Beruflich Dokumente

Kultur Dokumente

La Teoría Del Valor-Trabajo y Los Precios en China

Hochgeladen von

D. Silva EscobarOriginaltitel

Copyright

Verfügbare Formate

Dieses Dokument teilen

Dokument teilen oder einbetten

Stufen Sie dieses Dokument als nützlich ein?

Sind diese Inhalte unangemessen?

Dieses Dokument meldenCopyright:

Verfügbare Formate

La Teoría Del Valor-Trabajo y Los Precios en China

Hochgeladen von

D. Silva EscobarCopyright:

Verfügbare Formate

The labour theory of value and the prices in China: methodology and analysis.

Everlam Elias Montibeler (Universidade Federal de Mato Grosso Do Sul), Csar Snchez (Universidad

Nacional Autnoma de Mxico, Universidad Complutense de Madrid).

Resumo

Este trabalho examina a relao entre valores e preos para China. Utilizando as matrizes insumo-produto

chinesas de 2002 e a metodologia desenvolvida por Shaikh (1984) so estimados os diferentes tipos de

preos. Concluiu-se em primeiro lugar, e em linha com o que foi obtido em outros estudos, a existncia de

desvios, inferiores a 20%, entre os diferentes tipos de preos. Em segundo lugar, e em consonncia com

resultados de trabalhos similares, se detectou que o requerimento de trabalho, comparado com os

requerimentos (ao, petrleo, etc.) so os que melhores explicam a determinao de preos. Prope-se

uma metodologia para ponderar o tamanho do sector na anlise de regresso. Este teste determinou que os

preos so proporcionais ao valor. Alm disso, analisamos se uma m especificao possvel pode causar

um vis considervel no impacto de valores para os preos do mercado. Nosso estudo mostra que esse

vis de pouca importncia. Finalmente, foi estimado os valores mdios da taxa de lucro, mais-valia e

composio orgnica. interessante notar que os nveis das taxas de lucro na China so maiores que as

apresentadas em estudo similar para outros pases (Estados Unidos, Grcia, Espanha).

Abstract

This paper examines the relationship between values and prices in China. From the information of input-

output table from 2002 and using Shaikh`s methodology (1984) are counted the different types of prices.

We concluded first and in line with what was obtained in other studies, a distance between the different

types of prices, less than 20%. Secondly, and briefly reviewing some criticisms of these kind of studies, it

appears that labor requirements confronted with the requirements of steel, oil, etc., are the ones that

explain better market prices. Is proposed a way to weight the size of the sector in the regression analysis.

This test determines that prices proportional to the value. In addition, we analyze whether a possible

misspecification may cause a considerable bias in the impact of values to market prices. Our study shows

that this bias is of little importance. Finally, we estimate the average values of the rate of profit, capital

gain rate and organic composition. It is interesting to note that profit rate levels in China are higher than

those shown in other studies for other countries (United States, Greece, Spain).

KEY WORDS: China Economy, Prices Deviation, Labor Theory of Value.

JEL: B41, B50, P16

1. Introduction

In the classics there is developed the idea that prices of commodities are determined by the amount of

work (Meek, 1980). This idea is taking a gradual approach. Since Smith we have the notions of labor

commanded and, on the other side, the efforts, that involves producing goods. Ricardo is more accurate

and develops the idea that the value of a commodity is determined by the direct and indirect labor

incorporated in it. Marx theory not only develops the idea of Ricardo but includes the total labor (direct

and indirect) as social labor and work not only as the direct producer labor. In addition, Marx integrates

his value-labor theory (LTV, hereafter), his theory of the surplus value, absent in the understanding of

Ricardo (Carcanholo, 2002).

Since the eighties, the idea of calculating empirical values has emerged from the proposal of Shaikh

(1984). The author uses for the U.S. the input-output framework and Leontief data to estimate values and

direct and indirect labor requirements. These total requirements, standardized and expressed in money are

called direct prices, and also calculated Sraffian production prices and regression analysis and of distance

measures between the different prices, finding in general, values that approached quite well at current

prices (market). Ochoa (1984, 1989) again for U.S. and based on Shaikh methodology, calculates values,

direct prices, marxist production prices and sraffianos production prices using input-output tables (IOT,

hereafter) for several years, including measures of fixed capital in the estimations. Chilcote (1997)

updates the IOT for more recent years and OECD countries, in addition to examining the so-called

"alternative values (inputs other than labor which for some authors could also be explanatory such as

labor). Chilcote deepens as Ochoa in various ways of calculating the production prices gradually adding

different aspects: fixed capital, capital turnover, capacity utilization, etc. In this way producer prices are

conceptually closer to market prices. Both authors use different measures of distance, and conclude that

direct prices are quite close to production prices and even more to market prices. Cockshott y Cotrell

(1994), with IOT information from United Kingdom, consider the different kinds of prices and confirm

that the base values as electricity, petroleum, chemistry and agriculture do not explain better the current

prices than the estimated by labor. Guerrero (2000) following Chilcote, applies the methodology for

Spain finding that direct prices are closer to production ones if incorporating to the calculation fixed

capital, turnover etc. Guerrero also makes a thorough theoretical analysis of the calculated and developed

categories in this kind of studies and confirms that vertically integrates value capital compositions

explain almost totally deviations between direct prices and production ones, idea theorized by Marx in

volume III. On the other hand Tsoulfidis and Manitis (T&M hereafter) have applied this same

methodology to Greece with information from IOT from 1970. Tsoulfidis along with other authors has

extended this type of study to Korea, Japan, Canada and China. In the case of China, the central

difference in our study with that of Mariolis and Tsoulfidis (2009, with IOT from 1997 with 38 sectors) is

that incorporates data about fixed capital stock.

The structure of the research is as follows. After the introduction in the second section we will describe

the data and methodology used in this research. First, sources, data and adjustments made (2.1) and, right

away, the mathematical formalization and details of the determination of the different prices (2.2). In the

third section the empirical results are displayed, showing the different distance indicators among direct

prices, production prices, sraffianos ones and market ones (3.1). Immediately after comparing our results

of China to the proximity between prices found in the U.S., Greece and Spain. We will find very similar

results which reinforces the notion that current prices gravitate around the values raised by the LTV (3.2).

The fourth section addresses some specific replicas of LTV. Particularly that which suggests that human

labor is not the only one to explain the current prices as other prices aroused from requirements of

electricity and steel could supply the role of LTV (4.1). Another criticism that emerged recently in this

kind of work argues that the sector size can create a false correlation in regressions between values and

prices (4.2). In this section is shown how to create and incorporate a rank variable with vector size in

regression analysis does not become statistically significant values to explain current prices. On the other

hand, has also been raised that the regressions used may involve a bias in the estimates calculated, since

they omit the impact of vertically integrated compositions in the Shaikh prices model (4.3). It will be

exemplified empirically that this bias is minor in nature, since the explanatory variables of this model

imply a weak covariance. In the fifth section will appear under the different prices, levels of the key

variables in China: profit rate, rate of surplus value and composition of capital. Finally some conclusions

will be drawn.

