Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Paper Presentation EcbDokument3 SeitenPaper Presentation EcberikaNoch keine Bewertungen

- Activist Investing White Paper by Florida State Board of AdmistrationDokument48 SeitenActivist Investing White Paper by Florida State Board of AdmistrationBradley TirpakNoch keine Bewertungen

- Mutual Fund AssignmentDokument51 SeitenMutual Fund AssignmentKuljeet Singh83% (6)

- 40 SitaraDokument2 Seiten40 SitaraTIN_CUP_87100% (1)

- CASE 5 Rochester ManufacturingDokument5 SeitenCASE 5 Rochester Manufacturinglikha piao0% (1)

- Trade During The Industrial Revolution - EditedDokument3 SeitenTrade During The Industrial Revolution - EditedJames YangNoch keine Bewertungen

- Brs Practise SheetDokument1 SeiteBrs Practise Sheetapi-252642432Noch keine Bewertungen

- Industrial Estates in PakistanDokument3 SeitenIndustrial Estates in PakistanMuazzam Mughal33% (3)

- Reasonable AssuranceDokument12 SeitenReasonable AssuranceHossein DavaniNoch keine Bewertungen

- SMR - Group 5Dokument30 SeitenSMR - Group 5rishabhasthanaNoch keine Bewertungen

- The Bank of Nova ScotiaDokument18 SeitenThe Bank of Nova Scotiakash32192Noch keine Bewertungen

- The Following Is A List of Banks in IndiaDokument9 SeitenThe Following Is A List of Banks in IndiaSubash SundarNoch keine Bewertungen

- 12 - MWS96KEE127BAS - 1research Project - WalmartDokument7 Seiten12 - MWS96KEE127BAS - 1research Project - WalmartashibhallauNoch keine Bewertungen

- Malegam Committee Report 20-01-11Dokument2 SeitenMalegam Committee Report 20-01-11Mayank AgrawalNoch keine Bewertungen

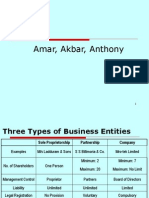

- Forms of Business EntityDokument20 SeitenForms of Business EntityMain Daiictian HuNoch keine Bewertungen

- Guidelines by RbiDokument7 SeitenGuidelines by RbiSandip BarotNoch keine Bewertungen

- FFMC Rbi DocsDokument51 SeitenFFMC Rbi DocsManikNoch keine Bewertungen

- JFK Killed Just Days After Shutting Down RothschildDokument12 SeitenJFK Killed Just Days After Shutting Down RothschildDomenico Bevilacqua100% (1)

- Donald Kohn Nomination Hearing For Federal Reserve Board - 2002Dokument151 SeitenDonald Kohn Nomination Hearing For Federal Reserve Board - 2002Matt StollerNoch keine Bewertungen

- Topic 3 - Todaro, Economic Development - Ch.3 (Wiscana AP)Dokument4 SeitenTopic 3 - Todaro, Economic Development - Ch.3 (Wiscana AP)Wiscana Chacha100% (1)

- Day Trading by Matthew MayburyDokument52 SeitenDay Trading by Matthew MayburyXRM09090% (1)

- Portfolio Management Professional Reference ListDokument1 SeitePortfolio Management Professional Reference ListMohammed AlnasharNoch keine Bewertungen

- RAPDokument42 SeitenRAPJozua Oshea PungNoch keine Bewertungen

- 2008 June Paper 1Dokument2 Seiten2008 June Paper 1zahid_mahmood3811Noch keine Bewertungen

- Company Introduction: Initial Report June 23rd, 2008Dokument19 SeitenCompany Introduction: Initial Report June 23rd, 2008beacon-docsNoch keine Bewertungen

- ACCA Corporate Governance Technical Articles PDFDokument17 SeitenACCA Corporate Governance Technical Articles PDFNicquainCTNoch keine Bewertungen

- Jurnal Imbalan KerjaDokument7 SeitenJurnal Imbalan KerjanikadekdiwayamiNoch keine Bewertungen

- Investor Presentation PDFDokument28 SeitenInvestor Presentation PDFshub56jainNoch keine Bewertungen

- Role of MNC/S in Growth of Indian EconomyDokument2 SeitenRole of MNC/S in Growth of Indian EconomyBhupen SharmaNoch keine Bewertungen

- Mubadala - Base Prospectus PDFDokument293 SeitenMubadala - Base Prospectus PDFAngkatan LautNoch keine Bewertungen