Oil Market Report

Iran sanctions start to bite

8 OCTOBER 2012

SEB Oil Market Report

Crude oil market

Looking back over Q3, Brent posted yet another turbulent quarter, trading at an average price of $109.4/b, $0.6/b below our forecast. With several major bullish and bearish factors still in play we doubt the oil market will be much calmer in Q4 either. However, we regard $110/b as a sound reference point for Brent, discounting as it does major macroeconomic and geopolitical uncertainties reasonably well. It also ensures cash flows remain strong enough to drive much needed investments in future supply. According to our main scenario, while H1-13 will be seasonally softer, crude oil prices should recover in H2-13 as macroeconomic conditions stabilize. Obvious short- to medium-term downside risks include the possibility that sanctions may force Iran back to the negotiating table, potential US SPR releases and uncertain Chinese demand. Entering Q4 the market balance remains loose even though maintenance work in several oil-producing regions has led to occasional supply disruptions lately. In addition to Iran, the biggest supply side concern currently is the prolonged North Sea maintenance outage delaying almost all planned October loadings. Meanwhile, evidence of strong late summer production is being received from several regions including Russia (which reported a post-Soviet era high of 10.4 mb/d), the US (posting its biggest production volume since the mid-1990s at 6.5 mb/d) and Iraq (3.4 mb/d). As regards both the US and Iraq, we think it highly likely output will continue to increase further over the coming year. MENA geopolitical influences on oil markets could be both bullish and bearish. Negatively, Iran shows signs of buckling under pressure of sanctions. Cracks are starting to appear here and there, inflation being one. Fuel shortage combined with pre-winter restocking seems to have been an important driver behind the recent surge in inflation. The resulting increasing social unrest is the last thing Iranian leaders want. So far the government has enjoyed massive popular support for its nuclear energy programme. However, if living conditions continue to deteriorate this could of course change. Consequently, Iran may potentially seek to re-enter negotiations, and to make limited concessions. Tentative initiatives have already been announced. We still consider the risk of an attack on the country as very low. Its leadership is unlikely to be seeking armed conflict, which is therefore only likely to result from an error of judgement rather than any determined intention to go to war. Elsewhere, tension is increasing along the Syrian border with Turkey after several Turks were killed by a probably unintentional Syrian grenade attack. In response Turkey has shelled Syrian positions and called on both fellow NATO members and the UN Security Council to guarantee their safety. These developments provide the West with further reason to bring down the Assad regime though it also increases the risk that Iran will become more involved in the conflict.

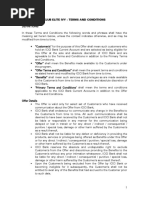

Crude oil price

(NYMEX/ICE, $/b, front month, daily closing)

10 3 15 2 10 2 15 1 10 1 15 0 10 0 9 5 9 0 8 5 8 0 7 5 7 0 ja -10 n fe -1 b 0 m r-1 a 0 a r-1 p 0 m j-1 a 0 ju -10 n ju l-10 ag 0 u -1 se -1 p 0 o 0 kt-1 n v-1 o 0 d c-1 e 0 ja -11 n fe -1 b 1 m r-1 a 1 a r-1 p 1 m j-1 a 1 ju -11 n ju l-11 ag 1 u -1 se -1 p 1 o 1 kt-1 n v-1 o 1 d c-1 e 1 ja -12 n fe -1 b 2 m r-1 a 2 a r-1 p 2 m j-1 a 2 ju -12 n ju l-12 ag 2 u -1 se -1 p 2 o 2 kt-1 6 5 N EXW I YM T IC Bre t E n

IEA global crude oil demand estimates

(mb/d)

9 2 9 1 9 0 8 9 8 8 8 7 8 6 8 5 8 4 8 3 8 2 8 1 8 0 7 9 a r-1 p 0 a r-1 p 1 a r-1 p 2 o 9 kt-0 ja -1 n 0 o 0 kt-1 ja -1 n 1 o 1 kt-1 ja -1 n 2 ju 9 l-0 ju 0 l-1 ju 1 l-1 ju 2 l-1 21 00 21 01 21 02 21 03

Chart Sources: IEA, Bloomberg, SEB Commodity Research

Monthly global crude oil demand estimates

2012 (mb/d) 89.8 89.09 88.74 Revision (kb/d) +130 +260 +30 2013 (mb/d) 90.6 90.10 89.55 Revision (kb/d) +90 +400 +30

IEA EIA OPEC

SEB average Brent crude oil price forecast

($/b) 2012 2013 2014 Q1 105 Q2 105 Q3 115 Q4 110 115 Full Year 111.8 110.0 115.0

10 0

12 0

14 0

16 0

18 0

10 1

12 1

14 1

10 0

10 1

10 2

10 3

10 4

10 5

100 000

n v-1 o 2 fe -1 b 3 9 2 9 4 9 6 9 8

1 0 20 03 20 04 20 05 20 06 20 07 20 08 20 09 21 00 21 01 21 02

2 0

3 0

4 0

5 0

6 0

7 0

8 0

9 0

100 500

200 000

200 500

300 000

300 500

400 000

400 500

500 00

m j-1 a 3 ag 3 u -1 n v-1 o 3 fe -1 b 4 m j-1 a 4 ag 4 u -1 n v-1 o 4 fe -1 b 5 m j-1 a 5 ag 5 u -1 n v-1 o 5 fe -1 b 6 m j-1 a 6 ag 6 u -1 n v-1 o 6 1 -1 -0 2 0 5 1 -0 -0 2 9 5 1 -0 -0 2 8 3

