Beruflich Dokumente

Kultur Dokumente

Capital Budgeting Narain Notes

Hochgeladen von

krishanptfmsOriginaltitel

Copyright

Verfügbare Formate

Dieses Dokument teilen

Dokument teilen oder einbetten

Stufen Sie dieses Dokument als nützlich ein?

Sind diese Inhalte unangemessen?

Dieses Dokument meldenCopyright:

Verfügbare Formate

Capital Budgeting Narain Notes

Hochgeladen von

krishanptfmsCopyright:

Verfügbare Formate

F CA Ranj eet Kunwar

Bri ght Prof es si onal s (P ) L TD. 1/53, Lal i t a Par k, Laxmi nagar , Del hi - 92

Phone 47665555 ( 30Li nes) , 9811136987, 9811042458

66

Capital Budgeting

Capital Budgeting and Time value of money

Meaning and Concepts:

Capital budgeting is commonly referred to as a fixed- asset management, when integrated with the financial

managers goal of attaining proper combinations of assets (i.e. optimal asset mix ) fixed assets assume a great

deal of significance . Fixed assets are also frequency termed as the earning assets of the firm since they usually

generate large returns.

Such return is contrary to the limited earning power of and returns from short term assets.

It is the decision making process by which the firms evaluate the purchase of major fixed assets. It involves

firms decision to invest its current funds for addition, disposition, modification and replacement of long-term or

fixed assets. Capital budgeting decision involve the entire process of decision making relating to acquisition of

long-term assets whose returns are expected to arise over a period beyond one year, planning and control of

capital expenditures is a major decision area in any organisation. Its basic features can be summarised as

follows:

(i) It has the potentially of making large anticipated profits

(ii) It involves a high degree of risk

(iii) It involves a relatively long-term period between the initial outlay and the anticipated return.

Significance of Capital Budgeting

There are several factors and consideration which make the capital budgeting decisions as the most important

decisions of a finance manager. The relevance and signify of capital budgeting may be stated as follows:

(a) Long term effects: the most important features of a capital budgeting decision and which makes the

capital budgeting so significant is that these decisions have long term effects on the risk and return

composition of the firm. These decisions affect the future position of the firm to a considerable extent as

the capital budgeting decisions have long term implications and consequences. By taking a capital

budgeting decision, a finance manager in pact makes a commitment into the future, both by committing

to the future needs of funds of the projects and by committing to its future implications.

(b) Substantial commitments: the capital budgeting decisions generally involve large commitment of

funds and as a result substantial portion of capital funds are blocked in the capital budgeting decisions,

otherwise the firm may suffer from the heavy capital losses in time to come. It is also possible that the

return from projects may not be sufficient enough to justify the capital budgeting decision.

(c) Irreversible decisions: most of the capital budgeting decisions are irreversible decisions. Once taken,

the firm may not be in a position to revert back unless it is ready to absorb heavy losses, which may result

due to abandoning a project in midway.

(d) Affect the capacity and strength to compete: The capital budgeting decisions affect the capacity and

strength of a firm to face the competition. A firm may lose competitiveness of the decision to modernise is

delayed or not rightly taken. Similarly, a timely decision to take over a minor competitor may ultimately

result even in the monopolistic position of the firm.

F CA Ranj eet Kunwar

Bri ght Prof es si onal s (P ) L TD. 1/53, Lal i t a Par k, Laxmi nagar , Del hi - 92

Phone 47665555 ( 30Li nes) , 9811136987, 9811042458

67

Capital Budgeting

Kinds of Capital Budgeting Decisions

Since capital budgeting includes the process of generating, evaluating, selecting and following up on capital expenditure

alternatives, allocation of financial resources should be made by the firm to its new investment projects in the most efficient

manner. A firm may adopt the following three types of capital budgeting decisions:

(i) Mutually Exclusive Projects

It means if a firm accepts one project, it may rule out the necessity for other, i.e. the alternatives are mutually exclusive and

only one is to be chosen.

(ii) Accept- Reject Decisions

The proposals which yield a higher rate of return in comparison with a certain rate of return or cost of capital are accepted

and naturally, the others are rejected. For example, if the minimum acceptable return from a project is say 10%, after tax

and an investment proposal which shows a return of 12%, may be accepted and another project which gives a return of 8%

only may be rejected.

In other words, using Net Present Value Method Criterion an investment opportunity will be accepted if NPV>0, or, the same

will be rejected if NPV< 0. That is, all independent projects are accepted under this criterion. It is to be noted that

independent projects are those which do not compete with one another, i.e. the acceptance of one precludes the acceptance

of other. At the same time, those projects which will satisfy the minimum investment criterion should be taken into

consideration.

(iii) Capital Rationing Decision

Capital rationing is normally applied to situations where the supply of funds to the firm is limited in some way. As such, the

term covers many different situations ranging from that where the borrowings and lending rates faced by the firm differ to

that where the funds available for investments are strictly limited.

In other words, it occurs when a firm has more acceptable proposals than it can finance. At this point, the firm ranks the

projects from highest to lowest priority and as such, a cut-off point is considered.

Naturally, those proposals which are above the cut-off point will be accepted and those which are below the cut-off point are

rejected, i.e. ranking is necessary to choose the best alternatives.

Capital Budgeting Techniques

Accounting Rate of Return Pay Back Period

Net Present Internal Rate Profitability Terminate

Value of Return Index Value

Traditional or Non-discounting

or, Unsophisticated

Time-Adjusted or Discounted Cash Flows

or, Sophisticated

F CA Ranj eet Kunwar

Bri ght Prof es si onal s (P ) L TD. 1/53, Lal i t a Par k, Laxmi nagar , Del hi - 92

Phone 47665555 ( 30Li nes) , 9811136987, 9811042458

68

Capital Budgeting

Traditional or non-discounted cash flow techniques.

(a) Payback period

The term pay-back refers to the period in which the project will generate the necessary cash to recoup the initial

investment.

For example, if a project requires Rs. 20,000 as initial investment and it will generate on annual cash inflow of

Rs. 5,000 for 10 years, the pay-back period will be 4 years, calculated as follows:-

Pay-back period =

flow in cash annual

investment initital

=

000 , 5

000 , 20

The annual cash inflow is calculated by taking into account the amount of net income on account of the asset

before depreciation but after taxation. The income so earned if expressed as a percentage of initial

investment, is termed as unadjusted rate of return.

Unadjusted rate of return = 100

investment initial

return annual

= % 25 100

000 , 20

5000

=

Advantages

(i) It is simple to apply, easy to understand and of particular importance to business which lack the

appropriate skills necessary for more sophisticated techniques.

(ii) In case of capital rationing, a company is compelled to invest in projects having shortest payback

period.

(iii) This method gives an indication to the prospective investors specifying when their funds are likely to

be repaid.

(iv) Ranking projects according to their ability to repay quickly may be useful to firm when experiencing

liquidity constraints.

Disadvantages

(i) It does not indicate whether an investment should be accepted or rejected, unless the payback period

is compared with an arbitrary managerial target.

(ii) If fails to take into account the timing of returns and the cost of capital. It fails to consider the whole

life of a project.

(iii) The traditional payback approach does not consider the salvage value of an investment. The bailout

payback method concentrates on the abandonment alternative.

(iv) This method makes no attempt to measure a percentage return on the capital investment and is

often used in conjunction with other methods.

(v) The investment in projects with long payback periods are made with long-term planning and may

not yield highest returns for a number of years and the payback method is biased against such

investments.

F CA Ranj eet Kunwar

Bri ght Prof es si onal s (P ) L TD. 1/53, Lal i t a Par k, Laxmi nagar , Del hi - 92

Phone 47665555 ( 30Li nes) , 9811136987, 9811042458

69

Capital Budgeting

(b) Average rate of return (ARR) method

According to this method, the capital investment proposals are judged on the basis of their relative profitability.

For this purpose, capital employed and related incomes are determined according to commonly accepted

accounting principle and practices over the entire economic life of the project and then the average yield is

calculated. Such a rate is termed as accounting rate if return. It may be calculated according to any of the

following methods.

(I) 100

investment original

earnings net Average Annual

(II) 100

investment Average

earnings net Average Annual

Average Investment: - (Initial Cost +Installation Expenses-Salvage Value) + Salvage Value

Advantages of ARR

(i) The most significant attribute of ARR is that it is very simple to understand and easy to calculate,

(ii) It can be easily computed on the basis of accounting data which are furnished by the financial statements.

Disadvantages of ARR

(i) The principal shortcoming of ARR is that it recognises only the accounting income instead of cash flows.

(ii) It does not recognise the time value of money.

(iii) It does not take into consideration the length of lives of the projects.

