Das könnte Ihnen auch gefallen

- PESTEL Analysis AssignmentDokument4 SeitenPESTEL Analysis AssignmentLeza smithNoch keine Bewertungen

- Financial Statement 31 December 2014Dokument52 SeitenFinancial Statement 31 December 2014Riyas KalpettaNoch keine Bewertungen

- AlmaraiDokument4 SeitenAlmaraiShruthiJangitiNoch keine Bewertungen

- Strategic Operations IssuesDokument20 SeitenStrategic Operations IssuesMichael YuleNoch keine Bewertungen

- FINANCIAL ANALYSIS FOR MANAGERSDokument40 SeitenFINANCIAL ANALYSIS FOR MANAGERSSumant KhetanNoch keine Bewertungen

- 2.5.3 Zenith Bank PLC HistoryDokument3 Seiten2.5.3 Zenith Bank PLC HistoryOyeleye TofunmiNoch keine Bewertungen

- Internship Saudi Pak Investment CompanyDokument39 SeitenInternship Saudi Pak Investment Companyikhan5100% (2)

- Assignment ECGDokument13 SeitenAssignment ECGsaitteyNoch keine Bewertungen

- Supply Chain Management Assignement On Green Supply ChainDokument10 SeitenSupply Chain Management Assignement On Green Supply ChainL-a DerricksNoch keine Bewertungen

- Financial Analysis For Eastman KodakDokument4 SeitenFinancial Analysis For Eastman KodakJacquelyn AlegriaNoch keine Bewertungen

- Financial Analysis in Mergers AcquisitionsDokument27 SeitenFinancial Analysis in Mergers AcquisitionsJas KainthNoch keine Bewertungen

- Managing Corporate Responsibility in The Wider Business EnvironmentDokument2 SeitenManaging Corporate Responsibility in The Wider Business EnvironmentUnknwn NouwnNoch keine Bewertungen

- Assignment On Mercantile Bank Limited, Dhaka, Bangladesh.Dokument6 SeitenAssignment On Mercantile Bank Limited, Dhaka, Bangladesh.নিশীথিনী কুহুরানীNoch keine Bewertungen

- 2018 UK Corporate Governance Code FINAL PDFDokument20 Seiten2018 UK Corporate Governance Code FINAL PDFMichał TomczykNoch keine Bewertungen

- Abbott Financial Report Analysis 2012Dokument85 SeitenAbbott Financial Report Analysis 2012Muhammad Zubair50% (2)

- BSc Business Administration Integrating ManagementDokument1 SeiteBSc Business Administration Integrating ManagementShaikh Ghassan AbidNoch keine Bewertungen

- Internet MarketingDokument5 SeitenInternet MarketingAssignmentLab.comNoch keine Bewertungen

- Supply Chain Management in Health Servic PDFDokument7 SeitenSupply Chain Management in Health Servic PDFSa Be MirNoch keine Bewertungen

- ESSENTIAL ELEMENTS OF A VALID CONTRACTDokument21 SeitenESSENTIAL ELEMENTS OF A VALID CONTRACTMegha NadhNoch keine Bewertungen

- #@$ Finance Investing The Islamic Way Verdell WalkerDokument194 Seiten#@$ Finance Investing The Islamic Way Verdell WalkerIcas PhilsNoch keine Bewertungen

- Supply Chain Drivers ObstaclesDokument22 SeitenSupply Chain Drivers ObstaclesRikudo Akyoshi0% (1)

- Human Resource Management - AssignmentDokument16 SeitenHuman Resource Management - AssignmentLazy FrogNoch keine Bewertungen

- Leadership AssignmentDokument12 SeitenLeadership AssignmentFoad AhmedNoch keine Bewertungen

- Final Report - International Marketing: Institute of Management Technology Nagpur Trimester V / PGDM (2008-10) / IMDokument6 SeitenFinal Report - International Marketing: Institute of Management Technology Nagpur Trimester V / PGDM (2008-10) / IMHemant KumarNoch keine Bewertungen

- Economics Assign Mba 9Dokument34 SeitenEconomics Assign Mba 9Dickson MdhlaloseNoch keine Bewertungen

