Das könnte Ihnen auch gefallen

- Bar Review Companion: Taxation: Anvil Law Books Series, #4Von EverandBar Review Companion: Taxation: Anvil Law Books Series, #4Noch keine Bewertungen

- 1040 Exam Prep Module XI: Circular 230 and AMTVon Everand1040 Exam Prep Module XI: Circular 230 and AMTBewertung: 1 von 5 Sternen1/5 (1)

- (Digest) Abakada v. PurisimaDokument5 Seiten(Digest) Abakada v. PurisimaJechel TBNoch keine Bewertungen

- Tax Law 1 DG3 NOTES Part 1Dokument15 SeitenTax Law 1 DG3 NOTES Part 1Fayie De LunaNoch keine Bewertungen

- TAXATION II-case DigestDokument54 SeitenTAXATION II-case Digestleo.rosarioNoch keine Bewertungen

- Tax 2 (Assignment 1)Dokument19 SeitenTax 2 (Assignment 1)Lenette LupacNoch keine Bewertungen

- 23 ABAKADA V Purisima GR No. 166715 Legislative Power Case DigestDokument4 Seiten23 ABAKADA V Purisima GR No. 166715 Legislative Power Case DigestGol Lum100% (2)

- 4 ABAKADA v. PURISIMADokument29 Seiten4 ABAKADA v. PURISIMAkpkintanarNoch keine Bewertungen

- Abakada Guro Party List V Purisima GR No.166715, Aug. 14, 2008Dokument16 SeitenAbakada Guro Party List V Purisima GR No.166715, Aug. 14, 2008amun dinNoch keine Bewertungen

- Case DigestDokument39 SeitenCase DigestKathleen Joy100% (1)

- COURAGE V CIR All IssuesDokument9 SeitenCOURAGE V CIR All IssuesJake MacTavishNoch keine Bewertungen

- FilinvestDokument36 SeitenFilinvestNolas JayNoch keine Bewertungen

- FactsDokument43 SeitenFactsRvic CivrNoch keine Bewertungen

- Asyn R2 Ay22324 Tax RevDokument10 SeitenAsyn R2 Ay22324 Tax RevBogs QuitainNoch keine Bewertungen

- ABAKADA GURO PARTY LIST Vs PURISIMADokument152 SeitenABAKADA GURO PARTY LIST Vs PURISIMAMichael SevillaNoch keine Bewertungen

- Abakadaguro VS Purisima CSDokument6 SeitenAbakadaguro VS Purisima CSSmile SiervoNoch keine Bewertungen

- IntroductionDokument9 SeitenIntroductionTonton ReyesNoch keine Bewertungen

- Taxing Authority Till Income TaxDokument8 SeitenTaxing Authority Till Income TaxRonellie Marie TinajaNoch keine Bewertungen

- Abakada Guro Party List Vs PurisimaDokument4 SeitenAbakada Guro Party List Vs PurisimaDennisgilbert Gonzales100% (1)

- March 16 CasesDokument14 SeitenMarch 16 CasesybunNoch keine Bewertungen

- Abakada PL VS PurisimaDokument14 SeitenAbakada PL VS PurisimaCristian Gregor AtacadorNoch keine Bewertungen

- BOCEA Vs TevesDokument2 SeitenBOCEA Vs TevesGem S. AlegadoNoch keine Bewertungen

- Critical Areas in TaxationDokument41 SeitenCritical Areas in TaxationAndro Julio QuimpoNoch keine Bewertungen

- Lecture Notes Tax Enforcement PDFDokument7 SeitenLecture Notes Tax Enforcement PDFEstele EstellaNoch keine Bewertungen

- Powers of Administrative AgenciesDokument16 SeitenPowers of Administrative Agenciesartburce30Noch keine Bewertungen

- 08 Abakada V PurisimaDokument53 Seiten08 Abakada V PurisimaPing KyNoch keine Bewertungen

- Taxation NotesDokument40 SeitenTaxation NotesFelixberto Jr. BaisNoch keine Bewertungen

- Retroactive Application If The Revocation, Modification or Reversal Will Be Prejudicial To The Taxpayers, Except in The Following CasesDokument4 SeitenRetroactive Application If The Revocation, Modification or Reversal Will Be Prejudicial To The Taxpayers, Except in The Following CasesIrish AnnNoch keine Bewertungen

- Creba vs. RomuloDokument4 SeitenCreba vs. RomuloJD BallosNoch keine Bewertungen

- LG-Electronics-vs.-CIR-digestDokument21 SeitenLG-Electronics-vs.-CIR-digestDarrel John SombilonNoch keine Bewertungen

