Das könnte Ihnen auch gefallen

- Yarn Dyed Weaving Factory Limited.: Costing SheetDokument3 SeitenYarn Dyed Weaving Factory Limited.: Costing SheetDeny Arisandi100% (2)

- A Presentation On Fusing MachinesDokument22 SeitenA Presentation On Fusing Machinesadibhai0680% (5)

- How To Calculate Dyeing Recipe in Textile Wet ProcessingDokument5 SeitenHow To Calculate Dyeing Recipe in Textile Wet ProcessingMuhammad HamzaNoch keine Bewertungen

- Costing Sheet Excel FormatDokument2 SeitenCosting Sheet Excel FormatDeny ArisandiNoch keine Bewertungen

- Costing of FabricDokument2 SeitenCosting of FabricBalaji N86% (7)

- Cost Conversion Rates SITRA 2 Rs Per KG Per Count AvgDokument18 SeitenCost Conversion Rates SITRA 2 Rs Per KG Per Count AvgPrashant Patil100% (3)

- Costing of Fabric: WovenDokument24 SeitenCosting of Fabric: WovenEktaJassal100% (3)

- Cost AccountingDokument28 SeitenCost Accountinglove_oct22100% (1)

- WEAVING ParameterDokument5 SeitenWEAVING ParameterAshraful Himel33% (3)

- Yarn Clearing SystemsDokument11 SeitenYarn Clearing SystemsLohit MohapatraNoch keine Bewertungen

- Costing of SkirtDokument16 SeitenCosting of SkirtmishrarNoch keine Bewertungen

- Plant Layout Group C 2019Dokument27 SeitenPlant Layout Group C 2019Mukarram Ali KhanNoch keine Bewertungen

- Account TitlesDokument4 SeitenAccount TitlesHermae Bucton100% (1)

- Hok Calculation in MillsDokument14 SeitenHok Calculation in MillsMarazaban Velati90% (10)

- Fiber To Yarn Spinning Process of Polyester FiberDokument12 SeitenFiber To Yarn Spinning Process of Polyester FiberVinod Kumar100% (1)

- Yarn Faults: Types Causes RemediesDokument20 SeitenYarn Faults: Types Causes Remediesஹரி கிருஷ்ணன் வாசு71% (7)

- Spinning Mill CostingDokument12 SeitenSpinning Mill CostingKrithika Salraj50% (2)

- PPTDokument56 SeitenPPTSomalika Banerjee100% (2)

- Cost ReductionDokument8 SeitenCost Reductionmlganesh666100% (3)

- Ring Spinning NTPELDokument92 SeitenRing Spinning NTPELCraig Martin67% (3)

- Break-Even Caluculation For Spinning MillDokument8 SeitenBreak-Even Caluculation For Spinning MillRanganatham Ummadisetty100% (1)

- Costing For A Spinning Mill PDFDokument13 SeitenCosting For A Spinning Mill PDFyogesh kumawatNoch keine Bewertungen

- NSQF - Knitting Machine Operator - Circular KnittingDokument23 SeitenNSQF - Knitting Machine Operator - Circular KnittingSakibMDShafiuddinNoch keine Bewertungen

- Air Jet SpinningDokument7 SeitenAir Jet SpinningAbi NikilNoch keine Bewertungen

- Wet Processing Pretreatment-LectureDokument28 SeitenWet Processing Pretreatment-Lecturearafathosain100% (3)

- Production Planning in SpinningDokument15 SeitenProduction Planning in SpinningSantosh100% (1)

- Blow RoomDokument27 SeitenBlow Roomapi-377494789% (19)

- Yarn WindingDokument22 SeitenYarn WindingPRAKASH B. MALAKANE0% (1)

- Yarn RealisationDokument7 SeitenYarn RealisationPulak Debnath100% (1)

- COSTING of Fabric. For Students. PPT - RanjanDokument75 SeitenCOSTING of Fabric. For Students. PPT - RanjanRavi Singh0% (1)

- Weaving Commission CalculationsDokument1 SeiteWeaving Commission Calculationsraj_85Noch keine Bewertungen

- Cost SheetDokument17 SeitenCost Sheet9986212378Noch keine Bewertungen

- Lect2 - Blow Room 1Dokument18 SeitenLect2 - Blow Room 1Mina Samy abd el zaherNoch keine Bewertungen

- Maintenance of Textile MachineryDokument27 SeitenMaintenance of Textile Machineryhmsohag100% (2)

