Das könnte Ihnen auch gefallen

- Modeling of Purchase and Sales Contracts in Supply Chain OptimizationDokument43 SeitenModeling of Purchase and Sales Contracts in Supply Chain OptimizationDemocracia real YANoch keine Bewertungen

- People, Environment and Democracy Before Profit and Corporate RightsDokument7 SeitenPeople, Environment and Democracy Before Profit and Corporate RightsDemocracia real YANoch keine Bewertungen

- Future Scenarios For The EurozoneDokument41 SeitenFuture Scenarios For The EurozoneYannis KoutsomitisNoch keine Bewertungen

- TTIP - Cross-Cutting Disciplines and Institutional ProvisionsDokument4 SeitenTTIP - Cross-Cutting Disciplines and Institutional ProvisionsDemocracia real YANoch keine Bewertungen

- 7DIFDokument63 Seiten7DIFgalm8807Noch keine Bewertungen

- Privatisation ProgrammeDokument27 SeitenPrivatisation ProgrammeCostas EfimerosNoch keine Bewertungen

- EU Ukraine Association Agreement EnglishDokument906 SeitenEU Ukraine Association Agreement Englishbi2458Noch keine Bewertungen

- James A. Yunker - Socialism Revised and Modernized. The Case For Pragmatic Socialism.Dokument360 SeitenJames A. Yunker - Socialism Revised and Modernized. The Case For Pragmatic Socialism.Democracia real YA0% (1)

- The Neo-Marxist Synthesis of Marx and Weber On ClassDokument24 SeitenThe Neo-Marxist Synthesis of Marx and Weber On ClassHamidEshaniNoch keine Bewertungen

- Joint Statement On Syria - The White HouseDokument1 SeiteJoint Statement On Syria - The White HouseDemocracia real YANoch keine Bewertungen

- Naoki Yoshihara - Reexamination of Marxian Explotation TheoryDokument35 SeitenNaoki Yoshihara - Reexamination of Marxian Explotation TheoryDemocracia real YANoch keine Bewertungen

- Greg Palast MemoDokument1 SeiteGreg Palast Memorichardck61Noch keine Bewertungen

- John E. Roemer - An Anti-Hayekian ManifestoDokument19 SeitenJohn E. Roemer - An Anti-Hayekian ManifestoDemocracia real YANoch keine Bewertungen

- The Brussels EU DictatorshipDokument32 SeitenThe Brussels EU DictatorshipDemocracia real YANoch keine Bewertungen

- André Gorz - From Strategy For LaborDokument16 SeitenAndré Gorz - From Strategy For LaborDemocracia real YANoch keine Bewertungen

- W. Wagner - DSF Policy Briefs 10.01.2012 - Eurobonds Are Likely To Increase The Risk of Joint Defaults in The Eurozone.Dokument3 SeitenW. Wagner - DSF Policy Briefs 10.01.2012 - Eurobonds Are Likely To Increase The Risk of Joint Defaults in The Eurozone.Democracia real YANoch keine Bewertungen

- The Euro Area Adjustment-About Half-Way ThereDokument16 SeitenThe Euro Area Adjustment-About Half-Way ThereGlinta CataNoch keine Bewertungen

- T. Herndon, M. Asch, R. Pollin - Does High Public Debt Consistently Stifle Economic Growth. A Critique of Reinhart and RogoffDokument26 SeitenT. Herndon, M. Asch, R. Pollin - Does High Public Debt Consistently Stifle Economic Growth. A Critique of Reinhart and RogoffDemocracia real YANoch keine Bewertungen

- Wolfson Prize Winner - Bootle - Leaving The EuroDokument189 SeitenWolfson Prize Winner - Bootle - Leaving The Euroonat85Noch keine Bewertungen

- Gerald Crabtree - Trends in Genetics. Our Fragile IntellectDokument6 SeitenGerald Crabtree - Trends in Genetics. Our Fragile IntellectDemocracia real YA100% (1)

- Takashi Satoh - The Mathematical Marxian Theory of Capital Accumulation and The Post-Keynesian Theory of Monetary Circuit. A SynthesisDokument21 SeitenTakashi Satoh - The Mathematical Marxian Theory of Capital Accumulation and The Post-Keynesian Theory of Monetary Circuit. A SynthesisDemocracia real YANoch keine Bewertungen

- Letter Express Yourself Against Nobel Peace PrizeDokument1 SeiteLetter Express Yourself Against Nobel Peace PrizeDemocracia real YANoch keine Bewertungen

- Irving Fisher - La Teoría de La Deuda-Deflación en Las Grandes DepresionesDokument22 SeitenIrving Fisher - La Teoría de La Deuda-Deflación en Las Grandes DepresionesDemocracia real YANoch keine Bewertungen

- Steve Keen, UWS Australia - A Marx For Post-KeynesiansDokument18 SeitenSteve Keen, UWS Australia - A Marx For Post-KeynesiansDemocracia real YANoch keine Bewertungen

- Spain - Memorandum of Understanding On Financial Sector Policy ConditionalityDokument20 SeitenSpain - Memorandum of Understanding On Financial Sector Policy ConditionalityDemocracia real YANoch keine Bewertungen

- EIR - There's Life After The Euro. An Economic Miracle For The MediterreneanDokument8 SeitenEIR - There's Life After The Euro. An Economic Miracle For The MediterreneanDemocracia real YANoch keine Bewertungen

