Das könnte Ihnen auch gefallen

- AccountingDokument437 SeitenAccountingNeel Hati100% (1)

- CMA Foundation (Accounts) by CA Mohit RohraDokument341 SeitenCMA Foundation (Accounts) by CA Mohit Rohramalltushar975Noch keine Bewertungen

- Financial Reporting and Analysis GuideDokument16 SeitenFinancial Reporting and Analysis GuideSagar KumarNoch keine Bewertungen

- GST Tally ERP9 English: A Handbook for Understanding GST Implementation in TallyVon EverandGST Tally ERP9 English: A Handbook for Understanding GST Implementation in TallyBewertung: 5 von 5 Sternen5/5 (1)

- A Practical Approach to the Study of Indian Capital MarketsVon EverandA Practical Approach to the Study of Indian Capital MarketsNoch keine Bewertungen

- 17 Checklist NBFC NDDokument11 Seiten17 Checklist NBFC NDaasitabhatt71% (7)

- Dr. Mehul P.Mehta: Assistant Professor BRCM College of Business Administration. Surat, GujaratDokument3 SeitenDr. Mehul P.Mehta: Assistant Professor BRCM College of Business Administration. Surat, GujaratMohammad ShirazNoch keine Bewertungen

- Whatsapp No: +917670919347 Tuesday, August 10, 2021: 12Th of August Weekly ExpiryDokument1 SeiteWhatsapp No: +917670919347 Tuesday, August 10, 2021: 12Th of August Weekly ExpiryKrishna SharmaNoch keine Bewertungen

- Organisation of Commerce and ManagementDokument100 SeitenOrganisation of Commerce and ManagementAMIN BUHARI ABDUL KHADERNoch keine Bewertungen

- India VIXDokument2 SeitenIndia VIXNihilisticDelusionNoch keine Bewertungen

- Calculation of AND Indexes: NSE BSEDokument5 SeitenCalculation of AND Indexes: NSE BSEnaveenNoch keine Bewertungen

- WWW Investopedia Com MACD PrimulDokument10 SeitenWWW Investopedia Com MACD PrimulAvram Cosmin GeorgianNoch keine Bewertungen

- The basics of stock market tradingDokument26 SeitenThe basics of stock market tradingSubhransuNoch keine Bewertungen

- Gss Sheet - Goela Stock Selector: Fact ListDokument9 SeitenGss Sheet - Goela Stock Selector: Fact ListRakesh BehuriaNoch keine Bewertungen

- Trading Plan Essentials: Capital: Risk: Risk/Reward: Profit Target: Processes: Management: Limits: WithdrawsDokument1 SeiteTrading Plan Essentials: Capital: Risk: Risk/Reward: Profit Target: Processes: Management: Limits: WithdrawsParviz GhoibovNoch keine Bewertungen

- Private Equity FundsDokument225 SeitenPrivate Equity FundsvnavaridasNoch keine Bewertungen

- Module 1 Chapter 2 Accounting ProcessDokument116 SeitenModule 1 Chapter 2 Accounting ProcessADITYAROOP PATHAKNoch keine Bewertungen

- Untangling NPS Taxation: Your ContributionsDokument8 SeitenUntangling NPS Taxation: Your ContributionsNItishNoch keine Bewertungen

- Yta School BookletDokument37 SeitenYta School BookletAditi100% (1)

- How To Predict If A Stock Will Go Up or DownDokument18 SeitenHow To Predict If A Stock Will Go Up or DownBrijesh YadavNoch keine Bewertungen

- Income Tax Complete - E-Notes - Udesh Regular - Group 1Dokument250 SeitenIncome Tax Complete - E-Notes - Udesh Regular - Group 1Uday Tomar100% (1)

- Accounting for Non-Profits ExplainedDokument6 SeitenAccounting for Non-Profits ExplainedSGENoch keine Bewertungen

- Easy Chart of Deductions U - S 80C To 80U Every Individual Should Aware of ! - TaxworryDokument2 SeitenEasy Chart of Deductions U - S 80C To 80U Every Individual Should Aware of ! - Taxworrytiata777Noch keine Bewertungen

- Income Tax Concept Book (Amended)Dokument298 SeitenIncome Tax Concept Book (Amended)Ajai SNoch keine Bewertungen

- JAIIB N I Act 1881Dokument42 SeitenJAIIB N I Act 1881Umesh ChandraNoch keine Bewertungen