- Arellano LMT TaxDokument32 SeitenArellano LMT TaxGretchen Alunday SuarezNoch keine Bewertungen

- ABKADA To LaurelDokument24 SeitenABKADA To LaurelJosephine Huelva VictorNoch keine Bewertungen

- Republic V CaguioaDokument3 SeitenRepublic V CaguioaViolet Parker100% (2)

- G.R. No. 166715Dokument13 SeitenG.R. No. 166715a aNoch keine Bewertungen

- AbakadaGuro Party List v. Purisima, 562 SCRA 251 (2008)Dokument31 SeitenAbakadaGuro Party List v. Purisima, 562 SCRA 251 (2008)Enrique Dela CruzNoch keine Bewertungen

- Remedies of The TaxpayerDokument4 SeitenRemedies of The TaxpayerAngelyn Sanjorjo50% (2)

- Cases Under Permissible Delegation and Rule-Making PowerDokument57 SeitenCases Under Permissible Delegation and Rule-Making PowerFaye Cience BoholNoch keine Bewertungen

- TAX GenPrin AdditionalDokument13 SeitenTAX GenPrin Additionalchristie joiNoch keine Bewertungen

- Tax CasesDokument5 SeitenTax CasesMelvin L. TomarongNoch keine Bewertungen

- Republic of The Philippines Vs CaguioaDokument3 SeitenRepublic of The Philippines Vs CaguioaSylver Jan100% (1)

- Abakada PL VS Purisima SummarizedDokument15 SeitenAbakada PL VS Purisima SummarizedCristian Gregor AtacadorNoch keine Bewertungen

- Abakada Guro Vs PurisimaDokument16 SeitenAbakada Guro Vs Purisimahmn_scribdNoch keine Bewertungen

- 1 Quasi-Legislative Power - Case #8Dokument13 Seiten1 Quasi-Legislative Power - Case #8JulieNoch keine Bewertungen

- 2016 Bar Exam Suggested Answers in Taxation by The UP Law ComplexDokument23 Seiten2016 Bar Exam Suggested Answers in Taxation by The UP Law Complexrobertoii_suarez67% (3)

- Petitioners: en BancDokument52 SeitenPetitioners: en BancCarol TumanengNoch keine Bewertungen

- Republic of The Philippines Vs CaguioaDokument3 SeitenRepublic of The Philippines Vs CaguioaCharlotte Louise Maglasang100% (3)

- Political Law Review Assignment For 10 17 15Dokument4 SeitenPolitical Law Review Assignment For 10 17 15Leonel DomingoNoch keine Bewertungen

- Justice Teresita Leonardo-De Castro Cases (2008-2015) : Scope and Limitations of Taxation (Constitutional Limitations)Dokument4 SeitenJustice Teresita Leonardo-De Castro Cases (2008-2015) : Scope and Limitations of Taxation (Constitutional Limitations)jimNoch keine Bewertungen

- Tax Digest For CTA JurisdictionDokument7 SeitenTax Digest For CTA JurisdictionGeoanne Battad BeringuelaNoch keine Bewertungen

- Sbu Tax MT Samaniego Emil (4S)Dokument5 SeitenSbu Tax MT Samaniego Emil (4S)Naked PolitixxxNoch keine Bewertungen

- A Bak AdaDokument23 SeitenA Bak Adarizzle88Noch keine Bewertungen

- G.R. No. 166715 Abakada Gurp v. PurisimaDokument12 SeitenG.R. No. 166715 Abakada Gurp v. PurisimaMarkNoch keine Bewertungen

- GR No. 166715Dokument10 SeitenGR No. 166715wafa tumindegNoch keine Bewertungen

- Taxation Cases No 21 To 25Dokument6 SeitenTaxation Cases No 21 To 25Alkhadri H MuinNoch keine Bewertungen

- 006 Abakada Guro Party-List v. Purisima, G.R. No. 166715, August 14, 2008, 562 SCRA 251Dokument14 Seiten006 Abakada Guro Party-List v. Purisima, G.R. No. 166715, August 14, 2008, 562 SCRA 251JD SectionDNoch keine Bewertungen

- Green Star Express, Inc. v. Nissin-Universal RobinaDokument5 SeitenGreen Star Express, Inc. v. Nissin-Universal RobinaRoger AquinoNoch keine Bewertungen

- Explanatory Notes NIRC 1-30 Part 1 Aug2018Dokument23 SeitenExplanatory Notes NIRC 1-30 Part 1 Aug2018Anonymous MikI28PkJcNoch keine Bewertungen