- Assignment On AccountingDokument5 SeitenAssignment On AccountingRodney ProcopioNoch keine Bewertungen

- Leading in Organisations: Chapter SummaryDokument24 SeitenLeading in Organisations: Chapter SummaryMD FAISALNoch keine Bewertungen

- Avari Towers, Fatima Jinnah Road, Karachi 75530, Pakistan Uan: +92-21-5660100 - Fax: +92-21-5680310 Uan: +92-21-111-Avaris (282747)Dokument44 SeitenAvari Towers, Fatima Jinnah Road, Karachi 75530, Pakistan Uan: +92-21-5660100 - Fax: +92-21-5680310 Uan: +92-21-111-Avaris (282747)ocean519Noch keine Bewertungen

- Supply Chain Management of Print MediaDokument39 SeitenSupply Chain Management of Print MediaHector MoodyNoch keine Bewertungen

- Enterprise SystemsDokument11 SeitenEnterprise SystemsumairaleyNoch keine Bewertungen

- Medd's Cafe - Group Assignment DraftDokument20 SeitenMedd's Cafe - Group Assignment DraftB UNoch keine Bewertungen

- A Summer Training Project Report On Country ClubDokument64 SeitenA Summer Training Project Report On Country ClubPrabhakar GautamNoch keine Bewertungen

- International Supply Chain Management Assignment 1Dokument6 SeitenInternational Supply Chain Management Assignment 1Mudit GoelNoch keine Bewertungen

- Operations Management b2bDokument23 SeitenOperations Management b2bmsulgadleNoch keine Bewertungen

- Assignment: Strategic Financial ManagementDokument7 SeitenAssignment: Strategic Financial ManagementVinod BhaskarNoch keine Bewertungen

- Dutch Lady Malaysia's History and Organizational StructureDokument10 SeitenDutch Lady Malaysia's History and Organizational StructureKah Weii100% (1)

- H&M: The Challenges of Global Expansion and The Move To Adopt International Financial Reporting StandardsDokument6 SeitenH&M: The Challenges of Global Expansion and The Move To Adopt International Financial Reporting StandardsSami KhanNoch keine Bewertungen

- Coca-Cola's BCG MatrixDokument28 SeitenCoca-Cola's BCG MatrixDhairya Parekh100% (1)

- Assesment 1strategic Financial Management R1812D7073086Dokument17 SeitenAssesment 1strategic Financial Management R1812D7073086Oluwadare AkinyeraNoch keine Bewertungen

- Chapter 1 Supply Chain Management True/False & Multiple ChoiceDokument11 SeitenChapter 1 Supply Chain Management True/False & Multiple ChoicePunit Tilani100% (1)

- Organizational Structures Used by UK Supermarkets PDFDokument10 SeitenOrganizational Structures Used by UK Supermarkets PDFIbrahim IrshadNoch keine Bewertungen

- Limitations of Balance SheetDokument6 SeitenLimitations of Balance Sheetshoms_007Noch keine Bewertungen

- Management of Services: Key Concepts and ClassificationsDokument9 SeitenManagement of Services: Key Concepts and ClassificationsPRABHUDEVANoch keine Bewertungen

- CBCS Guidelines For B.comh Sem VI Paper No - BCH 6.1 Auditing and Corporate GovernanceDokument2 SeitenCBCS Guidelines For B.comh Sem VI Paper No - BCH 6.1 Auditing and Corporate GovernanceJoel DinicNoch keine Bewertungen

- Inventory Management in Supply ChainDokument11 SeitenInventory Management in Supply Chainparadise AngelNoch keine Bewertungen

- Operation and Supply Chain ManagementDokument22 SeitenOperation and Supply Chain ManagementTyrone WaltersNoch keine Bewertungen

- Kedai Rakyat 1Malaysia: Low-Cost Grocery InitiativeDokument12 SeitenKedai Rakyat 1Malaysia: Low-Cost Grocery InitiativeJamilah EdwardNoch keine Bewertungen

- Rainforest Seafoods Supply Chain ExcellenceDokument18 SeitenRainforest Seafoods Supply Chain ExcellenceNordia BarrettNoch keine Bewertungen