2. Data and methodology

2.1 Sources and limits of statistics.

IOT for China are available for the period 1987-2005. These Tables are not published for every year,

although it certainly has been increasing the level of disaggregation in which they are presented.

Choosing to work with the Table of 2002 has been for several reasons: because it is a stable year in the

growth of China, because the data are deeply analyzed by other authors such as Holz (2006) and because

it will serve to better compare the results with other papers on deviations between prices (Greece and

Spain).

Most of the literature estimated the prices and productivity of China's economy has encountered problems

getting a reliable source for estimating capital stock. Beyond the statistical problems on the capital stock

we also had to face the problem of information on the labor force employed by each production sector.

This is because the China official statistical department publishes a very little detailed methodology and

unclear about how they are distributed and paid workers in the countryside and the city. Much of this

research was to estimate the statistics on labor and capital stock in China. For data on capital stock and

labor, were used the outstanding papers of the econometrist Gregory C. Chow (1993, 2002, 2006) as well

as Carsten A. Holzs (2006) who made pioneering estimates of the amounts of capital stock in China. The

IOT were obtained from the National Bureau of Statistics China (NBSC).

2.2. Methodology for calculating the different prices

Labor values are calculated according to expression one:

1

) (

D A I a

o

(1)

Where A is the technical coefficients matrix (39 sectors)

1

and D depreciation coefficients matrix, I

identity matrix and a

o

row vector of labor requirements

2

. Let`s explain how we can obtain a

o

. Labor

requirements represent direct labor required per production unit for j sector. However, the meaning of this

concept is still more complicated, as far as it includes reducing the concrete to abstract labor

3

. This,

theoretically, should be done weighing in some way the preparation of the workforce (in study years,

experience), but due to the lack of this information, for now, we are forced to reduce it by wages

rates. Thus, the abstract labor (Ta

i

) is the product of three components: the number of workers per sector

(Tc

i

), the annual working hours on (i

i

) and the relative salary rate (z

i

); more specifically, this last measure

is the ratio of average salaries for each sector among the lowest ones, which are agricultural.

i i i i

z i Tc Ta

(2)

For the calculation of (1) should be obtained before:

1

0

> < pb Ta a

Therefore:

1

> < pb T A

Where Tc

i

and Ta

i

are row vectors and T transactions matrix, A technical coefficients matrix, divided by

the gross production column vector invested and diagonalized (pb). Similarly, obtaining the depreciation

of fixed capital matrix, D, can be done as followed:

> < IL K D (3)

Depreciation matrix is the result of multiplying capital requirements square matrix (K) to produce one

unit of i for j sector, for the inverse of average life of capital goods column vector (IL) diagonalized. This

average was obtained following Holz estimation, Holz (2006: 162).

On the other side,

T

y

k f K (4) and i

i

j

fbcf

fbcf

f

1

(5)

Matrix (K) is the product of gross fixed capital formation participations row vector (f) y ratio

capital/sector product row vector (ky). Following this argumentation the estimation of direct and indirect

labor (values) from prices matrix and no quantities ones end in [

*

i

], this is, the quantity of total labor the

monetary unit of sector i.

Normalizing by the equation (6):

pb

pb U

T

This is, assuming that: pb pb U

T

(7)

Where U is a unit column vector and therefore (U

T

pb) represents the sum of sales at sectors market

prices. Then, direct prices are:

d= (8)

Production prices are defined following:

) ( ) ( B A K rp B D A p p + + + + +

(9)

Where p is production prices row vector, B salary goods requirements for workers square matrix and r

profit rate. We can rename and simplify the equation (9).

) ( ) ( M rp N p p +

,

where:

B D A N + + ; B K A M + +

( ) [ ]

1

) (

+ + D B A I B K A H

( ) [ ]

1

N I M H

Thus, the preceding eigenvalue equation defines the relation:

[ ] [ ] H p p

r

H p p

1

(10)

Following Perron-Frobenius we know the highest eigenvalue establishes the highest profit rate R (this is

R=r) and the associates left eigenvector of H, prices production without normalization, p*. As the former

case, we normalize using (11),

Pb p

Pb U

T

*

and obtain price production normalized:

* p p

(12)

Where p is marxist production prices row vector. We should highlight the two different ways of obtaining

B, following Chilcote (1997) and Guerrero (2000) or T&M (2002). If S and C are defined as salary

column vector and consume one both obtained by IOT. We can define:

C U

S U

x

T

T

(13)

Where x is, clearly, the proportion of consumption that is spent as salary. Then, we can define (14),

C x c

as row vector expressing consumption of salary goods for each sector. If we also define the

weight of employment in each sector as the following column vector (15),

1

> < Tc U Tc tcw

T

, this

weighting can be used for (16),

T

Tcw c E ) ( , this is the consumption square matrix in salary goods. The

last step is, as in the case of, A, D and K, expressing it in terms of gross production unit production:

1

> < pb E B

(17)

Sraffian prices can be obtained:

sA r sD sB s

s

) 1 ( + + +

(18)

This, like Marxist production prices, is an eigenvalue equation, where:

[ ] [ ]

s

H s s H s s * * 1

1

* *

1

]

1

(19)

In which

1

) (

B D I A H

s

. Similarly, we must normalize but now with (20),

pb s

pb U

T

*

, thus:

*

s s (21)

Where s is Sraffian prices row vector.

3. Empirical results

It is often mistaken empirical studies as mere statistical cumulus devoid of theory. However, in scientific

practice not all theoretical attempted is a scientific study and the same goes for empirical studies if they

are not supported by a theoretical model to contrast. The central hypothesis of these studies is to verify

the assertion that the values movements are determining prices movements. The methodology to get the

various prices involves the use of categories and concepts of the LTV that, due to its complexity in some

cases, are necessarily simplified in order to be estimated (vrg, reduction from complex to simple labor).

This type of study attempts to contrast a hypothesis as above within the broad LTV and under a very

specific model like Shaikh prices model (detailed in section 4.2). This is the context of empirical support

in this study.

3.1. The close proximity between values and prices in China, 2002

Next, in table (1), we present the distance measures that are usually shown in the literature. The Mean

Absolute Weighted Deviation (MAWD) between direct and market prices is 14.19%, while the distance

between direct and production ones is just 9.07%. The proximity between production and Sraffian prices

and market ones is even higher, 16.55% y 18.13% respectively. This is valid for the others distance

indexes, Mean Absolute Deviation (MAD), Normalized Vector Distance (NVD) and even with indexes:

d, Variation Coefficient, CV y proposed by Steedman & Tomkins (1998), who suggest to use these

parameters (d, CV, ) because they are independent of numeraire. As shown, these measures do not alter

the previous conclusions, direct prices and production are closer to market prices. It is interesting to note

that in China there is a greater proximity between (d,p) regarding (d,m), comparing with other studies

such as Ochoa`s (1989) for United States and Cockshott & Cotrell (1998) for United Kingdom

4

.

