Das könnte Ihnen auch gefallen

- US Internal Revenue Service: rp-05-46Dokument7 SeitenUS Internal Revenue Service: rp-05-46IRSNoch keine Bewertungen

- Judgment MUHAMMAD MUNIR PERACHA, J. - The Petitioners Were Served With Show-Cause NoticeDokument6 SeitenJudgment MUHAMMAD MUNIR PERACHA, J. - The Petitioners Were Served With Show-Cause NoticeMohammad AhmadNoch keine Bewertungen

- High Court Reduces GST Penalty From Rs. 56,00,952 to Rs. 10000- Taxguru.inDokument5 SeitenHigh Court Reduces GST Penalty From Rs. 56,00,952 to Rs. 10000- Taxguru.inVineet AgrawalNoch keine Bewertungen

- Supreme Court of India Page 1 of 4Dokument4 SeitenSupreme Court of India Page 1 of 4gopala1977Noch keine Bewertungen

- Appeal Before The Commissioner of IncomeDokument10 SeitenAppeal Before The Commissioner of IncomemarlinahmurungiNoch keine Bewertungen

- Doctrines in Tax Remedies CasesDokument7 SeitenDoctrines in Tax Remedies CasesMa Gabriellen Quijada-TabuñagNoch keine Bewertungen

- BOCW Welfare Cess Rules, 1998Dokument10 SeitenBOCW Welfare Cess Rules, 1998EricKankarNoch keine Bewertungen

- Lascona Land Vs CIRDokument2 SeitenLascona Land Vs CIRJOHN SPARKSNoch keine Bewertungen

- CIR's Right to Collect Tax PrescribedDokument4 SeitenCIR's Right to Collect Tax PrescribedKM Mac100% (2)

- SM DigestDokument4 SeitenSM Digestapril75Noch keine Bewertungen

- The Building and Other Construction Workers Cess Rules, 1998Dokument11 SeitenThe Building and Other Construction Workers Cess Rules, 1998shanti raj kumarNoch keine Bewertungen

- CH 22 Appeals Revision ICAI Study MatDokument29 SeitenCH 22 Appeals Revision ICAI Study MatAnkitha ReddyNoch keine Bewertungen

- Digests 2Dokument17 SeitenDigests 2Henry LNoch keine Bewertungen

- HTML File ProcessDokument10 SeitenHTML File ProcessSuresh SharmaNoch keine Bewertungen

- Examination Proper:: Tax Law Review Mid-Term ExaminationDokument9 SeitenExamination Proper:: Tax Law Review Mid-Term ExaminationGRACENoch keine Bewertungen

- Gulf Oil LubricantsDokument3 SeitenGulf Oil Lubricantsmdfaizan.alamNoch keine Bewertungen

- Assessing Tax, Interest and RefundsDokument9 SeitenAssessing Tax, Interest and RefundsMd Nazir HussainNoch keine Bewertungen

- Rmo 62-99Dokument6 SeitenRmo 62-99Klaters BokuNoch keine Bewertungen

- IEC 1956: General SpecificationsDokument4 SeitenIEC 1956: General SpecificationsdhananjaybaraikNoch keine Bewertungen

- Doctrines in Taxation: Prospectivity and ImprescriptibilityDokument14 SeitenDoctrines in Taxation: Prospectivity and Imprescriptibilityjuna luz latigayNoch keine Bewertungen

- Taxpayer's RemediesDokument5 SeitenTaxpayer's RemediesCel TanNoch keine Bewertungen

- The Building and Other Construction Workers Welfare Cess Rules, 1998Dokument9 SeitenThe Building and Other Construction Workers Welfare Cess Rules, 1998Rizwan PathanNoch keine Bewertungen

- PP 80 2007Dokument22 SeitenPP 80 2007davidwijaya1986Noch keine Bewertungen

- Appeals and Revision: After Studying This Chapter, You Will Be Able ToDokument25 SeitenAppeals and Revision: After Studying This Chapter, You Will Be Able TofirastiNoch keine Bewertungen

