Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- COPYRIGHT FRANCE ® U3S61B7 - Logo - Logan's Corporation LTDDokument1 SeiteCOPYRIGHT FRANCE ® U3S61B7 - Logo - Logan's Corporation LTDLogan's LtdNoch keine Bewertungen

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Logan's LTD 5832Dokument1 SeiteLogan's LTD 5832Logan's LtdNoch keine Bewertungen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Reviewing The OECD Harmful Tax Initiative: The St. Vincent and The Grenadines Perspective by Louise MitchellDokument16 SeitenReviewing The OECD Harmful Tax Initiative: The St. Vincent and The Grenadines Perspective by Louise MitchellLogan's LtdNoch keine Bewertungen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (894)

- 15th January, 2003 - Introduction To The Offshore Insurance Sector SVG Insurance Sector - Author Grenville A. John, Commissioner of Int'l InsuranceDokument3 Seiten15th January, 2003 - Introduction To The Offshore Insurance Sector SVG Insurance Sector - Author Grenville A. John, Commissioner of Int'l InsuranceLogan's LtdNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Mark ZuckerbergDokument1 SeiteMark ZuckerbergLogan's LtdNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- 24th May 2002 - USA Patriot Act Author Louise MitchellDokument5 Seiten24th May 2002 - USA Patriot Act Author Louise MitchellLogan's LtdNoch keine Bewertungen

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Logan's LTDDokument1 SeiteLogan's LTDLogan's LtdNoch keine Bewertungen

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Logan's LTD 1936Dokument1 SeiteLogan's LTD 1936Logan's LtdNoch keine Bewertungen

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Logan's LTD 195Dokument1 SeiteLogan's LTD 195Logan's LtdNoch keine Bewertungen

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- Logan's LimitedDokument1 SeiteLogan's LimitedLogan's LtdNoch keine Bewertungen

- 8th April 2003 - Anti-Money Laundering Training Seminar For Prosecutors, Public Legal Attorney General's Speech - Author AG Judith Jones-MorganDokument5 Seiten8th April 2003 - Anti-Money Laundering Training Seminar For Prosecutors, Public Legal Attorney General's Speech - Author AG Judith Jones-MorganLogan's LtdNoch keine Bewertungen

- 7th September 2005 - Do Offshore Financial Centres Still Offer Confidentiality Offshore Confidentiality - Author Louise MitchellDokument10 Seiten7th September 2005 - Do Offshore Financial Centres Still Offer Confidentiality Offshore Confidentiality - Author Louise MitchellLogan's LtdNoch keine Bewertungen

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- United Nations Anti-Terrorism Measures Act 2002Dokument16 SeitenUnited Nations Anti-Terrorism Measures Act 2002Logan's LtdNoch keine Bewertungen

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Amendment To Proceeds of Crime and Money Laundering (Prevention) ActDokument14 SeitenAmendment To Proceeds of Crime and Money Laundering (Prevention) ActLogan's LtdNoch keine Bewertungen

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- St. Vincent Building and Loan Assoc. Rules 2000Dokument48 SeitenSt. Vincent Building and Loan Assoc. Rules 2000Logan's LtdNoch keine Bewertungen

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Capital Adequcay GuidelinesDokument5 SeitenCapital Adequcay GuidelinesRavi Shanker PandeyNoch keine Bewertungen

- Registered Agent and Trustee License Application - Schedule ADokument2 SeitenRegistered Agent and Trustee License Application - Schedule ALogan's LtdNoch keine Bewertungen

- Statement of Guidance Large ExposuresDokument3 SeitenStatement of Guidance Large ExposuresLogan's LtdNoch keine Bewertungen

- Registered Agent & Trustee Licensing Statutory Rules and Orders 1996Dokument26 SeitenRegistered Agent & Trustee Licensing Statutory Rules and Orders 1996Logan's LtdNoch keine Bewertungen

