Das könnte Ihnen auch gefallen

- The Essentials of Finance and Accounting for Nonfinancial ManagersVon EverandThe Essentials of Finance and Accounting for Nonfinancial ManagersBewertung: 5 von 5 Sternen5/5 (1)

- Management AccountingDokument155 SeitenManagement AccountingBbaggi Bk100% (2)

- Management Accounting Concepts and TechniquesDokument277 SeitenManagement Accounting Concepts and TechniquesCalvince OumaNoch keine Bewertungen

- Management AccountingDokument188 SeitenManagement Accountingabdul100% (1)

- Management Accounting Concepts and Techniques: Scholars ArchiveDokument18 SeitenManagement Accounting Concepts and Techniques: Scholars ArchiveKristina BankauskaiteNoch keine Bewertungen

- Overview of Managerial Accounting: 1.2 The Position of Management Accounting in The OrganizationDokument6 SeitenOverview of Managerial Accounting: 1.2 The Position of Management Accounting in The OrganizationPrakash RawalNoch keine Bewertungen

- Uses of Management Accounting: Record KeepingDokument5 SeitenUses of Management Accounting: Record Keepingisfaq_kNoch keine Bewertungen

- Principles of AccountingDokument183 SeitenPrinciples of AccountingJoe UpZone100% (1)

- FC ProjectDokument17 SeitenFC Projectutub3abr0Noch keine Bewertungen

- Topic For Research Paper Related To AccountingDokument8 SeitenTopic For Research Paper Related To Accountingc9rbzcr0100% (1)

- Expanding Horizon of Entrepreneurship Through Computerized Accounting FullDokument10 SeitenExpanding Horizon of Entrepreneurship Through Computerized Accounting FullVasim AhmadNoch keine Bewertungen

- Sample Topics For Research Paper About AccountingDokument7 SeitenSample Topics For Research Paper About Accountingaflbmfjse100% (1)

- Assignment: Principles of AccountingDokument11 SeitenAssignment: Principles of Accountingmudassar saeedNoch keine Bewertungen

- Research Paper Topics Related To AccountingDokument4 SeitenResearch Paper Topics Related To Accountingegja0g11100% (1)

- AP NurTasnimDokument25 SeitenAP NurTasnimAtta UllahNoch keine Bewertungen

- Chapter 1 PAIDokument18 SeitenChapter 1 PAIabdihalimNoch keine Bewertungen

- Research Paper On Creative AccountingDokument7 SeitenResearch Paper On Creative Accountingwroworplg100% (1)

- Ap 1 RedoDokument23 SeitenAp 1 Redonguyenphamnhungoc51Noch keine Bewertungen

- Term Paper On Management AccountingDokument7 SeitenTerm Paper On Management Accountingc5ryek5a100% (1)

- Chapter 1Dokument23 SeitenChapter 1yvergara00Noch keine Bewertungen

- Financial Reporting Thesis PDFDokument6 SeitenFinancial Reporting Thesis PDFUK100% (2)

- Chapter 1 TVTDokument14 SeitenChapter 1 TVTtemedebereNoch keine Bewertungen

- Buy-Side Business Attribution - TABB VersionDokument11 SeitenBuy-Side Business Attribution - TABB VersiontabbforumNoch keine Bewertungen

- Thesis Financial Statement AnalysisDokument5 SeitenThesis Financial Statement Analysisheatheredwardsmobile100% (1)

- 1 Ch.1 Fundamentals of Financial Accounting: PIDP 3240 Assignment 4 (Textbook Chapter)Dokument7 Seiten1 Ch.1 Fundamentals of Financial Accounting: PIDP 3240 Assignment 4 (Textbook Chapter)Jaspal SinghNoch keine Bewertungen

- Contemporary Issues in Finance - International Aspects of Corporate Finance - Jerralyn AlvaDokument5 SeitenContemporary Issues in Finance - International Aspects of Corporate Finance - Jerralyn AlvaJERRALYN ALVANoch keine Bewertungen

- Lo 1Dokument3 SeitenLo 1Uzma SiddiquiNoch keine Bewertungen

- Discussion Questions Chapter 1 3Dokument16 SeitenDiscussion Questions Chapter 1 3April Ann C. GarciaNoch keine Bewertungen

- Abdul Sami FADokument76 SeitenAbdul Sami FAAbdul SamiNoch keine Bewertungen

- Chapter 1: Accounting and The Business Environment: Objective 1Dokument23 SeitenChapter 1: Accounting and The Business Environment: Objective 1jennyNoch keine Bewertungen

