Das könnte Ihnen auch gefallen

- Tax Remedies Comparison NIRC, TCC, Local Tax, Real Property TaxDokument3 SeitenTax Remedies Comparison NIRC, TCC, Local Tax, Real Property Taxares_aguilarNoch keine Bewertungen

- Remedies of Taxpayer Contesting Amount For Local Taxes, Fees, and Charges: A. AdministrativeDokument2 SeitenRemedies of Taxpayer Contesting Amount For Local Taxes, Fees, and Charges: A. AdministrativeJose Emmanuel DolorNoch keine Bewertungen

- Tax Remedies of Government and Tax PayersDokument3 SeitenTax Remedies of Government and Tax PayersHanah Grace DelfinNoch keine Bewertungen

- Two-year prescriptive period and 120+30 day rule for filing administrative and judicial claims for tax refunds or creditsDokument3 SeitenTwo-year prescriptive period and 120+30 day rule for filing administrative and judicial claims for tax refunds or creditsBeryl Joyce BarbaNoch keine Bewertungen

- Shall Have The Authority To Grant An Injunction To Restrain The Collection of Any National Internal Revenue Tax, Fee or Charge Imposed by This CodeDokument10 SeitenShall Have The Authority To Grant An Injunction To Restrain The Collection of Any National Internal Revenue Tax, Fee or Charge Imposed by This CodeSusannie AcainNoch keine Bewertungen

- TAX 2 REVIEW - REMEDIESDokument24 SeitenTAX 2 REVIEW - REMEDIESManuel VillanuevaNoch keine Bewertungen

- LTZ 2 Tax Law 1 Discussion Guide 2. Sept 2022Dokument15 SeitenLTZ 2 Tax Law 1 Discussion Guide 2. Sept 2022Bestie BushNoch keine Bewertungen

- Cristina Olarita Tax Cases 105-113Dokument6 SeitenCristina Olarita Tax Cases 105-113Maraipol Trading Corp.Noch keine Bewertungen

- TAX REMEDIES UNDER THE NIRCDokument5 SeitenTAX REMEDIES UNDER THE NIRCjonahNoch keine Bewertungen

- Tax RemediesDokument10 SeitenTax RemediesBryan CatungalNoch keine Bewertungen

- Nueva Ecija II Electric Cooperative Inc.20220913-11-H8h0weDokument3 SeitenNueva Ecija II Electric Cooperative Inc.20220913-11-H8h0weReynaldo GasparNoch keine Bewertungen

- Remedies in General As Per Tax Code Sec. 202-204Dokument3 SeitenRemedies in General As Per Tax Code Sec. 202-2042022107419Noch keine Bewertungen

- Taxation II ReportDokument6 SeitenTaxation II ReportKrishianne LabianoNoch keine Bewertungen

- A. Assessment B. Collection: Remedies of The GovernmentDokument10 SeitenA. Assessment B. Collection: Remedies of The GovernmentGianna CantoriaNoch keine Bewertungen

- RemediesDokument3 SeitenRemediesDesiree Ann MiralNoch keine Bewertungen

- 2016 P T D (Trib - PDF 6Dokument21 Seiten2016 P T D (Trib - PDF 6Ali WaqarNoch keine Bewertungen

- Lascona Land Co., Inc. v. CIRDokument2 SeitenLascona Land Co., Inc. v. CIRAron Lobo100% (1)

- Tax Cases 2Dokument8 SeitenTax Cases 2Jerald-Edz Tam AbonNoch keine Bewertungen

- Concept of Assessment Requisites For A Valid Assessment: 10 Years After DiscoveryDokument5 SeitenConcept of Assessment Requisites For A Valid Assessment: 10 Years After DiscoveryJD BarcellanoNoch keine Bewertungen

- CTA Case Decision on Sual Construction Corp Claim for Refund of P53M Withholding TaxesDokument10 SeitenCTA Case Decision on Sual Construction Corp Claim for Refund of P53M Withholding TaxesghilphilNoch keine Bewertungen

