Das könnte Ihnen auch gefallen

- Vystar StatementDokument13 SeitenVystar StatementPatsy Hilll100% (2)

- Chapter 29 PDFDokument11 SeitenChapter 29 PDFSangeetha Menon100% (1)

- PLATE BEARING TEST (Acc. DIN 18134) - Part - 1 (Field Data)Dokument2 SeitenPLATE BEARING TEST (Acc. DIN 18134) - Part - 1 (Field Data)EMANUELINoch keine Bewertungen

- Balance Statement ReportingDokument12 SeitenBalance Statement ReportingahnaflionheartNoch keine Bewertungen

- Output SPSSDokument76 SeitenOutput SPSSmuliadin_74426729Noch keine Bewertungen

- Week 11 FormulaeDokument5 SeitenWeek 11 FormulaeHarry SinghNoch keine Bewertungen

- AsdasdasdaDokument35 SeitenAsdasdasdayiesNoch keine Bewertungen

- Cash Flow Diagram ExampleDokument3 SeitenCash Flow Diagram ExampleFarid DarwishNoch keine Bewertungen

- Aggregate Sample Project: Click Cell G1 To Edit TitleDokument13 SeitenAggregate Sample Project: Click Cell G1 To Edit TitleHanamant HunashikattiNoch keine Bewertungen

- PFC Secpropsdimsprops Eurocode3 UK 16-11-2023Dokument8 SeitenPFC Secpropsdimsprops Eurocode3 UK 16-11-2023Zack DaveNoch keine Bewertungen

- Vie Key Indicators 2021Dokument4 SeitenVie Key Indicators 2021Nguyên NguyễnNoch keine Bewertungen

- Proyek Lokasi Material: Dynamic Cone Penetrometer Test (DCPT)Dokument4 SeitenProyek Lokasi Material: Dynamic Cone Penetrometer Test (DCPT)Ikhromul Khoirul AqshomNoch keine Bewertungen

- Aula 04 - Lista de Exercício - ResoluçãoDokument16 SeitenAula 04 - Lista de Exercício - ResoluçãoAmandaNoch keine Bewertungen

- Construction Report Project ManagementDokument7 SeitenConstruction Report Project ManagementTony ValdezNoch keine Bewertungen

- Venture Capital Journal Presentation For Iron Capital PartnersDokument8 SeitenVenture Capital Journal Presentation For Iron Capital PartnersVCJournal0% (1)

- Micro Eportfolio Monopoly Spreadsheet Data - SPG 18 - FinalDokument4 SeitenMicro Eportfolio Monopoly Spreadsheet Data - SPG 18 - Finalapi-302890540Noch keine Bewertungen

- Hertz Ω ° Ω °: Chart TitleDokument5 SeitenHertz Ω ° Ω °: Chart Title31flipyNoch keine Bewertungen

- Mix DesignDokument1 SeiteMix DesignDede NurcahyadiNoch keine Bewertungen

- International Tourist ArrivalsDokument4 SeitenInternational Tourist ArrivalsPrasanth KumarNoch keine Bewertungen

- Mix Design - DLC MujaDokument3 SeitenMix Design - DLC MujaMujahid choudharyNoch keine Bewertungen

- Uji Coba CobyneDokument12 SeitenUji Coba CobyneIvan PsykoNoch keine Bewertungen

- Data Untuk Routing Waduk: Hasil PerhitunganDokument2 SeitenData Untuk Routing Waduk: Hasil PerhitunganSiti RauhunNoch keine Bewertungen

- Diseño de Mezclas AsaflticasDokument3 SeitenDiseño de Mezclas AsaflticasJoel Ariste MendozaNoch keine Bewertungen

- Libro 1Dokument6 SeitenLibro 1Adrian DosalNoch keine Bewertungen

- Intervale de Variatie Ponderea Cumulata A Debitorilor N X XNDokument4 SeitenIntervale de Variatie Ponderea Cumulata A Debitorilor N X XNLena IlicishinaNoch keine Bewertungen

- gc42 gc6 2Dokument23 Seitengc42 gc6 2Alexander P. BelkaNoch keine Bewertungen

- Hero Moto Q4FY22 Result SnapshotDokument3 SeitenHero Moto Q4FY22 Result SnapshotBaria VirenNoch keine Bewertungen

- Sesion 2. Comparativo DespachosDokument63 SeitenSesion 2. Comparativo DespachosDanny MoshNoch keine Bewertungen