(ICE, $/b)

Crude oil

Crude oil price

20 07

SEB Oil Market Report

IC B n E re t

N M WI Y EX T

Brent futures curve

20 08

Speculative positions WTI

Nt e

Ln og

Sh rt o

Chart Sources: Bloomberg, SEB Commodity Research

20 09

(NYMEX, lots, futures and options, weekly data)

(NYMEX/ICE, $/b, front month, weekly closing)

21 00

21 01

21 02

8 7

8 8

8 9

9 0

9 1

9 2

9 3

9 4

9 5

9 6

9 7

9 8

(NYMEX, $/b)

(daily closing)

n v-1 o 2 fe -1 b 3 m j-1 a 3 ag 3 u -1 n v-1 o 3 fe -1 b 4 m j-1 a 4 ag 4 u -1 n v-1 o 4 fe -1 b 5 m j-1 a 5 ag 5 u -1 n v-1 o 5 fe -1 b 6 m j-1 a 6 ag 6 u -1 n v-1 o 6 1 -1 -0 2 0 5 1 -0 -0 2 9 5 1 -0 -0 2 8 3

WTI futures curve

Benchmark spreads

12 month time spread

(NYMEX/ICE, %, daily closing, >0: contango, <0: backwardation)

8 6 4 2 0 -2 -4 -6 -8 -1 0 -1 2 -1 4 -1 6 -1 8 -2 0 -2 2 -2 4 -2 6 -2 8

1 8 1 6 1 4 1 2

-4 -6 -8 -1 0

1 0 8 6 4 2 0 -2

W I m u Bre t T in s n Bre t m u D b i n in s u a Bre t m u U ls n in s ra

IC B n E re t

N EXW I YM T

ja -1 n 0 fe -1 b 0 m r-1 a 0 a r-1 p 0 m j-1 a 0 ju -1 n 0 ju 0 l-1 ag 0 u -1 se -1 p 0 o 0 kt-1 n v-1 o 0 d c-1 e 0 ja -1 n 1 fe -1 b 1 m r-1 a 1 a r-1 p 1 m j-1 a 1 ju -1 n 1 ju 1 l-1 ag 1 u -1 se -1 p 1 o 1 kt-1 n v-1 o 1 d c-1 e 1 ja -1 n 2 fe -1 b 2 m r-1 a 2 a r-1 p 2 m j-1 a 2 ju -1 n 2 ju 2 l-1 ag 2 u -1 se -1 p 2 o 2 kt-1

ja -1 n 0 fe -1 b 0 m r-1 a 0 a r-1 p 0 m j-1 a 0 ju -1 n 0 ju 0 l-1 ag 0 u -1 se -1 p 0 o 0 kt-1 n v-1 o 0 d c-1 e 0 ja -1 n 1 fe -1 b 1 m r-1 a 1 a r-1 p 1 m j-1 a 1 ju -1 n 1 ju 1 l-1 ag 1 u -1 se -1 p 1 o 1 kt-1 n v-1 o 1 d c-1 e 1 ja -1 n 2 fe -1 b 2 m r-1 a 2 a r-1 p 2 m j-1 a 2 ju -1 n 2 ju 2 l-1 ag 2 u -1 se -1 p 2 o 2 kt-1

SEB Oil Market Report

Crude oil

US crude oil inventories

(DOE, mb, weekly data)

3 90 3 80 3 70 3 60 3 50

c

OECD total industry oil stocks

(mb, monthly data)

20 80 27 75 25 70 22 75 20 70 27 65 25 60 22 65 5 ye r ra g , to a ne p 5 ye r ra g , b tto a ne o m 21 02 5 ye r a e g a v ra e

3 40 3 30 3 20 3 10 j f m a m j j a s o n d 5 ye av ar erag e 2 1 01 2 2 01

20 60 27 55 25 50 22 55 j f m a m j j a s o n d

OECD Europe industry oil stocks

(mb, monthly data)

13 00 12 00 11 00 10 00 90 9 90 8 90 7 90 6 90 5 5 ye r ra g , to a ne p 5 ye r ra g , b tto a ne o m 21 02 5 ye r a e g a v ra e

OECD North America industry oil stocks

(mb, monthly data)

10 40 17 35 15 30 12 35 10 30 17 25 15 20 12 25 5 ye r ra g , to a ne p 5 ye r ra g , b tto a ne o m 21 02 5 ye r a e g a v ra e

90 4 90 3 90 2 j f m a m j j a s o n d 10 20 17 15 j f m a m j j a s o n d

OECD Asia & Oceania industry oil stocks

(mb, monthly data)

40 5 45 4 40 4 45 3 40 3 45 2 40 2 45 1 40 1 45 0 40 0 35 9 30 9 35 8 30 8 35 7 j f m a m j j a s o n d 5 ye r ra g , to a ne p 5 ye r ra g , b tto a ne o m 21 02 5 ye r a e g a v ra e

OPEC production

(kb/d, monthly data)