(iv) It does not consider the fact that the profits may be re-invested

Modern or Discounted Cash Flow Techniques

Time Value of Money

One of the most important principles in all of finance is the relationship between value of a rupee today and

value of rupee in future. This relationship is known as the 'time value of money'. A rupee today is more valuable

than a rupee tomorrow. This is because current consumption is preferred to future consumption by the

individuals, firms can employ capital productively to earn positive returns and in an inflationary period, rupee

today represents greater purchasing power than a rupee tomorrow.

The value of money received today is different from the value of money received after some time in the future.

The preference of money now, as compared to future money is, known as time preference for money.

A rupee today is more valuable than a rupee after a year due to several reasons.

Inflation: Under inflationary conditions the value of money, expressed in terms of its purchasing power

over goods and services, declines.

Risk: Re. 1 now is certain, whereas Re.1 receivable tomorrow is less certain. This bird-in-the-hand

principle is extremely important in investment appraisal.

Personal consumption preference: Many individuals have a strong preference for immediate rather

F CA Ranj eet Kunwar

Bri ght Prof es si onal s (P ) L TD. 1/53, Lal i t a Par k, Laxmi nagar , Del hi - 92

Phone 47665555 ( 30Li nes) , 9811136987, 9811042458

70

Capital Budgeting

than delayed consumption. The promise of a bowl of rice next week counts for little to the hungry man

Investment opportunities: Many like any other desirable commodity have a price, given the choice of

Rs. 100 now or the same amount in one years time it is always preferable to take the Rs. 100 now

because it could be invested over the next year at say) 16 per cent interest rate to produce Rs. 116 at the

end of one year. If 16 per cent is the best return available then you would be indifferent to receiving Rs.

100 now or Rs. 116 in one years time. Expressed another way, the present value of Rs. 116 receivable

one year hence is Rs. 100.

The time value of the money may be computed in the following circumstances.

(a) Future value of a single cash flow

(b) Future value of an annuity

(c) Present value of a single cash flow

(d) Present value of an annuity

Future Value of a Single Cash Flow

For a given present value (PV) of money, future value of money (FV) after a period

t' for which compounding is

done at an interest rate of r, is given by the equation

FV = PV (1 + r)

t

This assumes that compounding is done at discrete intervals. However, in case of continuous compounding, the

future value is determined using the formula

FV = PV * e

rt

Where e' is a mathematical function called 'exponential' the value of exponential (e) = 2.7183.

The compounding factor is calculated by taking natural logarithm (log to the base of 2.7183).

Example 1: Calculate the value of a deposit of Rs.2,000 made today, 3 years hence if the interest rate is 10%.

By discrete compounding:

FV = 2,000 * (1+0.10)

3

= 2,000 * (1.1)

3

= 2,000 * 1.331 = Rs. 2,662

By continuous compounding:

FV = 2,000 * e (

0.10*3

) =2,000 * 1.349862 = Rs. 2699.72

Example 2. Find the value of Rs. 70,000 deposited for a period of 5 years at the end of the period when the

interest is 12% and continuous compounding is done.

Future Value = 70,000* e (0.12*5) = Rs. 1,27,548.827.

The future value (FV) of the present sum (PV) after a period 't' for which compounding is done

m' times a year at

an interest rate of r, is given by the following equation:

FV = PV (1 + (r/m)) ^mt

Example 3: How much a deposit of Rs. 10,000 will grow at the end of 2 years, if the nominal rate of interest is 12

% and compounding is done quarterly?

Future value = 10,000 *(1+0.12/4)

4*2

= Rs. 12,667.70

F CA Ranj eet Kunwar

Bri ght Prof es si onal s (P ) L TD. 1/53, Lal i t a Par k, Laxmi nagar , Del hi - 92

Phone 47665555 ( 30Li nes) , 9811136987, 9811042458

71

Capital Budgeting

Future Value of an Annuity

An annuity is a stream of equal annual cash flows. The future value (FVA) of a uniform cash flow (CF) made at

the end of each period till the time of maturity t for which compounding is done at the rate V is calculated as

follows:

r (1+ r)

t

-1

FVA = CF*l + r)

t

-

1

+ CF* (1+ r)

t-2

+ ...+ CF*(l + r)

1

+CF

= CF (1+r)

t

- 1)

r

The term (1+r)

t

- 1) is referred as the Future Value Interest factor for an annuity (FVIFA).

r

The same can be applied in a variety of contexts. For e.g. to know accumulated amount after a certain period,; to

know how much to save annually to reach the targeted amount, to know the interest rate etc.

Example 4: Suppose, you deposit Rs.3,000 annually in a bank for 5 years and your deposits earn a compound

interest rate of 10 per cent, what will be value of this series of deposits (an annuity) at the end of 5 years?

Assume that each deposit occurs at the end of the year.

Future value of this annuity is:

= Rs.3000*(1.10)

4

+ Rs.3000*(1.10)

3

+ Rs.3000*(1.10)

2

+ Rs.3000*(1.10)+ Rs.3000

= Rs.3000*(1.4641) + Rs.3000*(1.3310) + Rs.3000*(1.2100) + Rs.3000*(1.10)+ Rs.3000

= Rs. 18315.30

Example 5: You want to buy a house after 5 years when it is expected to cost 40 lakh how much should you save

annually, if your savings earn a compound return of 12 %?

The annual savings should be: 4000000/6.353 = 6,29,623.80

In case of continuous compounding, the future value of annuity is calculated using the formula:

FVA = CF * (e

rt

-1)/r.

Present Value of a Single Cash Flow

Present value of (PV) of the future sum (FV) to be received after a period 't' for which discounting is done at an

interest rate of V, is given by the equation

In case of discrete discounting: PV = FV / (1+r)

t

Example 6: What is the present value of Rs.5,000 payable 3 years hence, if the interest rate is 10 % p.a.

PV =5000/(1.10)

3

i.e. = Rs.3756.57

In case of continuous discounting: PV = FV * e

-rt

Example 7: What is the present value of Rs. 10,000 receivable after 2 years at a discount rate of 10% under continuous

discounting?

Present Value = 10,000/(exp^(0.1*2)) = Rs. 8187.297

F CA Ranj eet Kunwar

Bri ght Prof es si onal s (P ) L TD. 1/53, Lal i t a Par k, Laxmi nagar , Del hi - 92

Phone 47665555 ( 30Li nes) , 9811136987, 9811042458

72

Capital Budgeting

Present Value of an Annuity

The present value of annuity is the sum of the present values of all the cash inflows of this annuity.

Present value of an annuity (in case of discrete discounting)

PVA = FV[{(l + r)

t

- 1}/{r*(l + r)

t

}]

The term [(1+r)

1

- 1/ r*(1+r)t

1

] is referred as the Present Value Interest factor for an annuity (PVIFA).

Example 8: What is the present value of Rs. 2000/- received at the end of each year for 3 continuous years

= 2000*[1/1.10] + 2000*[1/1.10]^2+2000*[1/1.10]^3

= 2000*0.9091+2000*0.8264+2000*0.7513

= 1818.181818+1652.892562+1502.629602

= Rs. 4973.704

Example 9: Assume that you have taken housing loan of Rs.10 lakh at the interest rate of Rs.ll percent per annum. What

would be you equal annual installment for repayment period of 15 years?

Loan amount = Installment (A) *PVIFA n = 15, r=ll%

10,00,000 = A* [(1+r)

t

-1/r*(1+r)

t

]

10,00,000 = A* [(1.11)^15 - 1/ 0.11(1.11^15]

10,00,000 = A* 7.19087

10,00,000/7.19087 = A

A = Rs. 1,39,065.24

Present value of an annuity (in case of continuous discounting) is calculated as:

PVa - FVa * (l-e

-rt

)/r

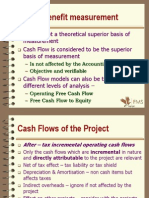

(a) Net present value method

This is generally considered to be the best method for evaluating the capital investment proposals. In case if this

method cash inflows and cash outflows associated with each project are first worked out. The present value of

these cash inflows and outflows in then calculated at the rate of return acceptable to the management this rate

of return is considered as the out-off rate and is generally determined on the basis of cost of capital suitably

adjusted to allow for the risk element involved in the project. The working capital is taken as cash out flow in the

year the project starts commercial production.

The net present value (NPV) is the difference between the total present value of future cash inflows and the total

present value of future cash inflows and future cash outflows.

Equation for NPV

NPV =

( )

( ) ( ) ( ) ( )

(

+

+

+

+

+

+

+

+

+

n

n

K

R

K

R

K

R

K

R

K

R

1 1 1 1

0 1

0

3

3

2

2

1

1

R = cash inflows at different time

K = cost of capital

The decision Rule: the decision rate under the NPV method is: accept the proposal if its NPV is positive and

reject the proposal if the NVP is negative. NPV represents the excess of benefits over the costs in real terms.

