Das könnte Ihnen auch gefallen

- Administrative Office ManagementDokument44 SeitenAdministrative Office ManagementLea VenturozoNoch keine Bewertungen

- REVIEWERDokument9 SeitenREVIEWERHanns Lexter PadillaNoch keine Bewertungen

- Essay 1 - Non-Financial InformationDokument3 SeitenEssay 1 - Non-Financial InformationSeiniNoch keine Bewertungen

- Assignment Prep Airing Journal Entries and Trail BalancesDokument13 SeitenAssignment Prep Airing Journal Entries and Trail BalancesChristine NorthrupNoch keine Bewertungen

- ACCOUNTING123Dokument5 SeitenACCOUNTING123April Vinas SabusapNoch keine Bewertungen

- FABM Assignment WS FS P C TB 1Dokument34 SeitenFABM Assignment WS FS P C TB 1memae0044Noch keine Bewertungen

- Acctng 1 pt1 NmarasignaDokument3 SeitenAcctng 1 pt1 NmarasignaMarielle Red AlmarioNoch keine Bewertungen

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionVon EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNoch keine Bewertungen

- ACCAF5 - Qbank2017 - by First Intuition Downloaded FromDokument384 SeitenACCAF5 - Qbank2017 - by First Intuition Downloaded FromAbdul Jabbar Al-Shaer100% (4)

- Accounting ExercisesDokument41 SeitenAccounting ExercisesKayla MirandaNoch keine Bewertungen

- Answer Prob 1 and 2Dokument3 SeitenAnswer Prob 1 and 2machelle franciscoNoch keine Bewertungen

- What Is AccountingDokument76 SeitenWhat Is AccountingMa Jemaris Solis0% (1)

- ABM 002 Teacher Day 17Dokument9 SeitenABM 002 Teacher Day 17Darelle Hannah MarquezNoch keine Bewertungen

- LASALA Partnership Formation SWDokument2 SeitenLASALA Partnership Formation SWLizzeille Anne Amor MacalintalNoch keine Bewertungen

- Assignment02 PDFDokument2 SeitenAssignment02 PDFAilene MendozaNoch keine Bewertungen

- Ast-Chapter 1 p3, p5, p6Dokument8 SeitenAst-Chapter 1 p3, p5, p6Geminah BellenNoch keine Bewertungen

- Ch28 Test Bank 4-5-10Dokument14 SeitenCh28 Test Bank 4-5-10KarenNoch keine Bewertungen

- Act 701 Assignment 2Dokument3 SeitenAct 701 Assignment 2Nahid HawkNoch keine Bewertungen

- Financial Accounting and Reporting: Exercise 1Dokument8 SeitenFinancial Accounting and Reporting: Exercise 1Lenneth Mones0% (1)

- The Need For AdjustmentDokument5 SeitenThe Need For AdjustmentAnna CharlotteNoch keine Bewertungen

- Acc 223a CH 5 AnswersDokument13 SeitenAcc 223a CH 5 Answersjr centenoNoch keine Bewertungen

- Comprehensive ProblemDokument1 SeiteComprehensive ProblemDavid Con RiveroNoch keine Bewertungen

- RR Diaz 1CED - CW Local and GlobalDokument2 SeitenRR Diaz 1CED - CW Local and GlobalJr DiazNoch keine Bewertungen

- FOA - 3rd Summative AssessmentDokument1 SeiteFOA - 3rd Summative AssessmentJohniel MartinNoch keine Bewertungen

- Effects of Transactions Instructions: Indicate The Effects of Each Transaction by Writing The ChoicesDokument1 SeiteEffects of Transactions Instructions: Indicate The Effects of Each Transaction by Writing The ChoicesHessiel Mae Jumalon Garcines100% (1)

- Solution Booklet 2 Installment LTCC, FranchiseDokument7 SeitenSolution Booklet 2 Installment LTCC, Franchisemarcus yapNoch keine Bewertungen

- C. Identification, Recording, Communication.: ExceptDokument9 SeitenC. Identification, Recording, Communication.: ExceptSylvia Al-a'maNoch keine Bewertungen

- Module 2 - The Accounting Equation and The Double-Entry SystemDokument41 SeitenModule 2 - The Accounting Equation and The Double-Entry SystemJenny Paculaba100% (1)

- Pure ProblemsDokument7 SeitenPure Problemschristine anglaNoch keine Bewertungen

- Ocean Atlantic Co Is A Merchandising Business The Account BalaDokument2 SeitenOcean Atlantic Co Is A Merchandising Business The Account BalaM Bilal SaleemNoch keine Bewertungen

- NSTP 2 Stewardship StewardshipDokument18 SeitenNSTP 2 Stewardship StewardshipLieeeNoch keine Bewertungen