- Ob Final AssignmentDokument38 SeitenOb Final AssignmentmenonshyaminiNoch keine Bewertungen

- CorporateFraudinNigeria ATwo CaseStudyDokument10 SeitenCorporateFraudinNigeria ATwo CaseStudyonyekachukwu0% (1)

- Financial Analysis of A CompanyDokument10 SeitenFinancial Analysis of A CompanyRupesh PuriNoch keine Bewertungen

- A Study On Performance AppraisalDokument7 SeitenA Study On Performance AppraisalMohanreddy AllamNoch keine Bewertungen

- Porter's Five Forces ModelDokument3 SeitenPorter's Five Forces ModelDokte Baulu Bangkit100% (1)

- Organisations and Leadership during Covid-19: Studies using Systems Leadership TheoryVon EverandOrganisations and Leadership during Covid-19: Studies using Systems Leadership TheoryNoch keine Bewertungen

- Business Improvement Districts: An Introduction to 3 P CitizenshipVon EverandBusiness Improvement Districts: An Introduction to 3 P CitizenshipNoch keine Bewertungen

- Value Chain Management Capability A Complete Guide - 2020 EditionVon EverandValue Chain Management Capability A Complete Guide - 2020 EditionNoch keine Bewertungen

- The Human in Human ResourceVon EverandThe Human in Human ResourceNoch keine Bewertungen

- Simplex Example 3.3Dokument4 SeitenSimplex Example 3.3haznawiNoch keine Bewertungen

- MODI VAM methods transportation problems tutorialDokument10 SeitenMODI VAM methods transportation problems tutorialVivek KumarNoch keine Bewertungen

- LAW CasesDokument21 SeitenLAW CaseshaznawiNoch keine Bewertungen

- CPM Problem - Critical Path Method Questions AnsweredDokument2 SeitenCPM Problem - Critical Path Method Questions Answeredhaznawi100% (2)

- KFC Marketing Plan For PakistanDokument26 SeitenKFC Marketing Plan For PakistanReader100% (4)

- CPM Problem - Critical Path Method Questions AnsweredDokument2 SeitenCPM Problem - Critical Path Method Questions Answeredhaznawi100% (2)

- Project Plan: Critical Path Method: STEP 1: Identify The Logic NetworkDokument5 SeitenProject Plan: Critical Path Method: STEP 1: Identify The Logic Networkhaznawi100% (1)

- Asgmt StatistikDokument4 SeitenAsgmt StatistikhaznawiNoch keine Bewertungen

- 20111004120509sample Answer EBTQ3103Dokument8 Seiten20111004120509sample Answer EBTQ3103haznawiNoch keine Bewertungen

- What Make Me A M'sia1Dokument10 SeitenWhat Make Me A M'sia1haznawiNoch keine Bewertungen

- PWC Loyalty Analytics ExposedDokument13 SeitenPWC Loyalty Analytics ExposedUmang GuptaNoch keine Bewertungen

- HAND OUT No. 3 FABM The Accounting EquationDokument9 SeitenHAND OUT No. 3 FABM The Accounting Equationnatalie clyde matesNoch keine Bewertungen

- Quality Earnings ChecklistDokument7 SeitenQuality Earnings ChecklistKevin SmithNoch keine Bewertungen

- Home Office and BranchDokument9 SeitenHome Office and BranchLive LoveNoch keine Bewertungen

- 1989 NY Poultry Farm Business SummaryDokument30 Seiten1989 NY Poultry Farm Business SummarysuelaNoch keine Bewertungen

- PCAOB Auditing Standards Chapter 5Dokument35 SeitenPCAOB Auditing Standards Chapter 5Daniel John Cañares Legaspi100% (1)

- BADM 2001 - Fall 2019 - Assignment 3Dokument2 SeitenBADM 2001 - Fall 2019 - Assignment 3Vanessa M. EzzatNoch keine Bewertungen

- CH 1Dokument85 SeitenCH 1EmadNoch keine Bewertungen

- Tipton Ice Cream Financial ForecastingDokument10 SeitenTipton Ice Cream Financial ForecastingFD ReynosoNoch keine Bewertungen