- Stock Market Basics: Name:-Pawan Chabriya. ROLL - NO: - 5. STD: - T.Y-B.F.M. Subject: - Marketing in Financial ServicesDokument17 SeitenStock Market Basics: Name:-Pawan Chabriya. ROLL - NO: - 5. STD: - T.Y-B.F.M. Subject: - Marketing in Financial ServicesPAWAN CHHABRIANoch keine Bewertungen

- Ca Inter Advanced Accounts Imp Questions BookletDokument112 SeitenCa Inter Advanced Accounts Imp Questions BookletUdaykiran BheemaganiNoch keine Bewertungen

- F&O NotescombinedDokument200 SeitenF&O NotescombinedMunish GuptaNoch keine Bewertungen

- Ultimate Guide To Investments For BeginnersDokument18 SeitenUltimate Guide To Investments For BeginnersArkya MojumderNoch keine Bewertungen

- Tax Study Material PDFDokument151 SeitenTax Study Material PDFROHITH R MENONNoch keine Bewertungen

- Annexure-92. (B.Com Hons) SYLLABUS PDFDokument136 SeitenAnnexure-92. (B.Com Hons) SYLLABUS PDFPrakharNoch keine Bewertungen

- Banknifty 3 30 FormulaTrading Strategy 1699629081727Dokument1 SeiteBanknifty 3 30 FormulaTrading Strategy 1699629081727samidh MorariNoch keine Bewertungen

- Kumar VishwasDokument2 SeitenKumar VishwasSimme MinaNoch keine Bewertungen

- CMSL Notes PDFDokument105 SeitenCMSL Notes PDFVamsi KrishnaNoch keine Bewertungen

- Passing of Board Resolution by Circulation Under Section 289Dokument3 SeitenPassing of Board Resolution by Circulation Under Section 289Rajagopal ChellappanNoch keine Bewertungen

- IT CircularDokument65 SeitenIT Circularnavdeepsingh.india8849100% (2)

- Final Project ForexDokument145 SeitenFinal Project ForexdamupatelNoch keine Bewertungen

- SM CMM RevDokument168 SeitenSM CMM Revprafulvg100% (2)

- Hero Motocorp Balance Sheet AnalysisDokument23 SeitenHero Motocorp Balance Sheet AnalysisabchbvNoch keine Bewertungen

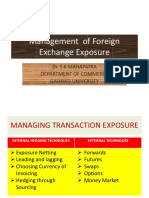

- Management of Foreign Exchange ExposureDokument13 SeitenManagement of Foreign Exchange ExposureTuki DasNoch keine Bewertungen

- Hedging Techniques in Indian Stock Market-Indiabulls (1) - FinalDokument108 SeitenHedging Techniques in Indian Stock Market-Indiabulls (1) - FinalUpendra SaiNoch keine Bewertungen

- Ind As 7 PDFDokument38 SeitenInd As 7 PDFmanan3466Noch keine Bewertungen

- Taxmann's Labour Laws With Code On Wages 2020 Edition TaxmannDokument799 SeitenTaxmann's Labour Laws With Code On Wages 2020 Edition Taxmannbharathi tNoch keine Bewertungen

- 52 Essential Metrics For The Stock MarketDokument10 Seiten52 Essential Metrics For The Stock Marketzekai yangNoch keine Bewertungen

- Dalal Street Sep 2019Dokument84 SeitenDalal Street Sep 2019rgecamitNoch keine Bewertungen

- What Is Sensex - How Is It Calculated - Basics of Share Market PDFDokument14 SeitenWhat Is Sensex - How Is It Calculated - Basics of Share Market PDFMayur Mohanji GuptaNoch keine Bewertungen

- Annual ReportDokument160 SeitenAnnual ReportSivaNoch keine Bewertungen

- Iso 14001 Syllabus PDFDokument4 SeitenIso 14001 Syllabus PDFSeni OkeNoch keine Bewertungen

- Mutual Fund Insight Mar - 2024Dokument85 SeitenMutual Fund Insight Mar - 2024AtulNoch keine Bewertungen

- Receipts and Payments Accounts and Income and Expenditure AccountsDokument5 SeitenReceipts and Payments Accounts and Income and Expenditure AccountsVikrant Joshi0% (2)

- Financial Accounting PPT 123Dokument29 SeitenFinancial Accounting PPT 123An KitNoch keine Bewertungen

- Financial Statements of Not For Profit Organisations BBEDokument27 SeitenFinancial Statements of Not For Profit Organisations BBEanirudh.dubey10001Noch keine Bewertungen

- Non Trading OrganizationDokument2 SeitenNon Trading OrganizationPBGYB60% (5)

