Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (894)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Fed U.S. Federal Individual Income Tax Rates History, 1862-2013Dokument68 SeitenFed U.S. Federal Individual Income Tax Rates History, 1862-2013Tax Foundation96% (23)

- Federal Individual Individual Income Tax Rate, Adjusted For InflationDokument66 SeitenFederal Individual Individual Income Tax Rate, Adjusted For InflationTax Foundation100% (4)

- Federal Individual Individual Income Tax Rate, Adjusted For InflationDokument66 SeitenFederal Individual Individual Income Tax Rate, Adjusted For InflationTax Foundation100% (4)

- Federal Income Tax Rates History, Nominal Dollars, 1913-2013Dokument66 SeitenFederal Income Tax Rates History, Nominal Dollars, 1913-2013Tax Foundation100% (1)

- HOLBORN Contemporary SociologyDokument776 SeitenHOLBORN Contemporary SociologyçiğdemNoch keine Bewertungen

- Rural Development Theory, Lec. 1,2Dokument16 SeitenRural Development Theory, Lec. 1,2Matin Muhammad AminNoch keine Bewertungen

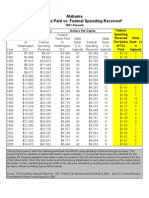

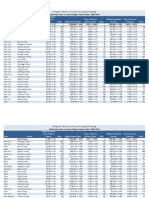

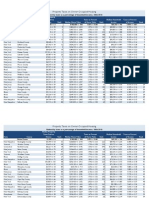

- Federal Taxes Paid Vs Federal Spending Received by States, 1981-2005Dokument51 SeitenFederal Taxes Paid Vs Federal Spending Received by States, 1981-2005Javier Arvelo-Cruz-SantanaNoch keine Bewertungen

- Facts and Figures 2013Dokument56 SeitenFacts and Figures 2013Tax FoundationNoch keine Bewertungen

- Christmas Cheer Return: Filing StatusDokument2 SeitenChristmas Cheer Return: Filing StatusTax FoundationNoch keine Bewertungen

- How Is The Money Used? Federal and State Cases Distinguishing Taxes and FeesDokument98 SeitenHow Is The Money Used? Federal and State Cases Distinguishing Taxes and FeesTax FoundationNoch keine Bewertungen

- Facts & Figures 2015: How Does Your State Compare?Dokument55 SeitenFacts & Figures 2015: How Does Your State Compare?Tax FoundationNoch keine Bewertungen

- Tax Foundation 2014 Annual ReportDokument32 SeitenTax Foundation 2014 Annual ReportTax FoundationNoch keine Bewertungen

- Explainer: Nevada Governor Sandoval's Business License Fee Restructuring - Appendix ADokument10 SeitenExplainer: Nevada Governor Sandoval's Business License Fee Restructuring - Appendix ATax FoundationNoch keine Bewertungen

- Facts and Figures 2014Dokument55 SeitenFacts and Figures 2014Tax FoundationNoch keine Bewertungen

- Tax Watch, Winter 2013Dokument28 SeitenTax Watch, Winter 2013Tax FoundationNoch keine Bewertungen

- Facts and Figures - How Does Your State Compare? 2013 EditionDokument56 SeitenFacts and Figures - How Does Your State Compare? 2013 EditionTax FoundationNoch keine Bewertungen

- North Carolina Tax Reform Options: A Guide To Fair, Simple, Pro-Growth ReformDokument84 SeitenNorth Carolina Tax Reform Options: A Guide To Fair, Simple, Pro-Growth ReformTax Foundation100% (1)

- Powerpoint Presentation For "North Carolina Tax Reform Options: A Guide To Fair, Simple, Pro-Growth Reform"Dokument38 SeitenPowerpoint Presentation For "North Carolina Tax Reform Options: A Guide To Fair, Simple, Pro-Growth Reform"Tax FoundationNoch keine Bewertungen

- Fiscal Cliff MSA TableDokument11 SeitenFiscal Cliff MSA TableTax FoundationNoch keine Bewertungen

- Fiscal Cliff MSA TableDokument11 SeitenFiscal Cliff MSA TableTax FoundationNoch keine Bewertungen

- Proptax10 Home ValueDokument28 SeitenProptax10 Home ValueTax FoundationNoch keine Bewertungen

- Scott Hodge, President Will Mcbride, Chief EconomistDokument20 SeitenScott Hodge, President Will Mcbride, Chief EconomistTax FoundationNoch keine Bewertungen

- Proptax 08 10 IncomeDokument66 SeitenProptax 08 10 IncomeTax FoundationNoch keine Bewertungen

- Proptax10 Taxes PaidDokument27 SeitenProptax10 Taxes PaidTax FoundationNoch keine Bewertungen

- Proptax 08 10 TaxespaidDokument67 SeitenProptax 08 10 TaxespaidTax FoundationNoch keine Bewertungen

- Proptax 06 10 HomevalueDokument102 SeitenProptax 06 10 HomevalueTax FoundationNoch keine Bewertungen

- Property Taxes On Owner-Occupied HousingDokument28 SeitenProperty Taxes On Owner-Occupied HousingTax FoundationNoch keine Bewertungen

