Das könnte Ihnen auch gefallen

- Ben Bernanke - Frequently Asked QuestionsDokument9 SeitenBen Bernanke - Frequently Asked QuestionsJohn SutherlandNoch keine Bewertungen

- David Dodge: The Bank of Canada and Monetary Policy: Future DirectionsDokument4 SeitenDavid Dodge: The Bank of Canada and Monetary Policy: Future DirectionsAnonymous pb0lJ4n5jNoch keine Bewertungen

- Artisan Autumn 2012Dokument6 SeitenArtisan Autumn 2012Arthur SalzerNoch keine Bewertungen

- The Outlook For Recovery in The U.S. EconomyDokument13 SeitenThe Outlook For Recovery in The U.S. EconomyZerohedgeNoch keine Bewertungen

- Globalisation, Financial Stability and EmploymentDokument10 SeitenGlobalisation, Financial Stability and EmploymentericaaliniNoch keine Bewertungen

- 2012Q3 - Newsletter October 2012 - PDF Single PageDokument4 Seiten2012Q3 - Newsletter October 2012 - PDF Single PagePacifica Partners Capital ManagementNoch keine Bewertungen

- Ben BernankeDokument9 SeitenBen BernankeManu_Bhagat_6345Noch keine Bewertungen

- Patient Capital Management IncDokument6 SeitenPatient Capital Management Incricher jpNoch keine Bewertungen

- Should We Blame Immigration For Canada's Economic WoesDokument152 SeitenShould We Blame Immigration For Canada's Economic Woesmohit01krishanNoch keine Bewertungen

- Marion Williams: The Global Financial Crisis - Can We Withstand The ShockDokument8 SeitenMarion Williams: The Global Financial Crisis - Can We Withstand The ShockRatihGizaJogjaNoch keine Bewertungen

- 8 Markets MythsDokument18 Seiten8 Markets MythsVicente Manuel Angulo GutiérrezNoch keine Bewertungen

- Janet Yell en 1110Dokument14 SeitenJanet Yell en 1110ZerohedgeNoch keine Bewertungen

- Sarthak Joshi July2022Dokument3 SeitenSarthak Joshi July2022SarthakNoch keine Bewertungen

- The Pensford Letter - 7.2.12Dokument5 SeitenThe Pensford Letter - 7.2.12Pensford FinancialNoch keine Bewertungen

- The Pensford Letter - 7.2.12Dokument5 SeitenThe Pensford Letter - 7.2.12Pensford FinancialNoch keine Bewertungen

- Canada's Federal Budget 2022Dokument304 SeitenCanada's Federal Budget 2022National PostNoch keine Bewertungen

- Debt, Profits, Canada & More .: Nvestment OmpassDokument4 SeitenDebt, Profits, Canada & More .: Nvestment OmpassPacifica Partners Capital ManagementNoch keine Bewertungen

- Hide and Seek: U.S. Economy UncertainDokument12 SeitenHide and Seek: U.S. Economy UncertainCanadianValueNoch keine Bewertungen

- Dow Closes Above 11,000 This Rally Has Ignored Fundamentals, and Will Be Corrected Painfully, Hussman SaysDokument10 SeitenDow Closes Above 11,000 This Rally Has Ignored Fundamentals, and Will Be Corrected Painfully, Hussman SaysAlbert L. PeiaNoch keine Bewertungen

- Dow Closes Above 11,000 This Rally Has Ignored Fundamentals, and Will Be Corrected Painfully, Hussman SaysDokument10 SeitenDow Closes Above 11,000 This Rally Has Ignored Fundamentals, and Will Be Corrected Painfully, Hussman SaysAlbert L. PeiaNoch keine Bewertungen

- Speech Discours EngDokument19 SeitenSpeech Discours EngJoe RaymentNoch keine Bewertungen

- Glenn Stevens: The Economic Outlook in 2002: The US Business CycleDokument8 SeitenGlenn Stevens: The Economic Outlook in 2002: The US Business CycleFlaviub23Noch keine Bewertungen

