Das könnte Ihnen auch gefallen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Quetion Paper by Kiran Sir On (25!12!10)Dokument1 SeiteQuetion Paper by Kiran Sir On (25!12!10)Esukapalli Siva ReddyNoch keine Bewertungen

- Law QP 6-2-11Dokument1 SeiteLaw QP 6-2-11Esukapalli Siva ReddyNoch keine Bewertungen

- Law QP 10-04-2011Dokument1 SeiteLaw QP 10-04-2011Esukapalli Siva ReddyNoch keine Bewertungen

- IPCC Accounts 31-10-10Dokument1 SeiteIPCC Accounts 31-10-10Esukapalli Siva ReddyNoch keine Bewertungen

- Ipcc LawDokument1 SeiteIpcc LawEsukapalli Siva ReddyNoch keine Bewertungen

- Ipcc Tax 9-1-11Dokument1 SeiteIpcc Tax 9-1-11Esukapalli Siva ReddyNoch keine Bewertungen

- Ipcc Tax - Law Q. P (22-5-2011)Dokument2 SeitenIpcc Tax - Law Q. P (22-5-2011)Esukapalli Siva ReddyNoch keine Bewertungen

- IPCC CostingDokument1 SeiteIPCC CostingEsukapalli Siva ReddyNoch keine Bewertungen

- IPCC Costing 7.08.2011Dokument1 SeiteIPCC Costing 7.08.2011Esukapalli Siva ReddyNoch keine Bewertungen

- Ipcc Law QP 13-02-11Dokument1 SeiteIpcc Law QP 13-02-11Esukapalli Siva ReddyNoch keine Bewertungen

- Ipcc Accounts QP 9-1-11Dokument1 SeiteIpcc Accounts QP 9-1-11Esukapalli Siva ReddyNoch keine Bewertungen

- SivaDokument1 SeiteSivaEsukapalli Siva ReddyNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Corporate Governance in MalaysiaDokument19 SeitenCorporate Governance in Malaysiakhorteik100% (1)

- YatharthDokument8 SeitenYatharthCp918315Noch keine Bewertungen

- Blackbook Project On Merchant BankingDokument66 SeitenBlackbook Project On Merchant BankingElton Andrade75% (12)

- Rein Hardware StoreDokument2 SeitenRein Hardware StoreMariñas, Romalyn D.Noch keine Bewertungen

- Valuasi Saham MppaDokument29 SeitenValuasi Saham MppaGaos FakhryNoch keine Bewertungen

- XLS EngDokument21 SeitenXLS EngRudra BarotNoch keine Bewertungen

- Common Size Financial StatementsDokument3 SeitenCommon Size Financial Statementsirfanabid828Noch keine Bewertungen

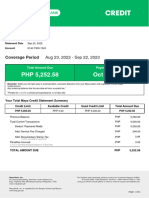

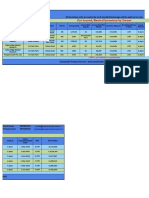

- MayaCredit SoA 2023SEPDokument3 SeitenMayaCredit SoA 2023SEPjepoy palaruanNoch keine Bewertungen

- New Zealand 2009 Financial Knowledge SurveyDokument11 SeitenNew Zealand 2009 Financial Knowledge SurveywmhuthnanceNoch keine Bewertungen

- National Insurance Company Ltd. Policy No: 57150031216760012077 1 Year Liability Only From 00:00:01 Hours On 28-Jan-2022 To Midnight of 27/01/2023Dokument2 SeitenNational Insurance Company Ltd. Policy No: 57150031216760012077 1 Year Liability Only From 00:00:01 Hours On 28-Jan-2022 To Midnight of 27/01/2023Benson BennyNoch keine Bewertungen

- Swaps PresentationDokument34 SeitenSwaps PresentationSherman WaltonNoch keine Bewertungen

- Societe GeneraleDokument42 SeitenSociete GeneraleMakuna NatsvlishviliNoch keine Bewertungen

- A Study On Lending Practices of RDCC Bank, SindhanurDokument60 SeitenA Study On Lending Practices of RDCC Bank, SindhanurHasan shaikhNoch keine Bewertungen

- Interim ReportDokument20 SeitenInterim ReportanushaNoch keine Bewertungen

- 1.what Is SAP Finance? What Business Requirement Is Fulfilled in This Module?Dokument163 Seiten1.what Is SAP Finance? What Business Requirement Is Fulfilled in This Module?sudhakarNoch keine Bewertungen

- Form No. 16 (See Rule 31 (1) (A) ) Certificate Under Section 203 of The Income-Tax Act, 1961 For Tax Deducted at Source On SalaryDokument2 SeitenForm No. 16 (See Rule 31 (1) (A) ) Certificate Under Section 203 of The Income-Tax Act, 1961 For Tax Deducted at Source On SalaryKrishna Chaitanya JonnalagaddaNoch keine Bewertungen

- Atlantic Tours General Journal Date: Account Titles and Explanation Ref: Debits Credits 2003Dokument4 SeitenAtlantic Tours General Journal Date: Account Titles and Explanation Ref: Debits Credits 2003babe447Noch keine Bewertungen

- Psak 72 10 Minutes PDFDokument2 SeitenPsak 72 10 Minutes PDFMentari AndiniNoch keine Bewertungen

- Madhuban Bapudham SchemeDokument3 SeitenMadhuban Bapudham SchemerahulNoch keine Bewertungen

- Deposit Mobilization of Commercial Bank in Nepal Case Study of Nabil Bank LTDDokument9 SeitenDeposit Mobilization of Commercial Bank in Nepal Case Study of Nabil Bank LTDKrishanKhadkaNoch keine Bewertungen

- Philippine Income Taxation - Supplemental Quizzes Part 1 (CHAPTERS 1-6)Dokument9 SeitenPhilippine Income Taxation - Supplemental Quizzes Part 1 (CHAPTERS 1-6)Wag mong ikalatNoch keine Bewertungen

- AOM 2023 001 Tuy ADokument18 SeitenAOM 2023 001 Tuy AKean Fernand BocaboNoch keine Bewertungen

- FINS1613 File 04 - All 3 Topics Practice Questions PDFDokument16 SeitenFINS1613 File 04 - All 3 Topics Practice Questions PDFisy campbellNoch keine Bewertungen

- Starbuck PPT by Pershing SquareDokument44 SeitenStarbuck PPT by Pershing SquareJainam VoraNoch keine Bewertungen

- Ratio Analysis of Shree Cement and Ambuja Cement Project Report 2Dokument7 SeitenRatio Analysis of Shree Cement and Ambuja Cement Project Report 2Dale 08Noch keine Bewertungen

- Sustainable Pre Leased 06122019Dokument2 SeitenSustainable Pre Leased 06122019vaibhav vermaNoch keine Bewertungen

- Notes The Intelligent Asset AllocatorDokument3 SeitenNotes The Intelligent Asset AllocatorEdwin GonzalitoNoch keine Bewertungen

- Blue Chip CompanyDokument12 SeitenBlue Chip CompanyMuralis MuralisNoch keine Bewertungen

- UCC 1 Security AgreementDokument1 SeiteUCC 1 Security Agreementtlh78great100% (7)

- CFAS Quiz Questions AddedDokument2 SeitenCFAS Quiz Questions AddedSaeym SegoviaNoch keine Bewertungen