Das könnte Ihnen auch gefallen

- Lecture Notes - Tort Law - DuressDokument18 SeitenLecture Notes - Tort Law - DuressBbbbbbbbNoch keine Bewertungen

- Client Letter ExamplesDokument4 SeitenClient Letter ExamplesOh Oh OhNoch keine Bewertungen

- Tax Cheat Sheet Exam 2 - CH 7,8,10,11Dokument2 SeitenTax Cheat Sheet Exam 2 - CH 7,8,10,11tyg1992Noch keine Bewertungen

- OutlineDokument71 SeitenOutlineMaxwell NdunguNoch keine Bewertungen

- The Polks Tax CalculationDokument8 SeitenThe Polks Tax CalculationhuytrinhxNoch keine Bewertungen

- Written Comment Public Hearing Title IX DOE Athletics Sex Discrimination June 10 2021Dokument65 SeitenWritten Comment Public Hearing Title IX DOE Athletics Sex Discrimination June 10 2021OnPointRadioNoch keine Bewertungen

- 15gift and Estate Tax - Katzenstein - Fall 2002Dokument95 Seiten15gift and Estate Tax - Katzenstein - Fall 2002proveitwasmeNoch keine Bewertungen

- Takeover Defense in MinnesotaDokument48 SeitenTakeover Defense in MinnesotaSteve QuinlivanNoch keine Bewertungen

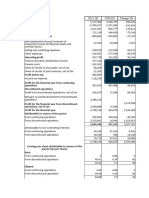

- Financial Statement AssignmentDokument16 SeitenFinancial Statement Assignmentapi-275910271Noch keine Bewertungen

- LGST 101 ProblemsDokument16 SeitenLGST 101 ProblemsKrishnan SethumadhavanNoch keine Bewertungen

- ComunicationDokument60 SeitenComunicationLya Hellen100% (3)

- Example of Tax Research LetterDokument3 SeitenExample of Tax Research LetterGrace Ann Aceveda QuinioNoch keine Bewertungen

- MemoDokument3 SeitenMemoAnonymous mO72yqNcNoch keine Bewertungen

- Study Unit 20Dokument13 SeitenStudy Unit 20Hazem El SayedNoch keine Bewertungen

- 15 Tax On S CorpDokument90 Seiten15 Tax On S CorpWahyudiNoch keine Bewertungen

- Partnership AllocationDokument63 SeitenPartnership AllocationMitchelGramaticaNoch keine Bewertungen

- Tax Research AssignmentDokument8 SeitenTax Research Assignmentanon_768972800100% (1)

- Taking Lawsuit by Vacation Rentals Vs Florida GovernorDokument39 SeitenTaking Lawsuit by Vacation Rentals Vs Florida GovernorAlex FotoNoch keine Bewertungen

- Income TaxDokument71 SeitenIncome TaxMahrukh MalikNoch keine Bewertungen

- Allen Feingold v. Liberty Mutual Group, 3rd Cir. (2014)Dokument7 SeitenAllen Feingold v. Liberty Mutual Group, 3rd Cir. (2014)Scribd Government DocsNoch keine Bewertungen

- Applied Food Sciences v. Monster BeverageDokument6 SeitenApplied Food Sciences v. Monster BeveragePriorSmartNoch keine Bewertungen

- 1347 Property Ins. v. Foley & Lardner (Complaint)Dokument8 Seiten1347 Property Ins. v. Foley & Lardner (Complaint)Ken VankoNoch keine Bewertungen

- Milliken V Pratt RealDokument8 SeitenMilliken V Pratt RealJulia Camille RealNoch keine Bewertungen

- Appellate Motion Brief (Writing Sample)Dokument15 SeitenAppellate Motion Brief (Writing Sample)shausoon100% (1)

- Notes On GST (Law of Taxation)Dokument15 SeitenNotes On GST (Law of Taxation)Bhoomika SinghNoch keine Bewertungen

- LA Slip and FallDokument5 SeitenLA Slip and FallMona DeldarNoch keine Bewertungen

- Memorandum: Allocation/ de Facto Monopoly Whereby Companies Agree To Steer Clear of EachDokument6 SeitenMemorandum: Allocation/ de Facto Monopoly Whereby Companies Agree To Steer Clear of EachKweeng Tayrus FaelnarNoch keine Bewertungen