- The Pensford Letter - 7.2.12Dokument5 SeitenThe Pensford Letter - 7.2.12Pensford FinancialNoch keine Bewertungen

- Recession Full Data Report and Financial and Market Analysis DoneDokument46 SeitenRecession Full Data Report and Financial and Market Analysis Doneamitsaini03Noch keine Bewertungen

- Economic Challenges and OpportunitiesDokument3 SeitenEconomic Challenges and OpportunitiesAsif Khan ShinwariNoch keine Bewertungen

- Top Ten Investments to Beat the Crunch!: Invest Your Way to Success even in a DownturnVon EverandTop Ten Investments to Beat the Crunch!: Invest Your Way to Success even in a DownturnNoch keine Bewertungen

- World Economy Forecast 2016Dokument8 SeitenWorld Economy Forecast 2016nsbmuraliNoch keine Bewertungen

- Is There A Double Dip Recession in The Making AC - FinalDokument2 SeitenIs There A Double Dip Recession in The Making AC - FinalPremal ThakkarNoch keine Bewertungen

- The Big Question: Business ArgusDokument1 SeiteThe Big Question: Business Argusapi-120443862Noch keine Bewertungen

- RecessionDokument20 SeitenRecessionTejas WaghuldeNoch keine Bewertungen

- September 2012 NewsletterDokument2 SeitenSeptember 2012 NewslettermcphailandpartnersNoch keine Bewertungen

- Current Issue in Canadian Business EnvironmentDokument13 SeitenCurrent Issue in Canadian Business EnvironmentChris KabilingNoch keine Bewertungen

- Eagle Capital Management, LLC: April 2010Dokument3 SeitenEagle Capital Management, LLC: April 2010azharaqNoch keine Bewertungen

- Understanding EconomicDokument4 SeitenUnderstanding Economicmustafa-ahmedNoch keine Bewertungen

- Current Issues in Financial MarketsDokument5 SeitenCurrent Issues in Financial Marketsreb_nicoleNoch keine Bewertungen

- MMB 13092010Dokument3 SeitenMMB 13092010admin866Noch keine Bewertungen

- Cash Is King: Maintain Liquidity, Build Capital, and Prepare Your Business for Every OpportunityVon EverandCash Is King: Maintain Liquidity, Build Capital, and Prepare Your Business for Every OpportunityNoch keine Bewertungen

- HHRG 112 BA00 WState JDimon 20120619Dokument4 SeitenHHRG 112 BA00 WState JDimon 20120619DinSFLANoch keine Bewertungen

- FES EEA 2023 enDokument141 SeitenFES EEA 2023 enrhodalwyNoch keine Bewertungen

- Deutsche Bank - Five Years After Subprime: Lending Trends in Europe and The USDokument2 SeitenDeutsche Bank - Five Years After Subprime: Lending Trends in Europe and The USkentselveNoch keine Bewertungen

- Transcript of 10/15/12 Speech: William Dudley, President of The Federal Reserve Bank of New YorkDokument12 SeitenTranscript of 10/15/12 Speech: William Dudley, President of The Federal Reserve Bank of New YorkLani RosalesNoch keine Bewertungen

- Cerberus LetterDokument5 SeitenCerberus Letterakiva80100% (1)

- Newsletter 1Dokument4 SeitenNewsletter 1sserifundNoch keine Bewertungen

- Our Strategy To Drive GrowthDokument36 SeitenOur Strategy To Drive GrowthjbsNoch keine Bewertungen

- Janet Yell en 0323Dokument14 SeitenJanet Yell en 0323ZerohedgeNoch keine Bewertungen

- Dollar Tree, Inc. Presents at Goldman Sachs 28th Annual Global Retailing Conference, Sep-10-2021 09 - 10 AMDokument13 SeitenDollar Tree, Inc. Presents at Goldman Sachs 28th Annual Global Retailing Conference, Sep-10-2021 09 - 10 AMRaghav MittalNoch keine Bewertungen

