Das könnte Ihnen auch gefallen

- STRATEGIC MANAGEMENT FOR COMPETITIVE ADVANTAGE - Part CDokument12 SeitenSTRATEGIC MANAGEMENT FOR COMPETITIVE ADVANTAGE - Part CShaji Viswanathan. Mcom, MBA (U.K)Noch keine Bewertungen

- Risk & Procure Management ExampleDokument27 SeitenRisk & Procure Management ExampleShaji Viswanathan. Mcom, MBA (U.K)Noch keine Bewertungen

- Risk & Procure ManagementDokument26 SeitenRisk & Procure ManagementShaji Viswanathan. Mcom, MBA (U.K)100% (1)

- Risk and Procurement Management 1Dokument28 SeitenRisk and Procurement Management 1Shaji Viswanathan. Mcom, MBA (U.K)100% (1)

- Finance Management and Control-FinalDokument30 SeitenFinance Management and Control-FinalShaji Viswanathan. Mcom, MBA (U.K)Noch keine Bewertungen

- Business Strategy "Telecommunication Sector (Uk) "Dokument20 SeitenBusiness Strategy "Telecommunication Sector (Uk) "Shaji Viswanathan. Mcom, MBA (U.K)Noch keine Bewertungen

- Strategy Management For Competitive AdvantageDokument29 SeitenStrategy Management For Competitive AdvantageShaji Viswanathan. Mcom, MBA (U.K)Noch keine Bewertungen

- Develop Individual Group OrganizationDokument24 SeitenDevelop Individual Group OrganizationShaji Viswanathan. Mcom, MBA (U.K)100% (2)

- BUSINESS STRATEGY (Re-Structured Strategic Plan of ASDA)Dokument33 SeitenBUSINESS STRATEGY (Re-Structured Strategic Plan of ASDA)Shaji Viswanathan. Mcom, MBA (U.K)Noch keine Bewertungen

- How Many Aware That There Is No Cure For Aids?Dokument13 SeitenHow Many Aware That There Is No Cure For Aids?Shaji Viswanathan. Mcom, MBA (U.K)Noch keine Bewertungen

- How Hiv Awareness Advertising Impact On Social Construction?Dokument14 SeitenHow Hiv Awareness Advertising Impact On Social Construction?Shaji Viswanathan. Mcom, MBA (U.K)Noch keine Bewertungen

- Obesity - Prevention and Precaution in UkDokument17 SeitenObesity - Prevention and Precaution in UkShaji Viswanathan. Mcom, MBA (U.K)Noch keine Bewertungen

- An Evidenced Base Case Study Report On HIV/AIDS To Invest and Prevent in UKDokument19 SeitenAn Evidenced Base Case Study Report On HIV/AIDS To Invest and Prevent in UKShaji Viswanathan. Mcom, MBA (U.K)Noch keine Bewertungen

- Loyalty Progams & Impact On Customer RetentionDokument48 SeitenLoyalty Progams & Impact On Customer RetentionShaji Viswanathan. Mcom, MBA (U.K)100% (1)

- Menstrual Hygiene and PracticesDokument24 SeitenMenstrual Hygiene and PracticesShaji Viswanathan. Mcom, MBA (U.K)Noch keine Bewertungen

- Finance Management and Control-FinalDokument30 SeitenFinance Management and Control-FinalShaji Viswanathan. Mcom, MBA (U.K)Noch keine Bewertungen

- Leading Strategic ChangeDokument22 SeitenLeading Strategic ChangeShaji Viswanathan. Mcom, MBA (U.K)100% (1)

- Cold Chain LogisticsDokument41 SeitenCold Chain LogisticsShaji Viswanathan. Mcom, MBA (U.K)100% (1)

- Loyalty Progams & Impact On Customer RetentionDokument48 SeitenLoyalty Progams & Impact On Customer RetentionShaji Viswanathan. Mcom, MBA (U.K)100% (1)

- HND Level 5 Business (Management) - Unit 17 Assignment Brief Sept 2018Dokument7 SeitenHND Level 5 Business (Management) - Unit 17 Assignment Brief Sept 2018Shaji Viswanathan. Mcom, MBA (U.K)100% (1)

- Developing Individuals, Teams and OrganizationsDokument28 SeitenDeveloping Individuals, Teams and OrganizationsShaji Viswanathan. Mcom, MBA (U.K)94% (17)

- Business StrategyDokument37 SeitenBusiness StrategyShaji Viswanathan. Mcom, MBA (U.K)Noch keine Bewertungen

- Course: HND Level 5 Business (Management) UNIT 32: Business StrategyDokument9 SeitenCourse: HND Level 5 Business (Management) UNIT 32: Business StrategyShaji Viswanathan. Mcom, MBA (U.K)0% (1)

- Working With Leading PeopleDokument24 SeitenWorking With Leading PeopleShaji Viswanathan. Mcom, MBA (U.K)Noch keine Bewertungen

- The Planning of Strategic Re-OrganizationDokument27 SeitenThe Planning of Strategic Re-OrganizationShaji Viswanathan. Mcom, MBA (U.K)Noch keine Bewertungen

- An Applied Research Project Proposal On HRMDokument39 SeitenAn Applied Research Project Proposal On HRMShaji Viswanathan. Mcom, MBA (U.K)100% (5)

- An Applied Research Project Proposal On INFRASTRUCTURE STIPULATED BY LAW FOR MENTAL HEALTH CARE CENTRESDokument26 SeitenAn Applied Research Project Proposal On INFRASTRUCTURE STIPULATED BY LAW FOR MENTAL HEALTH CARE CENTRESShaji Viswanathan. Mcom, MBA (U.K)100% (1)