- Registered Agent & Trustee Licensing Amendments 1996 & 2004Dokument5 SeitenRegistered Agent & Trustee Licensing Amendments 1996 & 2004Logan's LtdNoch keine Bewertungen

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Proceeds of Crime (Money Laundering) Regulations 2002Dokument14 SeitenProceeds of Crime (Money Laundering) Regulations 2002Logan's LtdNoch keine Bewertungen

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- Registered Agent & Trustee Licensing Act Chapter 105 of The Revised Laws of Saint Vincent and The Grenadines, 2009Dokument21 SeitenRegistered Agent & Trustee Licensing Act Chapter 105 of The Revised Laws of Saint Vincent and The Grenadines, 2009Logan's LtdNoch keine Bewertungen

- Personal Questionnaire - Registered Agent & Trustee License ApplicationDokument5 SeitenPersonal Questionnaire - Registered Agent & Trustee License ApplicationLogan's LtdNoch keine Bewertungen

- Registered Agent & Trustee License ApplicationDokument7 SeitenRegistered Agent & Trustee License ApplicationLogan's LtdNoch keine Bewertungen

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Proceeds of Crime (Amendment) Regulations 2002Dokument2 SeitenProceeds of Crime (Amendment) Regulations 2002Logan's LtdNoch keine Bewertungen

- Mutual Funds Checklist Jan-2012Dokument7 SeitenMutual Funds Checklist Jan-2012Logan's LtdNoch keine Bewertungen

- Proceeds of Crime and Money Laundering (Prevention) Act 2001Dokument90 SeitenProceeds of Crime and Money Laundering (Prevention) Act 2001Logan's LtdNoch keine Bewertungen

- Personal Questionnaire - International Banking License ApplicationDokument5 SeitenPersonal Questionnaire - International Banking License ApplicationLogan's LtdNoch keine Bewertungen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Mutual Funds Regulations 1999Dokument89 SeitenMutual Funds Regulations 1999Logan's LtdNoch keine Bewertungen

- Fee Information Document: Service Fee General Account ServicesDokument7 SeitenFee Information Document: Service Fee General Account ServicesAndreea SaftaNoch keine Bewertungen

- Credit Card StatementDokument4 SeitenCredit Card Statementsaeed shamiNoch keine Bewertungen

- 13 Overdraft SchemeDokument17 Seiten13 Overdraft SchemeShaurya SinghNoch keine Bewertungen

- Wells Fargo Combined Statement of AccountsDokument6 SeitenWells Fargo Combined Statement of AccountsTheNoch keine Bewertungen

- In Re Clifton J SpearsDokument9 SeitenIn Re Clifton J SpearswstNoch keine Bewertungen

- A Comparative Study of Recruitment Process Between HDFC Bank and Sbi Bank at Moradabad RegionDokument86 SeitenA Comparative Study of Recruitment Process Between HDFC Bank and Sbi Bank at Moradabad RegionbuddysmbdNoch keine Bewertungen

- MetaBank Deposit Account AgreementDokument31 SeitenMetaBank Deposit Account AgreementNarcara HarvilleNoch keine Bewertungen

- Standard Charted - SaadiqDokument16 SeitenStandard Charted - SaadiqkirshanlalNoch keine Bewertungen

- Indian Banking SystemDokument67 SeitenIndian Banking SystemTejas MakwanaNoch keine Bewertungen

- RAKBANK Credit Cards Terms & Conditions SummaryDokument52 SeitenRAKBANK Credit Cards Terms & Conditions SummaryRome AdolNoch keine Bewertungen

- Bank Appeal LetterDokument2 SeitenBank Appeal LetterCorvette Vittorio Vendetto50% (4)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Board Resolution For Opening Bank AccountDokument2 SeitenBoard Resolution For Opening Bank Accountnrlegal75% (4)

- Bank Reconciliation Statement NumericalDokument6 SeitenBank Reconciliation Statement NumericalTejas RajNoch keine Bewertungen