F CA Ranj eet Kunwar

Bri ght Prof es si onal s (P ) L TD. 1/53, Lal i t a Par k, Laxmi nagar , Del hi - 92

Phone 47665555 ( 30Li nes) , 9811136987, 9811042458

73

Capital Budgeting

In case of ranking of mutually exclusive proposals, the proposal with the highest positive NVP is given the top

priority and the proposal with the lowest positive NPV is assigned the lowest priority. The proposals with

negative NPV should be rejected. However, if NVP is 0 then firm may be indifferent between acceptance and

rejection of the proposal.

(i) It recognizes time value of money.

(ii) It also recognizes all cash flows throughout the life of the project.

(iii) It helps to satisfy the objectives for maximizing firm's values.

(iv) This method is particularly useful for the selection of mutually exclusive projects.

Disadvantages

(i) It is difficult to calculate as well as understand it as compared to accounting rate of return method or

payback method.

(ii) It does not present a satisfactory answer when there are different amounts of investments for the

purpose of comparison.

(iii) It does not also present a correct picture in case of alternative projects or where there are unequal

lives of the project with limited funds.

(iv) The NPV method of calculation is based on discount state which again depends on the firm's cost of

capital. The latter is to some extent difficult to understand as well as difficult to measure in actual

practice.

(b) Profitability Index (PI)

PI is defined as the benefits (in present value terms) per rupee invested in the proposal. This technique which is a

variant of the NPV technique, is also known as benefit-cost ratio, or present value index the PI is based upon the

basis concept of discounting the future cash flows and is ascertained by comparing the present value of the

future cash inflows with the present value of the future cash outflows. The PI is calculated by dividing the former

by the latter.

PI =

outflows cash of vaue present Total

lows cash of value present Total inf

The decision Rule: under the PI technique, the decision rule is: accept the project if its PI is more than I and

reject the proposal if the PI is less than I. if the PI is equal to 1, then the firm may be indifferent because the

present value of inflows is expected to be just equal to the present value of outflows.

(c) Internal Rule of return (IRR)

Internal rate of return is the rate at which the sum of discounted cash inflows equals the sum of discounted cash

outflows. In other words, it is the rate which discounts the cash flows to zero.

It can be stated in the form of a ratio as follows:

1

inf

=

outflows Cash

lows Cach

Thus, in case if this method the discount rate is not known bit the cash outflows and cash inflows are known.

For example, if a sum of Rs. 800 invested in a project becomes Rs. 1000 at the end of a year, the rate of return

comes to 25% calculated as follows:

I =

V I

R

+

I = cash outflow

K = cash inflow

F CA Ranj eet Kunwar

Bri ght Prof es si onal s (P ) L TD. 1/53, Lal i t a Par k, Laxmi nagar , Del hi - 92

Phone 47665555 ( 30Li nes) , 9811136987, 9811042458

74

Capital Budgeting

R = rate of return yielded by the investment

In case of return is over a number of years, the calculation would take the following pattern

I =

( ) ( ) ( )

( )

(

+

+

+

+

+

+

+

n v

Rn

v

R

v

R

v

R

1

1 1 1

3

3

2

2

1

1

I = cash outflow

R = cash inflow at different time periods

R = Rae of return yielded by the investment

The decision Rule: - In over to make a decision on the basis of IRR technique the firm has to determine, in the

firm instance, its own required rate of return (K)

A particular proposal may be accepted if its IRR (v) is more than the minimum rate I.e. (k), otherwise rejected.

However, if the IRR is just equal to the minimum rate, k, the firm may be indifferent. In case of mutually exclusive

proposals, the proposal with the highest IRR is given the top priority

Advantages

(i) It recognises the time value of money like Net Present Value Method;

(ii) It also takes into account the cash flows throughout the life of the project;

(iii) This method also reveals the maximum rate of return and presents a fairly good idea about the

profitability of the project even if the firm's cost of capital is absent since the latter is not a precondition

for use of it;

(iv) The percentage which is calculated under the method is more meaningful and justified and that is why it

is acceptable to the users since it satisfies them in relation to cost of capital.

Disadvantages

(i) The method of calculation is no doubt complicated and it is difficult to use and understand the same.

(ii) This method does not present unique answers under all circumstances and situations. It may even

present a negative rate or multiple rates under certain circumstances.

(iii) This method recognizes the fact that intermediate cash inflows which are generated by the project are

re-invested at the internal rate whereas the NPV method recognises that cash inflows are reinvested at

the firm's cost of capital which is more appropriate and justified in comparison with IRR method.

(iv) It may present inconsistent result with the NPV method when the projects actually differ from their

expected life or cash outlays or timing of cash flows.

Conflict in results under NPV and IRR

NPV and IRR methods may give conflicting results in case of mutually exclusive projects, i.e., projects where

acceptance of one world result in non-acceptance of the other such conflict of result may be due to any one or

more of the flowing reasons:

(i) The projects require different cash outlays

(ii) The projects have unequal loves.

(iii) The projects have different patterns of cash flows.

F CA Ranj eet Kunwar

Bri ght Prof es si onal s (P ) L TD. 1/53, Lal i t a Par k, Laxmi nagar , Del hi - 92

Phone 47665555 ( 30Li nes) , 9811136987, 9811042458

75

Capital Budgeting

In such a situation, the result given by the VPN method should be relied upon. This is because the objective of a

company is to maximise its shareholders wealth. IRR method is concerned with. The rate of return on investment

rather than total yield on investment hence it is not compliable with the goal of wealth maximisation. NPV

method considers the total yield on investment. Hence, in case if mutually exclusive projects, each having a

positive NVP, the one with largest NPV will have the most beneficial effect on shareholder is wealth.

The IRR approach solves for a rate unique to each project, while the NPV approach solves for the trade-off cash

inflows and outflows using a general required rate of return. On the basis of the above discussion of NPV and IRR,

a comparison between the two may be attempted as follows:

(a) Advantage of IRR over NPV: IRR may be considered superior to the NPV for the following reasons :

i) IRR gives percentage return while the NPV gives absolute return.

ii) For IRR, the availability of required rate of return is not a pre-requisite while for NPV it is

must.

(b) Advantage of NPV over IRR: The NPV is said to have superiority over IRR for

i) NPV shows expected increase in the wealth of the shareholders.

ii) NPV gives clear cut accept-reject decision rule, while the IRR may give multiple results also.

iii) The NPV of different projects are stabilizer while the IRR cannot be added.

iv) NPV gives better ranking as compare to the IRR.

Terminal Value (TV) Method

Under this method, it is assumed that each cash inflow is re-invested in another asset at a certain rate of return

and calculating the terminal value of net cash flows at the end of project life.

In short, the NCF and the outlay are compounded forward rather than backward by discounting which is used by

NPV method.

Acceptance Rule

From the foregoing discussion it becomes clear that if the value of the total compounded re-invested cash flows is

greater than the present value of outflow, i.e. if NCF have a higher terminal value in comparison with the outlay,

the project is accepted and vice-versa. The accept-reject rule can, thus, be formulated as under:

(1) If there is a single project : Accept the project if the terminal value (TV) is positive,

(2) If there are mutually exclusive projects : The project will be more profitable which has

a highest positive terminal value (TV).

It can also be stated that if TV is positive, accept the project and if TV is negative, reject the project.

It should be remembered that TV method is similar to NPV method. The only difference is that in case of former,

values are compounded while in case of latter, values are discounted, of course, both of them will present the same

result provided the rate is same.

F CA Ranj eet Kunwar

Bri ght Prof es si onal s (P ) L TD. 1/53, Lal i t a Par k, Laxmi nagar , Del hi - 92

Phone 47665555 ( 30Li nes) , 9811136987, 9811042458

76

Capital Budgeting

LEASE FINANCING

CONCEPT OF LEASING:

Leasing, as a financing concept, is an arrangement between two parties, the leasing company or lessor and the user

or lessee, whereby the former arranges to buy capital equipment for the use of the latter for an agreed period to

time in return for the payment of rent. The rentals are predetermined and payable at fixed intervals of time,

according to the mutual convenience of both the parties. However, the lessor remains the owner of the equipment

over the primary period. By resorting to leasing, the lessee company is able to exploit the economic value of the

equipment by using it as if he owned it without having to pay for its capital cost. Lease rentals can be conveniently

paid over the lease period out of profits earned from the use of the equipment and the rent is cent percent tax

deductible.

FORMS OF LEASE RENTALS:

The lease rentals may be quoted in several forms, for instance

(i) Level or constant period

(ii) Stepped where the lease rental increases at a fixed percentage over the earlier period,

(iii) Deferred, where the rental is deferred for certain periods to accommodate gestation period,

(iv) Ballooned under which major part of the rentals is collected in a lump sum at the end of the primary period,

(v) Bell shaped where the rental is gradually stepped up, rises to its peak in the middle of the lease period and is

then gradually stepped down and

(vi) Zig-zag where the rental is stepped up in one period and then stepped down in the succeeding period and so on.