- Applied Research Project ProposalDokument15 SeitenApplied Research Project ProposalShaji Viswanathan. Mcom, MBA (U.K)100% (2)

- The Impact of Drug Use and Binge Drinking On Leisure Industries in UkDokument47 SeitenThe Impact of Drug Use and Binge Drinking On Leisure Industries in UkShaji Viswanathan. Mcom, MBA (U.K)Noch keine Bewertungen

- Strategic Directions in Leadership, Marketing and PlanningDokument36 SeitenStrategic Directions in Leadership, Marketing and PlanningShaji Viswanathan. Mcom, MBA (U.K)Noch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Uncommon ServiceDokument3 SeitenUncommon ServiceEmanuel Gomez TapiaNoch keine Bewertungen

- 2 Hour Agency QuickstartDokument14 Seiten2 Hour Agency QuickstartMing Xiu Ho100% (1)

- Accounting Activity Manual MemorandumDokument29 SeitenAccounting Activity Manual Memorandummavuyanaledi07Noch keine Bewertungen

- Jaguar Racing LimitedDokument24 SeitenJaguar Racing LimitedVarun DubeyNoch keine Bewertungen

- Layman's Guide To Pair TradingDokument9 SeitenLayman's Guide To Pair TradingaporatNoch keine Bewertungen

- Chapter 3Dokument38 SeitenChapter 3shera samyNoch keine Bewertungen

- Rosewood Case 9 13Dokument10 SeitenRosewood Case 9 13venom_ftwNoch keine Bewertungen

- Journal Entry For Atkin AgencyDokument4 SeitenJournal Entry For Atkin AgencySamarth LahotiNoch keine Bewertungen

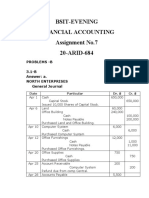

- Assignment No.7 AccountingDokument7 SeitenAssignment No.7 Accountingibrar ghaniNoch keine Bewertungen

- An Analysis On Advantages and Disadvantages of C2C E-Commerce in EntrepreneurshipDokument3 SeitenAn Analysis On Advantages and Disadvantages of C2C E-Commerce in EntrepreneurshipnafuturoNoch keine Bewertungen

- International Marketing: I-Executive SummaryDokument14 SeitenInternational Marketing: I-Executive SummaryNajia SalmanNoch keine Bewertungen

- Modul Praktikum APKM - Week 1 - Konsep Akuntansi Manajemen, Konsep Biaya, Dan Klasifikasi BiayaDokument15 SeitenModul Praktikum APKM - Week 1 - Konsep Akuntansi Manajemen, Konsep Biaya, Dan Klasifikasi BiayaYosefin SumbayakNoch keine Bewertungen

- Saa Group Acca F5 Mock 2011Dokument6 SeitenSaa Group Acca F5 Mock 2011Tasin Yeva LeoNoch keine Bewertungen

- MODMGT2 Syllabus - 3T1617Dokument5 SeitenMODMGT2 Syllabus - 3T1617OwlHeadNoch keine Bewertungen

- BV Transforming A Business Plan Into An Action PlanDokument6 SeitenBV Transforming A Business Plan Into An Action PlanCFC Zipy100% (2)

- MGT301 Assignment No 1 SolveDokument2 SeitenMGT301 Assignment No 1 SolveMA IQBALNoch keine Bewertungen

- Clenneth CompanyDokument21 SeitenClenneth CompanyRich ann belle AuditorNoch keine Bewertungen

- 1.supply Chain MistakesDokument6 Seiten1.supply Chain MistakesSantosh DevaNoch keine Bewertungen

- Distinguish Between Marginal Costing and Absorption CostingDokument10 SeitenDistinguish Between Marginal Costing and Absorption Costingmohamed Suhuraab50% (2)

- Marketing-Principles - Study ResourcesDokument12 SeitenMarketing-Principles - Study ResourcesSenumi FonsekaNoch keine Bewertungen

- A Mba Final Project by Riaz Ahmad and M Bilal AfzalDokument120 SeitenA Mba Final Project by Riaz Ahmad and M Bilal Afzalmoss4uNoch keine Bewertungen

- Inventory Management and Control: Chapter-05Dokument5 SeitenInventory Management and Control: Chapter-05Bijoy SalahuddinNoch keine Bewertungen

- Project Accounting Basic Microsoft DynamicsDokument91 SeitenProject Accounting Basic Microsoft DynamicsKannaiyakumarNoch keine Bewertungen

- ACC20020 Management - Accounting Exam - 16-17Dokument12 SeitenACC20020 Management - Accounting Exam - 16-17Anonymous qRU8qVNoch keine Bewertungen

- CGN Supplier Collaboration White PaperDokument7 SeitenCGN Supplier Collaboration White Papershshafei8367Noch keine Bewertungen

- Soal Percentage Completion MethodDokument7 SeitenSoal Percentage Completion Method30 Novita Kusuma WardhaniNoch keine Bewertungen

- Entreprenuership Gorup ProjectDokument9 SeitenEntreprenuership Gorup ProjectAmir IskandarNoch keine Bewertungen

- HR Manager As A Career (Young Kalpana 2023-24)Dokument7 SeitenHR Manager As A Career (Young Kalpana 2023-24)Akshat SharmaNoch keine Bewertungen

- Chapter 7 Primer On Cash Flow ValuationDokument37 SeitenChapter 7 Primer On Cash Flow ValuationK60 Phạm Thị Phương AnhNoch keine Bewertungen

- E4 8Dokument1 SeiteE4 8Emirza RahmanNoch keine Bewertungen