Das könnte Ihnen auch gefallen

- RR 4-99Dokument3 SeitenRR 4-99matinikkiNoch keine Bewertungen

- Payment Voucher OctoberDokument1 SeitePayment Voucher OctoberKris GrubaNoch keine Bewertungen

- RMC 39-2012Dokument2 SeitenRMC 39-2012Kris GrubaNoch keine Bewertungen

- E TicketDokument1 SeiteE TicketKris GrubaNoch keine Bewertungen

- Miriam College PtaDokument1 SeiteMiriam College PtaKris GrubaNoch keine Bewertungen

- Payment Voucher AugustDokument1 SeitePayment Voucher AugustKris GrubaNoch keine Bewertungen

- Boarding PassDokument1 SeiteBoarding PassKris GrubaNoch keine Bewertungen

- LedgerDokument1 SeiteLedgerKris GrubaNoch keine Bewertungen

- 50-Meralco Vs Province of LagunaDokument2 Seiten50-Meralco Vs Province of LagunaKris GrubaNoch keine Bewertungen

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Senior Retail Bank Manager in Plano TX Resume Steven CrosbieDokument2 SeitenSenior Retail Bank Manager in Plano TX Resume Steven CrosbieStevenCrosbieNoch keine Bewertungen

- Healthsouth ScandalDokument11 SeitenHealthsouth ScandalAnshak KumarNoch keine Bewertungen

- SC's NRA Judgement On Sec.68: Threadbare Analysis of Subsequent DecisionsDokument5 SeitenSC's NRA Judgement On Sec.68: Threadbare Analysis of Subsequent DecisionsArchit ShethNoch keine Bewertungen

- Shree Cement Cimb Oct13Dokument8 SeitenShree Cement Cimb Oct13Ajit AjitabhNoch keine Bewertungen

- Common Stocks and Uncommon Profits and Other WritingsDokument13 SeitenCommon Stocks and Uncommon Profits and Other WritingsAnirbanDeshmukhNoch keine Bewertungen

- BES171 00 Gist of Eco Survey 14 ChaptersDokument30 SeitenBES171 00 Gist of Eco Survey 14 Chaptersjainrahul2910Noch keine Bewertungen

- Auditing Midterm NotesDokument25 SeitenAuditing Midterm NotesAmanda Claro0% (2)

- A Literature Review On Investors Perception TowarDokument227 SeitenA Literature Review On Investors Perception Towartilak kumar vadapalliNoch keine Bewertungen

- Liquidity and Profitability AnalysisDokument100 SeitenLiquidity and Profitability Analysisjoel john100% (1)

- Training Tuesdays: Officials Mull Fix in Indio's Terra Lago Tax FightDokument5 SeitenTraining Tuesdays: Officials Mull Fix in Indio's Terra Lago Tax FightBrian DaviesNoch keine Bewertungen

- Chapter 06 - Risk & ReturnDokument42 SeitenChapter 06 - Risk & Returnmnr81Noch keine Bewertungen

- Rapport Efficient TechnoDokument134 SeitenRapport Efficient Technosouki1Noch keine Bewertungen

- Chapter 6-The Companies Act, 2013 Incorporation of Company and Matters Incidental TheretoDokument101 SeitenChapter 6-The Companies Act, 2013 Incorporation of Company and Matters Incidental TheretoJay senthilNoch keine Bewertungen

- Financial Services in India: Basic ConceptsDokument20 SeitenFinancial Services in India: Basic Conceptsgouri khanduallNoch keine Bewertungen

- OpenMind 2010Dokument48 SeitenOpenMind 2010Venture PublishingNoch keine Bewertungen

- The Time Value MoneyDokument4 SeitenThe Time Value Moneycamilafernanda85Noch keine Bewertungen

- The Balance of Payment of IndiaDokument6 SeitenThe Balance of Payment of IndiaAby Abdul Rabb100% (1)

- 4 8 15 CPB2impactreport PDFDokument13 Seiten4 8 15 CPB2impactreport PDFShaun AdamsNoch keine Bewertungen

- Cash Flow Indirec Metode PD Mitra Revisi Upk 2016Dokument2 SeitenCash Flow Indirec Metode PD Mitra Revisi Upk 2016Faie RifaiNoch keine Bewertungen

- Cashflows For Capital BudgetingDokument1 SeiteCashflows For Capital BudgetingSaurabh KumarNoch keine Bewertungen

- 54103bos43406 p1Dokument31 Seiten54103bos43406 p1Aman GuptaNoch keine Bewertungen

- Acheson-Anthropology of FishingDokument43 SeitenAcheson-Anthropology of FishingjonavarrosNoch keine Bewertungen

- Investment Behavior of Women: A Conceptual StudyDokument8 SeitenInvestment Behavior of Women: A Conceptual StudyDr. KavitaNoch keine Bewertungen

- STRATEGYDokument22 SeitenSTRATEGYPRAGYAN PANDANoch keine Bewertungen

- MarketingDokument3 SeitenMarketingN.MUTHUKUMARANNoch keine Bewertungen

- Chapter 15 - Consolidation: Controlled Entities: Review QuestionsDokument13 SeitenChapter 15 - Consolidation: Controlled Entities: Review QuestionsShek Kwun Hei100% (1)

- Akuntansi Keuangan Lanjutan: Laba Atas Transaksi Antarperusahaan - Persediaan P5-6 DAN P5-7Dokument5 SeitenAkuntansi Keuangan Lanjutan: Laba Atas Transaksi Antarperusahaan - Persediaan P5-6 DAN P5-7doniNoch keine Bewertungen

- 20132014ProposedBudget Sep19 9pmDokument765 Seiten20132014ProposedBudget Sep19 9pmChs BlogNoch keine Bewertungen

- SWOT AnalysisDokument13 SeitenSWOT AnalysisAkshat Kaul100% (2)

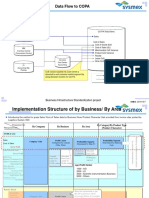

- Data Flow To COPA: Business Infrastructure Standardization ProjectDokument3 SeitenData Flow To COPA: Business Infrastructure Standardization ProjectT SAIKIRANNoch keine Bewertungen