F CA Ranj eet Kunwar

Bri ght Prof es si onal s (P ) L TD. 1/53, Lal i t a Par k, Laxmi nagar , Del hi - 92

Phone 47665555 ( 30Li nes) , 9811136987, 9811042458

77

Capital Budgeting

1. The cost of plant of Rs. 6,00,000. It has an estimated life of 5 years after which it would be

disposed-off (scrap value nil). Profit before depreciation, interest and taxes (PBIT) is

estimated to be Rs. 2,50,000 p.a. Find out the yearly cash flow from the plant. (Given the

tax rate @ 40%).

2. RMS Ltd. is evaluating a capital budgeting proposal for which relevant figures are as follows:

Cost of the plant Rs. 15, 00,000

Installation cost Rs. 5,000

Economic life 7 years

Scrap value Rs. 50,000

Profit before depreciation and tax Rs. 2,50,000

Tax rate 40%

Calculate yearly cash flows.

3. A firm buys an asset costing Rs. 2,00,000 and expects operating profits ( before

depreciation @ 15% WDV and tax @ 40%) of Rs. 35,000 p.a. for the next 4 years after

which the asset would be disposed-off for Rs. 1,40,000. find out the cash flows for different

years.

4. Following is the income statement of a project, on the basis of which calculate the annual

cash inflows.

Income statement of the project

Net sales revenue Rs. 5,75,000

- Cost of goods sold Rs. 2, 00,000

- General expenses Rs. 1, 00,000

- Depreciation 60,000 3,60,000

profit before interest and taxes 2,15,000

- interest 25,000

Profit before tax 1,90,000

- tax @ 40% 76,000

Profit after tax 1,14,000

5. Jaydev Ltd. in considering an investment proposal for which the relevant information is as

follows:

Rs.

Purchase price of the new asset 10,00,000

Installation costs 2,00,000

Increase in working capital in year zero 2,50,000

Scrap value of the new assets after 4 years 3,50,000

Revenues from new asset (annual) 21,50,000

Cash expenses on new asset (annual) 9,50,000

Current book value (old asset) 3,00,000

Present scrap value (old asset) 5,00,000

Revenue from old asset (annual) 19,25,000

Cash expenses on old asset 11,25,000

Planning period, 4 years. Tax rate 30%

Practice Questions

F CA Ranj eet Kunwar

Bri ght Prof es si onal s (P ) L TD. 1/53, Lal i t a Par k, Laxmi nagar , Del hi - 92

Phone 47665555 ( 30Li nes) , 9811136987, 9811042458

78

Capital Budgeting

Depreciation on new asset: 94% the cost is to be depreciated in the ratio of 5:6:7:4 over 4

years.

Existing asset is depreciated at a rate of Rs. 1,10,000 p.a.

6. Ramjee & Co. is considering a proposal to replace one of its old plant costing Rs. 80,000

and having a written down value of Rs. 25,000. The remaining economic life of the plant is

4 years after which it will have no salvage value. However, if sold today, it has a salvage

value of Rs. 20,000. The new machine costing Rs. 1,50,000 is also expected to have a life

of 4 years with a scrap value of Rs. 15,000. The new machine, due to its technological

superiority, is expected to contribute additional annual benefit (before depreciation and

tax) of Rs. 65,000. Find out the cash flows associated with this decision given that the tax

rate applicable to the firm is 40%. (The capital gain or loss may be taken as not subject to

tax.)

7. Gopikant Ltd. is interested in assessing the cash flows associated with the replacement of

an old machine by a new machine. The old machine bought a few years ago has a book

value of Rs. 95,000 and it can be sold for Rs. 95,000. It has a remaining life of five years

after which its salvage value is expected to be nil. It is being depreciated annually at the

rate of 15% per cent (written down value method).

The new machine costs Rs. 4,20,000. It is expected to fetch Rs. 2,00,000 after five years

when it will no longer be required. It will be depreciated annually at the rate of 30%

(written down value method.) The new machine is expected to bring a saving of Rs.

1,30,000 in manufacturing costs. Investment in working capital would remain unchanged.

The tax rate applicable to the firm is 40 %.

8. Ramlal & co. firm is currently using a machine which was purchased two years ago for Rs.

70,000 and has a remaining useful life of 5 years.

It is considering to replace the machine with a new one which will cost Rs. 1,40,000 . The

cost of installation will amount to Rs. 10,000. The increase in working capital will be Rs.

30,000. The expected cash inflows before depreciation and taxes for both the machines are

as follows;

Year existing machine new machine

1 30,000 50,000

2 30,000 60,000

3 30,000 70,000

4 30,000 90,000

5 30,000 1,00,000

The firm use straight line method of depreciation. The average tax on income as well as on

capital gain/loss is 40%.

Calculate the incremental cash flows assuming sale value of existing machine. (i) Rs. 80,000

(ii) Rs. 60,000 (iii) Rs. 50,000, (iv) Rs. 30,000

9. Kailashgiri Ltd. is trying to decide whether it should replace a manually operated machine

with a fully automatic version of the same machine. The existing machine, purchased ten

years ago, has a book value of Rs. 1,60,000 and remaining life of 10 years. Salvage value

was Rs. 50,000. The machine has recently begun causing problems with breakdowns and is

costing the company Rs. 24,000 per year in maintenance expenses. The company has been

F CA Ranj eet Kunwar

Bri ght Prof es si onal s (P ) L TD. 1/53, Lal i t a Par k, Laxmi nagar , Del hi - 92

Phone 47665555 ( 30Li nes) , 9811136987, 9811042458

79

Capital Budgeting

offered Rs. 1,00,000 for the old machine as a trade-in on the automatic model which has a

deliver price (before allowance for trade-in) of Rs. 2,10,000. It is expected to have a ten-

year life and a salvage value of Rs. 25,000. The new machine will require installation

costing Rs. 50,000 to the existing facilities, but it is estimated to have a cost savings in

materials of Rs. 85,000 per year. Maintenance costs are included in the purchase contract

and are borne by the machine manufacturer. The tax rate is 40% (applicable to both

revenue income as well as capital gains/losses). Straight line depreciation over ten years

will be used. Find out the relevant cash flows.

10. Udarraj Ltd. purchased a special machine one year ago at a cost of Rs. 25,000. At that time

the machine was estimated to have a useful life of 6 years and no salvage value. The

annual cash operating cost is approximately Rs. 21,000. A new machine has just come on

the market which will do the same job but with an annual cash operating cost of only Rs.

15,000. The new machine costs 30,000 and has an estimated life of 5 years with zero

salvage value. The old machine can be sold for Rs. 10,000 to a scrap dealer. Straight line

depreciation is used. And the companys income tax rate is 40 %. Assuming a cost of

capital of 10%, you are required to compute the incremental cash flows after taxes:

11. Tiripati Ltd. is considering installing a machine costing. Rs. 5,00,000 with an additional

investment of Rs. 1, 50,000 for its installation. The salvage value at the end of year 10 is

estimated at Rs. 2,50,000. The machine is estimated to generate sales revenue of Rs.

20,00,000 in the first year and the sales are expected to grow at 5% p.a. for the remaining

life of the machine. The profit after tax is expected at 10% of the sales while the working

capital requirement is expected to be 5% of the sales. Find out the cash flows generated by

the machine given that

1. The machine is depreciated as per straight line method, and

2. The additional working capital is required in the beginning of the year and is fully

salvageable year 10.

12. The initial outlay of the project is Rs. 1,00,000 and it generates cash inflows of Rs. 50,000, Rs.

40,000, Rs. 30,000 and Rs. 20.000 in the four years of its life span. You are required to

calculate the following:

(a) Net Present Value (NPV)

(b) Profitability Index (PI)

(c) Discounted payback period of the project assuming 10% rate of discount.

Present value of Re. 1 due at the end of a periods at 10% rate of discount.

Year 1 2 3 4 5

PV Fatl0% 0.909 0.826 0.751 0.683 0.621

13. Siddhvinayak Ltd. is considering the purchase of a new machine. Two alternative machines

have been suggested, each costing Rs. 4,00,000 earnings after tax but before depreciation are

expected to be as follows:

Year Cash-Flows

Machine

A

Machine B

1 40,000 1,20,000

2 1,20,000 1,60,000

3 1,60,000 2,00,000

4 2,40,000 1,20,000

5 1,60,000 80,000

7,20,000 6,80,000

F CA Ranj eet Kunwar

Bri ght Prof es si onal s (P ) L TD. 1/53, Lal i t a Par k, Laxmi nagar , Del hi - 92

Phone 47665555 ( 30Li nes) , 9811136987, 9811042458

80

Capital Budgeting

The company has a target rate of return on capital @ 10% and on this basis, you are required:

(i) Compare profitability (NPV) of the machines and state which alternative you consider

financially preferable.