- Fed Tax - Final OutlineDokument52 SeitenFed Tax - Final OutlineMike Binka KusiNoch keine Bewertungen

- Lawsuit Against GeicoDokument9 SeitenLawsuit Against GeicoLaw&CrimeNoch keine Bewertungen

- US Taxation - Outline: I. Types of Tax Rate StructuresDokument12 SeitenUS Taxation - Outline: I. Types of Tax Rate Structuresvarghese2007Noch keine Bewertungen

- Supreme Court of Florida 09-441Dokument32 SeitenSupreme Court of Florida 09-441asdfNoch keine Bewertungen

- Judge To Consider Competing PG&E Bankruptcy ProposalDokument4 SeitenJudge To Consider Competing PG&E Bankruptcy ProposaldanxmcgrawNoch keine Bewertungen

- New York Court SystemDokument1 SeiteNew York Court SystemKeith Vick100% (4)

- Connecticut W-4 Form Explains Codes For Withholding RatesDokument4 SeitenConnecticut W-4 Form Explains Codes For Withholding RatesestannardNoch keine Bewertungen

- Civ Pro OutlineDokument48 SeitenCiv Pro OutlineTR1912Noch keine Bewertungen

- Int TaxDokument24 SeitenInt TaxDane4545Noch keine Bewertungen

- Compensation For Breach of Employment ContractDokument31 SeitenCompensation For Breach of Employment ContractIbnu HassanNoch keine Bewertungen

- Memo in Support of Summary JudgmentDokument15 SeitenMemo in Support of Summary JudgmentAnthony WarrenNoch keine Bewertungen

- Bar Sanctions Jun 2020Dokument34 SeitenBar Sanctions Jun 2020the kingfishNoch keine Bewertungen

- Above The Line DeductionsDokument26 SeitenAbove The Line DeductionsZak KurtzNoch keine Bewertungen

- Revised Statutes of The United States June 22 1874 December 1 1873Dokument49 SeitenRevised Statutes of The United States June 22 1874 December 1 1873Matthew DanseyNoch keine Bewertungen

- EO OutlineDokument75 SeitenEO OutlineNicolas RiegerNoch keine Bewertungen

- Sergey Aleynikov Fees Memorandum of LawDokument39 SeitenSergey Aleynikov Fees Memorandum of LawDealBookNoch keine Bewertungen

- 2012 Consumer Protection Section Annual ReportDokument28 Seiten2012 Consumer Protection Section Annual ReportMike DeWineNoch keine Bewertungen

- Fall 2018 Contracts: Cases+ProblemsDokument5 SeitenFall 2018 Contracts: Cases+ProblemsFernanda Rodriguez TorresNoch keine Bewertungen

- Tax of Business Entities Chapter 4Dokument38 SeitenTax of Business Entities Chapter 4craig52292Noch keine Bewertungen

- United States Court of Appeals, Second Circuit.: No. 1116, Docket 81-6231Dokument13 SeitenUnited States Court of Appeals, Second Circuit.: No. 1116, Docket 81-6231Scribd Government DocsNoch keine Bewertungen

- Tax HW 1Dokument3 SeitenTax HW 1lexyramdeoNoch keine Bewertungen

- 2014 House Bill 585 (Requested Revisions)Dokument5 Seiten2014 House Bill 585 (Requested Revisions)the kingfishNoch keine Bewertungen

- Deductions From Gross IncomeDokument2 SeitenDeductions From Gross Incomericamae saladagaNoch keine Bewertungen

- Tax Framework PlanDokument9 SeitenTax Framework PlanCNBC.com100% (1)

- Amache ComplaintDokument3 SeitenAmache Complaintapi-341957708Noch keine Bewertungen

- IRS Publication 15 Withholding Tax Tables 2010Dokument73 SeitenIRS Publication 15 Withholding Tax Tables 2010Wayne Schulz100% (1)

- Hedge Funds and Private Equity - A Critical AnalysisDokument21 SeitenHedge Funds and Private Equity - A Critical AnalysisGeorge SatlasNoch keine Bewertungen

- Constitutional Law - Due Process - Double TaxationDokument3 SeitenConstitutional Law - Due Process - Double TaxationWilly WonkaNoch keine Bewertungen