300 30 300 20 300 10 300 00 200 90 200 80 200 70 200 60 200 50 ja -0 n 8 m r-0 a 8 m j-0 a 8 ju 8 l-0 se -0 p 8 n v-0 o 8 ja -0 n 9 m r-0 a 9 m j-0 a 9 ju 9 l-0 se -0 p 9 n v-0 o 9 ja -1 n 0 m r-1 a 0 m j-1 a 0 ju 0 l-1 se -1 p 0 n v-1 o 0 ja -1 n 1 m r-1 a 1 m j-1 a 1 ju 1 l-1 se -1 p 1 n v-1 o 1 ja -1 n 2 m r-1 a 2 m j-1 a 2 ju 2 l-1 se -1 p 2 200 40 O EC 2 p d ctio P -1 ro u n O EC 1 p d ctio P -1 ro u n

Chart Sources: Bloomberg, IEA, SEB Commodity Research

SEB Oil Market Report

European oil product markets

The Atlantic basin maintenance season is in full swing with around 2 mb/d of refinery capacity off-line compared to September. Generally, outages are fairly equally divided between North America and Europe. The European maintenance season will continue through October and into November keeping particularly middle distillate supply uncomfortably tight. Additional disturbances or an upturn in demand could easily send prices sharply higher. Tight supply ensures the economics of European refining remain highly satisfactory with the heavy end the only part of the barrel reporting weak crack spreads. With the maintenance season continuing, product inventories low and pre-winter restocking demand still modest, there are currently few reasons to expect crack spreads generally to fall, other than of course their present high levels. Light ends: The European naphtha market has largely stabilized in recent months. Inventories have decreased due to eastbound arbitrage cargoes, and the petrochemical industry preferring naphtha to higher priced propane. The naphtha crack has also largely normalized. The gasoline market is more bullish with abnormally low stocks on both sides of the Atlantic and additional support being provided by US supply disruptions. Indeed, West Coast retailers have reportedly run out of California grade gasoline from time to time. However, an already very strong crack and upcoming seasonally low demand suggest gasoline is as strong as it is likely to be in relative terms. Middle distillates: The middle part of the barrel remains very tight, even before substantial pre-winter restocking. While consumers have, until now, been relatively passive, when temperatures start to drop restocking will inevitably accelerate. Excepting gasoil, European inventories are very low. Even though gasoil inventories are more normal, they have shown some signs of falling back lately. In addition, US distillate inventories are weak, reducing potential arbitrage flows to Europe. While jet fuel demand is seasonally declining, cracks remain supported by low inventories and refineries focusing on the even tighter diesel market. Some middle distillate arbitrage flows into Europe during October should, to some extent, help stabilize the market. Heavy ends: Unlike the rest of the barrel the heavy end mainly shows signs of weakness. Demand is lacklustre and European inventories fairly normal despite eastbound arbitrage flows. At the receiving end the demand outlook remains unclear due to the uncertain Chinese economic outlook. Changes in market sentiment will probably also come from Asia. Improvements to the LS vs. HS supply situation have narrowed the Hi-Lo spread after it recently hit its highest level in over 12 months.

European light end benchmarks

($/t, daily closing)

10 20 15 10 10 10 15 00 10 00 90 5 90 0 80 5 80 0 70 5 70 0 60 5 ja -10 n fe -1 b 0 m r-1 a 0 a r-1 p 0 m j-1 a 0 ju -10 n ju l-10 ag 0 u -1 se -1 p 0 o 0 kt-1 n v-1 o 0 d c-1 e 0 ja -11 n fe -1 b 1 m r-1 a 1 a r-1 p 1 m j-1 a 1 ju -11 n ju l-11 ag 1 u -1 se -1 p 1 o 1 kt-1 n v-1 o 1 d c-1 e 1 ja -12 n fe -1 b 2 m r-1 a 2 a r-1 p 2 m j-1 a 2 ju -12 n ju l-12 ag 2 u -1 se -1 p 2 o 2 kt-1 J t fu l e e D se 1 p m ie l 0 p G so 0 % a il .1 60 0 N p th ah a G so e a lin

European middle distillate benchmarks

($/t, daily closing)

15 10 10 10 15 00 10 00 90 5 90 0 80 5 80 0 70 5 70 0 60 5 60 0 50 5

European fuel oil benchmarks

($/t, daily closing)

80 0 75 7 70 5 75 2 70 0 65 7 60 5 65 2 60 0 55 7 50 5 55 2 50 0 45 7 40 5 45 2 40 0 35 7 30 5 H h su h r fu l o (3 % ig lp u e il .5 ) L w su h r fu l o (1 % o lp u e il .0 )

Chart Sources: Bloomberg, SEB Commodity Research

ja -1 n 0 fe -1 b 0 m r-1 a 0 a r-1 p 0 m j-1 a 0 ju -1 n 0 ju 0 l-1 ag 0 u -1 se -1 p 0 o 0 kt-1 n v-1 o 0 d c-1 e 0 ja -1 n 1 fe -1 b 1 m r-1 a 1 a r-1 p 1 m j-1 a 1 ju -1 n 1 ju 1 l-1 ag 1 u -1 se -1 p 1 o 1 kt-1 n v-1 o 1 d c-1 e 1 ja -1 n 2 fe -1 b 2 m r-1 a 2 a r-1 p 2 m j-1 a 2 ju -1 n 2 ju 2 l-1 ag 2 u -1 se -1 p 2 o 2 kt-1

ja -1 n 0 fe -1 b 0 m r-1 a 0 a r-1 p 0 m j-1 a 0 ju -1 n 0 ju 0 l-1 ag 0 u -1 se -1 p 0 o 0 kt-1 n v-1 o 0 d c-1 e 0 ja -1 n 1 fe -1 b 1 m r-1 a 1 a r-1 p 1 m j-1 a 1 ju -1 n 1 ju 1 l-1 ag 1 u -1 se -1 p 1 o 1 kt-1 n v-1 o 1 d c-1 e 1 ja -1 n 2 fe -1 b 2 m r-1 a 2 a r-1 p 2 m j-1 a 2 ju -1 n 2 ju 2 l-1 ag 2 u -1 se -1 p 2 o 2 kt-1