- Advance Rulings Authority PowersDokument3 SeitenAdvance Rulings Authority Powersrahulkapur87Noch keine Bewertungen

- ProsecutionDokument12 SeitenProsecutionParth UpadhyayNoch keine Bewertungen

- Social Security and Cess in Respect of Building and Other Construction WorkersDokument19 SeitenSocial Security and Cess in Respect of Building and Other Construction WorkersAkhil DheliaNoch keine Bewertungen

- Rmo 35-90Dokument4 SeitenRmo 35-90xina_acosta100% (1)

- Assment Audit RulsDokument3 SeitenAssment Audit RulsGovind kalsangraNoch keine Bewertungen

- Bureau of Internal Revenue: Deficiency Tax AssessmentDokument9 SeitenBureau of Internal Revenue: Deficiency Tax AssessmentXavier Cajimat UrbanNoch keine Bewertungen

- Commissioner of Internal Revenue Vs Kudos Metal Corporation Gr. No. 178087 May 5, 2010Dokument13 SeitenCommissioner of Internal Revenue Vs Kudos Metal Corporation Gr. No. 178087 May 5, 2010nildin danaNoch keine Bewertungen

- Securities and Exchange Board of India (Settlement Proceedings) Regulations, 2018 (Last Amended On July 22, 2020)Dokument63 SeitenSecurities and Exchange Board of India (Settlement Proceedings) Regulations, 2018 (Last Amended On July 22, 2020)Parag KabraNoch keine Bewertungen

- Appeals and Revision: After Studying This Chapter, You Will Be Able ToDokument25 SeitenAppeals and Revision: After Studying This Chapter, You Will Be Able ToAtul PaiNoch keine Bewertungen

- CIR Vs PAL - ConstructionDokument8 SeitenCIR Vs PAL - ConstructionEvan NervezaNoch keine Bewertungen

- SEBI (Settlement of Administrative and Civil Proceedings) Regulations, 2014Dokument37 SeitenSEBI (Settlement of Administrative and Civil Proceedings) Regulations, 2014Parag KabraNoch keine Bewertungen

- Judgment Cadila Healthcare 488902Dokument12 SeitenJudgment Cadila Healthcare 488902venkatNoch keine Bewertungen

- Research On Claim of Operational Creditors Who Failed To Submit Claims Within Prescribed Time LimitDokument3 SeitenResearch On Claim of Operational Creditors Who Failed To Submit Claims Within Prescribed Time LimitRishabh GoswamiNoch keine Bewertungen

- PPDA - Administrative Review 2023Dokument9 SeitenPPDA - Administrative Review 2023richard.musiimeNoch keine Bewertungen

- Appeals and Revision: After Studying This Chapter, You Will Be Able ToDokument39 SeitenAppeals and Revision: After Studying This Chapter, You Will Be Able TodeepaksinghalNoch keine Bewertungen

- Lascona vs. CIR (TAX)Dokument4 SeitenLascona vs. CIR (TAX)Teff QuibodNoch keine Bewertungen

- Stay Application RequirementsDokument8 SeitenStay Application RequirementsSHIVJEE yadavNoch keine Bewertungen

- CH 22 APPEAL - UnlockedDokument40 SeitenCH 22 APPEAL - UnlockedVANDANA GOYALNoch keine Bewertungen

- CH 22 APPEAL - UnlockedDokument40 SeitenCH 22 APPEAL - UnlockedVANDANA GOYALNoch keine Bewertungen

- Samar-I Electric Cooperative vs. CirDokument2 SeitenSamar-I Electric Cooperative vs. CirRaquel DoqueniaNoch keine Bewertungen

- 35 Review of Taxation: Rule 35Dokument2 Seiten35 Review of Taxation: Rule 35Pieter-Hendrik van der SchyfNoch keine Bewertungen

- RMO 35-90 Guidelines Re SDTDokument3 SeitenRMO 35-90 Guidelines Re SDTAvelino Garchitorena Alfelor Jr.Noch keine Bewertungen

