Das könnte Ihnen auch gefallen

- The Intelligent REIT Investor: How to Build Wealth with Real Estate Investment TrustsVon EverandThe Intelligent REIT Investor: How to Build Wealth with Real Estate Investment TrustsBewertung: 4.5 von 5 Sternen4.5/5 (4)

- Accountancy exam questions on partnerships, shares and financial analysisDokument11 SeitenAccountancy exam questions on partnerships, shares and financial analysissahithi rudrarajuNoch keine Bewertungen

- Ca Ipcc May 2011 Qustion Paper 5Dokument11 SeitenCa Ipcc May 2011 Qustion Paper 5Asim DasNoch keine Bewertungen

- The Red Dream: The Chinese Communist Party and the Financial Deterioration of ChinaVon EverandThe Red Dream: The Chinese Communist Party and the Financial Deterioration of ChinaNoch keine Bewertungen

- I Sem EAFM FINANCIAL MANAGEMENTDokument3 SeitenI Sem EAFM FINANCIAL MANAGEMENTSuryaNoch keine Bewertungen

- Advanced Financial Management Exam QuestionsDokument3 SeitenAdvanced Financial Management Exam QuestionsRamakrishna NagarajaNoch keine Bewertungen

- 2018 April MGU Cbcss 4th Semester Corporate Accounting Question Paper Goodwill Tuition Centre 9846710963 9567902805Dokument4 Seiten2018 April MGU Cbcss 4th Semester Corporate Accounting Question Paper Goodwill Tuition Centre 9846710963 9567902805Rainy Goodwill0% (1)

- Paper - 1: Financial Reporting Questions Consolidated Balance Sheet (Chain Holding)Dokument52 SeitenPaper - 1: Financial Reporting Questions Consolidated Balance Sheet (Chain Holding)Anonymous duzV27Mx3Noch keine Bewertungen

- TEST Paper 1 Full TestDokument9 SeitenTEST Paper 1 Full Testjohny SahaNoch keine Bewertungen

- Analysis of Financial StatementsQ&AssignmentsDokument4 SeitenAnalysis of Financial StatementsQ&AssignmentsMalik FaisalNoch keine Bewertungen

- Accounting With AnswerDokument15 SeitenAccounting With Answermary louise maganaNoch keine Bewertungen

- Assignment 4 QuestionDokument8 SeitenAssignment 4 QuestionAhmad S GrewalNoch keine Bewertungen

- Internal ReconstructionDokument8 SeitenInternal Reconstructionsmit9993Noch keine Bewertungen

- Bachelor'S Degree ProgrammeDokument8 SeitenBachelor'S Degree ProgrammeUjjval TrivediNoch keine Bewertungen

- Faculty of Management: Financial Accounting and AnalysisDokument11 SeitenFaculty of Management: Financial Accounting and AnalysisHari KrishnaNoch keine Bewertungen

- Buy Back of SharesDokument32 SeitenBuy Back of SharesMehul SesodiyaNoch keine Bewertungen

- Mcom AnnualDokument140 SeitenMcom AnnualKiran TakaleNoch keine Bewertungen

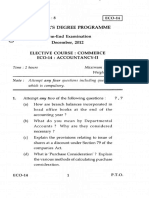

- Bachelor'S Degree Programme Term-End Examination December, 2012 Elective Course: Commerce Eco-14: Accountancy-IiDokument8 SeitenBachelor'S Degree Programme Term-End Examination December, 2012 Elective Course: Commerce Eco-14: Accountancy-IiRohit GhuseNoch keine Bewertungen

- Standalone Financial Results, Limited Review Report For September 30, 2016 (Result)Dokument5 SeitenStandalone Financial Results, Limited Review Report For September 30, 2016 (Result)Shyam SunderNoch keine Bewertungen

- Chapter Internal ReconstructionDokument4 SeitenChapter Internal ReconstructionAnonymous mTZsMOjNoch keine Bewertungen

- Engineering Economy Jan 2014Dokument2 SeitenEngineering Economy Jan 2014Prasad C MNoch keine Bewertungen

- Accounting concepts and principles in financial statementsDokument6 SeitenAccounting concepts and principles in financial statementskartikbhaiNoch keine Bewertungen