(ii) Compute the payback period for each project and.

(iii) Compute annual rate of return for each project.

14. Gopi Ltd. is considering the purchase of new machine. Two machine A and B are available,

each costing Rs. 5 lakhs. In comparing the profitability of the machine, a discounting rate of

10% is to be used and machine is to be written off in five years by straight line method of

depreciation with nil residual value. Cash inflows after tax are expected as follows:

Year Machine A Machine B

(Rs. In lakhs) (Rs. In lakhs)

1 1.5 0.5

2 2.0 1.5

3 2.5 2.5

4 1.5 3.0

5 1.0 2.0

Indicate which machine would be profitable using the following methods of ranking investment

proposals;

(i) Pay back method;

(ii) Net present value method;

(iii) Profitability index method ; and

(iv) Average rate of return method.

The discounting factors at 10% are

Year 1 2 3 4 5

Discounting factor 0.909 0.826 0.751 0.683 0.621

15. Hariom Ltd. has decided to purchase a machine to increase the installed capacity. There are three

machines under consideration. The relevant details including estimated yearly expenditure are

sales are given below: All sales are on cash and income tax rate is 40%.

Machine A Machine B Machine C

Initial investment required Rs. 6, 00,000 Rs. 6, 00,000 Rs. 6, 00,000

Estimated annual sales 9, 00,000 8, 00,000 8, 50,000

Cost of production (estimate):

Direct materials 80,000 90,000 88,000

Direct labour 90,000 60,000 76,000

Factory overheads 90,000 90,000 88,000

Administration costs 30,000 20,000 35,000

Selling and distribution costs 30,000 20,000 30,000

The economic life of machine A is 2 years, while it is 3 years for the other two. The scrap values

are Rs. 70,000, Rs. 45,000 and Rs. 60,000 respectively.

You are required to find most investment based on Pay Back Method.

F CA Ranj eet Kunwar

Bri ght Prof es si onal s (P ) L TD. 1/53, Lal i t a Par k, Laxmi nagar , Del hi - 92

Phone 47665555 ( 30Li nes) , 9811136987, 9811042458

81

Capital Budgeting

16. Nitse Ltd. decided to purchase a machine to increase the installed capacity.

The company has four machines under consideration. The relevant details including estimated yearly

expenditure and sales are given below. All sales are for cash. Corporate Tax Rate @ 33.99% (inclusive of

Surcharge @ 10%, Eduction cess @ 2% and Secondary & Higher Education cess @ 1%)

Particulars M1 M2 M3 M4

Initial Investment (Rs. lacs) 30.00 30.00 40.00 35.00

Estimated Annual Sales (Rs. lacs) 50.00 40.00 45.00 48.00

Cost of Production (Estd) (Rs. lacs) 18.00 14.00 16.70 21.00

Economic Life (yrs) 2 3 3 4

Scrap Values (Rs. lacs) 4.00 2.50 3.00 5.00

Calculate Payback Period

17. A project costing Rs. 10 lacs. EBITD (Earnings before Depreciation, Interest and Taxes) during the first five

years is expected to be Rs. 2,50,000; Rs. 3,00,000; Rs. 3,50,000; Rs. 4,00,000 and Rs. 5,00,000. Assume

33.99% tax and 30% depreciation on WDV Method.

18. Project Cost Rs. 1,10,000

Cash Inflows :

Year 1 Rs. 60,000

Year 2 Rs. 20,000

Year 3 Rs. 10,000

Year 4 Rs. 50,000

Calculate the Internal Rate of Return.

19. The Income Statement of Bertrand Russell Ltd. for the current year is as follows:

Sales 7,00,000

Less: Costs

Material 2,00,000

Labour 2,50,000

Other operating costs 80,000

Depreciation 70,000 6,00,000

EBIT 1,00,000

Less: Taxes: @ 40% 40,000

EAT 60,000

The plant manager proposes to replace an existing machine by another machine costing Rs. 2,40,000. The

new machine will have 8 years life having no salvage value. The old machine will realise Rs. 40,000.

Income statement does not include the depreciation on old machine (the one that is going to be replaced)

as the same had been fully depreciated, for a few years more. It is believed that there will be no change in

other expenses and revenues of the firm due to this replacement. The company requires an after tax return

10%. The rate of tax applicable to companys income is 40%. Should the company buy the new machine,

assuming that the company follows straight line method of depreciation and the same is allowed for tax

purposes?.

20. A firm whose cost of capital is 10% is considering two mutually exclusive projects A and B, the

details of which are:

Year Project A Project B

Cost 0 2,00,000 2,00,000

Cash inflows 1 20,000 1,00,000

2 40,000 80,000

3 60,000 40,000

4 80,000 20,000

5 1,20,000 20,000

F CA Ranj eet Kunwar

Bri ght Prof es si onal s (P ) L TD. 1/53, Lal i t a Par k, Laxmi nagar , Del hi - 92

Phone 47665555 ( 30Li nes) , 9811136987, 9811042458

82

Capital Budgeting

Compute the net present value at 10%. Profitability index and internal rate of return for the

two projects.

21. Ramveer Ltd. considers following mutually exclusive projects.

Project A Project B

Present Value of cash inflows Rs. 20,000 Rs. 8,000

Initial cash outlay 15,000 5,000

Net present value 5,000 3,000

Profitability index 1.33 1.6

Which project should be preferred and why?

22. Following details are provided you to evaluate which machine should be selected on the basis

of NPV approach?

Machine A costs Rs. 2,00,000 payable at Zero time.

Machine B costs Rs. 1,90,000 half payable immediately and half payable in one years time.

Receipt costs expected are as follows:

Year (at end) Machine A Machine B

1 Rs. 30,000 10,000

2 50,000 70,000

3 30,000 80,000

4 35,000 70,000

5 20,000 -------

At 8% opportunity cost, which machine should be selected on the basis of NPV?

23. Jayram Ltd. is considering a new project for which the investment data are as follows:

Capital outlay Rs. 3, 00,000

Depreciation 20% p.a.

Estimated annum income before charging depreciation, but after all other charges are as

follows:

Year

1 1,50,000

2 1,50,000

3 90,000

4 90,000

5 80,000

You are required to evaluate above project on the basis of following technique.

(a) Payback Period method.

(b) Rate of return on original investment.

24. Ram managing director of a private company has to consider the following project.

Cost Rs. 5,00,000

Cash inflows:

Year

1 50,000

2 50,000

3 1,00,000

4 4,80,000

Calculate the IRR and comment on the project if the cost of capital is 14%.

F CA Ranj eet Kunwar

Bri ght Prof es si onal s (P ) L TD. 1/53, Lal i t a Par k, Laxmi nagar , Del hi - 92

Phone 47665555 ( 30Li nes) , 9811136987, 9811042458

83

Capital Budgeting

25. Arundev Ltd. is considering a new five year project. Its investment costs and annual profits are

projected as follows:

Year Rs.

Investment

Profits

0

1

2

3

4

5

(5,00,000)

1,80,000

1,60,000

40,000

1,20,000

80,000

The residual value at the end of the project is expected to be Rs. 40,000 and depreciation of

the original investment is on straight line basis. Using average profits and average capital

employed calculated the ARR for the project and the payback period.

26. An investment of Rs. 1,36,000 yields the following cash inflows (profits before depreciation but

after tax).

Year 1 2 3 4 5

Cash flows 30,000 40,000 60,000 30,000 20,000

PVF at 10% 0.90

9

0.826 0.751 0.683 0.621

PVF at 12% 0.893 0.797 0.712 0.636 0.567

Calculate NPV at discount rate 10% and 12%. Also calculate IRR.

27. Ramdayal Ltd. proposes to install a machine involving a capital cost of Rs. 3,60,000. The life of

the machine is 5 years and its salvage value at the end of the life is nil. The machine will

produce the net operating income after depreciation of Rs. 68,000 per annum. The company's

tax rate is 45%. The Net Present Value factors for 5 years are as under:

Discounting Rate 14% 15% 16 % 17% 18%

Cumulative factor 3.43 3.35 3.27 3.20 3.13

You are required to calculate the internal rate of return of the proposal.

28. Following are the data on a capital project being evaluated by the management of Gopal Ltd.:

Annual cost saving Rs. 40,000

Useful life 4 years

I.R.R. 15%

Profitability Index (P.I.) 1.064

NPV ?

Cost of capital ?

Cost of project ?

Payback ?