SEB Oil Market Report

Oil products

US gasoline and distillate inventories

(DOE, mb, weekly data)

20 4 20 3 20 2 20 1 20 0 10 9 10 8 10 7 10 6 10 5 10 4 10 3 10 2 10 1 j f m a m j j a s o n d G so e 5 ye r a e g a lin a v ra e G so e 2 1 a lin 0 2 D istilla fu l o 5 ye r a e g te e il a v ra e D istilla fu l o 2 1 te e il 0 2

US product benchmarks

(NYMEX, /gal, front month, daily closing)

30 6 30 5 30 4 30 3 30 2 30 1 30 0 20 9 20 8 20 7 20 6 20 5 20 4 20 3 20 2 20 1 20 0 10 9 10 8 G so e a lin H a go e tin il

US refinery utilization

(%, weekly data)

9 3 9 2 9 1 9 0 8 9 8 8 8 7 8 6 8 5 8 4 8 3 8 2 8 1 j f m a m j j a s o n d 2 0 -2 1 a g 07 01 v. 21 02

ICE Gasoil and European premiums to Gasoil

($/t, daily closing)

10 10 15 00 10 00 90 5 90 0 80 5 80 0 70 5 70 0 60 5 60 0 50 5 IC G so 0 % (le E a il .1 ft) J t fu l p m m (rig t) e e re iu h D se 1 p m p m m (rig t) ie l 0 p re iu h 10 1 10 0 9 0 8 0 7 0 6 0 5 0 4 0 3 0 2 0 1 0 0 -1 0 -2 0

European product cracks

($/b, daily closing)

3 5 3 0 2 5 2 0 1 5 1 0 5 0 -5 -1 0 -1 5 -2 0 ja -1 n 0 fe -1 b 0 m 0 ar-1 a 0 pr-1 m 0 aj-1 ju -1 n 0 jul-1 0 au -1 g 0 se -1 p 0 o 0 kt-1 n ov-1 0 de 0 c-1 ja -1 n 1 fe -1 b 1 m 1 ar-1 a 1 pr-1 m 1 aj-1 ju -1 n 1 jul-1 1 au -1 g 1 se -1 p 1 o 1 kt-1 n ov-1 1 de 1 c-1 ja -1 n 2 fe -1 b 2 m 2 ar-1 a 2 pr-1 m 2 aj-1 ju -1 n 2 jul-1 2 au -1 g 2 se -1 p 2 o 2 kt-1 -2 5 N ph a a th J t fue e l L w su h fu o o lp ur el il D sel 1 pp ie 0 m G so a line G so 0 a il .1% H h sulp ur fu l o ig h e il

European low - high sulphur fuel oil differential

($/t, daily closing)

7 5 7 0 6 5 6 0 5 5 5 0 4 5 4 0 3 5 3 0 2 5 2 0 1 5 1 0 5 0 -5 -1 0 -1 5

Chart Sources: Bloomberg, SEB Commodity Research

ja -1 n 0 fe -1 b 0 m r-1 a 0 a r-1 p 0 m j-1 a 0 ju -1 n 0 ju 0 l-1 ag 0 u -1 se -1 p 0 o 0 kt-1 n v-1 o 0 d c-1 e 0 ja -1 n 1 fe -1 b 1 m r-1 a 1 a r-1 p 1 m j-1 a 1 ju -1 n 1 ju 1 l-1 ag 1 u -1 se -1 p 1 o 1 kt-1 n v-1 o 1 d c-1 e 1 ja -1 n 2 fe -1 b 2 m r-1 a 2 a r-1 p 2 m j-1 a 2 ju -1 n 2 ju 2 l-1 ag 2 u -1 se -1 p 2 o 2 kt-1

ja -1 n 0 fe -1 b 0 m r-1 a 0 a r-1 p 0 m j-1 a 0 ju -1 n 0 ju 0 l-1 ag 0 u -1 se -1 p 0 o 0 kt-1 n v-1 o 0 d c-1 e 0 ja -1 n 1 fe -1 b 1 m r-1 a 1 a r-1 p 1 m j-1 a 1 ju -1 n 1 ju 1 l-1 ag 1 u -1 se -1 p 1 o 1 kt-1 n v-1 o 1 d c-1 e 1 ja -1 n 2 fe -1 b 2 m r-1 a 2 a r-1 p 2 m j-1 a 2 ju -1 n 2 ju 2 l-1 ag 2 u -1 se -1 p 2 o 2 kt-1

ja -1 n 0 fe -1 b 0 m r-1 a 0 a r-1 p 0 m j-1 a 0 ju -1 n 0 ju 0 l-1 ag 0 u -1 se -1 p 0 o 0 kt-1 n v-1 o 0 d c-1 e 0 ja -1 n 1 fe -1 b 1 m r-1 a 1 a r-1 p 1 m j-1 a 1 ju -1 n 1 ju 1 l-1 ag 1 u -1 se -1 p 1 o 1 kt-1 n v-1 o 1 d c-1 e 1 ja -1 n 2 fe -1 b 2 m r-1 a 2 a r-1 p 2 m j-1 a 2 ju -1 n 2 ju 2 l-1 ag 2 u -1 se -1 p 2 o 2 kt-1