- Paper 11Dokument51 SeitenPaper 11eshwarsapNoch keine Bewertungen

- AdvDokument19 SeitenAdvashwin krishnaNoch keine Bewertungen

- CA Final Paper 2Dokument32 SeitenCA Final Paper 2MM_AKSINoch keine Bewertungen

- Financial Analysis 105-115Dokument10 SeitenFinancial Analysis 105-115deshpandep33Noch keine Bewertungen

- Chapter06 ProblemsDokument2 SeitenChapter06 ProblemsJesús Saracho Aguirre0% (1)

- Mayfield PlazaDokument9 SeitenMayfield PlazaPuran SarnaNoch keine Bewertungen

- Practical Questions: Derivatives Analysis and Valuation 7Dokument24 SeitenPractical Questions: Derivatives Analysis and Valuation 7RITZ BROWNNoch keine Bewertungen

- Appendix Scanner Gr. I GreenDokument25 SeitenAppendix Scanner Gr. I GreenMayank GoyalNoch keine Bewertungen

- Pccquestionpapers (2008)Dokument20 SeitenPccquestionpapers (2008)Samenew77Noch keine Bewertungen

- Question Papers Supplementary Exam 2007Dokument24 SeitenQuestion Papers Supplementary Exam 2007ce1978Noch keine Bewertungen

- Nirma: UniversityDokument3 SeitenNirma: UniversityBHENSDADIYA KEVIN PRABHULALNoch keine Bewertungen

- Unit-2, Regulations of Depository InstitutionsDokument6 SeitenUnit-2, Regulations of Depository InstitutionsUmesh LagejuNoch keine Bewertungen

- Financial Decision MakingDokument4 SeitenFinancial Decision MakingHarsh DedhiaNoch keine Bewertungen

- Engineering Economy June July 2008Dokument2 SeitenEngineering Economy June July 2008mechnoeNoch keine Bewertungen

- Analysis of Financial StatementsDokument16 SeitenAnalysis of Financial StatementsAlok ThakurNoch keine Bewertungen

- FFM Updated AnswersDokument79 SeitenFFM Updated AnswersSrikrishnan SNoch keine Bewertungen

- CS Professional Programme Group 4Dokument42 SeitenCS Professional Programme Group 4santhoshttacsNoch keine Bewertungen

- Img 0007Dokument1 SeiteImg 0007Burt Tio CorderoNoch keine Bewertungen

- CRV - Valuation - ExerciseDokument15 SeitenCRV - Valuation - ExerciseVrutika ShahNoch keine Bewertungen

- END TermDokument3 SeitenEND TermNida MehboobNoch keine Bewertungen

- GTU Exam - Financial Management QuestionsDokument3 SeitenGTU Exam - Financial Management QuestionsMRRYNIMAVATNoch keine Bewertungen

- Sem-5 10 BCOM HONS DSE-5.2A CORPORATE-ACCOUNTING-0758Dokument5 SeitenSem-5 10 BCOM HONS DSE-5.2A CORPORATE-ACCOUNTING-0758hussain shahidNoch keine Bewertungen

- Valuation of GoodwillDokument15 SeitenValuation of Goodwillbtsa1262013Noch keine Bewertungen

- Financial Management (MBOF 912 D) 1Dokument5 SeitenFinancial Management (MBOF 912 D) 1Siva KumarNoch keine Bewertungen

- Corporate Accounting Exam QuestionsDokument6 SeitenCorporate Accounting Exam QuestionsUtkalika R SahooNoch keine Bewertungen

- Finances em 2Dokument3 SeitenFinances em 2Craaft NishiNoch keine Bewertungen

- 2018 March B.com 4th Sem SH College Autonomous March Corporate Accounting Question Paper Goodwill Tuition Centre Thevara 9846710963 9567902805Dokument4 Seiten2018 March B.com 4th Sem SH College Autonomous March Corporate Accounting Question Paper Goodwill Tuition Centre Thevara 9846710963 9567902805Rainy GoodwillNoch keine Bewertungen

- Review Questions and ProblemsDokument13 SeitenReview Questions and ProblemsLalaina EnriquezNoch keine Bewertungen

- Final Examination Questions Cover Financial, Treasury and Forex ManagementDokument5 SeitenFinal Examination Questions Cover Financial, Treasury and Forex ManagementKaran NewatiaNoch keine Bewertungen

- QP - Corporate Accounts 2012Dokument2 SeitenQP - Corporate Accounts 2012Joydip DasguptaNoch keine Bewertungen