- 2 Managerial Accounting and The Budgeting ProcessDokument9 Seiten2 Managerial Accounting and The Budgeting ProcessAshraf Galal100% (1)

- PROJECT Chap. 1Dokument7 SeitenPROJECT Chap. 1Muabecho FatimatuNoch keine Bewertungen

- Finance For Managers NotesDokument114 SeitenFinance For Managers NotesDavid Luko Chifwalo100% (1)

- Accounting Information System Term PaperDokument5 SeitenAccounting Information System Term Paperafdtuwxrb100% (1)

- FINANCE FOR MANAGER TERM PAPERxxxDokument12 SeitenFINANCE FOR MANAGER TERM PAPERxxxFrank100% (1)

- Bbac 142 - Managerial Accounting 2022Dokument8 SeitenBbac 142 - Managerial Accounting 2022sipanjegivenNoch keine Bewertungen

- Informe Ignacio 2Dokument8 SeitenInforme Ignacio 2Gonzalo Ignacio AguilarNoch keine Bewertungen

- Accounting Research Paper Topics 2011Dokument6 SeitenAccounting Research Paper Topics 2011cakwn75t100% (1)

- Module-01-The Accounting CycleDokument9 SeitenModule-01-The Accounting CycleJade Doel RizalteNoch keine Bewertungen

- Bbap2103 - Management Accounting 2016Dokument16 SeitenBbap2103 - Management Accounting 2016yooheechulNoch keine Bewertungen

- The Role of Management Information Systems in Decision MakingDokument18 SeitenThe Role of Management Information Systems in Decision MakingSpencer100% (1)

- Scope of Management AccountingDokument3 SeitenScope of Management AccountingMuhammad Akmal HossainNoch keine Bewertungen

- Ch01 Ch02 PT Bea SpdfsDokument128 SeitenCh01 Ch02 PT Bea Spdfsmaria100% (1)

- Chapter 1Dokument16 SeitenChapter 1Genanew AbebeNoch keine Bewertungen

- Cash Flow Statement ThesisDokument5 SeitenCash Flow Statement ThesisOnlinePaperWritingServiceDesMoines100% (2)

- Sia 4Dokument9 SeitenSia 4Husnia GithaaNoch keine Bewertungen

- Final Term Project 15-01-2020Dokument7 SeitenFinal Term Project 15-01-2020Muhammad Umer ButtNoch keine Bewertungen

- Management Accounting CourseworkDokument5 SeitenManagement Accounting Courseworkydzkmgajd100% (2)

- Research Paper Topics For Financial AccountingDokument7 SeitenResearch Paper Topics For Financial Accountingogisxnbnd100% (1)

- Chapter 01 - Introduction To AccountingDokument8 SeitenChapter 01 - Introduction To AccountingThorngsokhomNoch keine Bewertungen

- Unit 1 THE FIELD OF ACCOUNTINGDokument9 SeitenUnit 1 THE FIELD OF ACCOUNTINGHang NguyenNoch keine Bewertungen

- Accouting Assignment AsadDokument8 SeitenAccouting Assignment AsadMohsin Ali KhanNoch keine Bewertungen

- BUSN 2nd Edition Kelly Solutions Manual 1Dokument3 SeitenBUSN 2nd Edition Kelly Solutions Manual 1sandra100% (34)

- Accounting TheoryDokument192 SeitenAccounting TheoryABDULLAH MOHAMMEDNoch keine Bewertungen

- CH I & II-Cost and MGT Acc IDokument41 SeitenCH I & II-Cost and MGT Acc IzewdieNoch keine Bewertungen

- Chapter One Management AccountingDokument26 SeitenChapter One Management AccountingsirnateNoch keine Bewertungen

- FPA I Chapter1Dokument18 SeitenFPA I Chapter1Tewanay BesufikadNoch keine Bewertungen

- s1 Accounting InformationDokument4 Seitens1 Accounting InformationmartinNoch keine Bewertungen

- Sample Thesis Financial AnalysisDokument5 SeitenSample Thesis Financial AnalysisTye Rausch100% (2)

- Financial Statement Analysis CourseworkDokument8 SeitenFinancial Statement Analysis Courseworkpqltufajd100% (2)

- Ch1 Introduction To UK Tax System 2019Dokument11 SeitenCh1 Introduction To UK Tax System 2019frieda20093835Noch keine Bewertungen

