Das könnte Ihnen auch gefallen

- Phpy MX0 QKDokument5 SeitenPhpy MX0 QKfred607Noch keine Bewertungen

- PHP KPPYp 5Dokument5 SeitenPHP KPPYp 5fred607Noch keine Bewertungen

- PHP 4 Nuv M4Dokument7 SeitenPHP 4 Nuv M4fred607Noch keine Bewertungen

- PHPV Iwg QMDokument5 SeitenPHPV Iwg QMfred607Noch keine Bewertungen

- Phpi 2 KB 84Dokument5 SeitenPhpi 2 KB 84fred607Noch keine Bewertungen

- PHP KXTT WRDokument5 SeitenPHP KXTT WRfred607Noch keine Bewertungen

- Phpdfasf KDokument5 SeitenPhpdfasf Kfred607Noch keine Bewertungen

- PHP IIt TPKDokument5 SeitenPHP IIt TPKfred607Noch keine Bewertungen

- PHP XgsukaDokument5 SeitenPHP Xgsukafred607Noch keine Bewertungen

- PHP J0 S DQWDokument5 SeitenPHP J0 S DQWfred607Noch keine Bewertungen

- PHPP 2 KBC LDokument5 SeitenPHPP 2 KBC Lfred607Noch keine Bewertungen

- PHP Ks 19 AMDokument5 SeitenPHP Ks 19 AMfred607Noch keine Bewertungen

- PHPD 2 XGzeDokument5 SeitenPHPD 2 XGzefred607Noch keine Bewertungen

- PHPXK YO6 UDokument6 SeitenPHPXK YO6 Ufred607Noch keine Bewertungen

- Phpvvu NG PDokument5 SeitenPhpvvu NG Pfred607Noch keine Bewertungen

- PHP G9 Mu KaDokument6 SeitenPHP G9 Mu Kafred607Noch keine Bewertungen

- Low Back: ECONOMIC DATA With ImpactDokument5 SeitenLow Back: ECONOMIC DATA With Impactfred607Noch keine Bewertungen

- PHP Ej HW SSDokument6 SeitenPHP Ej HW SSfred607Noch keine Bewertungen

- PHP 1 Ezpt IDokument5 SeitenPHP 1 Ezpt Ifred607Noch keine Bewertungen

- Phps AYL3 ADokument5 SeitenPhps AYL3 Afred607Noch keine Bewertungen

- PHPHZ A9 FWDokument5 SeitenPHPHZ A9 FWfred607Noch keine Bewertungen

- PHPH G0 QWPDokument5 SeitenPHPH G0 QWPfred607Noch keine Bewertungen

- PHPZ FB L6 WDokument5 SeitenPHPZ FB L6 Wfred607Noch keine Bewertungen

- PHP LMs Ea LDokument5 SeitenPHP LMs Ea Lfred607Noch keine Bewertungen

- PHP OSc 83 HDokument5 SeitenPHP OSc 83 Hfred607Noch keine Bewertungen

- PHP OJucjfDokument5 SeitenPHP OJucjffred607Noch keine Bewertungen

- PHPV 7 o 6 IfDokument8 SeitenPHPV 7 o 6 Iffred607Noch keine Bewertungen

- PHP Yu NC 3 HDokument5 SeitenPHP Yu NC 3 Hfred607Noch keine Bewertungen

- PHP Ilt KW KDokument5 SeitenPHP Ilt KW Kfred607Noch keine Bewertungen

- PHP 4 e JCIuDokument5 SeitenPHP 4 e JCIufred607Noch keine Bewertungen

- PHP BCBCXVDokument5 SeitenPHP BCBCXVfred607Noch keine Bewertungen

- Phpiei KS0Dokument5 SeitenPhpiei KS0fred607Noch keine Bewertungen

- PHP AAj PVXDokument5 SeitenPHP AAj PVXfred607Noch keine Bewertungen

- PHPWJK GTDDokument5 SeitenPHPWJK GTDfred607Noch keine Bewertungen

- PHPWH DGR 3Dokument5 SeitenPHPWH DGR 3fred607Noch keine Bewertungen

- PHP C8 EVP2Dokument8 SeitenPHP C8 EVP2fred607Noch keine Bewertungen

- PHPQP WRZPDokument6 SeitenPHPQP WRZPfred607Noch keine Bewertungen

- Phpatypm DDokument5 SeitenPhpatypm Dfred607Noch keine Bewertungen

- PHP Zo IpfzDokument5 SeitenPHP Zo Ipfzfred607Noch keine Bewertungen

- The Last of The Mohicans: ECONOMIC DATA With ImpactDokument5 SeitenThe Last of The Mohicans: ECONOMIC DATA With Impactfred607Noch keine Bewertungen