- Sensitivity Analysis: Enter Base, Minimum, and Maximum Values in Input CellsDokument5 SeitenSensitivity Analysis: Enter Base, Minimum, and Maximum Values in Input CellsSajid IqbalNoch keine Bewertungen

- PFC Secpropsdimsprops EC3UKNA UK 11 16 2023Dokument8 SeitenPFC Secpropsdimsprops EC3UKNA UK 11 16 2023Zack DaveNoch keine Bewertungen

- OK OK OK: Sieve Size, MMDokument8 SeitenOK OK OK: Sieve Size, MMAbdo AboretaNoch keine Bewertungen

- Bario Gram AsDokument16 SeitenBario Gram AsJoseph Marroquin YucraNoch keine Bewertungen

- Datos para Curvas Ifd: Curvas I.F.D ModalidadDokument4 SeitenDatos para Curvas Ifd: Curvas I.F.D ModalidadFernanda SierraNoch keine Bewertungen

- Parallel Flange Channels (PFC), Section Properties Dimensions & PropertiesDokument8 SeitenParallel Flange Channels (PFC), Section Properties Dimensions & PropertiesKevin Lekhraj HurreeramNoch keine Bewertungen

- TD Identification SolDokument4 SeitenTD Identification SolMack ClaroNoch keine Bewertungen

- Sensitivity Analysis: Enter Base, Minimum, and Maximum Values in Input CellsDokument5 SeitenSensitivity Analysis: Enter Base, Minimum, and Maximum Values in Input CellsAdeniyi AleseNoch keine Bewertungen

- Sensitivity Analysis: Enter Base, Minimum, and Maximum Values in Input CellsDokument5 SeitenSensitivity Analysis: Enter Base, Minimum, and Maximum Values in Input CellsediabcNoch keine Bewertungen

- Energy Cost Calculator Generic Power OnlyDokument5 SeitenEnergy Cost Calculator Generic Power OnlyalstomNoch keine Bewertungen

- Solution To HW 4 Problem 1Dokument2 SeitenSolution To HW 4 Problem 1ALWAYNE BUCKNORNoch keine Bewertungen

- Curva Granuometrica12121Dokument5 SeitenCurva Granuometrica12121MEGA FLASHNoch keine Bewertungen

- Grading Evelopes For GC Material - 28.5mm NomDokument2 SeitenGrading Evelopes For GC Material - 28.5mm NomAndrew MwambaNoch keine Bewertungen

- Titan Q4FY22 Result SnapshotDokument3 SeitenTitan Q4FY22 Result SnapshotBaria VirenNoch keine Bewertungen

- Air Bend Force ChartDokument2 SeitenAir Bend Force ChartOscar UscateguiNoch keine Bewertungen

- RSI:Internet:Textile, Clothing&footwear:all Bus:VAL NSA:internet Av Week Sales M Not Seasonally Adjusted Current Prices MillionDokument2 SeitenRSI:Internet:Textile, Clothing&footwear:all Bus:VAL NSA:internet Av Week Sales M Not Seasonally Adjusted Current Prices MillionPrasiddha PradhanNoch keine Bewertungen

- Conversion Velocidad de Reaccion X: Ra (Mol/m3.s)Dokument4 SeitenConversion Velocidad de Reaccion X: Ra (Mol/m3.s)KevinMendietaNoch keine Bewertungen

- SMADokument1 SeiteSMAvarun persadNoch keine Bewertungen

- Dynamic, Absolute and Kinematic Viscosity Fluid Density: - 3 2 - 1 2 - 6 2 2 - 4 2 1) o o o oDokument1 SeiteDynamic, Absolute and Kinematic Viscosity Fluid Density: - 3 2 - 1 2 - 6 2 2 - 4 2 1) o o o osrNoch keine Bewertungen

- Tarea E L-LDokument4 SeitenTarea E L-LRoco neluNoch keine Bewertungen

- Earthwork For Proposed RoadDokument4 SeitenEarthwork For Proposed RoadAh RashedNoch keine Bewertungen

- Stadium at Magadh University Bodh Gaya 200109ADokument2 SeitenStadium at Magadh University Bodh Gaya 200109APranabesh SenNoch keine Bewertungen

- Matriz de Tasas de Interes para CDT (Karol Sanchez)Dokument6 SeitenMatriz de Tasas de Interes para CDT (Karol Sanchez)Väłërï PërïlläNoch keine Bewertungen