SEB Oil Market Report

Oil products

Regional 3-2-1 cracks

($/b, daily closing)

4 2 4 0 3 8 3 6 3 4 3 2 3 0 2 8 2 6 2 4 2 2 2 0 1 8 1 6 1 4 1 2 1 0 8 6 4 2 0 -2 -4 -6 Asia (M a in s) U (W I) S T Eu p (Bre t) ro e n Pe n G lf (D b i) rsia u ua

European naphtha stocks

(kt, monthly data)

10 8 10 7 10 6 10 5 10 4 10 3 10 2 10 1 10 0 9 0 8 0 7 0 6 0 5 0 4 0 3 0 2 0 j f 4 ye r ra g , top a ne 4 ye r ra g , b tto a ne o m 21 02 4 ye r a e g a v ra e

ja -1 n 0 fe -1 b 0 m r-1 a 0 a r-1 p 0 m j-1 a 0 ju -1 n 0 ju 0 l-1 ag 0 u -1 se -1 p 0 o 0 kt-1 n v-1 o 0 d c-1 e 0 ja -1 n 1 fe -1 b 1 m r-1 a 1 a r-1 p 1 m j-1 a 1 ju -1 n 1 ju 1 l-1 ag 1 u -1 se -1 p 1 o 1 kt-1 n v-1 o 1 d c-1 e 1 ja -1 n 2 fe -1 b 2 m r-1 a 2 a r-1 p 2 m j-1 a 2 ju -1 n 2 ju 2 l-1 ag 2 u -1 se -1 p 2 o 2 kt-1

European gasoline stocks

(kt, monthly data)

15 10 10 10 15 00 10 00 90 5 90 0 80 5 80 0 70 5 70 0 60 5 60 0 50 5 50 0 40 5 40 0 j f m a m j j a s o n d 4 ye r ra g , to a ne p 4 ye r ra g , b tto a ne o m 21 02 4 ye r a e g a v ra e

European jet fuel stocks

(kt, monthly data)

90 0 80 5 80 0 70 5 70 0 60 5 60 0 50 5 50 0 40 5 40 0 30 5 30 0 20 5 20 0 10 5 10 0 j f m a m j j

4 ye r ra g , to a ne p 4 ye r ra g , b tto a ne o m 21 02 4 ye r a e g a v ra e a s o n d

European gasoil stocks

(kt, monthly data)

30 10 30 00 20 90 20 80 20 70 20 60 20 50 20 40 20 30 20 20 20 10 20 00 10 90 10 80 10 70 10 60 10 50 10 40 10 30 10 20 10 10 10 00 j f

European fuel oil stocks

(kt, monthly data)

15 00 10 00 90 5 90 0 80 5 80 0 70 5 70 0 60 5 60 0 50 5 50 0 40 5 40 0 4 ye r ra g , to a ne p 4 ye r ra g , b tto a ne o m 21 02 4 ye r a e g a v ra e

4 ye r ra g , to a ne p 4 ye r ra g , b tto a ne o m 21 02 4 ye r a e g a v ra e

Chart Sources: Bloomberg, PJK International, SEB Commodity Research

SEB Oil Market Report

Oil products

US implied crude oil demand

(DOE, mb/d, weekly data)

1 ,8 5 1 ,6 5 1 ,4 5 1 ,2 5 1 ,0 5 1 ,8 4 1 ,6 4 1 ,4 4 1 ,2 4 1 ,0 4 1 ,8 3 1 ,6 3 1 ,4 3 j f m a m j j a s o n d 5 ag y v. 21 01 21 02

8 ,9 5y a g v. 20 11 20 12 9 ,1 9 ,3 9 ,5

US implied gasoline demand

(DOE, mb/d, weekly data)

9 ,7

8 ,7

8 ,5 j f m a m j j a s o n d

US implied distillate demand

(DOE, mb/d, weekly data)

5 ,6 5 ,4 5 ,2 5 ,0 4 ,8 4 ,6 4 ,4 4 ,2 4 ,0 j f m a m j j a s o n d 5 a g. y v 2 1 01 2 2 01

Gasoline arbitrage Rotterdam to New York

($/t, daily closing)

4 4 4 0 3 6 3 2 2 8 2 4 2 0 1 6 1 2 8 4 0 -4 -8 -1 2 -1 6 -2 0 -2 4

ja -11 n fe -1 b 1 m r-1 a 1 a r-1 p 1 m j-1 a 1 ju -11 n ju l-11 ag 1 u -1 se -1 p 1 o 1 kt-1 n v-1 o 1 d c-1 e 1 ja -12 n fe -1 b 2 m r-1 a 2 a r-1 p 2 m j-1 a 2

Middle distillate arbitrage Rotterdam to New York

($/t, daily closing)