- M3 - Valuation Question SetDokument13 SeitenM3 - Valuation Question SetHetviNoch keine Bewertungen

- Accounting Theory 6-2023-1Dokument31 SeitenAccounting Theory 6-2023-1Titu magNoch keine Bewertungen

- Bba 3 Sem AccountsDokument9 SeitenBba 3 Sem Accountsanjali LakshcarNoch keine Bewertungen

- Financial and Treasury Management Guide - Project Analysis, Working Capital, ForexDokument7 SeitenFinancial and Treasury Management Guide - Project Analysis, Working Capital, Forexexcelsis_Noch keine Bewertungen

- No Te'::': ': "I :' :: " Jl,'il, I I,, "I",,' J, L,!J'JL C A RR YDokument6 SeitenNo Te'::': ': "I :' :: " Jl,'il, I I,, "I",,' J, L,!J'JL C A RR YreliableplacementNoch keine Bewertungen

- 2820003Dokument3 Seiten2820003ruckhiNoch keine Bewertungen

- Ca-Ii May 2022Dokument6 SeitenCa-Ii May 2022Gayathri V GNoch keine Bewertungen

- Sale DeedDokument5 SeitenSale DeedNitin GoyalNoch keine Bewertungen

- Income Declaration Scheme Rules, 2016: Form 1Dokument9 SeitenIncome Declaration Scheme Rules, 2016: Form 1Nikhil KasatNoch keine Bewertungen

- Black Money BillDokument30 SeitenBlack Money BillNikhil KasatNoch keine Bewertungen

- BLack Money RulesDokument23 SeitenBLack Money RulesLive LawNoch keine Bewertungen

- Derivatives Markets in Interest Rate & Foreign Exchange RateDokument20 SeitenDerivatives Markets in Interest Rate & Foreign Exchange RatehdjfhsjfhwjfNoch keine Bewertungen

- Hedging With Financial DerivativesDokument30 SeitenHedging With Financial DerivativesNikhil KasatNoch keine Bewertungen

- DTL Sec 10Dokument14 SeitenDTL Sec 10Nikhil KasatNoch keine Bewertungen

- Types of stamps and concepts of stamp dutyDokument5 SeitenTypes of stamps and concepts of stamp dutyNikhil Kasat100% (2)

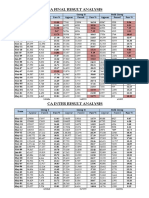

- CA Result AnalysisDokument1 SeiteCA Result AnalysisNikhil KasatNoch keine Bewertungen

- Banca SuranceDokument32 SeitenBanca SuranceNikhil KasatNoch keine Bewertungen

- Some Confusing & Debatable CSR Issues: Learning Series Vol.-I Issue - 2 2015-16Dokument21 SeitenSome Confusing & Debatable CSR Issues: Learning Series Vol.-I Issue - 2 2015-16Nikhil KasatNoch keine Bewertungen

- ApplicabiliTY of ProvisionsDokument3 SeitenApplicabiliTY of ProvisionsNikhil KasatNoch keine Bewertungen

- Delhi Dvat Registration InformationDokument4 SeitenDelhi Dvat Registration InformationNikhil KasatNoch keine Bewertungen

- Agricultural Income: Agricultural Income: - As Per Sec 10 (1) Agricultural Income Earned by TheDokument9 SeitenAgricultural Income: Agricultural Income: - As Per Sec 10 (1) Agricultural Income Earned by TheNikhil KasatNoch keine Bewertungen

- How to score 12-14 marks on Professional Ethics exam questionsDokument2 SeitenHow to score 12-14 marks on Professional Ethics exam questionsNikhil KasatNoch keine Bewertungen

- List of Indian As Convergence With IfrsDokument1 SeiteList of Indian As Convergence With IfrsNikhil KasatNoch keine Bewertungen

- Calculate Fees and Stamp Duty for Increase in Authorised Share CapitalDokument10 SeitenCalculate Fees and Stamp Duty for Increase in Authorised Share CapitalNikhil KasatNoch keine Bewertungen

- Directors Report As Per StatusDokument5 SeitenDirectors Report As Per StatusNikhil KasatNoch keine Bewertungen

- Web Base Timesheet ApplicationDokument4 SeitenWeb Base Timesheet ApplicationNikhil KasatNoch keine Bewertungen

- Curriculum VitaeDokument13 SeitenCurriculum VitaeNikhil KasatNoch keine Bewertungen