Salvage value 0

Find the missing values considering the following table of discount factor only:

Discount factor 15% 14% 13% 12%

1 year 0.869 0.877 0.885 0.893

2 year 0.756 0.769 0.783 0.797

3 year 0.658 0.675 0.693 0.712

4 year 0.572 0.592 0.613 0.636

2.855 _____ 2.913 ____ 2.974 _____ 3.038

29. Kailash Ltd. has an investment opportunity costing Rs. 3,00,000 with the following expected cash

inflow (i.e. after tax and before depreciation):

F CA Ranj eet Kunwar

Bri ght Prof es si onal s (P ) L TD. 1/53, Lal i t a Par k, Laxmi nagar , Del hi - 92

Phone 47665555 ( 30Li nes) , 9811136987, 9811042458

84

Capital Budgeting

Year Inflows PVF

(10%)

year inflows PVF

(10%.)

1 50,000 0.909 6 50,000 0.564

2 50,000 0.826 7 30,000 0.513

3 55,000 0.751 8 50,000 0.467

4 55,000 0.683 9 30,000 0.424

5 50,000 0.621 10 40,000 0.386

Using 10% as the cost of capital determine the

(i) Net present value; and

(ii) Profitability index.

30. Tirupati Ltd. requires an initial investment of Rs. 1,00,000. The estimated net cash flows are as

follows:

Year 1 2 3 4 5

Net cash 16,000 17,000 18,000 17,000 15,000

Year 6 7 8 9 10

20,000 30,000 40,000 25,000 10,000

Using 10% as the cost of capital (rate discount) determine the following:

(i) Pay Back (ii) Net Present Value and (iii) Internal Rate of Return.

31. Ramdeen Ltd. is considering the replacement of its existing machine which is outdated and unable

to meet the rapidly rising demand for its product.

The company has two alternatives:

(i) to buy machine A which is similar to the existing machine or

(ii) to go in for machine B which is more expensive and has much greater capacity. The cash

flows at the present level of operations under the two alternatives are as follows;

Cash flows ( in lacs ) at the end of year:

Time 0 1 2 3 4 5

Machine A -25 -- 2 20 14 14

Machine B -40 10 14 16 17 15

The companys cost of capital is 10%. The finance manager tries to evaluate the machines by

calculating the following:

1. Net present value,

2. Profitability index,

3. Pay- Back period,

At the end of his calculations, however, the finance manager is unable to make up his mind as to

which machine to recommend. You are required to make these calculation and in the light thereof to

advise the finance about the proposed investment.

Present values of re. 1 at 10% discount rates is as follows:

Year 0 1 2 3 4 5

P. V. 1.00 .91 .83 .75 .68 .62

F CA Ranj eet Kunwar

Bri ght Prof es si onal s (P ) L TD. 1/53, Lal i t a Par k, Laxmi nagar , Del hi - 92

Phone 47665555 ( 30Li nes) , 9811136987, 9811042458

85

Capital Budgeting

32. Prabhu Ltd. is forced to choose between two machines A and B. The two machines are designed

differently, but have identical capacity and do exactly the same job. Machine A costs Rs.

1,50,000 and will last for 3 years. It costs Rs. 40,000 per year to run. Machine B is an

economy' model costing only Rs. 1,00,000, but will last only for 2 years and costs Rs. 60,000

per year to run. Cost of capital is 10%. Which machine should buy?

33. Ramjee Ltd. is considering installing either of the two machines which are mutually exclusive. The details of

their purchase price and operating costs are:

Year Machine X Machine Y

Purchase cost 0 Rs. 10,000 Rs. 8,000

Operating cost 1 Rs. 2,000 Rs. 2,500

Operating cost 2 Rs. 2,000 Rs. 2,500

Operating cost 3 Rs. 2,000 Rs. 2,500

Operating cost 4 Rs. 2,500 Rs. 3,800

Operating cost 5 Rs. 2,500 Rs. 3,800

Operating cost 6 Rs. 2,500 Rs. 3,800

Operating cost 7 Rs. 3,000

Operating cost 8 Rs. 3,000

Operating cost 9 Rs. 3,000

Operating cost 10 Rs. 3,000

Machine X will recover salvage value of Rs. 1,500 in the year 10, while Machine Y will recover Rs. 1,000 in the

year 6. Determine which machine is cheaper at 10 per cent cost of capital, assuming that both the machines

operate at the same efficiency.

34. A project with 5 years life requires initial investments as under

Plant and Machinery Rs. 2,70,500

Working Capital Rs. 40,000

Rs. 3,10,500

The working capital will be fully realized at the end of the 5

th

year. The scrap value of the plant

expected to be realized at the end of the 5

th

year is only Rs. 5,500. The earnings from project

are:

Year 1 2 3 4 5

Cash flows Rs. 90,000 Rs. 1,30,000 Rs. 1,70,000 Rs. 1,16,000 Rs. 19,500

(before depreciation & tax)

Tax payable Rs. 20,000 Rs. 30,000 Rs. 40,000 Rs. 26,000 Rs 5,000

You are required to compute the present value of cash follows discounted at the various rates

of interests given below and state the return from the project.

PVF at Interest rate 15% 14% 13% 12%

1Year 0.869 0.877 0.885 0.893

2 Year 0.756 0.769 0.785 0.797

3 Year 0.658 0.675 0.693 0.712

4 Year 0.572 0.592 0.613 0.636

5 Year 0.497 0.519 0.543 0.567

F CA Ranj eet Kunwar

Bri ght Prof es si onal s (P ) L TD. 1/53, Lal i t a Par k, Laxmi nagar , Del hi - 92

Phone 47665555 ( 30Li nes) , 9811136987, 9811042458

86

Capital Budgeting

35. Bramha Ltd. is considering two different investment proposals, A and B details are as under:

Proposal A Proposal B

Investment cost Rs. 9,500 Rs. 20,000

Year1 4,000 8,000

Year 2 4,000 8,000

Year 3 4,500 12,000

Suggest the most attractive proposal on the basis of the NPV method considering that the

future incomes are discounted at 12% also find out the IRR of the two proposals.

36. The cash flows from two mutually exclusive projects A and B are as under;

Years Project A Project B

0 Rs. 22,000 Rs. 27,000

1-7 (annual) 6,000 7,000

Project life 7 years 7 years

i) Calculate NPV of the proposals at discount rates of 15%, 16%, 17%, 18%, 19% and 20%.

ii) Advise on the project on the basis of IRR method.

37. Tirudev Ltd. had the option to buy either Machine A or Machine B. Machine A has a cost of Rs.

75,000. Its expected life is 6 years with no salvage value at the end. It would generate net

cash flows of Rs. 20,000 per year. Machine B on the other hand would cost Rs. 50,000. Its

expected life is 6 years with no salvage value at the end. It would generate net cash of Rs.

15,000 per year. Assuming that the cost of capital of both the machines is 10%, you are

required to calculate:

a) Net present value for each machine.

b) Internal rate of return for each machine

c) Which machine should be recommended and shy?

38. Harigovind Ltd. is evaluating three investment situations. If only the project in question is under

taken, the expected present values and the amounts of investment required are

Project Investment

Required

Present value of

future cash flows

1

2

3

$200,000

115,000

270,000

$290,000

185,000

400,000

If projects 1 and 2 are jointly undertaken, there will be no economics, there will be no

economics, the investments required and present value will simply be the sum of the parts.

With projects 1 and 3, economics are possible in investment because one of the machines

acquired can be used in both production processes. The total investment required for projects 1

and 3 combined is $ 440,000. If projects 2 and 3 are undertaken, there are economics to be

achieved in marketing and producing the products but not in investment. The expected present

value of future cash flows for projects 2 and 3 is $ 620,000. If all three projects are undertaken

simultaneously, the economics noted will still hold. However, a $125,000 extension on the plant

will be necessary, as space is not available for all three projects. Which project or projects

should be chosen?

F CA Ranj eet Kunwar

Bri ght Prof es si onal s (P ) L TD. 1/53, Lal i t a Par k, Laxmi nagar , Del hi - 92

Phone 47665555 ( 30Li nes) , 9811136987, 9811042458

87

Capital Budgeting

39. Surya Ltd. Has Rs. 30 lacs available for investment in capital projects. It has the option of

making investment in projects 1,2,3 and 4. Each project is entirely independent and has a

useful life of 5 years. The expected present value of cash flows the projects are as follows:

Projects Initial Outflow PV of Cashflows

1 8,00,000 10,00,000

2 15,00,000 19,00,000

3 7,00,000 11,40,000

4 13,00,000 20,00,000

Which of the above investment should be undertaken? Assume that the cost of capital is 12%

and risk free interest rate is 10% per annum.