- Civ Pro 1 OutlineDokument35 SeitenCiv Pro 1 OutlineSavana DegroatNoch keine Bewertungen

- Contract (Obyrne Sem 2)Dokument41 SeitenContract (Obyrne Sem 2)JjjjmmmmNoch keine Bewertungen

- Kia Investor PresentationDokument1 SeiteKia Investor PresentationABC Action NewsNoch keine Bewertungen

- Review Questions: Chapter 04 - Legal Liability of CpasDokument14 SeitenReview Questions: Chapter 04 - Legal Liability of CpasJima KromahNoch keine Bewertungen

- Florida Real Estate Exam Prep: Everything You Need to Know to PassVon EverandFlorida Real Estate Exam Prep: Everything You Need to Know to PassNoch keine Bewertungen

- BusinessDokument9 SeitenBusinessLya HellenNoch keine Bewertungen

- BusinessDokument9 SeitenBusinessLya HellenNoch keine Bewertungen

- EconomicDokument8 SeitenEconomicLya HellenNoch keine Bewertungen

- Global TrendsDokument7 SeitenGlobal TrendsLya HellenNoch keine Bewertungen

- BusinessDokument10 SeitenBusinessLya HellenNoch keine Bewertungen

- HRDokument6 SeitenHRLya HellenNoch keine Bewertungen

- Tehnica STAR de Susţinere A UnuiDokument8 SeitenTehnica STAR de Susţinere A UnuiLya HellenNoch keine Bewertungen

- Presentation 1Dokument1 SeitePresentation 1Lya HellenNoch keine Bewertungen

- BusinessDokument9 SeitenBusinessLya HellenNoch keine Bewertungen

- Try ItDokument1 SeiteTry ItLya HellenNoch keine Bewertungen

- GLOIncoterms IDokument2 SeitenGLOIncoterms IWarren SappNoch keine Bewertungen

- Scholarship ContractDokument2 SeitenScholarship ContractLya HellenNoch keine Bewertungen

- Busuness RoleDokument5 SeitenBusuness RoleLya HellenNoch keine Bewertungen

- Necessary Formalities: Before LeavingDokument2 SeitenNecessary Formalities: Before LeavingLya HellenNoch keine Bewertungen

- Img 20130119 0004Dokument1 SeiteImg 20130119 0004Lya HellenNoch keine Bewertungen

- Casa Doina Dinner 16 NovemberDokument1 SeiteCasa Doina Dinner 16 NovemberLya HellenNoch keine Bewertungen

- Sdxckfjikofgheir FGMFTDRNHGKJRHT Efdrbgjfgh SkldbnhbfuiDokument1 SeiteSdxckfjikofgheir FGMFTDRNHGKJRHT Efdrbgjfgh SkldbnhbfuiLya HellenNoch keine Bewertungen

- IslamismDokument2 SeitenIslamismLya HellenNoch keine Bewertungen

- Business Ethics and EtiquetteDokument15 SeitenBusiness Ethics and EtiquetteLya Hellen100% (1)

- Business Ethics Get CodifiedDokument12 SeitenBusiness Ethics Get CodifiedLya HellenNoch keine Bewertungen

- Letter of ComplaintDokument2 SeitenLetter of ComplaintLya HellenNoch keine Bewertungen

- Of Total ExportsDokument1 SeiteOf Total ExportsLya HellenNoch keine Bewertungen

- London Bussines SchoolDokument1 SeiteLondon Bussines SchoolLya HellenNoch keine Bewertungen

- Non Verbal CommunicationDokument62 SeitenNon Verbal CommunicationLya HellenNoch keine Bewertungen

- Alum Adc SwotAnalysis WikipediaDokument5 SeitenAlum Adc SwotAnalysis WikipediaLya HellenNoch keine Bewertungen

- 2012 Application Annex - 1Dokument1 Seite2012 Application Annex - 1lulay1974Noch keine Bewertungen

- The Terminology of ContractsDokument12 SeitenThe Terminology of ContractsLya HellenNoch keine Bewertungen

- How Civilizations DieDokument6 SeitenHow Civilizations DieLya Hellen0% (1)

- Rutansh Final Itr 2022-23 - 2Dokument1 SeiteRutansh Final Itr 2022-23 - 2Rutansh JagtapNoch keine Bewertungen