- Taxpayer'S Obligations and Privileges: I. General Audit Procedures and DocumentationDokument4 SeitenTaxpayer'S Obligations and Privileges: I. General Audit Procedures and DocumentationKristen StewartNoch keine Bewertungen

- Week 10Dokument8 SeitenWeek 10Victor LimNoch keine Bewertungen

- 33 & 33aDokument4 Seiten33 & 33aSurya SriramNoch keine Bewertungen

- B&ocw Cess Act & RulesDokument5 SeitenB&ocw Cess Act & RulesRaghu RamNoch keine Bewertungen

- Taxation Review - Samar I Electric Cooperative Vs CIRDokument3 SeitenTaxation Review - Samar I Electric Cooperative Vs CIRMaestro LazaroNoch keine Bewertungen

- Appeals & Revision in Income TaxDokument9 SeitenAppeals & Revision in Income TaxTarun BhatiaNoch keine Bewertungen

- Lascona Land Vs CIRDokument3 SeitenLascona Land Vs CIRKM MacNoch keine Bewertungen

- Appeals: © The Institute of Chartered Accountants of IndiaDokument16 SeitenAppeals: © The Institute of Chartered Accountants of IndiaJitendra VernekarNoch keine Bewertungen

- Samar-I Electric Coop V CIR (2014) DigestDokument2 SeitenSamar-I Electric Coop V CIR (2014) Digestviktoriavillo67% (3)

- Introduction to Negotiable Instruments: As per Indian LawsVon EverandIntroduction to Negotiable Instruments: As per Indian LawsBewertung: 5 von 5 Sternen5/5 (1)

- How To Build Your Trading WatchlistDokument25 SeitenHow To Build Your Trading Watchlistpb41Noch keine Bewertungen

- Ninja Engulfing Reversal July 2011Dokument3 SeitenNinja Engulfing Reversal July 2011pb41Noch keine Bewertungen

- Hagerty, Kevin - 9 Ways To Improve Your TradingDokument4 SeitenHagerty, Kevin - 9 Ways To Improve Your Tradingartus14Noch keine Bewertungen

- 10 Ways To Improve Your Investment Process L Greg Speicher L 2011Dokument36 Seiten10 Ways To Improve Your Investment Process L Greg Speicher L 2011Vishesh SoodNoch keine Bewertungen

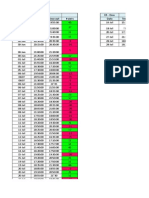

- Price Breaks ThroughDokument34 SeitenPrice Breaks Throughpb41Noch keine Bewertungen

- Depression The Homocysteine Hypothesis of DepressionDokument7 SeitenDepression The Homocysteine Hypothesis of Depressionpb41Noch keine Bewertungen

- What We Jews Believe - Samuel S. CohonDokument208 SeitenWhat We Jews Believe - Samuel S. Cohonpb41100% (2)

- Self Help - Everything We Wish We Had Learned About Life in School But Didn/'tDokument47 SeitenSelf Help - Everything We Wish We Had Learned About Life in School But Didn/'tElizabeth Lonbro100% (5)

- 12 Steps To Living Well EbookDokument15 Seiten12 Steps To Living Well Ebookpb41Noch keine Bewertungen

- Deed of Family Settlement Between Rival ClaimantsDokument4 SeitenDeed of Family Settlement Between Rival ClaimantsMahebub Ghante100% (1)

- All Contracts Are Agreements But All Agreements Are Not Contracts.Dokument14 SeitenAll Contracts Are Agreements But All Agreements Are Not Contracts.dasrk.95Noch keine Bewertungen

- Paulino vs. Court of AppealsDokument3 SeitenPaulino vs. Court of AppealsEl SitasNoch keine Bewertungen

- As 2124 2125 2127-1992 (Reference Use Only) General Conditions of ContractDokument7 SeitenAs 2124 2125 2127-1992 (Reference Use Only) General Conditions of ContractSAI Global - APACNoch keine Bewertungen

- Kimberly Covarrubias v. Citimortgage, Inc., 4th Cir. (2015)Dokument6 SeitenKimberly Covarrubias v. Citimortgage, Inc., 4th Cir. (2015)Scribd Government DocsNoch keine Bewertungen