{Insert Table 1. Here}

Guerrero (2000) points out that in deviations among prices there is a in which, whether they are

calculated by the method that uses only circulate capital such as the one that adds capital stock, the results

are not very different. In exchange for profit estimates, it is observed a significant difference. Also, when

it comes to measuring the deviations between p, m and d, the initial hypothesis is that deviations between

p and m are greater, and this can be found for the case of China in this paper (see Table 1) as well as in

Tsoulfides and Marioles (2009). In the same way, the regression analysis (Table 2) between prices shows

the following order of determination: the direct price growth determines the movement of production

ones (98%) and the latter determine the market prices (95%). However, prices proportional to the value

determine the movement of market prices very significantly (96%). This is confirmed statistically by the

greater robustness of the t calculated for the elasticity of models and for the joint explanation with F-test

note the greater robustness (d,p) and (d,m), in that order. Sraffian prices explain satisfactory market

prices; however, production prices and direct ones do better from the Marxist perspective.

{Insert Table 2. Here}

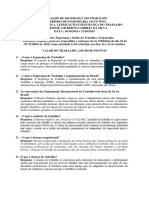

{Insert Figure 1. Here}

Figure 1 shows the dispersion of the different prices expressed in neperian logarithms, related to direct

prices (45 line). Each point represents a sector of the 39 used in China's TIO. It is slightly more dispersed

the cluster of points of market prices than production prices. But in general there is a good fit for different

prices. This means, in other words, the labor time direct plus indirect, expressed in money, is a useful

variable to explain to the production prices (Marxist and Sraffian) and market prices.

3.2. International Comparison: China, USA, Greece and Spain

Given the empirical research in recent years can make international comparisons of the distances between

these types of prices. With this purpose we will use data from 1970 from Greece (T&M 2002) and USA

(Ochoa 1989) for comparison with our results for 2002 for China and 2000 for Spain. In a general way

can be seen in the Table 3 that although there is a time lag between the countries compared, deviations in

the indices used do not exceed 26%, meaning, that for Marxist prices theory, the determination values

direct prices production prices market prices, is a valid general scheme to explain the prices system

in modern economies (Table 3).

{Insert Table 3. Here}

4. Some critics to the LTV.

If empirical support based on a theory and a specific model requires continuously analyze the relationship

between theory, categories and results, it is normal and necessary that contrast methods are also

continually reviewed (such as usually happens in natural sciences). Regression analysis and correlation

between prices have been the place of criticism of several authors. Without attempting to analyze all these

criticisms, we will briefly discuss some of them.

4.1 Comparing the labor values with other base values

Smith (1965: 47), Ricardo (1954: 22) and Marx (1990: 129) argued that the relative prices of

commodities are determined by the time of labor employed in production. In particular, for Marx, the

only value-creating factor is expressed as price is human labor. But the view that the labor value theory

determines the prices, is and has been persistently attacked because drives into analyzing capitalism on

the exploitation between social classes. Such critics argue that prices of goods could be measured by other

variables that refer to other theories of value, for example, wheat, steel, energy, etc. (see Guerrero 1997:

61-66). In this direction, Roemer (1981) and Hogdson (1982) suggest that the LTV would not be formally

the only theory that could explain the prices. However, these approaches miss a crucial question: What is

the only factor of production that is present in every processes of direct and indirect production of all

commodities?

{Insert Table 4. Here}

In Table 4 the DAMP between direct prices estimated from the different productive factors is presented

in ascending order of deviation, so between the LTV direct prices and market prices, the minimum

deviation found is 15.13%. The maximum deviation is established when using the farm inputs vector

(333.45%). On the other hand, in correlation of the direct prices of each "sector and alternative value" and

market prices we have that it is stronger with job requirements than with any other alternative productive

factor. The same findings throw the robustness of the t of the estimates of labor requirements and the joint

F-test. It should be noted that although estimates of alternative theories of value are statistically different

from zero, most robust estimator is the labor one an elasticity of 0.977 and greater individual significance

(33.55).

4.2. The relationship between prices and the size of each sector.

Might be expected that there is a necessary partnership between sectorial prices analyzed. Then, direct

prices and production ones would be correlated simply because small production sectors have small

prices d and p and sectors with higher production would have d and p prices proportional to the size. If

true, then the correlations obtained in regression analysis could hide a spurious component by the size of

sector, vgr. Kliman (2002) and Daz and Osuna (2009). This is a second critique of the LTV. To advance

an answer, we must remember that in econometrics temporal series, it is customary to monitor the effect

of the trend in the regression between two variables as in model (I). Then, if both series grow over time, it

is possible to isolate this component by incorporating a trend variable (t) as in model (II), of this way it

would be proves the relationship between Y and X excluding the underlying trend (as in well know

keynesian regression of consumption function explained by income). Returning to this idea, is similarly

possible in the cross-sectional analysis (III, between p and d, vgr.), approach to create a variable that

identifies the order of sectors sizes. This rank (R), orders each sector from lowest to highest according to

their level of production and incorporates it shaping the cross-sectional model (IV).

Y

t

=

1

+

2

X

2t

+ u

t

(I)

Y

t

=

1

+

2

X

2t

+

t + u

t

(II)

p

i

=

1

+

2

d

i

+ v

i

(III)

p

i

=

1

+

2

d

i

+

3

R

i

+v

i

(IV)

Figure 2 shows the correlation between prices: m, p, d and variable rank. The dispersion between these

variables in turn shows some unusual items that are modeled in the regressions of Table 5.

{Insert Figure 2. Here}

Model 1 and 2 of Table 5 shows how the inclusion of the rank variable, does not makes irrelevant the

direct prices to explain market prices. The models have a residue with homoskedastic and normal

distribution. Should be noted that all multiple models 2, 4 y 6 (where they are present more than one

explanatory variable), there appears not to be multicollinearity according to the determinant of the matrix

of explanatory variables, which does not approach zero and although are not reported of variance-

inflating factor (VIF) they did not turn out to be high. This way, being models 1 and 2 significant,

according to F-test, the direct price elasticity is also statistically significant individually. Can be stated

then for model 2, that with a 1% growth in direct prices, market prices will grow by 0.72%

5

, discounting

the effect of the sector size. A similar result is obtained with models 3 and 4, variable rank, again, is little

significative for production prices explaining market prices. It is interesting to note that the hierarchy of d

on p is maintained since the elasticity in model 4 is 0.625. In model 5 the explanation of p by d is not

affected by rank, in fact, this variable is not significant. Finally, model 6 explains production prices by

direct prices, Vertically Integrated Composition and variable rank. These variables are significant, but the

impact of proportional prices is also a unitary elasticity, even weighing the impact of other variables.