- Tax Invoice: Adinath Furniture Mall TI/GST21-22/1281 14-Aug-21 Card Swipe SMSDokument3 SeitenTax Invoice: Adinath Furniture Mall TI/GST21-22/1281 14-Aug-21 Card Swipe SMSKrishna ManchiNoch keine Bewertungen

- PDFDokument1 SeitePDFThei WhouhNoch keine Bewertungen

- CE Luzon v. CIRDokument2 SeitenCE Luzon v. CIRSab Amantillo Borromeo100% (1)

- Part B PDFDokument3 SeitenPart B PDFDebesh KuanrNoch keine Bewertungen

- Double Taxation ReliefDokument10 SeitenDouble Taxation ReliefJeeva Antony VictoriaNoch keine Bewertungen

- Karla Company Comprehensive IncomeDokument3 SeitenKarla Company Comprehensive Incomeakiko dilemNoch keine Bewertungen

- Solved Business K Exchanged Old Machinery FMV 95 000 For New Machinery PDFDokument1 SeiteSolved Business K Exchanged Old Machinery FMV 95 000 For New Machinery PDFAnbu jaromiaNoch keine Bewertungen

- And Inclusion Law) Revenue Regulations 13-2018Dokument2 SeitenAnd Inclusion Law) Revenue Regulations 13-2018Rnemcdg100% (1)

- Amar EnterprisesDokument2 SeitenAmar EnterprisesAmit DhochakNoch keine Bewertungen

- TAX102: Transfer and Business Taxation: Optional RegistrationDokument3 SeitenTAX102: Transfer and Business Taxation: Optional Registrationaccounts 3 lifeNoch keine Bewertungen

- 519061116100361201Dokument1 Seite519061116100361201Trilok GolchhaNoch keine Bewertungen

- IFSA Income StatementDokument2 SeitenIFSA Income StatementYaesnavy ParamesvaranNoch keine Bewertungen

- Business Taxation QuizDokument5 SeitenBusiness Taxation QuizWerpa PetmaluNoch keine Bewertungen

- Sin TítuloDokument14 SeitenSin TítuloTavo MCNoch keine Bewertungen

- Income Tax Rates For FY 2023-24 (AY 2024-25)Dokument13 SeitenIncome Tax Rates For FY 2023-24 (AY 2024-25)ghs niduvani niduvaniNoch keine Bewertungen

- RMC No. 34-2022 - New Version of 2316Dokument1 SeiteRMC No. 34-2022 - New Version of 2316Vence EugalcaNoch keine Bewertungen

- Itr Fy 22-23Dokument6 SeitenItr Fy 22-23Omkar kaleNoch keine Bewertungen

- E-Way BillDokument1 SeiteE-Way BillPEDAPUDI SIVANoch keine Bewertungen

- Chapter 14 IllustrationsDokument8 SeitenChapter 14 IllustrationsE.D.JNoch keine Bewertungen

- Pension FormsDokument5 SeitenPension FormsGunnie PandherNoch keine Bewertungen

- Form No. 16 (See Rule 31 (1) (A) ) : Certificate Under Section 203 of The Income-Tax Act, 1961 For Tax Deducted at SourceDokument4 SeitenForm No. 16 (See Rule 31 (1) (A) ) : Certificate Under Section 203 of The Income-Tax Act, 1961 For Tax Deducted at SourceJeevabinding xeroxNoch keine Bewertungen

- Dec22 - Compliance CalendarDokument4 SeitenDec22 - Compliance CalendarArman KhanNoch keine Bewertungen

- KtomDokument1 SeiteKtomJimmy Macharia100% (1)

- Do 4Dokument1 SeiteDo 4Niyati MakwanaNoch keine Bewertungen

- Sunil MewadaDokument1 SeiteSunil MewadaSteve BurnsNoch keine Bewertungen

- Mepco Online Billl PDFDokument1 SeiteMepco Online Billl PDFArslanNoch keine Bewertungen

- Accounting Voucher 1Dokument1 SeiteAccounting Voucher 1Sadiq SultanNoch keine Bewertungen

- Answers - Business Taxation - Gross Estate (Chapter 13)Dokument2 SeitenAnswers - Business Taxation - Gross Estate (Chapter 13)Gino Cajolo100% (1)