Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Freefincal - Prudent DIY Investing!Dokument11 SeitenFreefincal - Prudent DIY Investing!Ta WexNoch keine Bewertungen

- Market Segmentation of NokiaDokument93 SeitenMarket Segmentation of Nokiapriyanka9086% (22)

- CPAR - Auditing ProblemDokument12 SeitenCPAR - Auditing ProblemAlbert Macapagal83% (6)

- Long-Run Incremental Cost Pricing For Negative Growth RateDokument21 SeitenLong-Run Incremental Cost Pricing For Negative Growth RateDevendra SharmaNoch keine Bewertungen

- PresentationDokument15 SeitenPresentationapi-241493839Noch keine Bewertungen

- 2019 - Turner & Townsend - 547236 - Turnertownsend-Icms-2019 PDFDokument120 Seiten2019 - Turner & Townsend - 547236 - Turnertownsend-Icms-2019 PDFYi Jie100% (1)

- Michael Guichon Sohn Conference PresentationDokument49 SeitenMichael Guichon Sohn Conference PresentationValueWalkNoch keine Bewertungen

- Market Basket Analysis NewDokument21 SeitenMarket Basket Analysis NewAbhishek JhaveriNoch keine Bewertungen

- ForfeitingDokument7 SeitenForfeitingvandana_daki3941Noch keine Bewertungen

- Factoring and ForfaitingDokument34 SeitenFactoring and ForfaitingAbhishek JhaveriNoch keine Bewertungen

- Tata Steel QuestionDokument1 SeiteTata Steel QuestionAbhishek JhaveriNoch keine Bewertungen

- Various Savings Instruments Issued by NBFCDokument2 SeitenVarious Savings Instruments Issued by NBFCAbhishek JhaveriNoch keine Bewertungen

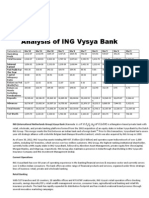

- Analysis of ING Vysya BankDokument2 SeitenAnalysis of ING Vysya BankAbhishek JhaveriNoch keine Bewertungen

- Nakamura Lacquer CompanyDokument12 SeitenNakamura Lacquer CompanyAbhishek Jhaveri50% (2)

- Brokers LocationDokument3 SeitenBrokers LocationAbhishek JhaveriNoch keine Bewertungen

- Legal PartDokument23 SeitenLegal PartAbhishek JhaveriNoch keine Bewertungen

- Utkarsh Sahai, Sec-A, Roll No.-13189: Orders of The DayDokument2 SeitenUtkarsh Sahai, Sec-A, Roll No.-13189: Orders of The DayAbhishek JhaveriNoch keine Bewertungen

- Strategic Management State Bank of IndiaDokument12 SeitenStrategic Management State Bank of IndiaAbhishek JhaveriNoch keine Bewertungen

- Chapter 1 Question AnswersDokument5 SeitenChapter 1 Question AnswersRoshan JaiswalNoch keine Bewertungen

- F7 - LSBF Revision - Kit PDFDokument168 SeitenF7 - LSBF Revision - Kit PDFanon_635916830% (1)

- Return, Risk, and The Security Market LineDokument48 SeitenReturn, Risk, and The Security Market LinehbuzdarNoch keine Bewertungen

- Module 1 Partnerships Basic Considerations and OrganizationsDokument48 SeitenModule 1 Partnerships Basic Considerations and Organizationscha11Noch keine Bewertungen

- Bank and NBFC Mehal PDFDokument38 SeitenBank and NBFC Mehal PDFPrasun AgarwalNoch keine Bewertungen

- Foreign Exchange and Risk ManagementDokument38 SeitenForeign Exchange and Risk ManagementRuta Vyas100% (1)

- Lecture SixDokument10 SeitenLecture SixSaviusNoch keine Bewertungen

- HDFC - LIC Right MARKETING STRATEGIESDokument56 SeitenHDFC - LIC Right MARKETING STRATEGIESMANISHA GAUTAMNoch keine Bewertungen

- Homework Week 4 TVMDokument9 SeitenHomework Week 4 TVMJon FruitNoch keine Bewertungen

- Jawaban Debt Investments (Mindmap, E17-1 p17-1)Dokument2 SeitenJawaban Debt Investments (Mindmap, E17-1 p17-1)Rahmat DarmawanNoch keine Bewertungen

- Happy Tour and Travel PART2-1Dokument11 SeitenHappy Tour and Travel PART2-1Katelyn Sillano100% (2)

- HW 5 SolutionDokument2 SeitenHW 5 SolutionChrissy DrakeNoch keine Bewertungen

- Exam Docs Dipifr 2010Dokument1 SeiteExam Docs Dipifr 2010cabamaroNoch keine Bewertungen

- John CV PDFDokument8 SeitenJohn CV PDFrwomubitooke johnNoch keine Bewertungen

- TwelveBiggestMistakes EstatePlanning PDFDokument37 SeitenTwelveBiggestMistakes EstatePlanning PDFDanno N100% (1)

- Accounting ConceptDokument17 SeitenAccounting ConceptSujith KarayilNoch keine Bewertungen

- Chapter Thirteen The Value of Operations and The Evaluation of Enterprise Price-to-Book Ratios and Price-Earnings RatiosDokument36 SeitenChapter Thirteen The Value of Operations and The Evaluation of Enterprise Price-to-Book Ratios and Price-Earnings RatiosceojiNoch keine Bewertungen

- DividendDokument5 SeitenDividendAkash79Noch keine Bewertungen

- Chapter 10Dokument37 SeitenChapter 10carlo knowsNoch keine Bewertungen

- Business Plan Assignment 1Dokument8 SeitenBusiness Plan Assignment 1Hariharan VigneshNoch keine Bewertungen

- Chapter 12. Tool Kit For Capital Budgeting: Decision CriteriaDokument16 SeitenChapter 12. Tool Kit For Capital Budgeting: Decision CriteriaSamuel DebebeNoch keine Bewertungen

- IjarahDokument15 SeitenIjarahArsalan Khan100% (1)

- 2018 National Budget Quick Glance 1172018Dokument2 Seiten2018 National Budget Quick Glance 1172018Jhave AñonuevoNoch keine Bewertungen

- FRM PPT Risk Adjusted Rate of Return in CapitalDokument10 SeitenFRM PPT Risk Adjusted Rate of Return in CapitalRachna MarcusNoch keine Bewertungen