- Valuation of InventoriesDokument4 SeitenValuation of InventoriesNikhil KasatNoch keine Bewertungen

- Importance of ArticleshipDokument6 SeitenImportance of ArticleshipNikhil KasatNoch keine Bewertungen

- Anf 4dDokument3 SeitenAnf 4dNikhil KasatNoch keine Bewertungen

- August Month CompliancesDokument1 SeiteAugust Month CompliancesNikhil KasatNoch keine Bewertungen

- C01Dokument23 SeitenC01Silvery DoeNoch keine Bewertungen

- Tds On SalariesDokument55 SeitenTds On SalariespunitNoch keine Bewertungen

- Privileges To Small CompaniesDokument2 SeitenPrivileges To Small CompaniesNikhil KasatNoch keine Bewertungen

- Ind As 2015Dokument2 SeitenInd As 2015Nikhil KasatNoch keine Bewertungen

- CUSTOMS VALUATION COMPUTATIONDokument8 SeitenCUSTOMS VALUATION COMPUTATIONNikhil KasatNoch keine Bewertungen

- Series-A Investment Opportunity: International Payments Service ProviderDokument3 SeitenSeries-A Investment Opportunity: International Payments Service ProviderDhiraj KhotNoch keine Bewertungen

- FIN254 Project NSU (Excel File)Dokument6 SeitenFIN254 Project NSU (Excel File)Sirazum SaadNoch keine Bewertungen

- Accounting For Developers 101Dokument7 SeitenAccounting For Developers 101Albin StigoNoch keine Bewertungen

- Promlem Solving Problem 1: Property, Plant and Equipment (Answer Key)Dokument27 SeitenPromlem Solving Problem 1: Property, Plant and Equipment (Answer Key)Rica Regoris100% (1)

- Financial Measures: (Amazon, 2021)Dokument6 SeitenFinancial Measures: (Amazon, 2021)najeeb shajudheenNoch keine Bewertungen

- Rating Update For Apple Inc: Stock Downgraded To Above Average From GoodDokument3 SeitenRating Update For Apple Inc: Stock Downgraded To Above Average From Gooda pNoch keine Bewertungen

- Corporate Finance Cost of Capital: Dr. Avinash Ghalke, CFADokument20 SeitenCorporate Finance Cost of Capital: Dr. Avinash Ghalke, CFAmansi agrawalNoch keine Bewertungen

- Capital & Derivatives MarketDokument12 SeitenCapital & Derivatives Marketvikas_bhatia2007Noch keine Bewertungen

- Adjusting Journal EntryDokument52 SeitenAdjusting Journal EntryJenny PadillaNoch keine Bewertungen

- Lesson 1 - CAPITAL MARKETDokument16 SeitenLesson 1 - CAPITAL MARKETkim che100% (4)

- Module 2 Concept of IncomeDokument3 SeitenModule 2 Concept of IncomeNormel DecalaoNoch keine Bewertungen

- Venture CapitalDokument22 SeitenVenture CapitalRiximNoch keine Bewertungen

- Analysis and Interpretation of Financial Statements 1Dokument10 SeitenAnalysis and Interpretation of Financial Statements 1Nikolai MarasiganNoch keine Bewertungen

- Quiz RationaleDokument3 SeitenQuiz RationaleitsayuhthingNoch keine Bewertungen

- GE3 Math of Finance-FinalsDokument28 SeitenGE3 Math of Finance-FinalsMicaela EncinasNoch keine Bewertungen

- Questions FinanceDokument3 SeitenQuestions Financeanish narayanNoch keine Bewertungen

- Tax and The Taxpayer by Lord TemplemanDokument9 SeitenTax and The Taxpayer by Lord TemplemannarkooNoch keine Bewertungen

- Cambridge IGCSE: Accounting 0452/11Dokument12 SeitenCambridge IGCSE: Accounting 0452/11Tamer AhmedNoch keine Bewertungen

- Provision For DepreciationDokument10 SeitenProvision For DepreciationAsh InuNoch keine Bewertungen

- Overview of Financial ManagementDokument30 SeitenOverview of Financial ManagementDeza Mae PabataoNoch keine Bewertungen

- CLASS - B Activity - FABM2Dokument43 SeitenCLASS - B Activity - FABM2FRANCES67% (3)

- Fundamental Security AnalysisDokument21 SeitenFundamental Security AnalysisAbhisek ShawNoch keine Bewertungen

