Das könnte Ihnen auch gefallen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Í Qhhoè Genovia Joshuaâââââââ M Ç0) '84zî Mr. Joshua Magbanua GenoviaDokument3 SeitenÍ Qhhoè Genovia Joshuaâââââââ M Ç0) '84zî Mr. Joshua Magbanua GenoviaJoshua M. GenoviaNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Drycargo 05-2019Dokument134 SeitenDrycargo 05-2019fracev100% (1)

- Barcela, John Christian 13634019 80031904 10,000.00 02/15/2023 02/15/2023Dokument1 SeiteBarcela, John Christian 13634019 80031904 10,000.00 02/15/2023 02/15/2023JCNoch keine Bewertungen

- TOPIC 6c - Cost of Capital and Capital StructureDokument42 SeitenTOPIC 6c - Cost of Capital and Capital StructureYasskidayo Hammyson100% (1)

- Wyckoff Trading Method Summary Cheat SheetDokument2 SeitenWyckoff Trading Method Summary Cheat SheetRbmanikandan100% (1)

- Hook - The Arrival of Tink - John WilliamsDokument2 SeitenHook - The Arrival of Tink - John WilliamsAntoine LagneauNoch keine Bewertungen

- Bollinger Bands Essentials 1Dokument13 SeitenBollinger Bands Essentials 1Kiran KudtarkarNoch keine Bewertungen

- The Avoidable War - Full ReportDokument89 SeitenThe Avoidable War - Full ReportAkshat TennetiNoch keine Bewertungen

- Duronto AshaDokument5 SeitenDuronto Ashaapi-26148947100% (1)

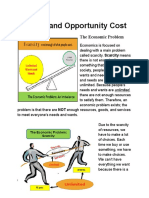

- Scarcity and Opportunity Cost: The Economic ProblemDokument10 SeitenScarcity and Opportunity Cost: The Economic ProblemElise Smoll (Elise)Noch keine Bewertungen

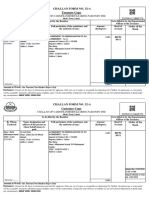

- Challan Form No. 32-A Treasury Copy: Challan of Cash/Transfer/Clearing Paid Into TheDokument1 SeiteChallan Form No. 32-A Treasury Copy: Challan of Cash/Transfer/Clearing Paid Into TheShahzad techNoch keine Bewertungen

- Room Assignment: Tuguegarao City Science High SchoolDokument6 SeitenRoom Assignment: Tuguegarao City Science High SchoolPhilBoardResultsNoch keine Bewertungen

- Economic Growth (Mankiw) PDFDokument69 SeitenEconomic Growth (Mankiw) PDFaminul akashNoch keine Bewertungen

- CE and HW On Debt SecuritiesDokument3 SeitenCE and HW On Debt SecuritiesAmy SpencerNoch keine Bewertungen

- BG 45 - BS - 95 - PremiumLine - EN - 905 - 819 - 2Dokument24 SeitenBG 45 - BS - 95 - PremiumLine - EN - 905 - 819 - 2Dilhara WickramaarachchiNoch keine Bewertungen

- Mindmap Ch1. Indian Economy On The Eve of IndependenceDokument1 SeiteMindmap Ch1. Indian Economy On The Eve of IndependenceAnup DubeyNoch keine Bewertungen

- Income Statement: Cost of Goods Sold 540,000 768000 999600 1300920Dokument4 SeitenIncome Statement: Cost of Goods Sold 540,000 768000 999600 1300920ASIF RAFIQUE BHATTINoch keine Bewertungen

- Issue 2 SMDokument3 SeitenIssue 2 SMAlisa AwaludinNoch keine Bewertungen

- Maple Leaf Case Study AssignmentDokument7 SeitenMaple Leaf Case Study AssignmentafzaalmoinNoch keine Bewertungen

- Thanks For Your Order!: Billing Information Payment Details Receipt DetailsDokument1 SeiteThanks For Your Order!: Billing Information Payment Details Receipt Detailschalapathi psNoch keine Bewertungen

- Swot Analysis of Revlon IncDokument5 SeitenSwot Analysis of Revlon IncSubhana AsimNoch keine Bewertungen

- PolestarDokument2 SeitenPolestarHusseinNoch keine Bewertungen

- Difference Between Production and ProductivityDokument1 SeiteDifference Between Production and ProductivityGiani Jacky OliverosNoch keine Bewertungen

- Ecodev Midterm Notes 2Dokument3 SeitenEcodev Midterm Notes 2Nichole BombioNoch keine Bewertungen

- BLR - Electives For MBA Class of 2024 - Sem III & IVDokument6 SeitenBLR - Electives For MBA Class of 2024 - Sem III & IVbhagyesh taleleNoch keine Bewertungen

- The Relationship Between Food and Fuel PricesDokument2 SeitenThe Relationship Between Food and Fuel PricesSamieNoch keine Bewertungen

- Cash Accounts Receivable JournalDokument56 SeitenCash Accounts Receivable Journallaale dijaanNoch keine Bewertungen

- To Get More Videos of All Subjects: ShareDokument50 SeitenTo Get More Videos of All Subjects: ShareMridul UpadhyayNoch keine Bewertungen

- Us Consumer Discretionary Equities PreferenceDokument52 SeitenUs Consumer Discretionary Equities PreferenceTung NgoNoch keine Bewertungen

- Week 2 Tutorial - Rio Tinto Case StudyDokument3 SeitenWeek 2 Tutorial - Rio Tinto Case StudyBaar SheepNoch keine Bewertungen