{Insert Table 5. Here}

In short, it seems that by including a variable that controls the size of the sector the relationship between

different prices remain significant. This suggests that the critique of spurious correlation is either small or

of no significant amount.

4.3 The effect of an omitted variable in the relationship between values and prices

Another critique of LTV arises from the possibility of bias of the estimates in the regressions among

prices. To understand the problem let us consider the Shaikh production prices model (1984 y 1990: 103-

112). Assuming any price (pc), they shall consist of the amount of wages, wage workload (wL) plus

profits () and material costs (M).

M wL p

c

+ +

These material costs are in turn composed of the same items:

) 1 ( ) 1 ( ) 1 (

M wL wL p

c

+ + + +

Where the superscript (1) indicates another stage of production. The other materials from other stages in

turn used other wages, profits and materials. Thus the price of a commodity can be viewed as the sum of

wages and earnings integrated.

T T

c

W p +

Where,

) ... (

) ( ) 2 ( ) 1 ( n T

L L L L w W + + + +

) ( ) 2 ( ) 1 (

...

n T

+ + + +

Consequently, above expression reduces to:

T

T

c

W

Z where Z w p

+ ) 1 (

Being Z the integrates quotient profit-wage, w salary rate and values.

If we relate two prices i and j:

) 1 (

) 1 (

j j j c

i i i c

Z w p

Z w p

+

+

ij ij

j j

i i

j

i

ij

z

Z w

Z w

p

p

pc

+

+

) 1 (

) 1 (

Any kind of relative prices depends on the product of relative values and relative integrated quotients

profit-wage. This works for any kind of price. But here Shaikh introduces a fundamental requirement in

the formation of production prices: He assumes that profits are equal to the product of profit rate (r) by

the total advanced integrated capital (K

T

).

T

K r

Then,

T

T

i

L

K

w

r

z

That is why now:

T

j

T

j

T

i

T

i

ij

L

K

L

K

z

ij ij ij

T

j

T

J

j

T

i

T

i

i

ij

z p

L

K

w

r

L

K

w

r

p

+

+

) 1 (

) 1 (

Simplifying with logarithms:

ij ij ij ij ij ij

z p p z ln ln ln ln ln ln +

By normalizing the production prices and direct ones and evaluating econometrically the previous model,

in general, empirical studies contrast:

i i i

u d p + + ln ' ' ln

1 0

(i)

However, considering all the variables could be adjusted:

i i i i

v z d p + + + ln ln ln

2 1 0

(ii)

There arises the need to assess whether there is bias in that

1

violates the LTV due to the exclusion of z

i

.

To this end, we consider also estimates:

i i i

w z p + + ln ln

1 0

(iii)

i i i

d z + + ln ln

1 0

(iv)

Although the bias and consistency of an estimator should be evaluated by the expected value and the limit

of the probability in an equation

6

, is possible to find a relationship between

1

and

1

using models (i-iv)

estimated by OLS. Can be shown of (i-iv) and coefficient

2

, z d

r

that

7

:

1 1

2

, 1 1 1

' +

z d

r

Always for sample values, if the coefficient of determination (

2

,z d

r

) is null, also will be coefficient

1

and,

for this reason,

1 1

' , this is, there is no bias, however if,

0

2

,

z d

r

there will be a difference established

by the previous equation. Coefficient

2

, z d

r

, as well as the estimated

1

are of moderate size, so the bias

will be small. After all, at the sectorial level the huge direct prices in agriculture or services need not be

associated with higher levels of vic (vertically integrated composition). At a theoretical level, the values

of different sectors should not have a relationship with their vic. If the vector d is a vector proportional to

the values, then it should not be associated either with the vic. In a log-log model the elasticity obtained in

(i) and (ii) will be very close to unity, however, this is an empirical question. For the previous models has

the following variances and covariances matrix of variables (Table 6).

{Insert Table 6. Here}

With this information we can calculate the elasticities of the models (i-iv) y and

2

,z d

r

.

664684 . 3

021520 . 0

078864 . 0

) var(ln

) ln , (ln

048570 . 1

238096 . 1

298231 . 1

) var(ln

) ln , (ln

'

1 1

z

z p Cov

d

d p Cov

120985 . 0

) var(ln ) var(ln

)] ln , (ln [

045857 . 0

238096 . 1

056776 . 0

) var(ln

) ln , (ln

2

2

, 1

z d

z d Cov

r

d

d z Cov

z d

1.001710

)] ln , (ln [ ) var(ln ) var(ln

) ln , (ln ) ln , (ln ) var(ln ) ln , (ln

2 1

d z Cov z d

d z Cov z p Cov z d p Cov

Then the bias can easily be deduced:

04716 . 0 ) ' ( : 048870 . 1 ] 04686 . 0 [ 001710 . 1 ] [ '

1 1

2

, 1 1 1 1 1

+ + bias r

z d

Therefore, the important conclusion is that no matter the size of the effect of ln z in ln p, if the association

among ln z and ln d is weak, the bias between

1 1

' y will be small in that measure. These observations

on the regression analysis recognize the need to further development of improved econometric

estimations. However, is shown that traditional empirical work based on a theoretical model such as

Shaikh's (1984) is still useful to explain the relationships among them

8

.

5. The level of fundamental variables in China

The calculations of the main Marxist variables: rate of profit, surplus value and composition of capital,

have specific behaviors when compared internationally with other researches. However, they follow the

guidelines outlined by the Marx theory. The rate of profit (r '), the rate of surplus value (s') and the capital

composition are defined as:

pb K p

pb D A I p

r

pb B p

pb D A I p

s

T

i u

T

i u

T

i u

T

i u

,

,

,

,

) (

'

) (

'

1

,

1

,

,

,

) (

) (

D A I B p

D A I K p

ccvi

pb B p

pb K p

ccs

T

i u

T

i u

T

i u

T

i u

Where

T

i u

p

,

are the row vectors of the various unit prices i, which indicates the various prices: d, p, s y

m. The other matrices and their orders have been defined above. We estimated the simple organic

composition (ccs) and a version of the vertically integrated composition (vic), with the aim to relate

immediately r=s/ccs and observe the levels of profitability rate based on the known s' and ccs, but also

to compare the ccs and vic (which presents a better inter-sectorial homogeneity).