- Developing Clear Learning Outcomes and Objectives PDFDokument6 SeitenDeveloping Clear Learning Outcomes and Objectives PDFfrieda20093835Noch keine Bewertungen

- Banana CakeDokument1 SeiteBanana Cakefrieda20093835Noch keine Bewertungen

- Chapter 1 Assessment MaterialDokument1 SeiteChapter 1 Assessment Materialfrieda20093835Noch keine Bewertungen

- MCQ On ErrorsDokument1 SeiteMCQ On Errorsfrieda20093835Noch keine Bewertungen

- Cardamom Rice Pudding Recipe PDFDokument1 SeiteCardamom Rice Pudding Recipe PDFfrieda20093835Noch keine Bewertungen

- Chapter 1: Accounting: Information For Decision MakingDokument17 SeitenChapter 1: Accounting: Information For Decision Makingfrieda20093835Noch keine Bewertungen

- What Exactly Happens To Your Brain When You MeditateDokument11 SeitenWhat Exactly Happens To Your Brain When You Meditatefrieda20093835Noch keine Bewertungen

- 01Dokument12 Seiten01priyaa03Noch keine Bewertungen

- Weekly Online Discussions Rubric Eme5050Dokument1 SeiteWeekly Online Discussions Rubric Eme5050frieda20093835Noch keine Bewertungen

- Current Value Accounting - AccountingToolsDokument3 SeitenCurrent Value Accounting - AccountingToolsfrieda20093835Noch keine Bewertungen

- IAS 16 and The Revaluation Approach - Reporting Property Plant AnDokument30 SeitenIAS 16 and The Revaluation Approach - Reporting Property Plant Anfrieda20093835Noch keine Bewertungen

- Current Cost Accounting (CCA) - Objective and EvaluationDokument36 SeitenCurrent Cost Accounting (CCA) - Objective and Evaluationfrieda20093835Noch keine Bewertungen

- 6179 22435 1 PB PDFDokument9 Seiten6179 22435 1 PB PDFJeffrey Ian M. KoNoch keine Bewertungen

- 357Dokument34 Seiten357heroe3awanNoch keine Bewertungen

- Ey The Audit Mandatory Rotation Rule The State of The ArtDokument33 SeitenEy The Audit Mandatory Rotation Rule The State of The Artfrieda20093835Noch keine Bewertungen

- Thomps 0324182813 1Dokument24 SeitenThomps 0324182813 1dehammoNoch keine Bewertungen

- 46933764Dokument33 Seiten46933764frieda20093835Noch keine Bewertungen

- KWLDokument1 SeiteKWLfrieda20093835Noch keine Bewertungen

- 01Dokument12 Seiten01priyaa03Noch keine Bewertungen

- Accounting Information Systems Implementation and Management Accounting ChangeDokument14 SeitenAccounting Information Systems Implementation and Management Accounting Changefrieda20093835Noch keine Bewertungen

- Example 1 PDFDokument1 SeiteExample 1 PDFfrieda20093835Noch keine Bewertungen

- IFRS3 Andtherevised IAS27Dokument18 SeitenIFRS3 Andtherevised IAS27lilyanamaNoch keine Bewertungen

- MCQ On ErrorsDokument1 SeiteMCQ On Errorsfrieda20093835Noch keine Bewertungen

- 6179 22435 1 PB PDFDokument9 Seiten6179 22435 1 PB PDFJeffrey Ian M. KoNoch keine Bewertungen

- 9825041Dokument48 Seiten9825041frieda20093835Noch keine Bewertungen

- Ias 38Dokument4 SeitenIas 38frieda20093835Noch keine Bewertungen

- Audit SkillsDokument36 SeitenAudit Skillsfrieda20093835Noch keine Bewertungen

- Financial Statements Study and Assessment Guide: 2013 AAT Accounting QualificationDokument13 SeitenFinancial Statements Study and Assessment Guide: 2013 AAT Accounting Qualificationfrieda20093835Noch keine Bewertungen

- MCQs PPEDokument10 SeitenMCQs PPEfrieda20093835100% (1)

- Can REIT Address Expectations of Indian Real Estate Investors?Dokument7 SeitenCan REIT Address Expectations of Indian Real Estate Investors?alim shaikhNoch keine Bewertungen

- VUL Mock Exam 1 (October 2018)Dokument12 SeitenVUL Mock Exam 1 (October 2018)Alona Villamor ChancoNoch keine Bewertungen

