Das könnte Ihnen auch gefallen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5782)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Garner Fructis ShampooDokument3 SeitenGarner Fructis Shampooyogesh0794Noch keine Bewertungen

- Apple Inc.: Managing Global Supply Chain: Case AnalysisDokument9 SeitenApple Inc.: Managing Global Supply Chain: Case AnalysisPrateek GuptaNoch keine Bewertungen

- Dead Can Dance - How Fortunate The Man With None LyricsDokument3 SeitenDead Can Dance - How Fortunate The Man With None LyricstheourgikonNoch keine Bewertungen

- Marylebone Construction UpdateDokument2 SeitenMarylebone Construction UpdatePedro SousaNoch keine Bewertungen

- Miriam Garcia Resume 2 1Dokument2 SeitenMiriam Garcia Resume 2 1api-548501562Noch keine Bewertungen

- CVA: Health Education PlanDokument4 SeitenCVA: Health Education Plandanluki100% (3)

- Bhojpuri PDFDokument15 SeitenBhojpuri PDFbestmadeeasy50% (2)

- Commissioning GuideDokument78 SeitenCommissioning GuideNabilBouabanaNoch keine Bewertungen

- 14 Worst Breakfast FoodsDokument31 Seiten14 Worst Breakfast Foodscora4eva5699100% (1)

- Shilajit The Panacea For CancerDokument48 SeitenShilajit The Panacea For Cancerliving63100% (1)

- Module 3 - Risk Based Inspection (RBI) Based On API and ASMEDokument4 SeitenModule 3 - Risk Based Inspection (RBI) Based On API and ASMEAgustin A.Noch keine Bewertungen

- E2415 PDFDokument4 SeitenE2415 PDFdannychacon27Noch keine Bewertungen

- Introduction to Networks Visual GuideDokument1 SeiteIntroduction to Networks Visual GuideWorldNoch keine Bewertungen

- Httpswww.ceec.Edu.twfilesfile Pool10j07580923432342090202 97指考英文試卷 PDFDokument8 SeitenHttpswww.ceec.Edu.twfilesfile Pool10j07580923432342090202 97指考英文試卷 PDFAurora ZengNoch keine Bewertungen

- Sale of GoodsDokument41 SeitenSale of GoodsKellyNoch keine Bewertungen

- Mental Health Admission & Discharge Dip NursingDokument7 SeitenMental Health Admission & Discharge Dip NursingMuranatu CynthiaNoch keine Bewertungen

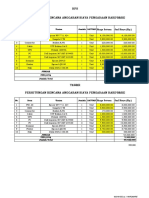

- HPS Perhitungan Rencana Anggaran Biaya Pengadaan Hardware: No. Item Uraian Jumlah SATUANDokument2 SeitenHPS Perhitungan Rencana Anggaran Biaya Pengadaan Hardware: No. Item Uraian Jumlah SATUANYanto AstriNoch keine Bewertungen

- GeM Bidding 2920423 - 2Dokument4 SeitenGeM Bidding 2920423 - 2Sulvine CharlieNoch keine Bewertungen

- Curriculum Vitae (October 31, 2011)Dokument5 SeitenCurriculum Vitae (October 31, 2011)Alvin Ringgo C. Reyes100% (1)

- Mitanoor Sultana: Career ObjectiveDokument2 SeitenMitanoor Sultana: Career ObjectiveDebasish DasNoch keine Bewertungen

- Infinitive Clauses PDFDokument3 SeitenInfinitive Clauses PDFKatia LeliakhNoch keine Bewertungen

- (Section-A / Aip) : Delhi Public School GandhinagarDokument2 Seiten(Section-A / Aip) : Delhi Public School GandhinagarVvs SadanNoch keine Bewertungen

- Temperature Rise HV MotorDokument11 SeitenTemperature Rise HV Motorashwani2101Noch keine Bewertungen

- Is The Question Too Broad or Too Narrow?Dokument3 SeitenIs The Question Too Broad or Too Narrow?teo100% (1)

- The RF Line: Semiconductor Technical DataDokument4 SeitenThe RF Line: Semiconductor Technical DataJuan David Manrique GuerraNoch keine Bewertungen

- JDDokument19 SeitenJDJuan Carlo CastanedaNoch keine Bewertungen

- Perilaku Ramah Lingkungan Peserta Didik Sma Di Kota BandungDokument11 SeitenPerilaku Ramah Lingkungan Peserta Didik Sma Di Kota Bandungnurulhafizhah01Noch keine Bewertungen

- Minsc and Boo's Journal of VillainyDokument158 SeitenMinsc and Boo's Journal of VillainyAPCommentator100% (1)

- Soap - WikipediaDokument57 SeitenSoap - Wikipediayash BansalNoch keine Bewertungen

- iPhone Repair FormDokument1 SeiteiPhone Repair Formkabainc0% (1)