- Proptax 06 10 TaxpaidDokument102 SeitenProptax 06 10 TaxpaidTax FoundationNoch keine Bewertungen

- Proptax 06 10 IncomeDokument102 SeitenProptax 06 10 IncomeTax FoundationNoch keine Bewertungen

- 107th Issue of SarvekshanaDokument80 Seiten107th Issue of SarvekshanaAnilNoch keine Bewertungen

- Vanishing Middle Class of BangladeshDokument5 SeitenVanishing Middle Class of BangladeshPiashi PurbitaNoch keine Bewertungen

- Demographia International Housing Affordability: 2022 EDITIONDokument23 SeitenDemographia International Housing Affordability: 2022 EDITIONNews 8 WROCNoch keine Bewertungen

- Inequality, Poverty and DevelopmentDokument38 SeitenInequality, Poverty and DevelopmentCresenciano MalabuyocNoch keine Bewertungen

- Life ExpectancyDokument12 SeitenLife Expectancymuqtadir100% (1)

- 2015 02 17 Leveraging Local Procurement To Drive Shared Value A Presentation by Clive GovenderDokument28 Seiten2015 02 17 Leveraging Local Procurement To Drive Shared Value A Presentation by Clive GovenderAlberto LobonesNoch keine Bewertungen

- Carina Fourie, Fabian Schuppert, Ivo Wallimann-Helmer-Social Equality - On What It Means To Be Equals-Oxford University Press (2015)Dokument257 SeitenCarina Fourie, Fabian Schuppert, Ivo Wallimann-Helmer-Social Equality - On What It Means To Be Equals-Oxford University Press (2015)Thor Veras100% (1)

- Manifesto Framing StatementDokument20 SeitenManifesto Framing Statementepcferreira6512Noch keine Bewertungen

- Chapter 5Dokument78 SeitenChapter 5chuasexyNoch keine Bewertungen

- Macroeconomic Stability, Inclusive Growth and Employment: Thematic Think Piece Ilo, Unctad, Undesa, WtoDokument12 SeitenMacroeconomic Stability, Inclusive Growth and Employment: Thematic Think Piece Ilo, Unctad, Undesa, WtoKasun DulanjanaNoch keine Bewertungen

- Understanding Global StratificationDokument12 SeitenUnderstanding Global StratificationLara Tessa VinluanNoch keine Bewertungen

- 2019 JC2 H1 GP Prelim Nanyang Junior CollegeDokument15 Seiten2019 JC2 H1 GP Prelim Nanyang Junior CollegesueNoch keine Bewertungen

- The Intersection of Gender and Race in The Labor MarketDokument28 SeitenThe Intersection of Gender and Race in The Labor MarketCaro SánchezNoch keine Bewertungen

- GC World ReviewerDokument12 SeitenGC World ReviewerKathleen SummerNoch keine Bewertungen

- Justifying Democracy - DahlDokument7 SeitenJustifying Democracy - DahlTelma Rocha Lisowski100% (1)

- Uganda PDFDokument114 SeitenUganda PDFMadhu KumarNoch keine Bewertungen

- Rousseaus Critique of Inequality Reconstructing The Second DiscourseDokument250 SeitenRousseaus Critique of Inequality Reconstructing The Second DiscourseDerek WilliamsNoch keine Bewertungen

- National Integration in Pakistan: EssaysDokument6 SeitenNational Integration in Pakistan: EssaysQasim FarooqNoch keine Bewertungen

- Social Science Class 10 Important Questions Politi+Dokument9 SeitenSocial Science Class 10 Important Questions Politi+Jaya SinghNoch keine Bewertungen

- Inequality and PovertyDokument42 SeitenInequality and PovertyTiffany SagitaNoch keine Bewertungen

- TVS Balance SheetDokument6 SeitenTVS Balance SheetNihal LamgeNoch keine Bewertungen

- Equity in Extractives: Stewarding Africa's Natural Resources For AllDokument120 SeitenEquity in Extractives: Stewarding Africa's Natural Resources For AllAfrica Progress Panel100% (1)

- African Success StoryDokument11 SeitenAfrican Success StoryAnamika ShakyaNoch keine Bewertungen

- Public Health Social Context and ActionDokument252 SeitenPublic Health Social Context and ActionUliadi BarlimNoch keine Bewertungen

- CEO CompensationDokument27 SeitenCEO CompensationmummimNoch keine Bewertungen

- Verena Barbara Braehler PHD ThesisDokument292 SeitenVerena Barbara Braehler PHD ThesisCarlos EduardoNoch keine Bewertungen

- Human Development Index (HDI)Dokument30 SeitenHuman Development Index (HDI)Kurnia Armedi AgusNoch keine Bewertungen

- Parenting, Family Policy and Children's Well-Being in An Unequal Society Parenting, Family Policy and Children's Well-Being in An Unequal SocietyDokument248 SeitenParenting, Family Policy and Children's Well-Being in An Unequal Society Parenting, Family Policy and Children's Well-Being in An Unequal SocietyMaya MayaNoch keine Bewertungen