- Market Reaction and Valuation of IFRS Reconciliation Adjustments First Evidence From The UK by Joanne Horton and George SerafeimDokument55 SeitenMarket Reaction and Valuation of IFRS Reconciliation Adjustments First Evidence From The UK by Joanne Horton and George SerafeimAlexandra NarcisaNoch keine Bewertungen

- Studi Kelayakan Investasi Pada Proyek Peningkatan JalanDokument18 SeitenStudi Kelayakan Investasi Pada Proyek Peningkatan JalanIrma MartaNoch keine Bewertungen

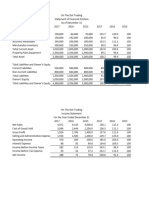

- Biwheels Excel SheetDokument18 SeitenBiwheels Excel SheetSREEDIP GHOSHNoch keine Bewertungen

- Measuring and Reporting Cash FlowDokument11 SeitenMeasuring and Reporting Cash Flowtom willetsNoch keine Bewertungen

- Trend AnalysisDokument1 SeiteTrend Analysisangel caoNoch keine Bewertungen

- Intangible Assets & Impairments of AssetsDokument72 SeitenIntangible Assets & Impairments of AssetsMuthia Khairani100% (2)

- Mega Quiz File Mgt101Dokument199 SeitenMega Quiz File Mgt101Azhar NadeemNoch keine Bewertungen

- Informe Anual CECA Cuentas Consolidadas 2019 - EngDokument181 SeitenInforme Anual CECA Cuentas Consolidadas 2019 - Engjosecente123321Noch keine Bewertungen

- Water StationDokument14 SeitenWater StationPrincess TolentinoNoch keine Bewertungen

- Financial Statement Analysis TechniquesDokument51 SeitenFinancial Statement Analysis TechniquesSumit Rp100% (4)

- Chapter 1 Financial AccountingDokument47 SeitenChapter 1 Financial Accountingslipns1ideNoch keine Bewertungen

- 21.understanding Retail ViabilityDokument23 Seiten21.understanding Retail ViabilitySai Abhishek TataNoch keine Bewertungen

- Kebijakan Modal Kerja Dalam Keuangan Syariah.Dokument11 SeitenKebijakan Modal Kerja Dalam Keuangan Syariah.shivakarlina273Noch keine Bewertungen

- ACCA Dec 2011 F7 Mock PaperDokument10 SeitenACCA Dec 2011 F7 Mock PaperCharles AdontengNoch keine Bewertungen

- Management Accounting Final ExamDokument4 SeitenManagement Accounting Final Examacctg2012Noch keine Bewertungen

- Accounting Standards ChartsDokument26 SeitenAccounting Standards ChartsEdu 4 AllNoch keine Bewertungen

- Summer Training Report Final 1Dokument65 SeitenSummer Training Report Final 1Nipun ChauhanNoch keine Bewertungen

- Financial Analysis - Molycorp, Inc. Produces Rare Earth Minerals. the Company Produces Rare Earth Products, Including Oxides, Metals, Alloys and Magnets for a Variety of Applications Including Clean Energy TechnologiesDokument8 SeitenFinancial Analysis - Molycorp, Inc. Produces Rare Earth Minerals. the Company Produces Rare Earth Products, Including Oxides, Metals, Alloys and Magnets for a Variety of Applications Including Clean Energy TechnologiesQ.M.S Advisors LLCNoch keine Bewertungen

- Estimation of Project Cash Flows: Centre For Financial Management, BangaloreDokument14 SeitenEstimation of Project Cash Flows: Centre For Financial Management, BangaloreNic KnightNoch keine Bewertungen

- Maini - Blueprint - Fi - 100 - Main Document - Ver - 3.0 PDFDokument69 SeitenMaini - Blueprint - Fi - 100 - Main Document - Ver - 3.0 PDFBhaskarChakraborty0% (2)

- Ifrs Edition: Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDokument56 SeitenIfrs Edition: Prepared by Coby Harmon University of California, Santa Barbara Westmont Collegemartinus linggoNoch keine Bewertungen