessBewertung: 5 von 5 Sternen5/5 (203)

- The Catalyst: How to Change Anyone's MindVon EverandThe Catalyst: How to Change Anyone's MindBewertung: 4.5 von 5 Sternen4.5/5 (272)

- Visibility Marketing: The No-Holds-Barred Truth About What It Takes to Grab Attention, Build Your Brand, and Win New BusinessVon EverandVisibility Marketing: The No-Holds-Barred Truth About What It Takes to Grab Attention, Build Your Brand, and Win New BusinessBewertung: 4.5 von 5 Sternen4.5/5 (7)

- Summary: $100M Leads: How to Get Strangers to Want to Buy Your Stuff by Alex Hormozi: Key Takeaways, Summary & Analysis IncludedVon EverandSummary: $100M Leads: How to Get Strangers to Want to Buy Your Stuff by Alex Hormozi: Key Takeaways, Summary & Analysis IncludedBewertung: 3 von 5 Sternen3/5 (6)

- How to Read People: The Complete Psychology Guide to Analyzing People, Reading Body Language, and Persuading, Manipulating and Understanding How to Influence Human BehaviorVon EverandHow to Read People: The Complete Psychology Guide to Analyzing People, Reading Body Language, and Persuading, Manipulating and Understanding How to Influence Human BehaviorBewertung: 4.5 von 5 Sternen4.5/5 (32)

- Storytelling: A Guide on How to Tell a Story with Storytelling Techniques and Storytelling SecretsVon EverandStorytelling: A Guide on How to Tell a Story with Storytelling Techniques and Storytelling SecretsBewertung: 4.5 von 5 Sternen4.5/5 (71)

- The Myth of the Rational Market: A History of Risk, Reward, and Delusion on Wall StreetVon EverandThe Myth of the Rational Market: A History of Risk, Reward, and Delusion on Wall StreetNoch keine Bewertungen

- Crossing the Chasm: Marketing and Selling Disruptive Products to Mainstream Customers(3rd Edition)Von EverandCrossing the Chasm: Marketing and Selling Disruptive Products to Mainstream Customers(3rd Edition)Bewertung: 5 von 5 Sternen5/5 (3)