- Phpcu 2 NCKDokument6 SeitenPhpcu 2 NCKfred607Noch keine Bewertungen

- PHP 7 Ab 1 EiDokument5 SeitenPHP 7 Ab 1 Eifred607Noch keine Bewertungen

- PHP TRYe 1 PDokument5 SeitenPHP TRYe 1 Pfred607Noch keine Bewertungen

- Phppa WP DKDokument6 SeitenPhppa WP DKfred607Noch keine Bewertungen

- Phpe 9 K OTYDokument5 SeitenPhpe 9 K OTYfred607Noch keine Bewertungen

- Phpo 1 NXAuDokument5 SeitenPhpo 1 NXAufred607Noch keine Bewertungen

- PHP 43 L TMIDokument5 SeitenPHP 43 L TMIfred607Noch keine Bewertungen

- PHPSP Q1 UtDokument5 SeitenPHPSP Q1 Utfred607Noch keine Bewertungen

- PHPTVM Ms 6Dokument5 SeitenPHPTVM Ms 6fred607Noch keine Bewertungen

- PHP WKPF BKDokument5 SeitenPHP WKPF BKfred607Noch keine Bewertungen

- PHPG KWZAYDokument5 SeitenPHPG KWZAYfred607Noch keine Bewertungen

- He After: ECONOMIC DATA With ImpactDokument5 SeitenHe After: ECONOMIC DATA With Impactfred607Noch keine Bewertungen

- PHP 1 RQi UgDokument5 SeitenPHP 1 RQi Ugfred607Noch keine Bewertungen

- PHPW J2 FKQDokument5 SeitenPHPW J2 FKQfred607Noch keine Bewertungen

- PHP 8 PB BSCDokument6 SeitenPHP 8 PB BSCfred607Noch keine Bewertungen

- Phpi P57 RsDokument5 SeitenPhpi P57 Rsfred607Noch keine Bewertungen

- PHP EQmt YvDokument6 SeitenPHP EQmt Yvfred607Noch keine Bewertungen

- Strategy Radar - 2012 - 0601 XX An Australian MomentDokument4 SeitenStrategy Radar - 2012 - 0601 XX An Australian MomentStrategicInnovationNoch keine Bewertungen

- Clock Ticking: ECONOMIC DATA With ImpactDokument5 SeitenClock Ticking: ECONOMIC DATA With Impactfred607Noch keine Bewertungen

- PHP ASYP25Dokument6 SeitenPHP ASYP25fred607Noch keine Bewertungen

- PHP HRty 8 RDokument5 SeitenPHP HRty 8 Rfred607Noch keine Bewertungen

- Phpatypm DDokument5 SeitenPhpatypm Dfred607Noch keine Bewertungen

- Phpdfasf KDokument5 SeitenPhpdfasf Kfred607Noch keine Bewertungen

- PHPSP Q1 UtDokument5 SeitenPHPSP Q1 Utfred607Noch keine Bewertungen

- PHP XgsukaDokument5 SeitenPHP Xgsukafred607Noch keine Bewertungen

- PHP 38 IZ1 NDokument5 SeitenPHP 38 IZ1 Nfred607Noch keine Bewertungen

- PHP OSc 83 HDokument5 SeitenPHP OSc 83 Hfred607Noch keine Bewertungen

- He After: ECONOMIC DATA With ImpactDokument5 SeitenHe After: ECONOMIC DATA With Impactfred607Noch keine Bewertungen

- PHP 1 B IWi DDokument5 SeitenPHP 1 B IWi Dfred607Noch keine Bewertungen

- Ormalization: ECONOMIC DATA With Impact Positive ImpactsDokument5 SeitenOrmalization: ECONOMIC DATA With Impact Positive Impactsfred607Noch keine Bewertungen

