Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Ionic ConductorsDokument20 SeitenIonic ConductorsGregorio GuzmanNoch keine Bewertungen

- Introduction To Interpretation of Infrared SpectraDokument3 SeitenIntroduction To Interpretation of Infrared SpectraBenni WewokNoch keine Bewertungen

- IR Absorption TableDokument2 SeitenIR Absorption TablefikrifazNoch keine Bewertungen

- Polymer BiodegradationDokument12 SeitenPolymer BiodegradationBenni WewokNoch keine Bewertungen

- Solomons Organic Chemistry Module IR TableDokument1 SeiteSolomons Organic Chemistry Module IR TableBenni WewokNoch keine Bewertungen

- What Is CivilizationDokument1 SeiteWhat Is CivilizationBenni WewokNoch keine Bewertungen

- Pyrolysis - Wikipedia, The Free EncyclopediaDokument9 SeitenPyrolysis - Wikipedia, The Free EncyclopediaBenni WewokNoch keine Bewertungen

- RejangDokument1 SeiteRejangBenni WewokNoch keine Bewertungen

- Examples of Stokes' Theorem and Gauss' Divergence TheoremDokument6 SeitenExamples of Stokes' Theorem and Gauss' Divergence TheoremBenni WewokNoch keine Bewertungen

- Lorentz-Lorenz Equation - Wikipedia, The Free EncyclopediaDokument1 SeiteLorentz-Lorenz Equation - Wikipedia, The Free EncyclopediaBenni WewokNoch keine Bewertungen

- BizDevOps - Group 5Dokument11 SeitenBizDevOps - Group 5Arth GuptaNoch keine Bewertungen

- Mini ServoDokument2 SeitenMini ServoShukri FaezNoch keine Bewertungen

- As 126558 FD-H Im B80GB WW GB 2122 3Dokument16 SeitenAs 126558 FD-H Im B80GB WW GB 2122 3Tim MarvinNoch keine Bewertungen

- Engr FT Intern W11 PDFDokument187 SeitenEngr FT Intern W11 PDFNilesh LambeNoch keine Bewertungen

- Fundamental of Computer - OdtDokument2 SeitenFundamental of Computer - OdtKoti NayakNoch keine Bewertungen

- Computer Basics TextbookDokument103 SeitenComputer Basics Textbookapi-19727066Noch keine Bewertungen

- Setting Up Remote Access To Intouch: Maury BeckDokument32 SeitenSetting Up Remote Access To Intouch: Maury BeckHalilNoch keine Bewertungen

- Linkedin-Skill-Assessments-Quizzes - Javascript-Quiz - MD at Main Ebazhanov - Linkedin-Skill-Assessments-Quizzes GitHubDokument41 SeitenLinkedin-Skill-Assessments-Quizzes - Javascript-Quiz - MD at Main Ebazhanov - Linkedin-Skill-Assessments-Quizzes GitHubAnkit RajNoch keine Bewertungen

- Automation KivaDokument25 SeitenAutomation KivaAnirudh KowthaNoch keine Bewertungen

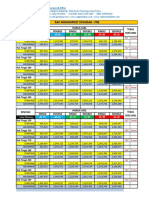

- Rak Minimarket Standar - P90: Single Double Single Double Single Double Rincian Harga Jual Tebal ShelvingDokument6 SeitenRak Minimarket Standar - P90: Single Double Single Double Single Double Rincian Harga Jual Tebal ShelvingAndi HadisaputraNoch keine Bewertungen

- UNITED STATES OF AMERICA Et Al v. MICROSOFT CORPORATION - Document No. 810Dokument16 SeitenUNITED STATES OF AMERICA Et Al v. MICROSOFT CORPORATION - Document No. 810Justia.comNoch keine Bewertungen

- SAP Invoice VerificationDokument9 SeitenSAP Invoice VerificationAJAY PALNoch keine Bewertungen

- DocFetcher ManualDokument5 SeitenDocFetcher Manualsergio_gutmanNoch keine Bewertungen

- ZTE UMTS Connection Management Feature Guide - V8.5 - 201312Dokument175 SeitenZTE UMTS Connection Management Feature Guide - V8.5 - 201312Muhammad Haris100% (1)

- Sixth Sense Technology Sixth SenseDokument19 SeitenSixth Sense Technology Sixth SenseswapnikaNoch keine Bewertungen

- Resume-Varalakshmi SDokument3 SeitenResume-Varalakshmi SCynosure- RahulNoch keine Bewertungen

- HP Storageworks Xp24000 Disk Array Site Preparation Guide: Part Number: Ae131-96036 Fourth Edition: June 2008Dokument72 SeitenHP Storageworks Xp24000 Disk Array Site Preparation Guide: Part Number: Ae131-96036 Fourth Edition: June 2008Adrian TurcuNoch keine Bewertungen

- XeditrefDokument29 SeitenXeditref2uarifNoch keine Bewertungen

- Service Manual: Blu-Ray Disc Home TheaterDokument58 SeitenService Manual: Blu-Ray Disc Home Theaterboroda2410Noch keine Bewertungen

- App-V Recipe For Office 2010 RTM Deployment Kit v3Dokument10 SeitenApp-V Recipe For Office 2010 RTM Deployment Kit v3Hemanth RamNoch keine Bewertungen

- SYS210 Final Revision 2021-2022 SpringDokument11 SeitenSYS210 Final Revision 2021-2022 SpringRefalz AlkhoNoch keine Bewertungen

- CIS Microsoft SQL Server 2019 Benchmark v1.0.0 PDFDokument100 SeitenCIS Microsoft SQL Server 2019 Benchmark v1.0.0 PDFConciencia ImmortalNoch keine Bewertungen

- RATAN CHANDRA ROY - CVDokument3 SeitenRATAN CHANDRA ROY - CVRatan RoyNoch keine Bewertungen

- India Insurance Perspective PDFDokument24 SeitenIndia Insurance Perspective PDFaishwarya raikarNoch keine Bewertungen

- E Katalog 2015Dokument10 SeitenE Katalog 2015Hendra JayaNoch keine Bewertungen

- Fares TicketingDokument41 SeitenFares TicketingKhanjiFarm100% (1)

- Geeta InstituteDokument7 SeitenGeeta Institutesdureja03Noch keine Bewertungen

- 7STEPUX Gift Chapter-6094217Dokument43 Seiten7STEPUX Gift Chapter-6094217Namrata KumariNoch keine Bewertungen

- HP iMC For EngineersDokument2 SeitenHP iMC For EngineersJacobNoch keine Bewertungen