2 0 1 5 1 0 5 0 -5 -1 0 -1 5 -2 0 H a g o a il e tin il/G so J t fu l/Ke se e e e ro n

ja -1 n 1 fe -1 b 1 m r-1 a 1 a r-1 p 1 m j-1 a 1 ju -1 n 1 ju 1 l-1 ag 1 u -1 se -1 p 1 o 1 kt-1 n v-1 o 1 d c-1 e 1 ja -1 n 2 fe -1 b 2 m r-1 a 2 a r-1 p 2 m j-1 a 2

-2 5

Chart Sources: Bloomberg, SEB Commodity Research

ju -1 n 2 ju 2 l-1 ag 2 u -1 se -1 p 2 o 2 kt-1

ju -12 n ju l-12 ag 2 u -1 se -1 p 2 o 2 kt-1

SEB Oil Market Report

Related energy markets

US natural gas price

(NYMEX, $/MMBtu, front month, weekly closing)

1 4 1 3 1 2 1 1 1 0 9 8 7 6 5 4 3 2 1

UK natural gas price

(ICE, front month, weekly closing)

1 6 1 5 1 4 1 3 1 2 1 1 1 0 9 8 7 6 5 4 3 2 1 0 4 0 3 0 2 0 5 0 $ M /M Btu (le a ft xis) G /th rm (rig t a Bp e h xis) 9 0 8 0 7 0 6 0

20 07

20 08

20 09

21 00

21 01

21 02

20 07

20 08

20 09

21 00

21 01

Nordic power price

(Nord Pool, /MWh, front quarter, weekly closing)

8 0 7 5 7 0 6 5 6 0 5 5 5 0 4 5 4 0 3 5 3 0 2 5 2 0

Continental power price

(EEX, /MWh, front quarter, weekly closing)

9 5 9 0 8 5 8 0 7 5 7 0 6 5 6 0 5 5 5 0 4 5 4 0 3 5 3 0 2 5 2 0

20 07

20 08

20 09

21 00

21 01

21 02 21 02

20 09

21 00

21 01

EUA price

(ECX ICE, /t, Dec. 11, weekly closing)

3 4 3 2 3 0 2 8 2 6 2 4 2 2 2 0 1 8 1 6 1 4 1 2 1 0 8 6

21 02

Coal price

(CIF ARA steam coal, API#2, daily closing)

15 3 10 3 15 2 10 2 15 1 10 1 15 0 10 0 9 5 9 0 8 5 8 0 7 5 7 0

20 07

20 08

20 09

21 00

21 01

Chart Sources: Bloomberg, SEB Commodity Research

21 02

ja -1 n 0 fe -1 b 0 m r-1 a 0 a r-1 p 0 m j-1 a 0 ju -1 n 0 ju 0 l-1 ag 0 u -1 se -1 p 0 o 0 kt-1 n v-1 o 0 d c-1 e 0 ja -1 n 1 fe -1 b 1 m r-1 a 1 a r-1 p 1 m j-1 a 1 ju -1 n 1 ju 1 l-1 ag 1 u -1 se -1 p 1 o 1 kt-1 n v-1 o 1 d c-1 e 1 ja -1 n 2 fe -1 b 2 m r-1 a 2 a r-1 p 2 m j-1 a 2 ju -1 n 2 ju 2 l-1 ag 2 u -1 se -1 p 2 o 2 kt-1

SEB Oil Market Report

Market indicators

MSCI World equity market index

(weekly closing)

10 70 10 60 10 50 10 40 10 30 10 20 10 10 10 00 90 0 80 0 70 0 60 0

UBS Bloomberg CMCI commodity market index

(price index, weekly closing)

10 80 10 70 10 60 10 50 10 40 10 30 10 20 10 10 10 00 90 0 80 0 70 0 60 0

20 05

20 06

20 07

20 08

20 09

21 00

21 01

21 02

20 05

20 06

20 07

20 08

20 09

21 00

21 01

JPM global manufacturing PMI

(monthly, PMIs >50 expansive)

5 8 5 6 5 4 5 2 5 0 4 8 4 6 4 4 4 2 4 0 3 8 3 6 3 4 3 2

Regional PMI:s

(monthly data)

6 5 6 0 5 5 5 0 4 5 4 0 3 5 3 0 U S Eu zo e ro n C in h a R fe n e re ce

20 05

20 06

20 07

20 08

20 09

21 00

21 01

Regional industrial production growth

(%, y/y, monthly data)

2 5 2 0 1 5 1 0 5 0 -5 -1 0 -1 5 -2 0 -2 5 m r-0 a 6 ju -0 n 6 se -0 p 6 d c-0 e 6 m r-0 a 7 ju -0 n 7 se -0 p 7 d c-0 e 7 m r-0 a 8 ju -0 n 8 se -0 p 8 d c-0 e 8 m r-0 a 9 ju -0 n 9 se -0 p 9 d c-0 e 9 m r-1 a 0 ju -1 n 0 se -1 p 0 d c-1 e 0 m r-1 a 1 ju -1 n 1 se -1 p 1 d c-1 e 1 m r-1 a 2 ju -1 n 2 U S E ro n u zo e C in h a

21 02

OECD composite leading indicators

(monthly, 100 corresponds to long term trend growth in industrial production)

14 0 13 0 12 0 11 0 10 0 9 9 9 8 9 7 9 6 9 5 9 4 9 3 20 05 20 06 20 07 20 08 20 09 21 00 21 01 21 02 C in h a E ro n u zo e O D EC U SA R fe n e re ce