- 12 Chapter 4Dokument43 Seiten12 Chapter 4Anu Mishra100% (1)

- Air Jet LoomsDokument6 SeitenAir Jet LoomsJuhi Nath100% (2)

- Yarn Unevenness and Its Impact On QualityDokument24 SeitenYarn Unevenness and Its Impact On QualityShan ImtiazNoch keine Bewertungen

- Lab ReportDokument24 SeitenLab ReportFahima RashidNoch keine Bewertungen

- Raw Material Consumption Calculation in Apparel Industry - Clothing IndustryDokument5 SeitenRaw Material Consumption Calculation in Apparel Industry - Clothing IndustryQad BestmplNoch keine Bewertungen

- Controlling and Check Points in Spinning ProcessDokument10 SeitenControlling and Check Points in Spinning ProcessBithy Paul100% (1)

- Spin PlanDokument15 SeitenSpin PlanMukesh Kumar100% (1)

- F Ancy Yarn Production: Chapters 2 3Dokument19 SeitenF Ancy Yarn Production: Chapters 2 3TKK-TEXTILE PSG CT100% (1)

- Yarn Count Used According To Grey GSM - Textile CalculationDokument3 SeitenYarn Count Used According To Grey GSM - Textile CalculationSZNoch keine Bewertungen

- Defects in KnitsDokument38 SeitenDefects in KnitsYogesh SharmaNoch keine Bewertungen

- Twist MultiplierDokument1 SeiteTwist MultiplierAniket Mahajan100% (5)

- CMT of FaultsDokument1 SeiteCMT of FaultsJigneshSaradava100% (1)

- Simplex Gearing DiagramDokument3 SeitenSimplex Gearing DiagramShan Imtiaz67% (3)

- Project ReportDokument35 SeitenProject ReportSK Azaharuddin100% (1)

- Yarn Manufacturing 2Dokument16 SeitenYarn Manufacturing 2Muhammad Farooq Kokab60% (5)

- Spinning CalculationsDokument40 SeitenSpinning Calculationsrajasekarmca100% (2)

- Calculate The Cleaning Efficiency of Blow Room Line.Dokument2 SeitenCalculate The Cleaning Efficiency of Blow Room Line.Ammar Naeem Bhatti83% (6)

- Intoduction & Draft Calculation in Yarn Spinning ProcessesDokument4 SeitenIntoduction & Draft Calculation in Yarn Spinning Processeszeshan100% (1)

- Combing ProcessDokument12 SeitenCombing ProcessSenthil Kumar100% (1)

- Internship Report - GMS Textiles Ltd. - BUBTDokument100 SeitenInternship Report - GMS Textiles Ltd. - BUBTAlif Sheikh100% (1)

- Open End Spinning RieterDokument94 SeitenOpen End Spinning RieterMuhammad Umair100% (2)

- 1.bale Management SystemDokument8 Seiten1.bale Management SystemMd NurunnabiNoch keine Bewertungen

- Elements of Cost: Expense TypesDokument17 SeitenElements of Cost: Expense Typesسعيد الشوكانيNoch keine Bewertungen

- In Production, Research, Retail, and Accounting, A Cost Is The Value of Money That Has Been Used Up To Produce Something or Deliver A ServiceDokument20 SeitenIn Production, Research, Retail, and Accounting, A Cost Is The Value of Money That Has Been Used Up To Produce Something or Deliver A ServiceBHUSHAN PATILNoch keine Bewertungen

- Cost AccountingDokument28 SeitenCost Accountingrenjithrkn12Noch keine Bewertungen

- Costing: Prepared By: Dr. B. K. MawandiyaDokument26 SeitenCosting: Prepared By: Dr. B. K. MawandiyaNamanNoch keine Bewertungen

- Nature and Purpose of Cost AccountingDokument10 SeitenNature and Purpose of Cost AccountingJustus100% (1)

- Financial Reporting and AnalysisDokument5 SeitenFinancial Reporting and AnalysisPiyush AgarwalNoch keine Bewertungen

- International Accounting 3Rd Edition Doupnik Test Bank Full Chapter PDFDokument40 SeitenInternational Accounting 3Rd Edition Doupnik Test Bank Full Chapter PDFJulieHaasyjzp100% (9)

- Introduction To AccountingDokument39 SeitenIntroduction To AccountingVikash HurrydossNoch keine Bewertungen

- PA2 X ESP HW10 G1 Revanza TrivianDokument9 SeitenPA2 X ESP HW10 G1 Revanza TrivianRevan KonglomeratNoch keine Bewertungen