{Insert Table 7. Here}

The fundamental variables in direct prices and production ones are almost identical, the differences are

only slightly higher between market prices and direct ones, as concluded above (column 5 and 6 of table

7). The rate of return (r ') in value appears to be higher than shown in current prices. It should be

remembered that in 2002 China's economy was expanding rapidly (in real terms grew by over 8%, Holz

2006: 113). Profitability levels are relatively high, between 51% and 58% if considered only the fixed

capital, but past relationships are maintained by adding the variable capital where levels change between

31% and 37%. With the limitations involved in comparing different IOT is interesting to note that with or

without weighting fixed capital, the profit rate of China is greater than that shown for other countries

around the same year with the same methodology and measurement of r'. In Spain, for example, with of

an IOT disaggregated to 65 sectors in 2000 the return is: 16.09%, 17.29% and 13.38% for market prices

direct ones and production ones respectively (Snchez and Nieto, 2010). On the other hand, in Korea with

of an IOT disaggregated to 27 sectors in 2000 and for the same price, returns are 11.6%, 13.6% and

13.3% (Tsoulfidis and Rieu, 2006). In contrast, when comparing rates of surplus value (s'), whereas in

China these are between 96% and 100% in Spain are between 66 and 76% and in Korea between 73%

and 86%. In short, China has a higher profit rate, based on a lower composition level (a measure of

technical change) but with a higher level of exploitation. This is interesting because following proposal of

Emmanuel (1972); Carchede (1991) and Shaikh (1998)-for whom the law of value operates at

international level - high profit rates are poles for attracting capital. Reflection of the high mobility of

international capital and the strong attraction of Foreign Direct Investment (FDI) are the poles of higher

rates of profit. Is not by chance that, in recent years, China has received a large amount of investment.

Investment in mainland China has already exceeded 100 billion dollars and the total investment amount

(Hong Kong, Macao and Taiwan) in 2008 surpassed 170 billion dollars in 2009.

6. Conclusions

The results of the close proximity between prices in Chinas case agree to other recent papers. The

weighted average absolute deviation between direct and market prices is 15.13%, while between direct

prices and production ones is only 9.07%. These results are not modified by changing the measure of

deviation or distance. The meaning and order in the vicinity is not significantly affected. It seems that for

one of the largest economies in the world, the force of attraction that have values to different prices is

quite strong, in particular, changes in values determine the variations in current prices by 97%. The

regression analysis between the different prices also shows this conclusion, in line with what has been

found in several countries like USA, Greece, Korea, Spain, etc...

Since Shaikh and Ochoa (1984) empirical studies, some doubts have been raised about the use of

correlation and regression analysis to assess the relationship between values and prices. Without

intending to answer to all approaches made so far, this papers deals with three aspects: the validity of

other alternative theories of value, the effect of the sector size in the regressions and the magnitude of bias

involved in excluding a variable in the model Shaikh for prices. As in the researchs Cockshott and

Cotrell (1995, 1997 and 1998), assessing other direct requirements to explain market prices, electricity

requirements, the chemical industry, oil, etc. have no higher goodness of fit and increased robustness in

their regressions. In this direction, the idea that the labor theory of value can be replaced by another

theory of value steel empirically remains in doubt. On the other hand, has been argued that sector size

could cause a false correlation, since it would necessarily have a direct association between the different

prices as those are related by the effect of physical production. Analogous to the use made of the trend in

the econometric analysis of time series, we propose the use of a variable in ascending order of production

levels; this variable has been appointed rank. The use of an instrument as the rank variable does not

make the goodness of fit previously found significantly modified. In the case of the relationship between

direct and market different prices, include the rank variable, the estimator that measures the direct price

effect on market prices does not become insignificant. Even when evaluating the regression between

prices of production explained by direct prices, the variable rank, is not significant as discussed above,

this study found greater closeness between these different prices. Finally, it could be argued that omitting

a relevant variable in the model that explains the different prices of production, like vertically integrated

compositions, there may be a bias in the estimated elasticity. This is just true to the extent the direct

prices are related to them. Theoretically there is no relationship between the various sectorial values and

vic, in any case, the correlation for a sample is very sparse, which makes the bias to be small. In the case

of China, this bias found was smaller as the coefficient of determination between ln p and ln vic is only

12%. A final point to emphasize is that China seems to show a relatively high rate of profit as the range of

this measured with different prices lies between 51% and 58% only fixed capital weighted. But, even

taking into account circulating capital the range goes down between 33% and 37%. In short, profitability

in China (2002) is well above profitability found with very similar methodologies in countries like Korea

(2000) and Spain (2000), below 18% for different prices. Again, it appears that the LTV has the empirical

explanatory power to assess the dynamism in an economy like China.

Apendix I

Deviation measures

If we deal, for example, with direct prices (d) and production ones (p), mean absolute deviation between

them is:

n d

d p

DAM

n

i i

i i

1

1

(1)

This measure assumes that a sector has the same weight as others, so may be more useful to ponder the

weight of each sector in the production (q). The weighted average absolute deviation is then defined as:

,

_

n

i

i

i

n

i i

i i

q

q

d

d p

DAMP

1

1

(2)

The normalized vector distance is used by Ochoa (1989) and is defined as:

n

i

i i

n

i

i i i i

q p

q d q p

DVN

1

2

1

2

) (

) (

(3)

A weighted measure (in addition to DAMP) is the Theil index of inequality, although based on a price

vector. In d case:

[ ]

1

1

1

1

1

1

1

]

1

1

1

1

1

]

1

1

]

1

n

i

n

i

i

i

n

i

i

i

n

i

i

i

i

i

n

i

i

d

d

p

p

d

d

d

p

d Theil

1

1

1

1

1

ln

~

~

ln

~

(4)

Gini coefficient:

It is the most popular measure for inequality and therefore deviation, but it should be noted here that it is

just an indicative measure, since the formulation is built for ungrouped data (Milanovic, 1997), however,

is calculated as it conceptually involves variation and correlation coefficients.

[ ]

1

]

1

1

]

1

) / 1 ( 1

) , (

3

1

n

CV G

(5)

Vector

i

i

d

p

is written in ascending order and is associated with a vector that indicates that order (),

subsequently we obtain the correlation between them.

Coefficient of variation is the quotient between of standard deviation and mean deviation.

n

V C

i

2

) (

. .

(6)

The distance Steedman y Tomkins (1998), is defined as:

)) ( cos 1 ( 2

2

2

,

_

sen d

(7) showing that:

. . ) ( tan V C

Defined

as a vector (see last Gini coefficient) and U unit vector, the angle measured in degrees can be

deduced as:

U U

U

' '

) ' (

arccos

(8)

Notes

The IOT originally of 42 sectors was reduced to 39, eliminating those non-mercantile.

2

For simplicity reasons, A is weightened as annual rotation. Must be warned that, even deviation between values and prices

should not be notably altered, levels of fundamental variables can suffer modification.

3

A proposal of reduction to simple labor, based in Brody (1970), is developed in Guerrero (2000), However, such as raised by

this latest study, disaggregated information is needed on labor which is currently not yet available.

4

It is interesting to note that in China there is a greater proximity between (d,p) and (d,m), when comparing with other studies

like Ochoas (1989) for U.S and Cockshott & Cotrells (1998) for United Kigdom. Further details in section 3.2.

5

The confidence interval for the estimated elasticity of 0.724 is, in fact,: [0.60, 0.84].