- PHP J0 S DQWDokument5 SeitenPHP J0 S DQWfred607Noch keine Bewertungen

- PHP TRYe 1 PDokument5 SeitenPHP TRYe 1 Pfred607Noch keine Bewertungen

- Phpi P57 RsDokument5 SeitenPhpi P57 Rsfred607Noch keine Bewertungen

- PHPP 2 KBC LDokument5 SeitenPHPP 2 KBC Lfred607Noch keine Bewertungen

- Phpga WVFRDokument4 SeitenPhpga WVFRfred607Noch keine Bewertungen

- PHP MDF SBZDokument5 SeitenPHP MDF SBZfred607Noch keine Bewertungen

- PHP MPPD ObDokument5 SeitenPHP MPPD Obfred607Noch keine Bewertungen

- Phps AYL3 ADokument5 SeitenPhps AYL3 Afred607Noch keine Bewertungen

- Phpo 1 NXAuDokument5 SeitenPhpo 1 NXAufred607Noch keine Bewertungen

- PHP NGK 0 BCDokument5 SeitenPHP NGK 0 BCfred607Noch keine Bewertungen

- PHP KXTT WRDokument5 SeitenPHP KXTT WRfred607Noch keine Bewertungen

- ECONOMIC DATA With ImpactDokument5 SeitenECONOMIC DATA With Impactfred607Noch keine Bewertungen

- PHP AAj PVXDokument5 SeitenPHP AAj PVXfred607Noch keine Bewertungen

- PHP H8 TV OTDokument5 SeitenPHP H8 TV OTfred607Noch keine Bewertungen

- PHP 1 RQi UgDokument5 SeitenPHP 1 RQi Ugfred607Noch keine Bewertungen

- PHP WKy VgeDokument5 SeitenPHP WKy Vgefred607Noch keine Bewertungen

- PHPQP WRZPDokument6 SeitenPHPQP WRZPfred607Noch keine Bewertungen

- PHPWH DGR 3Dokument5 SeitenPHPWH DGR 3fred607Noch keine Bewertungen

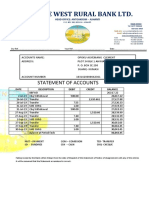

- Statement of Accounts AmansieDokument1 SeiteStatement of Accounts AmansieAgyei MichimelandNoch keine Bewertungen

- Welcome Letter PDFDokument3 SeitenWelcome Letter PDFKRISHNA DAS0% (1)

- Solved When A College Student Complained About A Particular Course TheDokument1 SeiteSolved When A College Student Complained About A Particular Course TheAnbu jaromiaNoch keine Bewertungen

- SKSE Securities LimitedDokument2 SeitenSKSE Securities LimitedsunitdaveNoch keine Bewertungen

- Important Question & AnswersDokument5 SeitenImportant Question & AnswersKrishnaNoch keine Bewertungen

- Banking LectureDokument1 SeiteBanking LectureЕлена ФадееваNoch keine Bewertungen

- Adv2019 0032Dokument1 SeiteAdv2019 0032Ralf Emmanuel BuenoNoch keine Bewertungen

- Ritesh Kumar Nimish Bansal Ankur Mittal Shwetab KumarDokument14 SeitenRitesh Kumar Nimish Bansal Ankur Mittal Shwetab KumardhikejuNoch keine Bewertungen

- An Overview of Branches and Atms of Commercial Banks in IndiaDokument12 SeitenAn Overview of Branches and Atms of Commercial Banks in IndiaPARAMASIVAN CHELLIAHNoch keine Bewertungen

- Bank ReconciliationDokument5 SeitenBank ReconciliationAngel PadillaNoch keine Bewertungen

- Locked File UnlockedDokument6 SeitenLocked File Unlocked76xzv4kk5vNoch keine Bewertungen

- Unit 4 Written Assignment BUS 2203: Principles of Finance 1 University of The People Galin TodorovDokument5 SeitenUnit 4 Written Assignment BUS 2203: Principles of Finance 1 University of The People Galin TodorovMarcusNoch keine Bewertungen