- Financial Statements PLDT and GLobeDokument18 SeitenFinancial Statements PLDT and GLobeArnelli GregorioNoch keine Bewertungen

- JEV CorrectionDokument18 SeitenJEV CorrectionJerwin Cases TiamsonNoch keine Bewertungen

- Solution To QN 6 (PG 135) : Calculation of Overhead Absorption RatesDokument10 SeitenSolution To QN 6 (PG 135) : Calculation of Overhead Absorption RatesGeorge BulikiNoch keine Bewertungen

- MAS Concept MapDokument1 SeiteMAS Concept MapCathlene TitoNoch keine Bewertungen

- Analisis Rasio Keuangan Sebagai Tolok Ukur Kinerja Keuangan Badan Usaha Milik Desa (Bumdes) Arum Dalu NgabarDokument12 SeitenAnalisis Rasio Keuangan Sebagai Tolok Ukur Kinerja Keuangan Badan Usaha Milik Desa (Bumdes) Arum Dalu NgabarWindy FeeNoch keine Bewertungen

- Financial Accounting Assignment 2Dokument6 SeitenFinancial Accounting Assignment 2kirubelNoch keine Bewertungen

- Ebay Webdoc 649Dokument9 SeitenEbay Webdoc 649Abdirisaq MohamudNoch keine Bewertungen

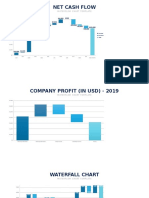

- Waterfall Chart Slides PowerPoint TemplateDokument30 SeitenWaterfall Chart Slides PowerPoint Templateziad ghanemNoch keine Bewertungen

- Problem 1. Prepare AJE From The Books of Silent As of Consider The FF InformationDokument10 SeitenProblem 1. Prepare AJE From The Books of Silent As of Consider The FF InformationYuan LoganNoch keine Bewertungen

- CFAS Module 1 - ReviewerRRRDokument4 SeitenCFAS Module 1 - ReviewerRRRAthena LedesmaNoch keine Bewertungen

- VP Religious AffairDokument4 SeitenVP Religious Affairjaiscey valenciaNoch keine Bewertungen

- AventDokument9 SeitenAventLiigiia San YrafatsarNoch keine Bewertungen

- Accounting 14 - Applied Auditing OkDokument12 SeitenAccounting 14 - Applied Auditing OkNico evansNoch keine Bewertungen

- PQ 2019 - Financial Accounting SyllabusDokument5 SeitenPQ 2019 - Financial Accounting SyllabusUmeesh NantakumarNoch keine Bewertungen

- D Business Combinations - IFRS 3 (Revised)Dokument10 SeitenD Business Combinations - IFRS 3 (Revised)Brook KongNoch keine Bewertungen

- 1.statutory Audit MSME PDFDokument17 Seiten1.statutory Audit MSME PDFchariNoch keine Bewertungen

- Advanced Financial Accounting - Paper 8 CPA PDFDokument10 SeitenAdvanced Financial Accounting - Paper 8 CPA PDFAhmed Suleyman100% (1)

- Instapdf - in Accounting Ratios Class 12 All Formulas 176Dokument18 SeitenInstapdf - in Accounting Ratios Class 12 All Formulas 176Subhavi DikshitNoch keine Bewertungen

- Final Term 14 Papers MGT101 SOLVED by Chanda Rehman, Kamran Haider, Abr N Anjum-1Dokument146 SeitenFinal Term 14 Papers MGT101 SOLVED by Chanda Rehman, Kamran Haider, Abr N Anjum-1Muhammad HassanNoch keine Bewertungen

- IVY Fee StatementDokument3 SeitenIVY Fee StatementIVYNoch keine Bewertungen

- Robert Half Salary Guide 2012Dokument9 SeitenRobert Half Salary Guide 2012cesarthemillennialNoch keine Bewertungen

- Chapter 11Dokument26 SeitenChapter 11ENG ZI QINGNoch keine Bewertungen

- Sarangapani & Co: Chartered AccountantsDokument14 SeitenSarangapani & Co: Chartered AccountantsSarangapani KaliyamoorthyNoch keine Bewertungen

- Q Financial RatiosDokument5 SeitenQ Financial RatiosUmmi KalthumNoch keine Bewertungen

- 中英文对照版财务报表及专业名词Dokument6 Seiten中英文对照版财务报表及专业名词sandywhgNoch keine Bewertungen