6

When it comes to seeing the relationship of sample value to their population value, the relations are simplified. In fact, the

expected value, i.e. the average value with infinite sampling of 1 in (i) is: E(1)= 1+21, while the consistency of the

same is the limit of the probability when the sample size grows indefinitely: plim (1)= 1+21. In both concepts the

important aspect is the size of the Cov (ln z, ln d) because the latter determines the value 1. What is made with models (i-iv)

is simply to find a relationship of OLS estimation of the coefficients 1 and 1. It should also be noted that the standard

deviation of 1 'is greater and so the estimator is inefficient.

7

The estimator 1 can be inferred directly of the normal equations of OLS in a model with two explanatory variables.

8

For example, Valle (2010) and Frlich (2011) show the total validity of the measures correlation and distance between values

and prices, from the viewpoint of dimensional analysis (DA). This type analysis has unfortunately been neglected in

economics, still quite useful for checking the consistency of an equation, an instrument used quite frequently in economic

modeling and corroboration. Discussion about correlation and measure distance between values and prices is undetermined,

and, therefore, the relation between these two variables was unverifiable empirically has been superseded (Daz y Osuna,

2009). Valle and Frlich show that correlation between two non-homogeneous vectors is an impossible operation. Focusing

just in the correlation coefficient, the relationship between sectorial p and d must be value like Corr (puq, duq), where prices

vectors are unitarian multiplied by its quantities, this is, Corr (p, d) calculated in this paper. While Corr(pu , du) must be seen

as an impossible operation more tan undetermined. Of course, when dealing with sector producing more than one good and

with information in money and no in physical quantities, discussion terms are a Little bit modified but not in conclusion and

sense: only homogeneous variables can be correlated. Because of this, correlation coefficient is not modified by the units

measure change in unitarian prices such as is determined by (DA). This way, continues being valid and precious for economic

theory empirical corroboration between values and prices.

Tables, Pictures and Graphics

Table 1 - Deviation measures among prices

Deviation

Measures

(d,m) (d,p) (p,m) (s,m)

1. MAD

14.19 12.01 16.54 18.50

2. MAWD

15.13 9.07 16.55 18.13

3. NVD

23 8.7 25.5 22.9

4. Theil

2.03 0.76 2.94 3.16

5. Gini

10.7 8.9 13. 14.1

6. C.V.

19.25 15.53 23.25 24.58

7. d

18.99 15.39 22.79 24.04

8. (degrees) 10.89 8.82 13.08 13.81

Note: Where; d = direct prices, p = production prices, s = sraffian production prices y m = market prices. Deviation measures are defined in the Appendix.

Table 2 - Simple log-log regressions among prices

Models F R

2

mi = f(di) ln mi = 0.64 + 0.97 ln di + ui

t (0.82) (33.50)

1122.29 96.81%

pi = f(di) ln pi = -0.59 + 1.04 ln di + ui

t (-2.43) (50.37)

2537.38 98.56%

mi = f(pi) ln mi = 0.99 + 0.91 ln pi + ui

t (2.54) (27.34)

747.49 95.28%

mi = f(si) ln mi = 1.24 + 0.89 ln si + ui

t (3.18) (26.74)

715.46 95.08%

Note: Being n=39 sectors and k=2 number of estimator, critical value t/2 with freedom degrees n-k=3740, so t5%/2=2.02. As we know, in these models, critical

value of F 5% significance is F(k-1), (n-k) F1,40= t

2

5%/2 = 4.08. Thus, to be larger t and F values calculated than critical values are statistically significant: the

explanatory variables used and the model in general.

Figure 1 - Dispersion of different prices related to direct prices.

Table 3 - Deviation and correlation between values and prices: China, USA, Greece and Spain

Direct prices/market prices

(d,m)

Production prices/market prices

(p,m)

Direct prices/production prices

(d,p)

China

2002

USA

1970

Gr

1970

Sp

2000

China

2002

USA

1970

Gr

1970

Sp

2000

China

2002

USA

1970

Gr

1970

Sp

2000

DAM 14.1 10.3 23.1 12.2 16.5 12.5 14.3 18.8 12.01 16.9 18.7 19.0

DAMP 15.1 11.1 21.6 11.0 16.5 13.1 15.4 18.9 9.07 17.8 18.1 19.0

DVN 23.0 12.7 25.1 13.2 25.5 15.3 20.4 20.6 8.7 18.3 23.0 20.5

R

2

97.8 97.8 94.2 97.8 94.9 98.6 93.9 95.8 94.3 97.1 97.1 95.4

Note: Data for USA are from Ochoas (1989) with 71 sectors, data for Greece are from T&Ms (2002) with 35 sectors and to Spain from Snchez and Nieto`s

(2010) with 65 sectors.

Table 4 - Deviation and regression of the labor value and "base values" on market prices

Independent

Variable

MAWD %

(d,m)

Models F R

2

Labor 15.13

ln mi = 0.280 + 0.977 (ln di ) + ui

t (0.825) (33.500) 1122.29 96.81%

Electricity 35.46

ln mi = 227 + 0.706 (ln di ) + ui

t (2.548) (8.916) 79.50 68.83%

Chemistry 37.14

ln mi = 140

+ 0.806 (ln di ) + ui

t (1.762) (10.304) 106.171 74.68%

Oil 61.13

ln mi = 571

+ 0.256 (ln di ) + ui

t (4.666) (3.073) 9.446 20.79%

Farm 333.45

ln mi = 725

+ 0.067 (ln di ) + ui

t (7.052) (3.325) 11.062 23.51%

Note: For alternative bases values, the first estimator is 10

9

RMB.

Figure 2 - Dispersions between prices and la variable rank

24

25

26

27

28

29

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30 31

32

3334

35

36

37

38

39

l

n

m

24

25

26

27

28

29

30

1

2

3 4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31 32

33

34

35

36

37

38

39

l

n

p

1

2

3 4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31 32

33

34

35

36

37

38

39

0

10

20

30

40

24 25 26 27 28 29 30

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

ln d

R

a

n

k

24 25 26 27 28 29

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

ln m

24 25 26 27 28 29 30

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

ln p

Table 5 - Different price regressions including the variable rank and VIC

(below p. values)

Mod.1 Mod.2 Mod.3 Mod.4 Mod.5 Mod.6

Dependent variable ln(m) ln(m) ln(m) ln(m) ln(p) ln(p)

Independent variable

Constant 0.646 6.849 1.777 9.408 0.266 -2.13

0.414 0.00005 0.0304 0.0001 0.8766 0.8154

ln (d) 0.977 0.724 0.982 1.01

<0.0001 <0.0001 <0.0001 <0.0001

ln (p) 0.936 0.625

<0.0001 <0.0001

ln (vicr) 1.02

<0.0001>

Rank 0.027 0.033 0.006 -0.001

0.00004 0.0001 0.3196 0.0048

Dummy 0.447 0.808 0.579 -0.03

<0.0001 0.0007 <0.0001 <0.0001

R

2

0.968 .9884 0.9658 .9802 0.9860 0.999

Adjusted R

2

0.967 .9874 0.9639 .9785 0.9852 0.999

F (k-1, n-k) F(1,37) F(3,35) F(2,36) F(3,35) F(2,36) F(4,34)