- Lascona Land Co. Inc. vs. Commission of Internal Revenue: FactsDokument4 SeitenLascona Land Co. Inc. vs. Commission of Internal Revenue: FactsJoVic2020Noch keine Bewertungen

- Lascona Land Co. Inc. vs. Commission of Internal Revenue: FactsDokument4 SeitenLascona Land Co. Inc. vs. Commission of Internal Revenue: FactsJoVic2020Noch keine Bewertungen

- Taxation-2-Power-Point-part-2Dokument32 SeitenTaxation-2-Power-Point-part-2Vince Q. MatutinaNoch keine Bewertungen

- Taxpayer's RemediesDokument5 SeitenTaxpayer's RemediesCel TanNoch keine Bewertungen

- Module 6 Tax Remedies ReviewerDokument11 SeitenModule 6 Tax Remedies ReviewerburgerpattygirlNoch keine Bewertungen

- Taxpayer Remedies for Real Property Tax AppealsDokument25 SeitenTaxpayer Remedies for Real Property Tax AppealsJohn Michael VidaNoch keine Bewertungen

- Qeourt: L/epublir of Tbe TlbilippinesDokument7 SeitenQeourt: L/epublir of Tbe TlbilippineswewNoch keine Bewertungen

- REMEDIESDokument9 SeitenREMEDIESkathlenejane.garciaNoch keine Bewertungen

- CBDT Issued New Guidelines For Compounding of Income Tax Offences - Taxguru - inDokument22 SeitenCBDT Issued New Guidelines For Compounding of Income Tax Offences - Taxguru - inveer_bcaNoch keine Bewertungen

- Tax Remedies of The Taxpayer PDFDokument4 SeitenTax Remedies of The Taxpayer PDFJester LimNoch keine Bewertungen

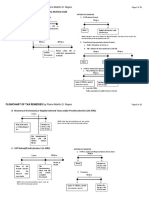

- Flowchart of Tax Remedies I. Remedies UnDokument12 SeitenFlowchart of Tax Remedies I. Remedies UnKevin Ken Sison Ganchero100% (2)

- Mindanao I Geothermal Partnership vs. Commissioner of Internal Revenue, 844 SCRA 386, November 08, 2017Dokument12 SeitenMindanao I Geothermal Partnership vs. Commissioner of Internal Revenue, 844 SCRA 386, November 08, 2017Vida MarieNoch keine Bewertungen

- ProsecutionDokument12 SeitenProsecutionKomal JaiswalNoch keine Bewertungen

- Republic of The Philippines of Tax Quezon: Court Appeals CityDokument15 SeitenRepublic of The Philippines of Tax Quezon: Court Appeals CityElvin LouieNoch keine Bewertungen

- Digests 2Dokument17 SeitenDigests 2Henry LNoch keine Bewertungen

- Doctrines in Taxation: Prospectivity and ImprescriptibilityDokument14 SeitenDoctrines in Taxation: Prospectivity and Imprescriptibilityjuna luz latigayNoch keine Bewertungen

- The Sigma Rho Fraternity: Commissioner of Internal Revenue v. St. Luke's (GR No. 195909)Dokument10 SeitenThe Sigma Rho Fraternity: Commissioner of Internal Revenue v. St. Luke's (GR No. 195909)Daryl DumayasNoch keine Bewertungen

- TITLE VIII REMEDIESDokument2 SeitenTITLE VIII REMEDIESAira kaye BernardinoNoch keine Bewertungen

- DIGEST - Sitel Philippines Corp. v. CIRDokument3 SeitenDIGEST - Sitel Philippines Corp. v. CIRAgatha ApolinarioNoch keine Bewertungen

- DIGEST - Sitel Philippines Corp. v. CIRDokument3 SeitenDIGEST - Sitel Philippines Corp. v. CIRAgatha ApolinarioNoch keine Bewertungen