- Lesson 10 Assignment 4Dokument4 SeitenLesson 10 Assignment 4marcied357Noch keine Bewertungen

- Chapter 10 AFAR 2 ProblemsDokument3 SeitenChapter 10 AFAR 2 ProblemsMa Alyssa DelmiguezNoch keine Bewertungen

- FinAcc Vol. 3 Chap3 ProblemsDokument26 SeitenFinAcc Vol. 3 Chap3 ProblemsGelynne Arceo33% (3)

- Exercises On Closing Entries & Reversing EntriesDokument3 SeitenExercises On Closing Entries & Reversing EntriesRoy BonitezNoch keine Bewertungen

- Chapter 5Dokument19 SeitenChapter 5Rochelle Esquivel ManaloNoch keine Bewertungen

- Pequit Company Chart of Accounts For The Year Ended December 31, 2019 Account No. Description Account TypeDokument41 SeitenPequit Company Chart of Accounts For The Year Ended December 31, 2019 Account No. Description Account TypePia Suril0% (1)

- Advanced Accounting BU 455A Spring 2013 Test OneDokument14 SeitenAdvanced Accounting BU 455A Spring 2013 Test OneMichael Tai Maimoni100% (2)

- A Study On The Market Growth of Penshopp PDFDokument18 SeitenA Study On The Market Growth of Penshopp PDFmaria rosalyn palconNoch keine Bewertungen

- Assets Liabilities and EquityDokument2 SeitenAssets Liabilities and EquityArian Amurao50% (2)

- PDF Club Medica Practice Set 2 1xlsxDokument74 SeitenPDF Club Medica Practice Set 2 1xlsxHerah SexyNoch keine Bewertungen

- To Record Raw Materials Purchased On AccountDokument4 SeitenTo Record Raw Materials Purchased On AccountKathleen MercadoNoch keine Bewertungen

- FM 1 Assignment 1Dokument3 SeitenFM 1 Assignment 1Jelly Ann AndresNoch keine Bewertungen

- Cost Classifications As To Product and BehaviourDokument2 SeitenCost Classifications As To Product and BehaviourJimbo ManalastasNoch keine Bewertungen

- 1n2 QuestionDokument3 Seiten1n2 QuestionJohn_Byron_Ign_270100% (1)

- AnswerDokument6 SeitenAnswerAinin Sofea FoziNoch keine Bewertungen

- Group B Teresita Buenaflor ShoesDokument38 SeitenGroup B Teresita Buenaflor ShoesAlexandrea San Buenaventura BaayNoch keine Bewertungen

- Quiz No. 7: A. MULTIPLE CHOICE: Write The Correct Letter Choice BeforeDokument6 SeitenQuiz No. 7: A. MULTIPLE CHOICE: Write The Correct Letter Choice BeforeJOHN MITCHELL GALLARDONoch keine Bewertungen

- Local Media8011400976913649007Dokument16 SeitenLocal Media8011400976913649007Ivan dela CruzNoch keine Bewertungen

- Case Study #3 - Arambulo, Dianne Khate Q.Dokument2 SeitenCase Study #3 - Arambulo, Dianne Khate Q.Dianne ArambuloNoch keine Bewertungen

- OMDokument1 SeiteOMLULUNoch keine Bewertungen

- Module 1.1 Orientation & PFRS 15Dokument22 SeitenModule 1.1 Orientation & PFRS 15NCTNoch keine Bewertungen

- Division of ProfitsDokument55 SeitenDivision of ProfitsMichole chin MallariNoch keine Bewertungen

- Diagnostic Quiz On Accounting 2Dokument9 SeitenDiagnostic Quiz On Accounting 2Anne Ford67% (3)

- Rizal LawDokument3 SeitenRizal LawMark Angelo TemplanzaNoch keine Bewertungen

- C1 Financial ReportingDokument23 SeitenC1 Financial ReportingSteeeeeeeephNoch keine Bewertungen

- Bam 006: Bank Reconciliation Quiz 2: Use The Problem Below To Answer Numbers 5 - 7Dokument2 SeitenBam 006: Bank Reconciliation Quiz 2: Use The Problem Below To Answer Numbers 5 - 7honeyjoy salapantanNoch keine Bewertungen

- Case Study: Soltronicz EmsDokument7 SeitenCase Study: Soltronicz EmsFritz John Tiamsing MingaoNoch keine Bewertungen

- Activity 2 ECODokument2 SeitenActivity 2 ECOEugene AlipioNoch keine Bewertungen

- Value Chain Management Capability A Complete Guide - 2020 EditionVon EverandValue Chain Management Capability A Complete Guide - 2020 EditionNoch keine Bewertungen