- Bad Debts and Provision For Doubtful DebtsDokument13 SeitenBad Debts and Provision For Doubtful DebtsbillNoch keine Bewertungen

- 19674ipcc Acc Vol1 Chapter-9Dokument44 Seiten19674ipcc Acc Vol1 Chapter-9Sonu KamalNoch keine Bewertungen

- Receipts & Payments - Income & Expenditure AccountsDokument16 SeitenReceipts & Payments - Income & Expenditure AccountsAriel JonesNoch keine Bewertungen

- 16 - Not For Profit Organisation - An Introduction (134 KB) PDFDokument14 Seiten16 - Not For Profit Organisation - An Introduction (134 KB) PDFramneekdadwalNoch keine Bewertungen

- Accounts of Non Trading OrganisationDokument13 SeitenAccounts of Non Trading OrganisationMahesh Kumar100% (2)

- Trial Balance To Profit & Loss A/c and Balance Sheet For Corporate & Non-Corporate EntitiesDokument24 SeitenTrial Balance To Profit & Loss A/c and Balance Sheet For Corporate & Non-Corporate EntitiesChintan PatelNoch keine Bewertungen

- Affiliation Rules & RegulationsDokument22 SeitenAffiliation Rules & RegulationsMuhammad Usman SaeedNoch keine Bewertungen

- Suggested Answers Intermediate Examination - Spring 2013: TaxationDokument7 SeitenSuggested Answers Intermediate Examination - Spring 2013: TaxationMuhammad Usman SaeedNoch keine Bewertungen

- 4bfp Brochure-Qatar PDFDokument1 Seite4bfp Brochure-Qatar PDFMuhammad Usman SaeedNoch keine Bewertungen

- MFN Status and Trade Between Pakistan and IndiaDokument18 SeitenMFN Status and Trade Between Pakistan and IndiaMuhammad Usman SaeedNoch keine Bewertungen

- Audit EngagementDokument2 SeitenAudit EngagementMuhammad Usman SaeedNoch keine Bewertungen

- Government of Pakistan Federal Board of RevenueDokument2 SeitenGovernment of Pakistan Federal Board of Revenuezubairkhan_leoNoch keine Bewertungen

- Commission, Fee and ChargesDokument1 SeiteCommission, Fee and ChargesMuhammad Usman SaeedNoch keine Bewertungen

- Digital Library Registration RequirementsDokument1 SeiteDigital Library Registration Requirementsasher_tfm1693Noch keine Bewertungen

- Types of Software Used in BanksDokument3 SeitenTypes of Software Used in BanksMussadaq JavedNoch keine Bewertungen

- First Women Bank LimitedDokument18 SeitenFirst Women Bank LimitedMuhammad Usman SaeedNoch keine Bewertungen

- Job Advertisement StyleDokument2 SeitenJob Advertisement StyleMuhammad Usman SaeedNoch keine Bewertungen

- OriginDokument2 SeitenOriginMuhammad Usman SaeedNoch keine Bewertungen

- 2013 LalPir Power LTD ProspectusDokument84 Seiten2013 LalPir Power LTD ProspectusMuhammad Usman Saeed0% (1)

- 2002 National Bank of PakistanDokument29 Seiten2002 National Bank of PakistansooperusmanNoch keine Bewertungen

- Iv. Information and Communication Technology Infrastructure: A. IntroductionDokument18 SeitenIv. Information and Communication Technology Infrastructure: A. IntroductionMuhammad Usman SaeedNoch keine Bewertungen

- The 7 CS: The Essential Building Blocks of ResilienceDokument1 SeiteThe 7 CS: The Essential Building Blocks of ResilienceMuhammad Usman SaeedNoch keine Bewertungen

- AC07Dokument2 SeitenAC07shreyas_devangaNoch keine Bewertungen

- Alberta Budget 2019 Fiscal PlanDokument208 SeitenAlberta Budget 2019 Fiscal Planedmontonjournal100% (4)

- The Effect of Capital Flight On Nigerian EconomyDokument127 SeitenThe Effect of Capital Flight On Nigerian EconomyAdewole Aliu OlusolaNoch keine Bewertungen

- 5.1 Demand and Supply-Side PoliciesDokument13 Seiten5.1 Demand and Supply-Side PoliciesMarisa VetterNoch keine Bewertungen

- UGB371 Managing and Leading ChangeDokument16 SeitenUGB371 Managing and Leading ChangePhương Anh Nguyễn100% (1)

- Saudi EconomicDokument70 SeitenSaudi EconomicFrancis Salviejo100% (1)