- Abakada Guro v. Purisima, G.R. No. 166715, August 14, 2008. Full TextDokument20 SeitenAbakada Guro v. Purisima, G.R. No. 166715, August 14, 2008. Full TextRyuzaki HidekiNoch keine Bewertungen

- RA 9160-Anti-Money Laundering Act of 2001Dokument49 SeitenRA 9160-Anti-Money Laundering Act of 2001Rocky MarcianoNoch keine Bewertungen

- TITLE VII of RPC - Crimes Committed by Public OfficersDokument11 SeitenTITLE VII of RPC - Crimes Committed by Public OfficersCrislene CruzNoch keine Bewertungen

- RA 9208 - Anti-Trafficking in Persons Act of 2003Dokument13 SeitenRA 9208 - Anti-Trafficking in Persons Act of 2003Rocky MarcianoNoch keine Bewertungen

- RA 8505 - Rape Victim Protection and Assistance Act of 1998Dokument3 SeitenRA 8505 - Rape Victim Protection and Assistance Act of 1998Rocky MarcianoNoch keine Bewertungen

- RA 9262 - Anti-Violence Against Women and Their Children Act of 2004Dokument16 SeitenRA 9262 - Anti-Violence Against Women and Their Children Act of 2004Rocky MarcianoNoch keine Bewertungen

- Executive Order 317 - Prescribing A Code of Condut For Relatives and Close Personal Relations of The President Etc..Dokument4 SeitenExecutive Order 317 - Prescribing A Code of Condut For Relatives and Close Personal Relations of The President Etc..Crislene CruzNoch keine Bewertungen

- RA 9262 - Anti-Violence Against Women and Their Children Act of 2004Dokument16 SeitenRA 9262 - Anti-Violence Against Women and Their Children Act of 2004Rocky MarcianoNoch keine Bewertungen

- RA 9372-Human Security Act of 2007 (Securing and Protecting The State From Terrorism)Dokument23 SeitenRA 9372-Human Security Act of 2007 (Securing and Protecting The State From Terrorism)Rocky Marciano100% (1)

- BP 186-An Act Increasing The Penalty For White Slave Trade, Amending For The Purpose Article 341 of The Revised Penal Code.Dokument1 SeiteBP 186-An Act Increasing The Penalty For White Slave Trade, Amending For The Purpose Article 341 of The Revised Penal Code.Rocky MarcianoNoch keine Bewertungen

- Commonwealth Act 578-An Act To Amend Art 152 of The RPC To Include Teachers, Professors, Etc With The Term Persons in AuthorityDokument1 SeiteCommonwealth Act 578-An Act To Amend Art 152 of The RPC To Include Teachers, Professors, Etc With The Term Persons in AuthorityRocky MarcianoNoch keine Bewertungen

- Commonwealth Act No. 616 An Act To Punish Espionage and Other Offenses Against The National SecurityDokument5 SeitenCommonwealth Act No. 616 An Act To Punish Espionage and Other Offenses Against The National SecurityJulia RosalesNoch keine Bewertungen

- Executive Order 12 - Creating The Presidential Anti-Graft Commission EtcDokument14 SeitenExecutive Order 12 - Creating The Presidential Anti-Graft Commission EtcCrislene CruzNoch keine Bewertungen

- BP 33-An Act Defining and Penalizing Certain Prohibited Acts Inimical To The Public Interest and National Security Involving Petroleum and or Petroleum Products Etc.Dokument2 SeitenBP 33-An Act Defining and Penalizing Certain Prohibited Acts Inimical To The Public Interest and National Security Involving Petroleum and or Petroleum Products Etc.Rocky MarcianoNoch keine Bewertungen

- BP 71-An Act Further Amending Article 310 of The Revised Penal CodeDokument1 SeiteBP 71-An Act Further Amending Article 310 of The Revised Penal CodeRocky MarcianoNoch keine Bewertungen

- Act 4103 - The Indeterminate Sentence LawDokument3 SeitenAct 4103 - The Indeterminate Sentence LawRocky MarcianoNoch keine Bewertungen

- Part I and Part II On The Law of The SeaDokument11 SeitenPart I and Part II On The Law of The SeaCrislene CruzNoch keine Bewertungen

- BP 6-An Act Reducing The Penalty For Illegal Possession of Bladed, Pointed or Blunt Weapons, and For Other Purposes, Amending For The Purpose PD 9Dokument1 SeiteBP 6-An Act Reducing The Penalty For Illegal Possession of Bladed, Pointed or Blunt Weapons, and For Other Purposes, Amending For The Purpose PD 9Rocky MarcianoNoch keine Bewertungen