- Perpetual Vs Periodic Inventory SystemDokument3 SeitenPerpetual Vs Periodic Inventory SystemTrina Joy HomerezNoch keine Bewertungen

- Financial Accounting Reviewer - Chapter 58Dokument13 SeitenFinancial Accounting Reviewer - Chapter 58Coursehero PremiumNoch keine Bewertungen

- F2-15 Flexible Budgets, Budgetary Control and ReportingDokument16 SeitenF2-15 Flexible Budgets, Budgetary Control and ReportingJaved ImranNoch keine Bewertungen

- Toast Profit Loss Statement Template 2022Dokument24 SeitenToast Profit Loss Statement Template 2022Krishna SharmaNoch keine Bewertungen

- Ifrs Edition: Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDokument29 SeitenIfrs Edition: Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeBafesh RoyNoch keine Bewertungen

- Business Plan: Horizon Catering: Ms. Christine Joy L. BajadeDokument13 SeitenBusiness Plan: Horizon Catering: Ms. Christine Joy L. BajadeZabdiel B. BatoyNoch keine Bewertungen

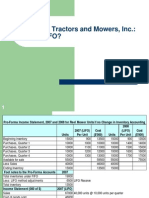

- FDP - Merrimack Tractors and Mowers, Inc.Dokument13 SeitenFDP - Merrimack Tractors and Mowers, Inc.Devyani SinghNoch keine Bewertungen

- Joint and by ProductDokument6 SeitenJoint and by ProductJeric Lagyaban AstrologioNoch keine Bewertungen

- Q - 204 - Peony CompnayDokument4 SeitenQ - 204 - Peony CompnayhusseinNoch keine Bewertungen

- Exercise 1: Solution: Dewitt's Budgeted Operating Income StatementDokument6 SeitenExercise 1: Solution: Dewitt's Budgeted Operating Income StatementShawn MendezNoch keine Bewertungen

- Managerial and Cost Accounting Exercises IIIDokument26 SeitenManagerial and Cost Accounting Exercises IIIMary AngelNoch keine Bewertungen

- Deductions From Gross Income: (Sec. 65, Rev. Reg. No. 2)Dokument69 SeitenDeductions From Gross Income: (Sec. 65, Rev. Reg. No. 2)Brian TorresNoch keine Bewertungen

- FS AnalysisDokument46 SeitenFS AnalysisjaxxNoch keine Bewertungen

- Test Bank Cost Accounting 6e by Raiborn and Kinney Chapter 2Dokument29 SeitenTest Bank Cost Accounting 6e by Raiborn and Kinney Chapter 2PauNoch keine Bewertungen

- CELADokument66 SeitenCELAXha100% (1)

- Problem Solving 1-4Dokument9 SeitenProblem Solving 1-4Mary Ann PerezNoch keine Bewertungen

- 11 Edition: Mcgraw Hill/IrwinDokument79 Seiten11 Edition: Mcgraw Hill/IrwinShinji100% (1)

- Akuntansi Manajemen 8-24Dokument8 SeitenAkuntansi Manajemen 8-24Chika Slalubahagia SlamanyaNoch keine Bewertungen

- 4 FM AssignmentDokument3 Seiten4 FM AssignmentGorav BhallaNoch keine Bewertungen

- M 2010 and 2011 June PDFDokument91 SeitenM 2010 and 2011 June PDFMoses LukNoch keine Bewertungen

- Special Production IssuesDokument43 SeitenSpecial Production IssuesMonique VillaNoch keine Bewertungen

- Financial & Managerial Accounting: Information For DecisionsDokument67 SeitenFinancial & Managerial Accounting: Information For DecisionsHime Silhouette GabrielNoch keine Bewertungen

- Ankur Agarwal InfosysDokument6 SeitenAnkur Agarwal InfosysswatisalonipatroNoch keine Bewertungen

- Technical Study DraftDokument18 SeitenTechnical Study DraftHonorato BugayongNoch keine Bewertungen

- Cost Concepts Class ExercisesDokument7 SeitenCost Concepts Class ExercisesAngel Alejo AcobaNoch keine Bewertungen

- ACCT 504 Midterm ExamDokument7 SeitenACCT 504 Midterm ExamDeVryHelpNoch keine Bewertungen

- CBDT Instructions For Filing New Form Itr 6 Fy 2018 19 Ay 2019 20Dokument66 SeitenCBDT Instructions For Filing New Form Itr 6 Fy 2018 19 Ay 2019 20Anonymous SFy3Uv6Noch keine Bewertungen

- Trend AnalysisDokument3 SeitenTrend AnalysisAniket KedareNoch keine Bewertungen