Compounded sum of Re. 1 at 10% in 5 years is Rs. 1.611 and discount factor of Re. at 12%

rate for 5 years is 0.567

40. Radheshyam Ltd. is considering its capital investment (Rs. 12 lacs) programme for next year. It

has five projects all of which give a positive NPV at the company cut-off rate of 15%. The

investment outflows and PV being as follows:

Project Investment (Rs.) NPV @ 15% (Rs.)

A

B

C

D

E

500000

400000

250000

300000

350000

154000

187000

101000

112000

193000

You are required to optimize the returns from a package of projects within the capital spending

limit. The projects are independent of each other and are divisible (i.e. part-project is

possible).

41. Five Projects M, N, O, P and Q are available to a company for consideratio.

The investment required for each project and the cash flows it yields are tabulated below. Projects N and Q

are mutually exclusive. Taking the cost of capital @ 10%, which combination of projects should be taken

up for a total capital outlay not exceeding Rs. 3 lakhs on the basis on NPV and Benefit-Cost Ratio (BCR)?

Project Investment Cash flow p.a. No of years P.V. @ 10%

M 50,000 18,000 10 6.145

N 1,00,000 50,000 4 3.170

O 1,20,000 30,000 8 5.335

P 1,50,000 40,000 16 7.824

Q 2,00,000 30,000 25 9.077

Total Capital outlay < Rs. 3.00 lakhs

42. Gopi Ltd. is considering 5 capital projects for the years 2002, 2003, 2004, 2005. The company

is financed by equity entirely and its cost of capital is 12%. The expected cash flows of the

projects are as follows:

project Years and cash flows

2002 2003 2004 2005

A

B

C

D

E

(70,000)

(40,000)

(50,000)

--

(60,000)

35,000

(30,000)

(60,000)

(90,000)

20,000

35,000

45,000

70,000

55,000

40,000

20,000

55,000

80,000

65,000

50,000

F CA Ranj eet Kunwar

Bri ght Prof es si onal s (P ) L TD. 1/53, Lal i t a Par k, Laxmi nagar , Del hi - 92

Phone 47665555 ( 30Li nes) , 9811136987, 9811042458

88

Capital Budgeting

All projects are divisible i.e. size of investment can be reduced, if necessary in relation to

availability of funds. None of the projects can be delayed or undertaken more than once.

Calculate which project should undertake if the capital available for investment is limited to Rs.

1,10,000 in year 2002 and with no limitation in subsequent years. For your analysis, use the

following PVF:

Year 2002 2003 2004 2005

PVF 1.00 0.89 0.80 0.71

43. A share of the face value of Rs. 100 has current market price of Rs. 480. Annual expected dividend is

30%. During the fifth year, the shareholder is expecting a bonus in the ratio of 1:5. Dividend rate is

expected to be maintained on the expanded capital base. The shareholder intends to retain the share till

the end of the eighth year. At that time the value of share is expected to be Rs. 1,000. Incidental

expenses at the time of purchase and sale are estimated at 5% on the market price. There is no tax on

dividend income and capital gain. The shareholder expects a minimum return of 15% p.a.

Should he buy the share? What is the maximum price he can pay for the share? Show complete working.

44. Ramjee Ltd. is in the business of manufacturing. It has a plant on a piece of land measuring two

acres which was purchased ten years ago for Rs. 10 lacs. The firm is now planning to set up

another plant on the same land. 50% of the existing plot is to be earmarked for this purpose.

The accountant has supplied the following information:

Capital expenditure for setting up new plant (incurred in the beginning of the year):

Year 1 Cost of land 5,00,000

Land development 2,00,000

Payment to building contractor 15,00,000

Payment for purchase of machine 20,00,000

Year 2 Final payment to building contractor 15,00,000

Final payment to machine supplier 70,00,000

The plant has an estimated useful life of 5 years and the company follows SLM of depreciation.

The information regarding sales and operational expenses is as follows:

Year 1 2 3 4 5

Sales (Rs. Lacs) 25 30 35 40 45

Expenses (Rs. Lacs) 5 7 10 12 15

During first year and last year, all sales will be cash sales. In others, 10% of sales will be on

credit for a period of one year. If the companys rate of discount is 15% and the tax rate is

50%, should the above proposal be accepted.

45. Thomas Alva Edison Limited, a highly profitable company, is engaged in the manufacture of power

intensive products. As part of its diversification plans, the company proposes to put up a Windmill to

generate electricity. The details of the scheme are as follows:

(1) Cost of the Windmill Rs. 300 lakhs

(2) Cost of Land Rs. 15 lakhs

(3) Subsidy from State Govenment to be received at the end of first year of installation Rs. 15 lakhs

(4) Cost of electricity will be Rs. 2.25 per unit in year 1. This will incerease by Rs. 0.25 per unit every

year till year 7.

After that it wil increae by Rs. 0.50 per unit.

(5) Maintennce cos will be Rs. 4 lakhs in year 1 and the same will increase by Rs. 2 lakhs every year.

F CA Ranj eet Kunwar

Bri ght Prof es si onal s (P ) L TD. 1/53, Lal i t a Par k, Laxmi nagar , Del hi - 92

Phone 47665555 ( 30Li nes) , 9811136987, 9811042458

89

Capital Budgeting

(6) Estimated life 10 years.

(7) Cost of capital 15%.

(8) Residual value of Windmill will be nil. However land value will go up to Rs. 60 lakhs, at the end of

year 10.

(9) Depreciation will be 10% of the cost of the Windmill in year 1 and the same will be allolwed for tax

purposes.

(10) As Windmills are expected to work based on wind velocity, the efficiency is expected to be an

average 30%. Gross electricity generates at this level will be 25 lakh units per annum. 4% of this

electricity generated will be committed free to the State Electriciy Board as per the agreement.

(11) Tax rate 50%.

From the above information you are required to:

(a) Calculate the Net Present Value. [Ignore tax on capital profits.]

(b) List down two non-financial factors that should be considered before taking a decision.

For your exercise use the following discount factors.

Year 1 2 3 4 5 6 7 8 9 10

PVF 0.87 0.76 0.66 0.57 0.50 0.43 0.38 0.33 0.28 0.25

46. Determine which of the following two mutually exclusive projects should be selected it may are :

(i) One-off investments or (ii) It they can be repeated indefinitely:

(Rs.)

Particulars Project A Project B

Investment 40,000 60,000

Life 4 years 7 years

Annual net cash inflows 15,000 16,000

Scrap value 5,000 3,000

Cost of capital is 15%. Ignore taxation. The Present Value of annuity for 4 years and 7 years at 15% are

respectively 2.8550 and 4.1604 and the discounting factors at 4 years/7 years respectively 0.5718 and 0.3759.

47. Appa Ltd. is evaluating the following two mutually exclusive proposals.

Project X Project Y

Outlay 80,000 1,20,000

Annual net inflow 30,000 32,000

Life 4 years 7 years

Scrap value 10,000 6,000

Evaluate the proposals if the discount rate is 15%.

48. During the manufacturing process the Gopikant Ltd. is generating 1,00,000 units waste material

per annum. The waste material can be processed further and sold @ Rs. 1000 per unit and the

variable cost of processing comes to 70% of selling price.

Out of the processed waste material, 25% can be refabricated at a cost of Rs. 100 per unit. the

prefabricated product can be sold at a price of 1500 per unit and there is a waste of 20% of

processed material at the time of refabrication.

The refabrication procedure requires

F CA Ranj eet Kunwar

Bri ght Prof es si onal s (P ) L TD. 1/53, Lal i t a Par k, Laxmi nagar , Del hi - 92

Phone 47665555 ( 30Li nes) , 9811136987, 9811042458

90

Capital Budgeting

(i) A Plant costing Rs. 1,00,00,000 with life 5 years . (Depreciation is chargeable @ 25%

WDV) and

(ii) Additional working capital of Rs. 10,00,000.

Evaluate the proposal to refabricate the processed waste material given that:

(i) Required rate of return if 15%

(ii) Tax rate applicable of company is 30%.

(iii) Expected salvage value of the plant is Rs. 10,00,000.

(iv) There is no other asset in the same block of assets.

49. Ramdhun Ltd. wants to installed computer for office work. For this purpose two models have

shortlist, for which the relevant information is as follows:

Model I Model II

Cost 1,50,000 2,50,000

Salvage value nil 20,000

Working capital required 50,000 70,000

Savings in expense 1,00,000 p.a. 1,50,000 p.a.

Life 5 years 5 years

Depreciation 15% W. D. V. 15% W.D. V.

Find out which model is better given that

(i) Tax rate is 30% .

(ii) Required rate of return is 13% .

(iii) There is no other asset in the same block of assets.

50. Asmi industries Ltd. is expanding its operations and is in the middle of replacing one of its plant

(original cost Rs. 10,00,000 life 10 years, Dec. @ 15% WDV) which has a remaining life of 6

years. This machine has a salvage value of Rs. 2,00,000 at present.