- CTA resolves motion on jurisdiction in VAT refund caseDokument6 SeitenCTA resolves motion on jurisdiction in VAT refund caseReina Noreen IgnacioNoch keine Bewertungen

- Respondent Prescriptive Period of Assessment - General Rule (Sec. 203) (Rationale & Interpretation)Dokument5 SeitenRespondent Prescriptive Period of Assessment - General Rule (Sec. 203) (Rationale & Interpretation)Joshua Erik MadriaNoch keine Bewertungen

- Finals Personal Study Guide Tax2Dokument116 SeitenFinals Personal Study Guide Tax2TeacherEliNoch keine Bewertungen

- Tax Chair - S DigestsDokument18 SeitenTax Chair - S Digestsruth sab-itNoch keine Bewertungen

- GSTDokument193 SeitenGSTdevikrish897Noch keine Bewertungen

- Chapter 1 To 4Dokument27 SeitenChapter 1 To 4Karla Barbacena100% (1)

- TaxationBarQ26A TaxRemediesDokument32 SeitenTaxationBarQ26A TaxRemediesjuneson agustinNoch keine Bewertungen

- Report On Sec 220 To 227 of NIRCDokument29 SeitenReport On Sec 220 To 227 of NIRCAnonymous VRuxJ3IgNoch keine Bewertungen

- CTA Ruling on Prescription of Tax AssessmentDokument7 SeitenCTA Ruling on Prescription of Tax AssessmentEric TamayoNoch keine Bewertungen

- Remedies Under The Tax Code of 1997Dokument7 SeitenRemedies Under The Tax Code of 1997mnyngNoch keine Bewertungen

- Chapter 3Dokument61 SeitenChapter 3Allaiza Mhel Arcenal EusebioNoch keine Bewertungen

- Week 3: Tax Administration IIDokument32 SeitenWeek 3: Tax Administration IIElmeerajh JudavarNoch keine Bewertungen

- Labor LawDokument29 SeitenLabor LawmissyaliNoch keine Bewertungen

- An Overview of Compulsory Strata Management Law in NSW: Michael Pobi, Pobi LawyersVon EverandAn Overview of Compulsory Strata Management Law in NSW: Michael Pobi, Pobi LawyersNoch keine Bewertungen

- Bar Review Companion: Taxation: Anvil Law Books Series, #4Von EverandBar Review Companion: Taxation: Anvil Law Books Series, #4Noch keine Bewertungen

- Computerised Accounting Practice Set Using Xero Online Accounting: Australian EditionVon EverandComputerised Accounting Practice Set Using Xero Online Accounting: Australian EditionNoch keine Bewertungen

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionVon EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNoch keine Bewertungen

- BIR Ruling No. 47-1980Dokument2 SeitenBIR Ruling No. 47-1980Stacy Liong BloggerAccountNoch keine Bewertungen

- COA Cir No. 2009-001-Submission of Pos, ContractsDokument28 SeitenCOA Cir No. 2009-001-Submission of Pos, Contractscrizalde de dios100% (1)

- RA7900 High CropsDokument6 SeitenRA7900 High CropsStacy Liong BloggerAccountNoch keine Bewertungen

- Making Constitutional SenseDokument31 SeitenMaking Constitutional SenseStacy Liong BloggerAccountNoch keine Bewertungen

- SSRN Id3460962Dokument79 SeitenSSRN Id3460962Stacy Liong BloggerAccountNoch keine Bewertungen

- Comparative Law in The Modalities of Constitutional ArgumentDokument32 SeitenComparative Law in The Modalities of Constitutional ArgumentStacy Liong BloggerAccountNoch keine Bewertungen

- BIR Ruling No. 3-1973Dokument2 SeitenBIR Ruling No. 3-1973Stacy Liong BloggerAccountNoch keine Bewertungen

- The Constitutional Canon as Argumentative Metonymy: How Canonical Cases are Used to Represent Broader Constitutional PrinciplesDokument69 SeitenThe Constitutional Canon as Argumentative Metonymy: How Canonical Cases are Used to Represent Broader Constitutional PrinciplesStacy Liong BloggerAccountNoch keine Bewertungen

