Das könnte Ihnen auch gefallen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Personal Loan AgreementDokument3 SeitenPersonal Loan AgreementMj AndesNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- 04 Park ISM ch04 PDFDokument28 Seiten04 Park ISM ch04 PDFBenn DoucetNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Clarity Inquiry #4y8tjzb6g4Dokument56 SeitenClarity Inquiry #4y8tjzb6g4Patricia CarvajalNoch keine Bewertungen

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Loan-Level Price Adjustment (LLPA) MatrixDokument8 SeitenLoan-Level Price Adjustment (LLPA) MatrixLashon SpearsNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- REVIEWDokument2 SeitenREVIEWJulie Anne DanteNoch keine Bewertungen

- TVOM Theory QuizDokument2 SeitenTVOM Theory QuizKim DavilloNoch keine Bewertungen

- Reflective Writing For Mortgage ProjectDokument2 SeitenReflective Writing For Mortgage Projectapi-355663066Noch keine Bewertungen

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Master of Arts in EconomicsDokument82 SeitenMaster of Arts in EconomicsArchakam RakshithaNoch keine Bewertungen

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- 856437638Dokument5 Seiten856437638FierDaus Mfmm0% (1)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- SabrDokument1.359 SeitenSabr007hanaNoch keine Bewertungen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Bachelor of Art B.A (Compulsory) : Directorate of Distance Education Swami Vivekanand Subharti University III YearDokument4 SeitenBachelor of Art B.A (Compulsory) : Directorate of Distance Education Swami Vivekanand Subharti University III YearUMANG COMPUTERSNoch keine Bewertungen

- Quantity Theory of MoneyDokument8 SeitenQuantity Theory of MoneySamin SakibNoch keine Bewertungen

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Loan Detail & Fee WorksheetDokument1 SeiteLoan Detail & Fee WorksheetEricNoch keine Bewertungen

- My Mortgage: Click Here FAQ'sDokument1 SeiteMy Mortgage: Click Here FAQ'smaria elenaNoch keine Bewertungen

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Mitchell Blandino 1Dokument12 SeitenMitchell Blandino 1api-610323726Noch keine Bewertungen

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Rising Interest RatesDokument4 SeitenRising Interest RatesRAJESH BHANDERINoch keine Bewertungen

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- Zarro Inference 3 The Affidavits of Michael ZarroDokument190 SeitenZarro Inference 3 The Affidavits of Michael ZarroDeontosNoch keine Bewertungen

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Interest Rate Lock AgreementDokument2 SeitenInterest Rate Lock AgreementSarahi AlvarengaNoch keine Bewertungen

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Conditions Home MortgageDokument77 SeitenConditions Home MortgageamfipolitisNoch keine Bewertungen

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Define Pledge, Hypothecation and MortgageDokument3 SeitenDefine Pledge, Hypothecation and MortgageMuhammadAliNoch keine Bewertungen

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Lesson 9. Amortization of DebtsDokument23 SeitenLesson 9. Amortization of DebtsLorenaNoch keine Bewertungen

- EMI CalculatorDokument7 SeitenEMI Calculatorarunasagar_2011Noch keine Bewertungen

- Jan Notices Q 12 15 09Dokument200 SeitenJan Notices Q 12 15 09TRISTARUSANoch keine Bewertungen

- Home Direct Ebook - How To Finance Your Manufactured HomeDokument28 SeitenHome Direct Ebook - How To Finance Your Manufactured HomexNoch keine Bewertungen

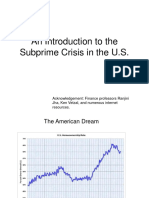

- An Introduction To The Subprime Crisis in The U.SDokument25 SeitenAn Introduction To The Subprime Crisis in The U.SAdeel RanaNoch keine Bewertungen

- Fama 1981Dokument22 SeitenFama 1981Marcelo BalzanaNoch keine Bewertungen

- 504 Loan Refinancing ProgramDokument5 Seiten504 Loan Refinancing ProgramPropertywizzNoch keine Bewertungen

- Debt Consolidation TipsDokument6 SeitenDebt Consolidation TipsKrittiNoch keine Bewertungen

- 8765511.1 1 CostofBorrowingPackage 20201230 095517HPMZWDokument7 Seiten8765511.1 1 CostofBorrowingPackage 20201230 095517HPMZWsabNoch keine Bewertungen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Week 3 - Ian Benedict - Everything You Need To Know About Housing Loans in The PhilippinesDokument4 SeitenWeek 3 - Ian Benedict - Everything You Need To Know About Housing Loans in The PhilippinesDon J AsuncionNoch keine Bewertungen

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)