F-statistic 1122.2 1000.2 508.7 496.6 1269.8 217624

<0.0001 <0.0001 <0.0001 <0.0001 <0.0001

Homoskedastic

White 0.8807 0.6862 0.7315 0.6475 0.1345 0.4469

Breusch-Pagan 0.6891 0.9032 0.7184 0.2750 0.4281 0.3253

Koenker 0.6891 0.9181 0.7837 0.2524 0.2902 0.2366

Normality

Chi-squared 0.18929 0.25521 0.165189 0.7598 0.4756 0.9670

Multicollinearity

Determinant XX - 2338594.4 - 1781802.1 861720.9

3069527.5

590067.2

Note: The variable dummy, controls outliers for model 2 in sectors: 3, 11 y 28, for model 3: just in sector 3, for model 4: 3 and 11 and for model 6: the sector

11. All econometric estimates have been developed in Gretl, free software, designed and supported by Allin Cotrell.

Table 6 - Variances and covariances matrix of the variables: p, d and z (in logarithms)

Ln p Ln d Ln z

Ln p 1.381137 1.298231 0.078864

Ln d 1.298231 1.238096 0.056776

Ln z 0.078864 0.056776 0.021520

Table 7 - Marxist Fundamental Variables

Market

prices

(1)

Direct

prices

(2)

Production

prices

(3)

Sraffa

production

prices

(4)

(2)/(3) (2)/(1)

Profit rate % (r) 51.24 56.18 56.02 58.45 1.002 1.096

Surplus rate% (s) 100.41 96.82 96.21 102.24 1.006 0.964

Simple organic composition

(ccs)

1.9593 1.7231 1.7173 1.7492

1.005

0.882

Vertically integrated

composition (vic)

2.2609 1.9884 1.9817 2.0185 1.003 0.876

Bibliography

Carcanholo, R. A. 2002. Ricardo e o fracasso de uma teoria do valor. Curitiba, In: VII Encontro Nacional

de Economia Poltica, Anais do VII Encontro Nacional de Economia Poltica.

Chilcote, E. 1997. Interindustry structure, relative prices and productivity: an input-output study of the

U.S. and O.E.C.D countries, theses doctoral no posted, New York, New School for Social Research.

Cockshott, P., Cottrell, A. and Michaelson, G. 1995. Testing Marx: some new results form UK data,

Capital and Class, vol. 55, Spring, pp. 103-29.

Cockshott, P. and Cottrell, A. 1997 Labour time versus alternative value bases: a research note,

Cambridge Journal of Economics, vol. 21, pp. 545-49.

Cockshott, P. and Cottrell, A. 1998. Does Marx need to transform?, in R. Bellafiore (Ed.) Marxian

economics: A Reapparasal, vol. 2 Basingstoke, McMIllan st Martins Press.

Chow, G.C. 1993. Capital Formation and Economic Growth in China, Quarterly Journal of Economics

vol. 108. pp. 809-42.

_________ 2006. New Capital Estimates for China: Comments, China Economic, Review 17, pp. 186-92.

Chow, G.C. and Kui-Wai Li 2002. Chinas Economic Growth: 1952-2010, Economic Development and

Cultural Change, vol. 51, 247-56.

Daz-Calleja, E.; Osuna, R. 2009. From correlation to dispertion: geometry of the prices- value

deviation, Empirical Economics, vol. 36(2), pp. 427-440.

Frlich, N. 2010. Dimensional analysis of price-value deviation. Chemnitz University of Technology.

http://www.boeckler.de/pdf/v_2010_10_29_froehlich.pdf

Guerrero, D. 2000. Teora del valor y anlisis insumo-producto, manuscrito, 158 pp.

Hogdson, G., Capitalism, Value and Explotation, Oxford, Martin Robertson, 1982.

Holz, C.A. 2006. Measuring Chinese Productivity Growth, 1952-2005, disponible en SSRN:

http://ssrn.com/abstract=928568

Kliman, A. 2002. The law of value and laws of statistics: sectoral values and prices in the US economy,

1977-1997, Cambridge Journal of Economics, vol. 26, pp. 299-311.

Mariolis, T. y Tsoulfidis, L. 2009. Decomposing the Changes in Production Prices into Capital-

Intensity and Price Effects: Theory and Evidence from the Chinese Economy, Contributions to

Political Economy.

Marx, K. 2002. El Capital, Libros, I, II y III, Madrid, S. XXI.

Meek, Ronald. 1980. Smith, Marx y despus: Diez ensayos sobre el desarrollo del pensamiento

econmico, Madrid, Ed. Siglo XXI.

Milanovic, B. A simple way to calculate the Gini coefficient, and some implications. Economics

Letters, vol. 56, issue 1, 1997, pp. 45-49.

Ochoa, E. 1984. Labor Values and Prices of Production: An Interindustry Study of the U. S. Economy,

1947-1972, Ph. D. dissertation, Department of Economics, New School for Social Research, New York.

Ochoa, E. 1989. Values, prices and wage-profit curves in the U.S. economy, Cambridge Journal of

Economics, vol. 13, pp. 413-429.

Roemer, J. Analytical Foundations of Marxian Economic Theory. Cambridge University Press, 1981.

Shaikh, A. 1984. The Transformation from Marx to Sraffa: prelude to a critique of the neo-ricardians, in

E. Mandel and A. Freeman (eds.), Ricardo, Marx, Sraffa: The Langston memorial volume, London,

Verso, pp. 43-84.

Shaikh, A. 1990. Valor, acumulacin y crisis, Bogot, Tercer Mundo Editores.

Tsoulfidis, L. 2008. Price-Value Deviations: Further Evidence from Input-Output Data of Japan.

International Review of Applied Economics.

Tsoulfidis, L. and Paitaridis, D. 2008. On the Labor Theory Value: Statistical Artefacts or

Regularities?, Research in Political Economy.

Tsoulfidis, L. and Rieu, D. 2006. Labor Values, Prices of Production and Wage-Profit Rate Frontiers of

the Korean Economy, Seoul Journal of Economics.

Tsoulfidis, L., Maniatis, T. 2002. Values, prices of production and market prices: some more evidence

form the Greek economy, Cambridge Journal of Economics, vol. 26, pp. 359-369.

Steedman, I. and Tomkins, J. 1998. On measuring the deviation of prices from values, Cambridge

Journal of Economics, vol. 22, no. 3, pp. 379-85.

Valle, A.1994. Correspondence between labour values and prices: a new approach, Review of Radical

Political Economics, vol. 26, no 2, pp. 57-66.