- Bir Ruling (Da-031-07)Dokument2 SeitenBir Ruling (Da-031-07)Stacy Liong BloggerAccountNoch keine Bewertungen

- Republic Act No. 7227Dokument13 SeitenRepublic Act No. 7227Stacy Liong BloggerAccountNoch keine Bewertungen

- Bir Ruling No. 098-A-98Dokument2 SeitenBir Ruling No. 098-A-98Stacy Liong BloggerAccountNoch keine Bewertungen

- BIR Ruling on Exemption from IAET for PEZA-Registered FirmDokument3 SeitenBIR Ruling on Exemption from IAET for PEZA-Registered FirmStacy Liong BloggerAccountNoch keine Bewertungen

- Implementing Presidential Decree No. 1671 on Gasoline Dealers TaxDokument3 SeitenImplementing Presidential Decree No. 1671 on Gasoline Dealers TaxStacy Liong BloggerAccountNoch keine Bewertungen

- Pathetic Argument in Constitutional LawDokument95 SeitenPathetic Argument in Constitutional LawStacy Liong BloggerAccountNoch keine Bewertungen

- Bir Ruling (Da 089 97)Dokument2 SeitenBir Ruling (Da 089 97)Stacy Liong BloggerAccountNoch keine Bewertungen

- Bir Ruling (Da - (Il-041) 742-09)Dokument2 SeitenBir Ruling (Da - (Il-041) 742-09)Stacy Liong BloggerAccountNoch keine Bewertungen

- Political+Law+Review+ (Jimenez) +2011 2012Dokument349 SeitenPolitical+Law+Review+ (Jimenez) +2011 2012Miel StarrNoch keine Bewertungen

- California Pizza Kitchen MenuDokument24 SeitenCalifornia Pizza Kitchen MenuStacy Liong BloggerAccountNoch keine Bewertungen

- Proper execution of tax waiverDokument2 SeitenProper execution of tax waiverStacy Liong BloggerAccountNoch keine Bewertungen

- BIR Memo On Taxation On Social Media Influencers IncomeDokument10 SeitenBIR Memo On Taxation On Social Media Influencers IncomeAlora Uy GuerreroNoch keine Bewertungen

- Mabuhay Palace (New A La Carte Menu)Dokument9 SeitenMabuhay Palace (New A La Carte Menu)Stacy Liong BloggerAccountNoch keine Bewertungen

- The Food Photography Book SAMPLE RecipeTin EatsDokument17 SeitenThe Food Photography Book SAMPLE RecipeTin EatsStacy Liong BloggerAccount80% (5)

- Bail Bond Guide PhilippinesDokument100 SeitenBail Bond Guide PhilippinesSakuraCardCaptor60% (5)

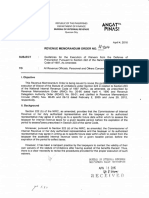

- RMONo14 2016Dokument3 SeitenRMONo14 2016Yan Rodriguez DasalNoch keine Bewertungen

- Bar 2016 PDFDokument31 SeitenBar 2016 PDFGlenn Mark Frejas RinionNoch keine Bewertungen

- Civ Pro FlowchartDokument1 SeiteCiv Pro FlowchartStacy Liong BloggerAccountNoch keine Bewertungen

- 2 R1 BRulebookDokument25 Seiten2 R1 BRulebookRichie ChanNoch keine Bewertungen

- Advanced Character Cards: Blue TeamDokument51 SeitenAdvanced Character Cards: Blue TeamStacy Liong BloggerAccount100% (1)

- Suggested Answer To 2014 Bar Exam CriminallawDokument13 SeitenSuggested Answer To 2014 Bar Exam CriminallawMyn Mirafuentes Sta Ana100% (1)

- RecipeDokument1 SeiteRecipeStacy Liong BloggerAccountNoch keine Bewertungen