- 1 HW1 FinishedDokument5 Seiten1 HW1 Finishedheckwithit9Noch keine Bewertungen

- Tromp Value: Feed % Pass Fines % Pass Dim. Rejects % PassDokument5 SeitenTromp Value: Feed % Pass Fines % Pass Dim. Rejects % PassThaigroup CementNoch keine Bewertungen

- OS GradingDokument38 SeitenOS GradingNico TorresNoch keine Bewertungen

- FV 1000 1 2 3 C 10% Fvofcf E.Y. 10% PV OF CF 90.909090909 82.6446281 826.446281 T 3 Price FV C E.Y. T Price FV C E.Y. T PriceDokument10 SeitenFV 1000 1 2 3 C 10% Fvofcf E.Y. 10% PV OF CF 90.909090909 82.6446281 826.446281 T 3 Price FV C E.Y. T Price FV C E.Y. T PriceMayank GuptaNoch keine Bewertungen

- TEST METHOD:AASHTO T127, ASTM C136 (Dry) ASTM C117 Procedure A (Wet), BS 812 PART 103Dokument8 SeitenTEST METHOD:AASHTO T127, ASTM C136 (Dry) ASTM C117 Procedure A (Wet), BS 812 PART 103Mubashar Islam JadoonNoch keine Bewertungen

- Carry RolloverDokument12 SeitenCarry RolloverKoushik SenNoch keine Bewertungen

- 3 LabuanDokument30 Seiten3 LabuanAiman Ariffin NordinNoch keine Bewertungen

- Chapter Four 4. Data Analysis and PresentationDokument14 SeitenChapter Four 4. Data Analysis and PresentationAbdurohmanNoch keine Bewertungen

- 1.ley de Atenuacion RP92442 (RNG)Dokument31 Seiten1.ley de Atenuacion RP92442 (RNG)cristian MuñozNoch keine Bewertungen

- Analisa SaringanDokument2 SeitenAnalisa SaringanNP Project Music26Noch keine Bewertungen

- Government Publications: Key PapersVon EverandGovernment Publications: Key PapersBernard M. FryNoch keine Bewertungen

- Math Practice Simplified: Decimals & Percents (Book H): Practicing the Concepts of Decimals and PercentagesVon EverandMath Practice Simplified: Decimals & Percents (Book H): Practicing the Concepts of Decimals and PercentagesBewertung: 5 von 5 Sternen5/5 (3)

- NYU 2009 RushmoreDokument30 SeitenNYU 2009 RushmoreJim Butler100% (7)

- Lender Alternatives For Troubled Hotel LoansDokument8 SeitenLender Alternatives For Troubled Hotel LoansJim Butler100% (4)

- MTM 2009 Mark Lomanno STR 5-6-09Dokument35 SeitenMTM 2009 Mark Lomanno STR 5-6-09Jim Butler100% (1)

- Hospitality Attorney With Pearls From NYU - Smith Travel Research NYU 2008Dokument39 SeitenHospitality Attorney With Pearls From NYU - Smith Travel Research NYU 2008Jim Butler100% (2)

- Hospitality Lawyer On Green Hotel Development at Hotel Developers Conference - Dan EstyDokument21 SeitenHospitality Lawyer On Green Hotel Development at Hotel Developers Conference - Dan EstyJim ButlerNoch keine Bewertungen

- Hospitality Attorney - What Makes The Orchard Garden Inn A LEED Certified Hotel?Dokument7 SeitenHospitality Attorney - What Makes The Orchard Garden Inn A LEED Certified Hotel?Jim Butler100% (2)

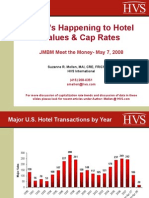

- What's Happening To Hotel Values & Cap RatesDokument23 SeitenWhat's Happening To Hotel Values & Cap RatesJustia Inc.100% (1)

- Hospitality Lawyer On Hotel of Tomorrow (H.O.T.) by Ron Swidler at JMBM's MTM 2008Dokument95 SeitenHospitality Lawyer On Hotel of Tomorrow (H.O.T.) by Ron Swidler at JMBM's MTM 2008Jim Butler100% (1)

- Guidelines For Local SubsidyDokument31 SeitenGuidelines For Local SubsidynesijaycoNoch keine Bewertungen