Valle, A. 1991. Valor y precio: una forma de regulacin del trabajo social. Facultad de Economa,

UNAM, Mxico.

Valle, A. 2010. Dimensional analysis of price-value correspondence: a spurious case of spurious

correlation. Investigacin Econmica. UNAM. Mxico.

Das könnte Ihnen auch gefallen

- Direitos TrabalhoDokument2 SeitenDireitos TrabalhoLuis Marques Lavrador67% (6)

- Proposta Administração de Obra-ProtectedDokument4 SeitenProposta Administração de Obra-ProtectedLucas KaiqueNoch keine Bewertungen

- Plano de Cargos e SaláriosDokument42 SeitenPlano de Cargos e Saláriosijaraujo98% (105)

- Formulario Entrevista de DesligamentoDokument3 SeitenFormulario Entrevista de DesligamentoAnnaDoyNoch keine Bewertungen

- A Agricultura No Crescimento Economico RegionalDokument11 SeitenA Agricultura No Crescimento Economico RegionalD. Silva EscobarNoch keine Bewertungen

- NETTO, José Paulo. Lukács Guerreiro Sem RepousoDokument105 SeitenNETTO, José Paulo. Lukács Guerreiro Sem RepousocuernicabraNoch keine Bewertungen

- Michal Kalecki - Teoria Da Dinâmica EconômicaDokument193 SeitenMichal Kalecki - Teoria Da Dinâmica EconômicaMarcelo K Mata100% (1)

- Formação de Preços Como Processo Complexo - Nova VersãoDokument40 SeitenFormação de Preços Como Processo Complexo - Nova VersãoD. Silva EscobarNoch keine Bewertungen

- Uma Formalização Da Mão InvisívelDokument20 SeitenUma Formalização Da Mão InvisívelD. Silva EscobarNoch keine Bewertungen

- Ciência Positiva e Crítica DialéticaDokument14 SeitenCiência Positiva e Crítica DialéticaD. Silva EscobarNoch keine Bewertungen

- Historia em A Ideologia AlemãDokument12 SeitenHistoria em A Ideologia AlemãD. Silva EscobarNoch keine Bewertungen

- Dialética e EvolucionismoDokument18 SeitenDialética e EvolucionismoD. Silva EscobarNoch keine Bewertungen

- Dialética e Realismo CríticoDokument22 SeitenDialética e Realismo CríticoD. Silva EscobarNoch keine Bewertungen

- Reflexoes Sobre o SocialismoDokument6 SeitenReflexoes Sobre o SocialismoD. Silva EscobarNoch keine Bewertungen

- Correção Contestação - Loteria Alfa LtdaDokument10 SeitenCorreção Contestação - Loteria Alfa LtdaJúlia FariaNoch keine Bewertungen

- Teoria de Administração Científica de Taylor-1Dokument7 SeitenTeoria de Administração Científica de Taylor-1Summer Márcio DomingosNoch keine Bewertungen

- Direitos dos grevistas e do empregadorDokument4 SeitenDireitos dos grevistas e do empregadorPauloNoch keine Bewertungen

- Requerimento Pessoa Fisica PDFDokument2 SeitenRequerimento Pessoa Fisica PDFAlexandre HugenNoch keine Bewertungen

- Regras férias MPUDokument9 SeitenRegras férias MPUJOSE OLIVEIRANoch keine Bewertungen

- Trabalho noturno: direitos e regrasDokument9 SeitenTrabalho noturno: direitos e regrasPatrícia FreitasNoch keine Bewertungen

- Ebook Guia FeriasDokument16 SeitenEbook Guia FeriasallanmauNoch keine Bewertungen

- Trabalho Sobre Saúde e Segurança Do TrabalhoDokument4 SeitenTrabalho Sobre Saúde e Segurança Do TrabalhoCapelania Militar Evangélica100% (1)

- Reclamação trabalhista por danos morais e verbas rescisórias não pagasDokument5 SeitenReclamação trabalhista por danos morais e verbas rescisórias não pagasRenan GiolloNoch keine Bewertungen

- Curso 192920 Aula 04 Af1e CompletoDokument109 SeitenCurso 192920 Aula 04 Af1e CompletocamilaNoch keine Bewertungen

- Trabalhadores de Aplicativos_ Seus DireitosDokument6 SeitenTrabalhadores de Aplicativos_ Seus DireitosRenato Rj limaNoch keine Bewertungen

- Sim - Como Fazer - PPPDokument18 SeitenSim - Como Fazer - PPPAlex SandroNoch keine Bewertungen

- DDS - O Papel Intimativo Da LeiDokument1 SeiteDDS - O Papel Intimativo Da LeiLuiz Rubens Souza CantelliNoch keine Bewertungen

- Apostila Adminitracao RH e Materiais Giovanna CarranzaDokument98 SeitenApostila Adminitracao RH e Materiais Giovanna CarranzaAlanCarlosDaSilvaFerreira100% (1)

- 04 - Seceg e Sindilojas 2019 - 2020Dokument5 Seiten04 - Seceg e Sindilojas 2019 - 2020andreNoch keine Bewertungen

- KEYNESIANISMODokument3 SeitenKEYNESIANISMOMarina PereiraNoch keine Bewertungen

- LIVRO CAP 2 - ADM de RH - George Bohlander-Scott SnellDokument41 SeitenLIVRO CAP 2 - ADM de RH - George Bohlander-Scott SnellFelipeNoch keine Bewertungen

- Tabela Das Verbas Salariais e IndenizatóriasDokument1 SeiteTabela Das Verbas Salariais e IndenizatóriasADRIANO COSTANoch keine Bewertungen

- Resumo das Normas Regulamentadoras NR 1 a 20Dokument34 SeitenResumo das Normas Regulamentadoras NR 1 a 20Fabricio Santos FerreiraNoch keine Bewertungen

- Abandono de emprego: entenda a falta grave e seus prazosDokument8 SeitenAbandono de emprego: entenda a falta grave e seus prazosFinanceiro - GSL ContabilidadeNoch keine Bewertungen

- Direitos e funções dos sindicatos segundo a CLTDokument3 SeitenDireitos e funções dos sindicatos segundo a CLTGabriel TheCatNoch keine Bewertungen

- Requisitos Legais AplicaveisDokument472 SeitenRequisitos Legais AplicaveisAdony AmorimNoch keine Bewertungen

- Motivação em tempos de criseDokument66 SeitenMotivação em tempos de criseRui Matias0% (1)

- Os - Carpinteiro C C G F Engenharia e Construcoes LtdaDokument2 SeitenOs - Carpinteiro C C G F Engenharia e Construcoes LtdaThiagoPachecoNoch keine Bewertungen

- Manual DIRF 2021Dokument60 SeitenManual DIRF 2021Alex BatistaNoch keine Bewertungen

- Experiência saúde humanaDokument2 SeitenExperiência saúde humanaCaio ReisNoch keine Bewertungen