- Acc-106 Sas 5Dokument13 SeitenAcc-106 Sas 5hello millieNoch keine Bewertungen

- SBM Due Deligency Report by CADokument34 SeitenSBM Due Deligency Report by CASURANA1973Noch keine Bewertungen

- Measurement: ©2018 John Wiley & Sons Australia LTDDokument50 SeitenMeasurement: ©2018 John Wiley & Sons Australia LTDdickzcaNoch keine Bewertungen

- Chapter 5 - Worksheet and The Financial StatementsDokument21 SeitenChapter 5 - Worksheet and The Financial StatementsFrancis MateosNoch keine Bewertungen

- RIM ReportDokument23 SeitenRIM Reportsoyuz chitrakarNoch keine Bewertungen

- FNSACC507 Case Study and Practical AssessmentDokument3 SeitenFNSACC507 Case Study and Practical AssessmentnattyNoch keine Bewertungen

- VAL UE FRO M Fitn ESS: Talwalkars Better Value Fitness Limited Annual Report, 2015-16Dokument124 SeitenVAL UE FRO M Fitn ESS: Talwalkars Better Value Fitness Limited Annual Report, 2015-16ranbirholicNoch keine Bewertungen

- Izzy Trading - Transaction Entries - General Book of Accounts - SOLUTIONS-1Dokument21 SeitenIzzy Trading - Transaction Entries - General Book of Accounts - SOLUTIONS-1Franze Beatriz FLORESNoch keine Bewertungen

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Von EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Bewertung: 4.5 von 5 Sternen4.5/5 (12)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindVon EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindBewertung: 5 von 5 Sternen5/5 (231)

- Excel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetVon EverandExcel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetNoch keine Bewertungen

- The E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItVon EverandThe E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItBewertung: 5 von 5 Sternen5/5 (13)

- Love Your Life Not Theirs: 7 Money Habits for Living the Life You WantVon EverandLove Your Life Not Theirs: 7 Money Habits for Living the Life You WantBewertung: 4.5 von 5 Sternen4.5/5 (146)

- Financial Accounting - Want to Become Financial Accountant in 30 Days?Von EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Bewertung: 5 von 5 Sternen5/5 (1)

- Profit First for Therapists: A Simple Framework for Financial FreedomVon EverandProfit First for Therapists: A Simple Framework for Financial FreedomNoch keine Bewertungen

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Von EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Bewertung: 4.5 von 5 Sternen4.5/5 (5)

- Financial Accounting For Dummies: 2nd EditionVon EverandFinancial Accounting For Dummies: 2nd EditionBewertung: 5 von 5 Sternen5/5 (10)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanVon EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanBewertung: 4.5 von 5 Sternen4.5/5 (79)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesVon EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNoch keine Bewertungen

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Von EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Bewertung: 4.5 von 5 Sternen4.5/5 (14)

- Bookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesVon EverandBookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesBewertung: 4.5 von 5 Sternen4.5/5 (30)

- LLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyVon EverandLLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyBewertung: 5 von 5 Sternen5/5 (1)

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsVon EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsBewertung: 4 von 5 Sternen4/5 (7)

- Bookkeeping: A Beginner’s Guide to Accounting and Bookkeeping for Small BusinessesVon EverandBookkeeping: A Beginner’s Guide to Accounting and Bookkeeping for Small BusinessesNoch keine Bewertungen

- Project Control Methods and Best Practices: Achieving Project SuccessVon EverandProject Control Methods and Best Practices: Achieving Project SuccessNoch keine Bewertungen

- A Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineVon EverandA Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineNoch keine Bewertungen

- Basic Accounting: Service Business Study GuideVon EverandBasic Accounting: Service Business Study GuideBewertung: 5 von 5 Sternen5/5 (2)

- SAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsVon EverandSAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsNoch keine Bewertungen

- Mysap Fi Fieldbook: Fi Fieldbuch Auf Der Systeme Anwendungen Und Produkte in Der DatenverarbeitungVon EverandMysap Fi Fieldbook: Fi Fieldbuch Auf Der Systeme Anwendungen Und Produkte in Der DatenverarbeitungBewertung: 4 von 5 Sternen4/5 (1)

- Finance Basics (HBR 20-Minute Manager Series)Von EverandFinance Basics (HBR 20-Minute Manager Series)Bewertung: 4.5 von 5 Sternen4.5/5 (32)