The new machine being considered for replacement is costing Rs. 15,00,000 ( salvage value

10% at the end of 6 years). The important data regarding new machine are as follows:

Incremental revenue 5,00,000

Fixed cost (excluding depreciation) unchanged

Variable cost 30%

Depreciation rate 15% WDV.

(i) the required rate decision given that 10%

(ii) rate of tax 30%

(iii) There are several assets in the same block of assets.

51. An oil company proposes to install a pipeline for transport of crude from wells to refinery. Investments and

operating costs of the pipeline very for different sizes of pipelines (diameter). The following details have

been conducted :

(a) Pipeline diamter (in inches) 3 4 5 6 7

(b) Investment required (Rs. lakhs) 16 24 36 64 150

(c) Gross annual savings in operating

Costs before depreciation (Rs. lakhs) 5 8 15 30 50

The estimated life of the installation is 10 years. The oil companys tax rate is 50%. There is no salvage value

and straight line rate of depreciation is followed. Calculate the net savings after tax and cash flow generation

and recommend therefrom, the largest pipeline to be installed, if the company desires a 15% post-tax return.

Also indicate which pipeline will have the shortest payback. The annuity P.V. factor at 15% for 10 years is

5.019.

F CA Ranj eet Kunwar

Bri ght Prof es si onal s (P ) L TD. 1/53, Lal i t a Par k, Laxmi nagar , Del hi - 92

Phone 47665555 ( 30Li nes) , 9811136987, 9811042458

91

Capital Budgeting

52. Indo Plastics Ltd. is a manufacturer of high quality plastic products. Rasik, President, is considering

computerizing the companys ordering, inventory and billing procedures. He estimates that the annual

savings from computerization include a reduction of 4 clerical employees with annual salaries of Rs.

50,000 each, Rs. 30,000 from reduced production delays caused by raw materials inventory problems, Rs.

25,000 from lost sales due to inventory stock outs and Rs. 18,000 associated with timely billing

procedures.

The purchase price of the system in Rs. 2,50,000 and installation costs are Rs. 50,000. These outlays will

be capitalized (depreciated) on a straight line basis to a zero books salvage value which is also its market

value at the end of five years. Operation of the new system requires two computer specialists with annual

salaries of Rs. 80,000 per person. Also annual maintenance and operating (cash) expenses of Rs. 22,000

are estimated to be required. The companys tax rate is 40% and its required rate of return (cost of capital)

for this project is 12%

You are required to

(i) Evaluate the project using NPV method;

(ii) Evaluate the project using PI method;

(iii) Calculate the Projects payback period.

Note :

(a) Present value of annuity of Re. 1 at 12% rate of discount for 5 years is 3.605.

(b) Present value of Re. 1 at 12% rate of discount, received at the end of 5 years is 0.567.

53. Deenanath Ltd. is presently operating with a machine X (WDV of Rs. 1,00,000, Salvage value

today Rs. 50,000) and it can be used for next 5 years to general net annual earning of Rs.

1,50,000 (before depreciation). The salvage value after 5 years is expected to be Rs. 5000

only.

The machine could be replaced by a new machine costing Rs. 4,00,000 ( life 5 years, salvage

value Rs. 20,000). The new machine is expected to generate net annual earnings of Rs.

3,00,000 (before depreciation)

The firm depreciates its asset @ 15% WDV and there is no other asset in the same block of

asset. Evaluate the replacement proposal.

Tax rate is 30% and cost of capital is 20%.

54. JJ Associates is considering to acquire an asset costing Rs. 5,00,000. The company has an offer

from a bank to lend @15%. The principal amount is repayable in 5 years end installments. A

leasing company has also submitted a proposal to the company to acquire the asset on lease at

yearly rentals of Rs. 300 per Rs. 1,000 of the assets value for 5 years payable at year end. The

salvage value of the asset at the end of 5 years period is estimated to be Rs. 1,000. Whether

the company should accept the proposal of bank or leasing company, if the effective tax rate of

the company is 40% and discount rate is 15%?

55. William Ford Ltd. has received 3 proposals for the acquisition of an assets on lease costing Rs. 1,50,000.

Option I : The terms of offer envisaged payment of lease rentals for 96 months. During the first 72

months, the lease rentals were to be paid @ Rs. 30 p.m. per Rs. 1,000 and during the reamining 24

months @ Rs. 5 p.m. per Rs. 1,000. At the expiry of lease period, the lessor has offered to sale the assets

at 5% of the original cost.

Option II : Lease agreement for a period of 72 months during whcih lease rentals to be paid per month

per Rs. 1,000 are Rs. 35, Rs. 30, Rs. 26, Rs. 24, Rs. 22 and Rs. 20 for next 6 years. At the end of lease

period the asset is proposed to be abandoned.

F CA Ranj eet Kunwar

Bri ght Prof es si onal s (P ) L TD. 1/53, Lal i t a Par k, Laxmi nagar , Del hi - 92

Phone 47665555 ( 30Li nes) , 9811136987, 9811042458

92

Capital Budgeting

Option III : Under this offer a lease agreement is proposed to be signed for a period of 60 months

wherein an initial lease deposit to the extent of 15% will be made at the time of signing of agreement.

Lease rentals @ Rs. 35 per Rs. 1,000 per months will have to be paid for a period of 60 months on the

expiry of leasing agreement, the assets shall be sold against the initial deposit and the asset is expected

to last for a further period of three years.

You are required to evaluate the proposals keeping in view the following parameters.

(i) Depreciation @ 25%

(ii) Discounting rate @ 15%

(iii) Tax rate applicable @ 40%

The monthly and yearly discounting factors @ 15% discount rate are as follows:

Period 1 2 3 4 5 6 7 8

Monthly 0.923 0.765 0.685 0.590 0.509 0.438 0.377 0.325

Yearly 0.869 0.756 0.658 0.572 0.497 0.432 0.376 0.327

56. The following details relate to an investment proposal of Freud Ltd.

Investment outlay Rs. 100 lakhs

Lease Rentals are payable at Rs. 180 per Rs.1000

Term of lease 8 years

Cost of capital for the firm is 12%

Find the Present Value of Lease Rentals if

a. Lease Rentals are payable at the end of the year

b. Lease Rentals are payable at the beginning of the year

57. Find out Loan payments per annum for the following :

Cost of Equipment : Rs. 50 lakhs

Borrowing rate : 15%

Term of Loan : 5 years

a. Principal is payable in equal investment over the period of five years

b. Amount of Loan is payable equally over the period of five years

Prepare a table showing principle & interest payments and the total payable over period of five years.

58. Mao Leasing Company is considering a proposal lease out a school bus. The bus can be purchased for

Rs. 50,0000 and in turn, be leased out at Rs. 125000 per year for 8 years with payments occuring at the

end of each year.

(a) Estimate the IRR for the company assuming tax is ignored.

(b) What should be the yearly lease payment charged by the company in order to earn 20% annual

compounded rate of return before expenses and taxes?

(c) Calculate the annual lease rent to be charged so as to amount to 20% after tax annual compounded

rate of return, based on thr following assumptions :

i. Tax rate is 40%

ii. Straight Line Depreciation

iii. Annual expenses of Rs. 50000, and

iv. Resale value Rs. 100000 after the turn.

F CA Ranj eet Kunwar

Bri ght Prof es si onal s (P ) L TD. 1/53, Lal i t a Par k, Laxmi nagar , Del hi - 92

Phone 47665555 ( 30Li nes) , 9811136987, 9811042458

93

Capital Budgeting

59. ABC and Co. is considering two mutually exclusive machines A and B. the company uses

certainty Equivalent approaches to evaluate the proposals. The estimated cash and certainty

equivalents for both machines are as follows:

Machine X Machine Y

Year Cash flow Cer. Eqult. Cash flow Cer. Equilt.

0 30,000 1.00 40,000 1.00

1 15,000 .95 25,000 .90

2 15,000 .85 20,000 .80

3 10,000 .70 15,000 .70

4 10,000 .65 10,000 .60

Which machine should be accepted, if the risk free discount rate is 5 percent?

60. You are required to determine the Risk Adjusted Net Present Value of the following projects:

G K R

Net cash outlay (Rs.) 1,00,000 1,20,000 2,10,000

Project life 5 years 5 years 5 years

Annual cash inflow (Rs.) 30,000 42,000 70,000

Coefficient of Variation 0.4 0.8 1.2

The company selects the risk adjusted rate of discount on the basis of the coefficient of variation;

Coefficient of Risk adjusted rate Present Value factor 1 to 5

Variation of discount years at Risk Adjusted

Rate of discount

0.0 10% 3.791

0.4 12% 3.605

0.8 14% 3.433

1.2 16% 3.274

1.6 18% 3.127

2.0 22% 2.864

More than 2.0 25% 2.689