Das könnte Ihnen auch gefallen

- Sonia F Sap Fico ProjectDokument108 SeitenSonia F Sap Fico ProjectSarmistha Biswal80% (10)

- 1 Financial Accounting 1 1Dokument71 Seiten1 Financial Accounting 1 1Hadi KhanNoch keine Bewertungen

- Sap BiDokument1 SeiteSap BiPraveen K SinhaNoch keine Bewertungen

- Play ClawDokument1 SeitePlay ClawHadi KhanNoch keine Bewertungen

- Trade Visitor Form IweDokument1 SeiteTrade Visitor Form IweHadi KhanNoch keine Bewertungen

- Company Profile (1) .11Dokument20 SeitenCompany Profile (1) .11Gowtham Reloaded DNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- FinalDokument107 SeitenFinalAarthi PriyaNoch keine Bewertungen

- Ogr 1990 2011 Front Page Final.Dokument43 SeitenOgr 1990 2011 Front Page Final.Jenny BandiolaNoch keine Bewertungen

- Key Account ManagementDokument34 SeitenKey Account Managementmanin1804100% (1)

- University CatalogueDokument166 SeitenUniversity CatalogueOloo Yussuf Ochieng'Noch keine Bewertungen

- Urban Clap 1Dokument3 SeitenUrban Clap 1naughty ajayNoch keine Bewertungen

- SAL ReportDokument130 SeitenSAL ReportjlolhnpNoch keine Bewertungen

- Sap Pa LISTDokument281 SeitenSap Pa LISTdaniel22% (9)

- Overview of The Front Office DepartmentDokument2 SeitenOverview of The Front Office DepartmentReina100% (3)

- Procurement KPIs - NCTDokument22 SeitenProcurement KPIs - NCTMohamed ElnagdyNoch keine Bewertungen

- MTPDokument5 SeitenMTPNavyanth KalerNoch keine Bewertungen

- Economics - Final Exam Review Questions-Fall 2016Dokument4 SeitenEconomics - Final Exam Review Questions-Fall 2016arvageddonNoch keine Bewertungen

- Upgrade AprMay08 AnalexFDMPlusDokument4 SeitenUpgrade AprMay08 AnalexFDMPlusAzhar AbdullahNoch keine Bewertungen

- ANALYSIS of Walt Disney CaseDokument11 SeitenANALYSIS of Walt Disney CaseStacy D'Souza100% (3)

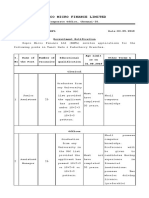

- Repco Micro Finance Limited: Corporate Office, Chennai-35Dokument4 SeitenRepco Micro Finance Limited: Corporate Office, Chennai-35Abaraj IthanNoch keine Bewertungen

- Catalogo AlconDokument27 SeitenCatalogo Alconaku170% (1)

- PAGCOR Site Regulatory ManualDokument4 SeitenPAGCOR Site Regulatory Manualstaircasewit4Noch keine Bewertungen

- Mathematics of Finance Exercise and SolutionDokument14 SeitenMathematics of Finance Exercise and Solutionfarid rosliNoch keine Bewertungen

- Tourism Merchandise As A MeansDokument16 SeitenTourism Merchandise As A MeansSean O'ConnorNoch keine Bewertungen

- ODC - Project - RITES Ltd. - 10P010 - 10P019 - 10P023Dokument20 SeitenODC - Project - RITES Ltd. - 10P010 - 10P019 - 10P023Sehgal AnkitNoch keine Bewertungen

- A 227Dokument1 SeiteA 227AnuranjanNoch keine Bewertungen

- LMS European Aerospace Conference - AIRBUSDokument26 SeitenLMS European Aerospace Conference - AIRBUSCarlo FarlocchianoNoch keine Bewertungen

- Marketing Strategies of Different Products of HUL LTDDokument84 SeitenMarketing Strategies of Different Products of HUL LTDSweetie Rastogi57% (7)

- Ammonia WeeklyDokument18 SeitenAmmonia Weeklymtarek2k100% (1)

- Accounting For Income TaxDokument21 SeitenAccounting For Income Taxkara mNoch keine Bewertungen

- Project Management, Tools, Process, Plans and Project Planning TipsDokument16 SeitenProject Management, Tools, Process, Plans and Project Planning TipsChuma Khan100% (1)

- Essay Test 2021 (Practice Test)Dokument3 SeitenEssay Test 2021 (Practice Test)Philani HadebeNoch keine Bewertungen

- F FFF FFFFFFFFDokument9 SeitenF FFF FFFFFFFFvirenderjpNoch keine Bewertungen

- Tenet Healthcare Corporation 401 (K) Retirement Savings Plan 25100Dokument5 SeitenTenet Healthcare Corporation 401 (K) Retirement Savings Plan 25100anon-822193Noch keine Bewertungen

- 3rd Grading Periodical Exam-EntrepDokument2 Seiten3rd Grading Periodical Exam-EntrepJoan Pineda100% (3)

- M.a.part - I - Macro Economics (Eng)Dokument341 SeitenM.a.part - I - Macro Economics (Eng)Divyesh DixitNoch keine Bewertungen