- Basic Instructions For A Bank Reconciliation StatementDokument4 SeitenBasic Instructions For A Bank Reconciliation StatementMary100% (14)

- Bank Reconciliation StatementsDokument6 SeitenBank Reconciliation StatementsTawanda Tatenda Herbert0% (1)

- Vaishnavi Dandekar - Financial Performance Commercial BankDokument67 SeitenVaishnavi Dandekar - Financial Performance Commercial BankMitesh Prajapati 7765Noch keine Bewertungen

- Barclays Bank statement transactionsDokument4 SeitenBarclays Bank statement transactionsAli RAZA100% (1)

- Knecht vs. United Cigarette CorpDokument17 SeitenKnecht vs. United Cigarette CorpVern Villarica CastilloNoch keine Bewertungen

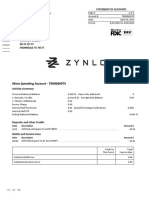

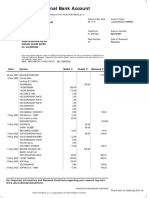

- Zynlo Bank April 2023 Statement for Account 7000060975Dokument2 SeitenZynlo Bank April 2023 Statement for Account 7000060975mrs merle westonNoch keine Bewertungen

- DH 0222Dokument14 SeitenDH 0222The Delphos HeraldNoch keine Bewertungen

- Check, DefinedDokument17 SeitenCheck, DefinedMykee NavalNoch keine Bewertungen

- Business Studies Finance and Accounting Unit 5 Chapter 26Dokument38 SeitenBusiness Studies Finance and Accounting Unit 5 Chapter 26Krishna Das ShresthaNoch keine Bewertungen

- Standard Accounts: IntroducingDokument24 SeitenStandard Accounts: IntroducingsathishNoch keine Bewertungen

- View Your Credit Union Account StatementDokument5 SeitenView Your Credit Union Account StatementZheng YangNoch keine Bewertungen

- Bank Reconciliation StatementDokument3 SeitenBank Reconciliation StatementZoie JulienNoch keine Bewertungen

- Entoto polytechnic savings plan moduleDokument13 SeitenEntoto polytechnic savings plan moduleembiale ayaluNoch keine Bewertungen

- Indian Overseas Bank ..BranchDokument6 SeitenIndian Overseas Bank ..Branchanwarali1975Noch keine Bewertungen

- Wells Fargo Everyday Checking: Important Account InformationDokument3 SeitenWells Fargo Everyday Checking: Important Account Informationbreanne100% (3)

- 2nd August 2022Dokument8 Seiten2nd August 2022Lucas PaixaoNoch keine Bewertungen

- Plastic MoneyDokument13 SeitenPlastic MoneyMaliha IrshadNoch keine Bewertungen

- The Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsVon EverandThe Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsNoch keine Bewertungen

- Budget Management for Beginners: Proven Strategies to Revamp Business & Personal Finance Habits. Stop Living Paycheck to Paycheck, Get Out of Debt, and Save Money for Financial Freedom.Von EverandBudget Management for Beginners: Proven Strategies to Revamp Business & Personal Finance Habits. Stop Living Paycheck to Paycheck, Get Out of Debt, and Save Money for Financial Freedom.Bewertung: 5 von 5 Sternen5/5 (82)

- You Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You WantVon EverandYou Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You WantBewertung: 4 von 5 Sternen4/5 (104)

- Rich Nurse Poor Nurses The Critical Stuff Nursing School Forgot To Teach YouVon EverandRich Nurse Poor Nurses The Critical Stuff Nursing School Forgot To Teach YouNoch keine Bewertungen

- Financial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassVon EverandFinancial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassNoch keine Bewertungen

- Sacred Success: A Course in Financial MiraclesVon EverandSacred Success: A Course in Financial MiraclesBewertung: 5 von 5 Sternen5/5 (15)