- JPMCStatementDokument4 SeitenJPMCStatementJoe Whitelaw50% (2)

- Mountain Village ClinicDokument21 SeitenMountain Village Clinicapi-490410600100% (1)

- Forex Market PPT 1227282355822375 8Dokument71 SeitenForex Market PPT 1227282355822375 8Naveed RkhanNoch keine Bewertungen

- HDFC BankDokument82 SeitenHDFC BankNishant ParmarNoch keine Bewertungen

- Name: Mejia, Andrew Ben M. Section: BSIT 1 - 1, AADokument1 SeiteName: Mejia, Andrew Ben M. Section: BSIT 1 - 1, AAandrewbenmejia13Noch keine Bewertungen

- Week3 Homework3Dokument3 SeitenWeek3 Homework3merteraslan2003Noch keine Bewertungen

- Bingham University, Karu, Nasarawa State.: AnswersDokument6 SeitenBingham University, Karu, Nasarawa State.: AnswersOkpihwo Blessing EseogheneNoch keine Bewertungen

- Account StatementDokument4 SeitenAccount Statementvickey chandraNoch keine Bewertungen

- Debit/Credit Card Fellow/Member/IMM Application Fee Debit/Credit Card Fellow/Member/IMM Application FeeDokument1 SeiteDebit/Credit Card Fellow/Member/IMM Application Fee Debit/Credit Card Fellow/Member/IMM Application FeeChandar KumarNoch keine Bewertungen

- D3 Handout SMT 3 - Bhs Inggris Profesi 2Dokument70 SeitenD3 Handout SMT 3 - Bhs Inggris Profesi 2Asri PutriNoch keine Bewertungen

- BITS HD-2013 Print Challan Form .Dokument1 SeiteBITS HD-2013 Print Challan Form .Naveen Kumar SinhaNoch keine Bewertungen

- Axis Service Charges of Foreign ExchangeDokument9 SeitenAxis Service Charges of Foreign ExchangeHimesh ShahNoch keine Bewertungen

- Nego Reviewer FinalDokument159 SeitenNego Reviewer FinalI.G. Mingo MulaNoch keine Bewertungen

- Introduction To Bank Reconciliation Statement: ReconcileDokument2 SeitenIntroduction To Bank Reconciliation Statement: ReconcileJayesh RasalNoch keine Bewertungen

- Fa Q Son RestructuringDokument4 SeitenFa Q Son RestructuringSoma ShekharNoch keine Bewertungen

- BOP Credit Card Sales Training Tool Kit (7 Files Merged)Dokument115 SeitenBOP Credit Card Sales Training Tool Kit (7 Files Merged)Shivam KumarNoch keine Bewertungen

- FAR.2917 Bank-ReconciliationDokument4 SeitenFAR.2917 Bank-ReconciliationmarielleNoch keine Bewertungen

- JK Essentials Corp.: Request For ReimbursementDokument3 SeitenJK Essentials Corp.: Request For ReimbursementColleen LucarezaNoch keine Bewertungen

- Prisoners of Geography: Ten Maps That Explain Everything About the WorldVon EverandPrisoners of Geography: Ten Maps That Explain Everything About the WorldBewertung: 4.5 von 5 Sternen4.5/5 (1146)

- Reagan at Reykjavik: Forty-Eight Hours That Ended the Cold WarVon EverandReagan at Reykjavik: Forty-Eight Hours That Ended the Cold WarBewertung: 4 von 5 Sternen4/5 (4)

- How States Think: The Rationality of Foreign PolicyVon EverandHow States Think: The Rationality of Foreign PolicyBewertung: 5 von 5 Sternen5/5 (7)

- Son of Hamas: A Gripping Account of Terror, Betrayal, Political Intrigue, and Unthinkable ChoicesVon EverandSon of Hamas: A Gripping Account of Terror, Betrayal, Political Intrigue, and Unthinkable ChoicesBewertung: 4.5 von 5 Sternen4.5/5 (503)

- Age of Revolutions: Progress and Backlash from 1600 to the PresentVon EverandAge of Revolutions: Progress and Backlash from 1600 to the PresentBewertung: 4.5 von 5 Sternen4.5/5 (8)