- Book One - Articles 1-113Dokument51 SeitenBook One - Articles 1-113Crislene CruzNoch keine Bewertungen

- BP 33-An Act Defining and Penalizing Certain Prohibited Acts Inimical To The Public Interest and National Security Involving Petroleum and or Petroleum Products Etc.Dokument2 SeitenBP 33-An Act Defining and Penalizing Certain Prohibited Acts Inimical To The Public Interest and National Security Involving Petroleum and or Petroleum Products Etc.Rocky MarcianoNoch keine Bewertungen

- Batas Pambansa Blg. 22-Check and Bouncing LawDokument2 SeitenBatas Pambansa Blg. 22-Check and Bouncing LawRocky MarcianoNoch keine Bewertungen

- RA 6733-Amending Sec. 21, Title I, Book I of The Revised Administrative Code of 1987Dokument2 SeitenRA 6733-Amending Sec. 21, Title I, Book I of The Revised Administrative Code of 1987Rocky MarcianoNoch keine Bewertungen

- BP 185-Implementing Sec. 15 of Article 14 of The Phil Constitution EtcDokument3 SeitenBP 185-Implementing Sec. 15 of Article 14 of The Phil Constitution EtcRosa GamaroNoch keine Bewertungen

- RA 6645-Prescribing The Manner of Filling A Vacancy in The CongressDokument2 SeitenRA 6645-Prescribing The Manner of Filling A Vacancy in The CongressRocky MarcianoNoch keine Bewertungen

- RA 6735 - The Initiative and Referendum ActDokument8 SeitenRA 6735 - The Initiative and Referendum ActRocky MarcianoNoch keine Bewertungen

- RA 6832 - Creating A Commission of Fact-Finding Investigation of The Coup De'tat (Dec 1989)Dokument5 SeitenRA 6832 - Creating A Commission of Fact-Finding Investigation of The Coup De'tat (Dec 1989)Rocky MarcianoNoch keine Bewertungen

- RA 6682 - Amending The Effectivity Clause of The Administrative Code (Exec Order 292)Dokument1 SeiteRA 6682 - Amending The Effectivity Clause of The Administrative Code (Exec Order 292)Rocky MarcianoNoch keine Bewertungen

- RA 6826 - Authorizing The President To Declare National Emergency Etc..Dokument5 SeitenRA 6826 - Authorizing The President To Declare National Emergency Etc..Rocky Marciano100% (1)

- RA 6766 - Providing An Organic Act For The Cordillera Autonomous RegionDokument44 SeitenRA 6766 - Providing An Organic Act For The Cordillera Autonomous RegionRocky MarcianoNoch keine Bewertungen

- RA 6942-Increasing The Insurance Benefits of The Local Govt OfficialsDokument6 SeitenRA 6942-Increasing The Insurance Benefits of The Local Govt OfficialsRocky MarcianoNoch keine Bewertungen

- RA 6975-Department of The Interior and Local Govt Act of 1990Dokument38 SeitenRA 6975-Department of The Interior and Local Govt Act of 1990Rocky MarcianoNoch keine Bewertungen

- What Will Become of The Philippines Within A Century? Will They Continue To Be A Spanish Colony?Dokument4 SeitenWhat Will Become of The Philippines Within A Century? Will They Continue To Be A Spanish Colony?Hamoy RhomelNoch keine Bewertungen

- TAITZ V ASTRUE (USDC HI) - 15 - ORDER DENYING PLAINTIFF'S EMERGENCY EX PARTE MOTION FOR EMERGENCY ORDER TO SHOW CAUSE AND - Gov - Uscourts.hid.98529.15.0Dokument2 SeitenTAITZ V ASTRUE (USDC HI) - 15 - ORDER DENYING PLAINTIFF'S EMERGENCY EX PARTE MOTION FOR EMERGENCY ORDER TO SHOW CAUSE AND - Gov - Uscourts.hid.98529.15.0Jack RyanNoch keine Bewertungen

- Can The World Health Organization Meet The Challenge of The Pandemic - DER SPIEGELDokument9 SeitenCan The World Health Organization Meet The Challenge of The Pandemic - DER SPIEGELveroNoch keine Bewertungen

- WARN Trans States AirlinesDokument2 SeitenWARN Trans States AirlinesDavid PurtellNoch keine Bewertungen

- CSC158 Practice Problems 6Dokument4 SeitenCSC158 Practice Problems 6Cantillo, AdrianeNoch keine Bewertungen