- Charlie Munger 10 PrinciplesDokument2 SeitenCharlie Munger 10 PrinciplesRohan Pinto100% (8)

- OutputDokument50 SeitenOutputNeha toshniwalNoch keine Bewertungen

- An Introduction To Stock & Options For The Tech Entrepreneur or Startup EmployeeDokument20 SeitenAn Introduction To Stock & Options For The Tech Entrepreneur or Startup EmployeeDavid E. Weekly97% (37)

- Grow Your Small Savings To One Crore PDFDokument12 SeitenGrow Your Small Savings To One Crore PDFqwqNoch keine Bewertungen

- 1Dokument10 Seiten1Sai Krishna DhulipallaNoch keine Bewertungen

- Peter Lynch's 25 Golden Rules For InvestingDokument3 SeitenPeter Lynch's 25 Golden Rules For InvestingSantiko LaurentNoch keine Bewertungen

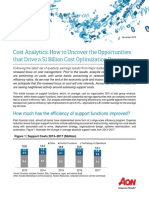

- How Much Has The Efficiency of Support Functions Improved?: Figure 1: Support Costs 2013 - 2017 ($billion)Dokument7 SeitenHow Much Has The Efficiency of Support Functions Improved?: Figure 1: Support Costs 2013 - 2017 ($billion)Mehadi HasanNoch keine Bewertungen

- PWC Emerging Trends in Real Estate 2017Dokument108 SeitenPWC Emerging Trends in Real Estate 2017TBP_Think_Tank100% (4)

- Retire On Monthly DividendsDokument15 SeitenRetire On Monthly DividendsDanaNoch keine Bewertungen

- ASF Model RMBS Representations and WarrantiesDokument21 SeitenASF Model RMBS Representations and WarrantiesModel RepsNoch keine Bewertungen

- Laurus Property Partners Company ProfileDokument4 SeitenLaurus Property Partners Company ProfileRama KarunagaranNoch keine Bewertungen

- Investment Decision and Portfolio Management (ACF 722)Dokument36 SeitenInvestment Decision and Portfolio Management (ACF 722)yebegashetNoch keine Bewertungen

- Boutique House Business Plan USADokument12 SeitenBoutique House Business Plan USAKelly McmillanNoch keine Bewertungen

- Shareholders Agreement TemplateDokument14 SeitenShareholders Agreement TemplateBernard Chung Wei Leong84% (25)

- Assignment On SebiDokument8 SeitenAssignment On SebiasthaparasarNoch keine Bewertungen

- Impact of Fii and Fdi On Indian Stock MarketDokument68 SeitenImpact of Fii and Fdi On Indian Stock Markethappysunilrana100% (12)

- Bba EntrepreneureshipDokument31 SeitenBba EntrepreneureshipKishan KhadkaNoch keine Bewertungen

- Finance Project TitlesDokument8 SeitenFinance Project TitlesArjun Mv100% (1)

- Investment Banking Course NotesDokument44 SeitenInvestment Banking Course NotesPenn CollinsNoch keine Bewertungen

- Earnings Management Are View of LiteratureDokument13 SeitenEarnings Management Are View of LiteratureLujin MukdadNoch keine Bewertungen

- Trishla VrodhiyaDokument95 SeitenTrishla VrodhiyaTrishla VirodhiyaNoch keine Bewertungen

- Solution Manual For Introduction To Corporate Finance 2nd Asia Pacific Edition by Graham For Only 59 99Dokument12 SeitenSolution Manual For Introduction To Corporate Finance 2nd Asia Pacific Edition by Graham For Only 59 99a340726614Noch keine Bewertungen

- United BrewDokument462 SeitenUnited BrewSwapnil GuravNoch keine Bewertungen

- J.M. Hurst Cyclic AnalysisDokument45 SeitenJ.M. Hurst Cyclic AnalysisChristian Robinson80% (10)

- Pert 12 Intercorporate Investments Chapter15Dokument34 SeitenPert 12 Intercorporate Investments Chapter15Chevalier ChevalierNoch keine Bewertungen

- Projects TopicsDokument116 SeitenProjects TopicsRajesh Soni0% (1)

- Thesis Performance of Mutual Funds in IndiaDokument110 SeitenThesis Performance of Mutual Funds in IndiaAnuj Kumar Singh50% (2)

- Ipo OrderDokument252 SeitenIpo Orderapi-3701467Noch keine Bewertungen