- A DECADE OF SQUANDERED OPPORTUNITY by JM MinorDokument55 SeitenA DECADE OF SQUANDERED OPPORTUNITY by JM MinorDesmond Sullivan100% (1)

- Summer ForecastDokument2 SeitenSummer Forecastkatdoerr17Noch keine Bewertungen

- July 222010 PostsDokument107 SeitenJuly 222010 PostsAlbert L. PeiaNoch keine Bewertungen

- Marking The 11th Hour - Corona Associates Capital Management - Year End Investment Letter - December 24th 2015Dokument13 SeitenMarking The 11th Hour - Corona Associates Capital Management - Year End Investment Letter - December 24th 2015Julian ScurciNoch keine Bewertungen

- Why Would It Be Useful To Examine A Country's Balance-Of-Payments Data?Dokument2 SeitenWhy Would It Be Useful To Examine A Country's Balance-Of-Payments Data?Picasales, Frenzy M.Noch keine Bewertungen

- Picton MahoneyDokument3 SeitenPicton Mahoneyderailedcapitalism.comNoch keine Bewertungen

- Prepare The Following Based On This Topic: Inflation and Juan Dela Cruz. Statement of The ProblemDokument4 SeitenPrepare The Following Based On This Topic: Inflation and Juan Dela Cruz. Statement of The ProblemFrencis A. EsquierdoNoch keine Bewertungen

- September 22, 2010 PostsDokument543 SeitenSeptember 22, 2010 PostsAlbert L. PeiaNoch keine Bewertungen

- Made in America 2.0: 10 Big Ideas for Saving the United States of America from Economic DisasterVon EverandMade in America 2.0: 10 Big Ideas for Saving the United States of America from Economic DisasterNoch keine Bewertungen

- The Economi of Success: Twelve Things Politicians Don't Want You to KnowVon EverandThe Economi of Success: Twelve Things Politicians Don't Want You to KnowNoch keine Bewertungen

- Acknowled Gement: Impact of Recent Recession On India and UsDokument60 SeitenAcknowled Gement: Impact of Recent Recession On India and Uskashifsecret9003Noch keine Bewertungen

- Myanmar: Rice ExportDokument88 SeitenMyanmar: Rice Exportericaalini100% (1)

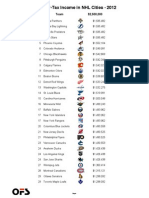

- Net After-Tax Income in NHL Cities - 2013: Team $2,500,000Dokument2 SeitenNet After-Tax Income in NHL Cities - 2013: Team $2,500,000ericaaliniNoch keine Bewertungen

- NHL 2013-2012Dokument1 SeiteNHL 2013-2012ericaaliniNoch keine Bewertungen

- NHL 2013-2012Dokument1 SeiteNHL 2013-2012ericaaliniNoch keine Bewertungen

- NHL 2012Dokument1 SeiteNHL 2012ericaaliniNoch keine Bewertungen

- Speech From The ThroneDokument24 SeitenSpeech From The ThroneCPAC TV0% (1)

- Globalisation, Financial Stability and EmploymentDokument10 SeitenGlobalisation, Financial Stability and EmploymentericaaliniNoch keine Bewertungen

- DramaturgyDokument4 SeitenDramaturgyThirumalaiappan MuthukumaraswamyNoch keine Bewertungen

- Ciplaqcil Qcil ProfileDokument8 SeitenCiplaqcil Qcil ProfileJohn R. MungeNoch keine Bewertungen

- Odysseus JourneyDokument8 SeitenOdysseus JourneyDrey MartinezNoch keine Bewertungen

- Region 12Dokument75 SeitenRegion 12Jezreel DucsaNoch keine Bewertungen

- Greek Mythology ReviewerDokument12 SeitenGreek Mythology ReviewerSyra JasmineNoch keine Bewertungen