Chart Sources: Bloomberg, OECD, SEB Commodity Research

m r-0 a 6 ju -0 n 6 se -0 p 6 d c-0 e 6 m r-0 a 7 ju -0 n 7 se -0 p 7 d c-0 e 7 m r-0 a 8 ju -0 n 8 se -0 p 8 d c-0 e 8 m r-0 a 9 ju -0 n 9 se -0 p 9 d c-0 e 9 m r-1 a 0 ju -1 n 0 se -1 p 0 d c-1 e 0 m r-1 a 1 ju -1 n 1 se -1 p 1 d c-1 e 1 m r-1 a 2 ju -1 n 2 se -1 p 2

10

21 02

SEB Oil Market Report

COMMODITY RESEARCH DISCLAIMER

This statement affects your rights

This report has been compiled by SEBs Commodity Research, a division within Skandinaviska Enskilda Banken AB (publ) (SEB), to provide background information only. It is confidential to the recipient, any dissemination, distribution, copying, or other use of this communication is strictly prohibited.

Good faith & limitations

Opinions, projections and estimates contained in this report represent the authors present opinion and are subject to change without notice. Although information contained in this report has been compiled in good faith from sources believed to be reliable, no representation or warranty, expressed or implied, is made with respect to its correctness, completeness or accuracy of the contents, and the information is not to be relied upon as authoritative. To the extent permitted by law, SEB accepts no liability whatsoever for any direct or consequential loss arising from use of this document or its contents.

Disclosures

The analysis and valuations, projections and forecasts contained in this report are based on a number of assumptions and estimates and are subject to contingencies and uncertainties; different assumptions could result in materially different results. The inclusion of any such valuations, projections and forecasts in this report should not be regarded as a representation or warranty by or on behalf of the SEB Group or any person or entity within the SEB Group that such valuations, projections and forecasts or their underlying assumptions and estimates will be met or realized. Past performance is not a reliable indicator of future performance. Foreign currency rates of exchange may adversely affect the value, price or income of any security or related investment mentioned in this report. This document does not constitute investment advice and is being provided to you without regard to your investment objectives or circumstances. Anyone considering taking actions based upon the content of this document is urged to base investment decisions upon such investigations as they deem necessary. This document does not constitute an offer or an invitation to make an offer, or solicitation of, any offer to subscribe for any securities or other financial instruments.

Conflicts of Interest

SEB has in place a Conflicts of Interest Policy designed, amongst other things, to promote the independence and objectivity of reports produced by its Research departments, which are separated from the rest of SEB business areas by information barriers; as such, research reports are independent and based solely on publicly available information. Your attention is drawn to the fact that a member of, or an entity associated with, SEB or its affiliates, officers, directors, employees or shareholders of such members (a) may be represented on the board of directors or similar supervisory entity of the companies mentioned herein (b) may, to the extent permitted by law, have a position in the securities of (or options, warrants or rights with respect to, or interest in the securities of the companies mentioned herein or may make a market or act as principal in any transactions in such securities (c) may, acting as principal or as agent, deal in investments in or with companies mentioned herein, and (d) may from time to time provide investment banking, underwriting or other services to, or solicit investment banking, underwriting or other business from the companies mentioned herein.

Recipients

In the UK, this report is directed at and is for distribution only to (I) persons who have professional experience in matters relating to investments falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (The Order) or (II) high net worth entities falling within Article 49(2)(a) to (d) of the Order (all such persons together being referred to as relevant persons. This report must not be acted on or relied upon by persons in the UK who are not relevant persons. In the US, this report is distributed solely to persons who qualify as major U.S. institutional investors as defined in Rule 15a-6 under the Securities and Exchange Act of 1934. U.S. persons wishing to effect transactions in any security discussed herein should do so by contacting Skandinaviska Enskilda Banken AB (publ) (SEBAB). SEBAB accepts responsibility for the content of this report in connection with its distribution in the US. The distribution of this document may be restricted in certain jurisdictions by law, and persons into whose possession this documents comes should inform themselves about, and observe, any such restrictions.

The SEB Group: members, memberships and regulators Skandinaviska Enskilda Banken AB (publ) is incorporated in Sweden, as a Limited Liability Company. It is regulated by Finansinspektionen, and by the local financial regulators in each of the jurisdictions in which it has branches or subsidiaries, including in the UK, by the Financial Services Authority; Denmark by Finanstilsynet; Finland by Finanssivalvonta; Germany by Bundesanstalt fr Finanzdienstleistungsaufsicht and Norway by Finanstilsynet. In the US, SEBAB is a U.S. broker-dealer, registered with the Financial Industry Regulatory Authority (FINRA). SEBAB is a direct subsidiary of SEB. SEB is active on major Nordic and other European Regulated Markets and Multilateral Trading Facilities, in as well as other non-European equivalent markets, for trading in financial instruments. For a list of execution venues of which SEB is a member or participant, visit http://www.seb.se.