- Republic Acts Relevant For LETDokument2 SeitenRepublic Acts Relevant For LETAngelle BahinNoch keine Bewertungen

- Fascism Is More Than Reaction - Roger GriffinDokument8 SeitenFascism Is More Than Reaction - Roger GriffinCastro Ricardo100% (1)

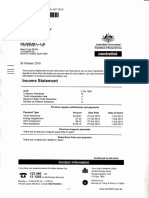

- Income Statement: Llillliltll) Ilililtil)Dokument1 SeiteIncome Statement: Llillliltll) Ilililtil)Indy EfuNoch keine Bewertungen

- Multiculturalism Goes To CollegeDokument10 SeitenMulticulturalism Goes To CollegeArdel B. CanedayNoch keine Bewertungen

- Good Governance and Public Policy in India: V Mallika VedanthamDokument12 SeitenGood Governance and Public Policy in India: V Mallika Vedanthamdurgesh kumar gandharveNoch keine Bewertungen

- Bock-Ch15 Problems Probability RulesDokument10 SeitenBock-Ch15 Problems Probability RulesTaylorNoch keine Bewertungen

- Application For Judicial TitlingDokument4 SeitenApplication For Judicial TitlingBernadine Nacua100% (3)

- 1 PANTRANCO Vs PSC Admin LawDokument2 Seiten1 PANTRANCO Vs PSC Admin Lawmarianbdr100% (1)

- Instant Download Real Estate Principles A Value Approach 4th Edition Ling Test Bank PDF Full ChapterDokument32 SeitenInstant Download Real Estate Principles A Value Approach 4th Edition Ling Test Bank PDF Full Chaptersinhhanhi7rp100% (4)

- Owens Charge2 PDFDokument2 SeitenOwens Charge2 PDFmjguarigliaNoch keine Bewertungen

- Team Based Compensation: Made By: Prashansa Madan Pragya SabharwalDokument18 SeitenTeam Based Compensation: Made By: Prashansa Madan Pragya SabharwalVijay AnandNoch keine Bewertungen

- Reflection Paper Human Right and GenderDokument8 SeitenReflection Paper Human Right and GenderStephen Celoso EscartinNoch keine Bewertungen

- Financial Times Europe - 30-10-2018Dokument26 SeitenFinancial Times Europe - 30-10-2018Shivam ShuklaNoch keine Bewertungen

- Un Challenges and Response To Issues Maritime Dispute in The West Philippine SeaDokument2 SeitenUn Challenges and Response To Issues Maritime Dispute in The West Philippine SeaNicole PalimaNoch keine Bewertungen

- General Knowledge - Awareness Quiz - Multiple Choice Question (MCQ) Answers Solution 2013 Online Mock TestDokument8 SeitenGeneral Knowledge - Awareness Quiz - Multiple Choice Question (MCQ) Answers Solution 2013 Online Mock TestSanjay Thapa100% (1)

- b2 Open Cloze - World War 2 1Dokument3 Seitenb2 Open Cloze - World War 2 1Delia MaroneNoch keine Bewertungen

- 10 Mesmerizing Facts About Hypnosis - Listverse PDFDokument20 Seiten10 Mesmerizing Facts About Hypnosis - Listverse PDFWeiya Cuña100% (1)

- Brgy Mapalad Resolution No. 23 Barangay Health CenterDokument2 SeitenBrgy Mapalad Resolution No. 23 Barangay Health Center잔돈100% (1)

- Alalayan V NPCDokument5 SeitenAlalayan V NPCRush YuviencoNoch keine Bewertungen

- 11-6-New York (Siena)Dokument3 Seiten11-6-New York (Siena)NoFilter PoliticsNoch keine Bewertungen

- Indian Power DistanceDokument3 SeitenIndian Power DistanceKing ThameNoch keine Bewertungen

- Geneva AccordsDokument13 SeitenGeneva AccordsGirly placeNoch keine Bewertungen

- Law, Rhetoric, and Irony in The Formation of Canadian Civil Culture (PDFDrive)Dokument374 SeitenLaw, Rhetoric, and Irony in The Formation of Canadian Civil Culture (PDFDrive)Dávid KisNoch keine Bewertungen

- Critical Thinking and Discussion QuestionsDokument2 SeitenCritical Thinking and Discussion QuestionsLhea ClomaNoch keine Bewertungen

- 2 The Legal and Financial FrameworkDokument2 Seiten2 The Legal and Financial FrameworkJaden CallanganNoch keine Bewertungen