- CBRE Zuidas Amsterdam (Jun 2013)Dokument16 SeitenCBRE Zuidas Amsterdam (Jun 2013)vdmaraNoch keine Bewertungen

- Persons Midterms CoverageDokument28 SeitenPersons Midterms CoverageKate MontenegroNoch keine Bewertungen

- RENT AGREEMENT AtrDokument4 SeitenRENT AGREEMENT AtrakashsattwikeeNoch keine Bewertungen

- NEW KIDS ON THE BLOCK v. NEWS AMERICA PUBLISHINGDokument2 SeitenNEW KIDS ON THE BLOCK v. NEWS AMERICA PUBLISHINGCedricNoch keine Bewertungen

- Cuaycong vs. Benedicto.Dokument17 SeitenCuaycong vs. Benedicto.Ivn Maj NopuenteNoch keine Bewertungen

- City Officials Dispute Tax Sale Redemption PeriodDokument11 SeitenCity Officials Dispute Tax Sale Redemption PeriodAlfie OmegaNoch keine Bewertungen

- Vicarious LiabilityDokument6 SeitenVicarious LiabilityJoey WongNoch keine Bewertungen

- Social Media Marketing AgreementDokument3 SeitenSocial Media Marketing AgreementSoniya Agarwal100% (3)

- Affidavit FormDokument3 SeitenAffidavit FormmaryNoch keine Bewertungen

- Notes in Succession Dean Navarros LectureDokument49 SeitenNotes in Succession Dean Navarros LectureBea de Leon100% (1)

- Tamil Nadu Ordinance On Area Sabha and Ward CommittesDokument10 SeitenTamil Nadu Ordinance On Area Sabha and Ward Committesurbangovernance99Noch keine Bewertungen

- RMC 46-99Dokument7 SeitenRMC 46-99mnyng100% (1)

- Roque Vs LapuzDokument2 SeitenRoque Vs LapuzJames Evan I. ObnamiaNoch keine Bewertungen

- Valerie Kinnon v. Arcoub, Gopman & Assocs., 490 F.3d 886, 11th Cir. (2007)Dokument9 SeitenValerie Kinnon v. Arcoub, Gopman & Assocs., 490 F.3d 886, 11th Cir. (2007)Scribd Government DocsNoch keine Bewertungen

- Davao Light and Power Co p6Dokument2 SeitenDavao Light and Power Co p6Tet DomingoNoch keine Bewertungen

- SPA - Joana Mae Cagurangan EchonDokument2 SeitenSPA - Joana Mae Cagurangan EchonMiguel CasimNoch keine Bewertungen

- RRB c03-2015 Silliguri ResultDokument4 SeitenRRB c03-2015 Silliguri ResultVikashKumarNoch keine Bewertungen

- CD - 38. Torres Vs LApinidDokument2 SeitenCD - 38. Torres Vs LApinidCzarina CidNoch keine Bewertungen

- United Airlines Supreme Court Ruling on Discrimination CaseDokument9 SeitenUnited Airlines Supreme Court Ruling on Discrimination CaseImport Back upNoch keine Bewertungen

- Letter To Follow Time ScheduleDokument2 SeitenLetter To Follow Time ScheduleAjay KumarNoch keine Bewertungen

- 05-Civil Registration of Kingdom of CambodiaDokument32 Seiten05-Civil Registration of Kingdom of CambodiaPhearun PayNoch keine Bewertungen

- Script AgreementDokument2 SeitenScript AgreementKripa SaravananNoch keine Bewertungen

- Gordley. ConsiderationDokument7 SeitenGordley. ConsiderationValeria ButorinaNoch keine Bewertungen

- Debt dispute letter to collections agencyDokument5 SeitenDebt dispute letter to collections agencyACNoch keine Bewertungen

- Effects of Conditions Precedent in Building ContractsDokument5 SeitenEffects of Conditions Precedent in Building ContractsPameswaraNoch keine Bewertungen