11

SEB Commodity Research

Bjarne Schieldrop, Chief Commodity Analyst bjarne.schieldrop@seb.no +47 9248 9230 Filip Petersson, Commodity Strategist filip.petersson@seb.se +46 8 506 230 47

www.seb.se

Das könnte Ihnen auch gefallen

- Insights From 2014 of Significance For 2015Dokument5 SeitenInsights From 2014 of Significance For 2015SEB GroupNoch keine Bewertungen

- Economic Insights: Riksbank To Lower Key Rate, While Seeking New RoleDokument3 SeitenEconomic Insights: Riksbank To Lower Key Rate, While Seeking New RoleSEB GroupNoch keine Bewertungen

- Economic Insights: The Middle East - Politically Hobbled But With Major PotentialDokument5 SeitenEconomic Insights: The Middle East - Politically Hobbled But With Major PotentialSEB GroupNoch keine Bewertungen

- Economic Insights: Subtle Signs of Firmer Momentum in NorwayDokument4 SeitenEconomic Insights: Subtle Signs of Firmer Momentum in NorwaySEB GroupNoch keine Bewertungen

- CFO Survey 1403: Improving Swedish Business Climate and HiringDokument12 SeitenCFO Survey 1403: Improving Swedish Business Climate and HiringSEB GroupNoch keine Bewertungen

- SE-Banken, Investment Outlook, Dec 2013, "Market Hopes Will Require Some Evidence"Dokument35 SeitenSE-Banken, Investment Outlook, Dec 2013, "Market Hopes Will Require Some Evidence"Glenn ViklundNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- T&L BrochureDokument2 SeitenT&L BrochuremottebossNoch keine Bewertungen

- Credit Suisse S&T Cover Letter 1Dokument1 SeiteCredit Suisse S&T Cover Letter 1Dylan AdrianNoch keine Bewertungen

- ABS CBN V CTADokument7 SeitenABS CBN V CTAcaloytalaveraNoch keine Bewertungen

- The Cost of Trigger Happy InvestingDokument4 SeitenThe Cost of Trigger Happy InvestingBrazil offshore jobsNoch keine Bewertungen

- SAP ReportsDokument4 SeitenSAP Reportsbalaji.amubanNoch keine Bewertungen

- Asian Paints IndiaDokument114 SeitenAsian Paints IndiaZain TahirNoch keine Bewertungen

- CA IVY Account Terms ConditionsDokument2 SeitenCA IVY Account Terms Conditionskanna275Noch keine Bewertungen

- Coal India 1Dokument14 SeitenCoal India 1SuMit PaTilNoch keine Bewertungen

- Closing Summary Oct 30 2022 EN - tcm10-29081 - tcm10-29081Dokument2 SeitenClosing Summary Oct 30 2022 EN - tcm10-29081 - tcm10-29081indraseenayya chilakalaNoch keine Bewertungen

- GST PDFDokument81 SeitenGST PDFPankaj JainNoch keine Bewertungen

- Derivatives QuestionsDokument3 SeitenDerivatives QuestionsLoc nguyenNoch keine Bewertungen

- Ielts Writing Practise Test 14 19th August 2019Dokument3 SeitenIelts Writing Practise Test 14 19th August 2019Ivan SamNoch keine Bewertungen

- DDDDDokument2 SeitenDDDDVinod PallathNoch keine Bewertungen

- Insider Trading RegulationsDokument22 SeitenInsider Trading Regulationspreeti211Noch keine Bewertungen

- Promissory NoteDokument2 SeitenPromissory NoteTom WilkinsonNoch keine Bewertungen

- Thompson Corporations Outline: General PrinciplesDokument32 SeitenThompson Corporations Outline: General PrinciplesthebhurdNoch keine Bewertungen

- Barbri Corp OutlineDokument12 SeitenBarbri Corp Outlineshaharhr1100% (3)

- Company Profile: Ariya Bridge CapitalDokument6 SeitenCompany Profile: Ariya Bridge Capitalee sNoch keine Bewertungen

- High Frequency TradingDokument4 SeitenHigh Frequency TradingAmsalu WalelignNoch keine Bewertungen

- Factors Influencing The Investors' Decision Making in Stock MarketDokument27 SeitenFactors Influencing The Investors' Decision Making in Stock Marketحمامة السلامNoch keine Bewertungen

- Phoenix Commodities Webinar Synopsis & Trading SetupDokument15 SeitenPhoenix Commodities Webinar Synopsis & Trading Setupvinayak sontakkeNoch keine Bewertungen

- KCP (Repaired)Dokument61 SeitenKCP (Repaired)keerthiNoch keine Bewertungen

- Enron ScandalDokument15 SeitenEnron ScandalMarielNoch keine Bewertungen

- Derivatives Markets 3rd Edition McDonald Test Bank DownloadDokument5 SeitenDerivatives Markets 3rd Edition McDonald Test Bank DownloadBarbara Sosa100% (28)

- BluestarDokument11 SeitenBluestaramol1928Noch keine Bewertungen

- Book Value Per Share: Problem 3: ExercisesDokument4 SeitenBook Value Per Share: Problem 3: ExercisesNikky Bless LeonarNoch keine Bewertungen

- Trading For Profit - Oli HilleDokument100 SeitenTrading For Profit - Oli HilleShyam Ramavarapu100% (1)

- Bristol Application Tracker 2023 - 24Dokument76 SeitenBristol Application Tracker 2023 - 24junklandshereNoch keine Bewertungen

- CERTIFICATE of TRUST For Opening AccountsDokument1 SeiteCERTIFICATE of TRUST For Opening AccountsTiggle Madalene100% (24)

- PE RatioDokument8 SeitenPE RatioVaidyanathan RavichandranNoch keine Bewertungen