- MCQ's On EconomicsDokument42 SeitenMCQ's On EconomicsDHARMA DAZZLENoch keine Bewertungen

- Differences PSAK 45 (Organization and Entity) and PSAK 1 + ISAK 35Dokument2 SeitenDifferences PSAK 45 (Organization and Entity) and PSAK 1 + ISAK 35Vanadisa SamuelNoch keine Bewertungen

- Warnings of The Maharlika Investment FundDokument1 SeiteWarnings of The Maharlika Investment FundAha BodowskyNoch keine Bewertungen

- Rudiger Dornbusch, Mario Draghi-Public Debt Management - Theory and History-Cambridge University Press (1990)Dokument378 SeitenRudiger Dornbusch, Mario Draghi-Public Debt Management - Theory and History-Cambridge University Press (1990)Koen van den Bos100% (2)

- CFA三级密卷 题目Dokument61 SeitenCFA三级密卷 题目vxm9pctmrrNoch keine Bewertungen

- BC Budget 2023Dokument182 SeitenBC Budget 2023CityNewsToronto100% (1)

- Ela Career Development Unit 3-Module 1 - Resource 2 Analyze A Salary-Based Budget 1Dokument3 SeitenEla Career Development Unit 3-Module 1 - Resource 2 Analyze A Salary-Based Budget 1api-542822113Noch keine Bewertungen

- 01-Sta - mariaIS2021 Audit ReportDokument107 Seiten01-Sta - mariaIS2021 Audit ReportAnjo BrillantesNoch keine Bewertungen

- ECON212 Sample Final ExamDokument17 SeitenECON212 Sample Final Examstharan23Noch keine Bewertungen

- Economic Growth: Trade BalanceDokument54 SeitenEconomic Growth: Trade BalancepiyushmamgainNoch keine Bewertungen

- How To Crack The IELTS Writing Test - Vol 1Dokument308 SeitenHow To Crack The IELTS Writing Test - Vol 1JaydenNoch keine Bewertungen

- Midterm 2 With SolutionsDokument12 SeitenMidterm 2 With SolutionsNikoleta TrudovNoch keine Bewertungen

- 2018 Peoples Budget For PostingDokument49 Seiten2018 Peoples Budget For PostingAlvinDumanggas100% (1)

- Social Security and Medicare Trustees ReportDokument28 SeitenSocial Security and Medicare Trustees ReportAustin DeneanNoch keine Bewertungen

- Chattisgarh CSERC MYT Tariff Order For State Power Companies 2011-12Dokument315 SeitenChattisgarh CSERC MYT Tariff Order For State Power Companies 2011-12Neeraj Singh GautamNoch keine Bewertungen

- Ias Exam Portal: (Online Course) Pub Ad For IAS Mains: Public Policy - State Theories & Public Policy (Paper - 1)Dokument4 SeitenIas Exam Portal: (Online Course) Pub Ad For IAS Mains: Public Policy - State Theories & Public Policy (Paper - 1)Gourangi KumarNoch keine Bewertungen

- Critical Issues in Transportation: Congestion, Emergencies, Energy, Equity, Finance, Innovation, Infrastructure, Institutions, and SafetyDokument16 SeitenCritical Issues in Transportation: Congestion, Emergencies, Energy, Equity, Finance, Innovation, Infrastructure, Institutions, and SafetyKamal MirzaNoch keine Bewertungen

- Indian Economy Paper - Key ConceptsDokument13 SeitenIndian Economy Paper - Key ConceptsMad MadhaviNoch keine Bewertungen

- Public Finance MCQs ExplainedDokument11 SeitenPublic Finance MCQs ExplainedIbrahimGorgage100% (1)

- Economics Crisis of PakistanDokument6 SeitenEconomics Crisis of PakistanHassam MalhiNoch keine Bewertungen

- October 2022 Revision Rbi 247Dokument71 SeitenOctober 2022 Revision Rbi 247Nitika VermaNoch keine Bewertungen

- Canada Telecommunication SWOT AnalysisDokument3 SeitenCanada Telecommunication SWOT AnalysisTheonlyone01Noch keine Bewertungen

- How Will Modi Govt Handle Revenue Deficit Without Raising Income TaxDokument3 SeitenHow Will Modi Govt Handle Revenue Deficit Without Raising Income TaxPNoch keine Bewertungen

- Chapter 1Dokument10 SeitenChapter 1Ngoh Jia HuiNoch keine Bewertungen

- Cash BudgetDokument10 SeitenCash BudgetShrinivasan IyengarNoch keine Bewertungen