- Annual Report 2007-2008 (ENG) - 20100603063436Dokument89 SeitenAnnual Report 2007-2008 (ENG) - 20100603063436Rakshya ShresthaNoch keine Bewertungen

- Composition of Cash and Cash EquivalentDokument20 SeitenComposition of Cash and Cash EquivalentYenelyn Apistar CambarijanNoch keine Bewertungen

- Boughton James. Porqué White y No Keynes. 25 Páginas InglésDokument25 SeitenBoughton James. Porqué White y No Keynes. 25 Páginas InglésKaro GutierrezNoch keine Bewertungen

- BiiiimplmoniwbDokument34 SeitenBiiiimplmoniwbShruti DubeyNoch keine Bewertungen

- Funds TypesDokument28 SeitenFunds TypesYna AltoverosNoch keine Bewertungen

- Lecture 3Dokument25 SeitenLecture 3Balu BhsNoch keine Bewertungen

- 978 613 9 45336 8Dokument325 Seiten978 613 9 45336 8drmadhav kothapalliNoch keine Bewertungen

- Contribution Midterm Answers and SolutionsDokument10 SeitenContribution Midterm Answers and SolutionsKimNoch keine Bewertungen

- Bank Marketing 1Dokument69 SeitenBank Marketing 1nirosha_398272247Noch keine Bewertungen

- NFCC - Oclp TemplateDokument1 SeiteNFCC - Oclp TemplateFranz Xavier GarciaNoch keine Bewertungen

- An Case Study On Exley Chemical CompanyDokument12 SeitenAn Case Study On Exley Chemical CompanyChristian JimmyNoch keine Bewertungen

- EconomicsDokument12 SeitenEconomicsASMARA HABIBNoch keine Bewertungen

- FINA1094 - 2020 - MAY - EXAM - Approved - TAKE HOME EXAMDokument5 SeitenFINA1094 - 2020 - MAY - EXAM - Approved - TAKE HOME EXAMShehry VibesNoch keine Bewertungen

- Survey of Accounting 4th Edition Edmonds Solutions ManualDokument62 SeitenSurvey of Accounting 4th Edition Edmonds Solutions Manualdariusarnoldvin100% (29)

- IM in ENSC-20093-ENGINEERING-ECONOMICS-TAPAT #CeaDokument73 SeitenIM in ENSC-20093-ENGINEERING-ECONOMICS-TAPAT #CeaAHSTERINoch keine Bewertungen

- Presented By:-: Shreya.RDokument14 SeitenPresented By:-: Shreya.RAkash ChoudharyNoch keine Bewertungen

- BSc2 Principles of Banking and Finance 2021-22Dokument8 SeitenBSc2 Principles of Banking and Finance 2021-22loNoch keine Bewertungen

- 00000785-CURRENT ACCOUNT - I-4129-Feb-19Dokument2 Seiten00000785-CURRENT ACCOUNT - I-4129-Feb-19AUTO online VTONoch keine Bewertungen

- 1519 Loza, JesusDokument17 Seiten1519 Loza, JesusIsabella Kings100% (1)

- Boi and HDFCDokument24 SeitenBoi and HDFCDharmikNoch keine Bewertungen

- Study Guide - Chapter 3 - Issuance of Shares and Loan CapitalDokument23 SeitenStudy Guide - Chapter 3 - Issuance of Shares and Loan CapitalHappy PillsNoch keine Bewertungen

- Transaction Date Narration Cheque / Ref No. Value Date Withdra Wal (DR) Deposit (CR) BalanceDokument27 SeitenTransaction Date Narration Cheque / Ref No. Value Date Withdra Wal (DR) Deposit (CR) BalancePravin kumar aenamNoch keine Bewertungen

- Rate of Return Analysis: Single Alternative: Gra W HillDokument99 SeitenRate of Return Analysis: Single Alternative: Gra W HillalfaselNoch keine Bewertungen

- Kerala Water Authority: Office of The Executive EngineerDokument32 SeitenKerala Water Authority: Office of The Executive EngineerKkrkollam KrishnaKumarNoch keine Bewertungen

- CH 16 Hull Fundamentals 8 The DDokument28 SeitenCH 16 Hull Fundamentals 8 The DHarsh JaiswalNoch keine Bewertungen

- Effective Interest Rate CalculatorDokument2 SeitenEffective Interest Rate CalculatormmahaliNoch keine Bewertungen