- ACR Format Assisstant and ClerkDokument3 SeitenACR Format Assisstant and ClerkJalil badnasebNoch keine Bewertungen

- Implications - CSR Practices in Food and Beverage Companies During PandemicDokument9 SeitenImplications - CSR Practices in Food and Beverage Companies During PandemicMy TranNoch keine Bewertungen

- ECONOMÍA UNIT 5 NDokument6 SeitenECONOMÍA UNIT 5 NANDREA SERRANO GARCÍANoch keine Bewertungen

- Binder PI T4 Weber July 2017Dokument63 SeitenBinder PI T4 Weber July 2017Nilesh GaikwadNoch keine Bewertungen

- Project Initiation Document (Pid) : PurposeDokument17 SeitenProject Initiation Document (Pid) : PurposelucozzadeNoch keine Bewertungen

- UntitledDokument9 SeitenUntitledRexi Chynna Maning - AlcalaNoch keine Bewertungen

- Risk AssessmentDokument11 SeitenRisk AssessmentRutha KidaneNoch keine Bewertungen

- Donralph Media Concept LimitedDokument1 SeiteDonralph Media Concept LimitedDonRalph DMGNoch keine Bewertungen

- He Hard Truth - If You Do Not Become A BRAND Then: Examples Oprah WinfreyDokument11 SeitenHe Hard Truth - If You Do Not Become A BRAND Then: Examples Oprah WinfreyAbd.Khaliq RahimNoch keine Bewertungen

- Development of Modern International Law and India R.P.anandDokument77 SeitenDevelopment of Modern International Law and India R.P.anandVeeramani ManiNoch keine Bewertungen

- The Lightworker's HandbookDokument58 SeitenThe Lightworker's HandbookEvgeniq Marcenkova100% (9)

- Nurlilis (Tgs. Bhs - Inggris. Chapter 4)Dokument5 SeitenNurlilis (Tgs. Bhs - Inggris. Chapter 4)Latifa Hanafi100% (1)

- The New Rich in AsiaDokument31 SeitenThe New Rich in AsiaIrdinaNoch keine Bewertungen

- Uboot Rulebook v1.1 EN PDFDokument52 SeitenUboot Rulebook v1.1 EN PDFUnai GomezNoch keine Bewertungen

- Aims of The Big Three'Dokument10 SeitenAims of The Big Three'SafaNoch keine Bewertungen

- E Commerce AssignmentDokument40 SeitenE Commerce AssignmentHaseeb Khan100% (3)

- Case2-Forbidden CItyDokument10 SeitenCase2-Forbidden CItyqzbtbq7y6dNoch keine Bewertungen

- Term Paper Air PollutionDokument4 SeitenTerm Paper Air Pollutionaflsnggww100% (1)

- A2 UNIT 2 Extra Grammar Practice RevisionDokument1 SeiteA2 UNIT 2 Extra Grammar Practice RevisionCarolinaNoch keine Bewertungen

- Total Gallium JB15939XXDokument18 SeitenTotal Gallium JB15939XXAsim AliNoch keine Bewertungen

- Leander Geisinger DissertationDokument7 SeitenLeander Geisinger DissertationOrderPapersOnlineUK100% (1)

- Sharmila Ghuge V StateDokument20 SeitenSharmila Ghuge V StateBar & BenchNoch keine Bewertungen

- Country in A Box ProjectDokument6 SeitenCountry in A Box Projectapi-301892404Noch keine Bewertungen

- 3 Longman Academic Writing Series 4th Edition Answer KeyDokument21 Seiten3 Longman Academic Writing Series 4th Edition Answer KeyZheer KurdishNoch keine Bewertungen

- Abhiraj's Data Comm - I ProjectDokument15 SeitenAbhiraj's Data Comm - I Projectabhirajsingh.bscllbNoch keine Bewertungen