- Four Battlegrounds: Power in the Age of Artificial IntelligenceVon EverandFour Battlegrounds: Power in the Age of Artificial IntelligenceBewertung: 5 von 5 Sternen5/5 (5)

- The Future of Geography: How the Competition in Space Will Change Our WorldVon EverandThe Future of Geography: How the Competition in Space Will Change Our WorldBewertung: 4 von 5 Sternen4/5 (6)

- How Everything Became War and the Military Became Everything: Tales from the PentagonVon EverandHow Everything Became War and the Military Became Everything: Tales from the PentagonBewertung: 4 von 5 Sternen4/5 (40)

- The Shadow War: Inside Russia's and China's Secret Operations to Defeat AmericaVon EverandThe Shadow War: Inside Russia's and China's Secret Operations to Defeat AmericaBewertung: 4.5 von 5 Sternen4.5/5 (12)

- The War Below: Lithium, Copper, and the Global Battle to Power Our LivesVon EverandThe War Below: Lithium, Copper, and the Global Battle to Power Our LivesBewertung: 4.5 von 5 Sternen4.5/5 (8)

- Chip War: The Quest to Dominate the World's Most Critical TechnologyVon EverandChip War: The Quest to Dominate the World's Most Critical TechnologyBewertung: 4.5 von 5 Sternen4.5/5 (229)

- New Cold Wars: China’s rise, Russia’s invasion, and America’s struggle to defend the WestVon EverandNew Cold Wars: China’s rise, Russia’s invasion, and America’s struggle to defend the WestNoch keine Bewertungen

- The Tragic Mind: Fear, Fate, and the Burden of PowerVon EverandThe Tragic Mind: Fear, Fate, and the Burden of PowerBewertung: 4 von 5 Sternen4/5 (14)

- The Power of Geography: Ten Maps that Reveal the Future of Our WorldVon EverandThe Power of Geography: Ten Maps that Reveal the Future of Our WorldBewertung: 4.5 von 5 Sternen4.5/5 (54)

- Palestine Peace Not Apartheid: Peace Not ApartheidVon EverandPalestine Peace Not Apartheid: Peace Not ApartheidBewertung: 4 von 5 Sternen4/5 (197)

- The Generals Have No Clothes: The Untold Story of Our Endless WarsVon EverandThe Generals Have No Clothes: The Untold Story of Our Endless WarsBewertung: 3.5 von 5 Sternen3.5/5 (3)

- Unholy Alliance: The Agenda Iran, Russia, and Jihadists Share for Conquering the WorldVon EverandUnholy Alliance: The Agenda Iran, Russia, and Jihadists Share for Conquering the WorldBewertung: 3 von 5 Sternen3/5 (16)

- A Life Removed: Hunting for Refuge in the Modern WorldVon EverandA Life Removed: Hunting for Refuge in the Modern WorldBewertung: 4.5 von 5 Sternen4.5/5 (10)

- Dancing in the Glory of Monsters: The Collapse of the Congo and the Great War of AfricaVon EverandDancing in the Glory of Monsters: The Collapse of the Congo and the Great War of AfricaBewertung: 4 von 5 Sternen4/5 (82)

- Overreach: The Inside Story of Putin’s War Against UkraineVon EverandOverreach: The Inside Story of Putin’s War Against UkraineBewertung: 4.5 von 5 Sternen4.5/5 (29)

- Except for Palestine: The Limits of Progressive PoliticsVon EverandExcept for Palestine: The Limits of Progressive PoliticsBewertung: 4.5 von 5 Sternen4.5/5 (52)

- Mossad: The Greatest Missions of the Israeli Secret ServiceVon EverandMossad: The Greatest Missions of the Israeli Secret ServiceBewertung: 4 von 5 Sternen4/5 (84)

- Never Give an Inch: Fighting for the America I LoveVon EverandNever Give an Inch: Fighting for the America I LoveBewertung: 4 von 5 Sternen4/5 (10)

- Freedom is a Constant Struggle: Ferguson, Palestine, and the Foundations of a MovementVon EverandFreedom is a Constant Struggle: Ferguson, Palestine, and the Foundations of a MovementBewertung: 4.5 von 5 Sternen4.5/5 (567)