- MOU (Spain FFA Post EWG Clean) - Contrato de La Asistencia Financiera Con EuropaDokument74 SeitenMOU (Spain FFA Post EWG Clean) - Contrato de La Asistencia Financiera Con EuropaDemocracia real YANoch keine Bewertungen

- Private Banking 2012Dokument7 SeitenPrivate Banking 2012Patricia DillonNoch keine Bewertungen

- Dimitris From Greece - The Truth About GreeceDokument28 SeitenDimitris From Greece - The Truth About GreeceDemocracia real YA100% (1)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Aescartin/Tlopez/Jpapa: Mobile Telephone GmailDokument7 SeitenAescartin/Tlopez/Jpapa: Mobile Telephone GmailReynalyn BarbosaNoch keine Bewertungen

- 1231.3376.01 -ל הרמהל ח"גאמ - Convertible ArbitrageDokument3 Seiten1231.3376.01 -ל הרמהל ח"גאמ - Convertible ArbitrageitzikhevronNoch keine Bewertungen

- Exercise Invesment Financial AccountingDokument7 SeitenExercise Invesment Financial Accountingukandi rukmanaNoch keine Bewertungen

- NCB Saudi ArabiaDokument3 SeitenNCB Saudi ArabiaAbdul HaseebNoch keine Bewertungen

- Ratio Analysis ReportDokument121 SeitenRatio Analysis ReportChandrakant ChopdeNoch keine Bewertungen

- Uladzislau KharashkevichDokument7 SeitenUladzislau KharashkevichHarry BurgeNoch keine Bewertungen

- Profitability Turnover RatiosDokument32 SeitenProfitability Turnover RatiosAnushka JindalNoch keine Bewertungen

- Basic FinanceDokument3 SeitenBasic Financezandro_ico5041Noch keine Bewertungen

- Multinational Financial ManagementDokument95 SeitenMultinational Financial ManagementANoch keine Bewertungen

- E - Challan Government of Haryana E - Challan Government of HaryanaDokument1 SeiteE - Challan Government of Haryana E - Challan Government of HaryanaAmit KumarNoch keine Bewertungen

- Case Study - Stock Pitch GuideDokument7 SeitenCase Study - Stock Pitch GuideMuyuchen Shi100% (1)

- When Are Personal Loans A Good Idea?Dokument2 SeitenWhen Are Personal Loans A Good Idea?Sandeep KumarNoch keine Bewertungen

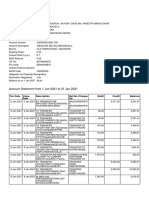

- Sbi Account Jan 2021Dokument2 SeitenSbi Account Jan 2021Manoj GaurNoch keine Bewertungen

- Responsibility Centers: Revenue and Expense Centers: Summary of Chapter 4-Assignment 2Dokument4 SeitenResponsibility Centers: Revenue and Expense Centers: Summary of Chapter 4-Assignment 2Indah IndrianiNoch keine Bewertungen

- Its Function, Performance, and Potential As An Investment OpportunityDokument20 SeitenIts Function, Performance, and Potential As An Investment OpportunityGvantsa MorchadzeNoch keine Bewertungen

- Security Valuations - Stocks EZDokument9 SeitenSecurity Valuations - Stocks EZAakash RegmiNoch keine Bewertungen

- Draft SciDokument5 SeitenDraft SciMariella Antonio-NarsicoNoch keine Bewertungen

- 1.false 2. True 3. False 4. True 5. False 6. False 7. True 8. False 9. False 10. FALSEDokument9 Seiten1.false 2. True 3. False 4. True 5. False 6. False 7. True 8. False 9. False 10. FALSEHazel Kaye EspelitaNoch keine Bewertungen

- Basic Account 1Dokument10 SeitenBasic Account 1COMPUTER WORLDNoch keine Bewertungen

- Basel-III Norms and Indian Financial SystemDokument3 SeitenBasel-III Norms and Indian Financial SystemNavneet MayankNoch keine Bewertungen

- Bitcoin RoughDokument19 SeitenBitcoin RoughSaloni Jain 1820343Noch keine Bewertungen

- SHEKAR - Rural BankingDokument20 SeitenSHEKAR - Rural BankingkizieNoch keine Bewertungen

- The Asian Crisis and Recent DevelopmentDokument30 SeitenThe Asian Crisis and Recent DevelopmentfabyunaaaNoch keine Bewertungen

- National Income New PDFDokument25 SeitenNational Income New PDFLaksh SahniNoch keine Bewertungen

- "Credit Risk Management": Tribhuvan University Faculty of Management A Project Proposal OnDokument14 Seiten"Credit Risk Management": Tribhuvan University Faculty of Management A Project Proposal Onrk shahNoch keine Bewertungen

- F5 - 14financial Performance MeasurementDokument7 SeitenF5 - 14financial Performance Measurementsajid newaz khanNoch keine Bewertungen

- 39 1 Vijay KelkarDokument14 Seiten39 1 Vijay Kelkargrooveit_adiNoch keine Bewertungen

- Hyundai KiaDokument3 SeitenHyundai KiaIra PutriNoch keine Bewertungen

- Mini Case: Shrewsbury Herbal Products, LTDDokument7 SeitenMini Case: Shrewsbury Herbal Products, LTDSriSaraswathy100% (1)

- Xpress Money - API - 2.0 Manadtory PDFDokument52 SeitenXpress Money - API - 2.0 Manadtory PDFvinuNoch keine Bewertungen