Das könnte Ihnen auch gefallen

- Credit CreationDokument32 SeitenCredit CreationNithin VargheseNoch keine Bewertungen

- Mankiw - Money and Finansial SystemDokument37 SeitenMankiw - Money and Finansial SystemBRYAN SIANDRYNoch keine Bewertungen

- M7 MoneyDokument35 SeitenM7 MoneyJohnny SinsNoch keine Bewertungen

- Money and Financial SystemDokument37 SeitenMoney and Financial SystemTheresiaNoch keine Bewertungen

- Modern Measures of MoneyDokument6 SeitenModern Measures of MoneyCrisly-Mae Ann AquinoNoch keine Bewertungen

- Lecture No.6 (Updated - For CLASS)Dokument26 SeitenLecture No.6 (Updated - For CLASS)Deep ThinkerNoch keine Bewertungen

- The Money Supply and The Federal Reserve System: Presented by Sanchita SomDokument31 SeitenThe Money Supply and The Federal Reserve System: Presented by Sanchita SomSanchita SomNoch keine Bewertungen

- Frictional & Instrumen Kebij MoneterDokument41 SeitenFrictional & Instrumen Kebij MoneterBagus GilangNoch keine Bewertungen

- DR Neelam Tandon Chapter 3 Unit II The Concept of Money Supply 1647093903Dokument26 SeitenDR Neelam Tandon Chapter 3 Unit II The Concept of Money Supply 1647093903SPICYASHISH15374Noch keine Bewertungen

- Money - Meaning and Supply 2Dokument42 SeitenMoney - Meaning and Supply 2Alans TechnicalNoch keine Bewertungen

- CH 29Dokument36 SeitenCH 29Robelen CallantaNoch keine Bewertungen

- Ec103 Week 07 and 08 s14Dokument31 SeitenEc103 Week 07 and 08 s14юрий локтионовNoch keine Bewertungen

- Money Is Defined As Any Asset That People Are Willing To Accept in Exchange For Goods andDokument4 SeitenMoney Is Defined As Any Asset That People Are Willing To Accept in Exchange For Goods andVũ Hồng PhươngNoch keine Bewertungen

- #5 Money, Inflation & The Monetary SystemDokument22 Seiten#5 Money, Inflation & The Monetary Systemmjgx12Noch keine Bewertungen

- 3 - Money Supply and Money CreationDokument14 Seiten3 - Money Supply and Money Creationmajmmallikarachchi.mallikarachchiNoch keine Bewertungen

- The Monetary System: Prepared by FacultyDokument44 SeitenThe Monetary System: Prepared by FacultyBUSHRA ZAINABNoch keine Bewertungen

- Money, Banking, & Monetary PolicyDokument31 SeitenMoney, Banking, & Monetary PolicyAkmal HamdanNoch keine Bewertungen

- Apuntes Unit 3Dokument12 SeitenApuntes Unit 3Sara TapiaNoch keine Bewertungen

- Topic - Money & Banking System & Monetary Policy STU BDokument51 SeitenTopic - Money & Banking System & Monetary Policy STU BLai Yen FenNoch keine Bewertungen

- (Lecture 8.1) Chapter 11 Money and Financial System (L8)Dokument28 Seiten(Lecture 8.1) Chapter 11 Money and Financial System (L8)Chen Yee KhooNoch keine Bewertungen

- Major Duties and Responsibilities of Central BankDokument25 SeitenMajor Duties and Responsibilities of Central BankSakkarai ManiNoch keine Bewertungen

- Monetary Policy and Money SupplyDokument68 SeitenMonetary Policy and Money SupplypearlksrNoch keine Bewertungen

- Macroeconomics1:: The Monetary SystemDokument39 SeitenMacroeconomics1:: The Monetary SystemTy VoNoch keine Bewertungen

- Princ ch29 PresentationDokument34 SeitenPrinc ch29 PresentationSandra Hanania PasaribuNoch keine Bewertungen

- C4 - Theory of Central Bank - NHACLC - G I L PDokument23 SeitenC4 - Theory of Central Bank - NHACLC - G I L Pk60.2114310053Noch keine Bewertungen

- 3 Bank Negara, Monetary PolicyDokument67 Seiten3 Bank Negara, Monetary Policycharlie simoNoch keine Bewertungen

- Princ Ch29monetarysystem 141116093415 Conversion Gate02 PDFDokument55 SeitenPrinc Ch29monetarysystem 141116093415 Conversion Gate02 PDFDila OthmanNoch keine Bewertungen

- Chap29 PremiumDokument34 SeitenChap29 PremiumNGOC HOANG BICHNoch keine Bewertungen

- Ch30 Notetaking GuideDokument12 SeitenCh30 Notetaking Guidedrivestash528491Noch keine Bewertungen

- Money and Banking Chapter-11Dokument30 SeitenMoney and Banking Chapter-11Tanvir IslamNoch keine Bewertungen

- The Money Supply and Money MultiplierDokument22 SeitenThe Money Supply and Money MultiplierNandiniNoch keine Bewertungen

- CH 29 The Monetary SystemDokument43 SeitenCH 29 The Monetary SystemNazeNoch keine Bewertungen

- Central Bank Money Supply2017Dokument60 SeitenCentral Bank Money Supply2017Brian YehNoch keine Bewertungen

- The Money MarketDokument20 SeitenThe Money MarketNick GrzebienikNoch keine Bewertungen

- 2022 M23 Macro Chap 2 MoneyDokument35 Seiten2022 M23 Macro Chap 2 MoneyUpamanyu BasuNoch keine Bewertungen

- Major Duties and Responsibilities of Central BankDokument25 SeitenMajor Duties and Responsibilities of Central BankUyên PhươngNoch keine Bewertungen

- Money Supply NotesDokument10 SeitenMoney Supply Notesmary wanjiruNoch keine Bewertungen

- InfoDokument18 SeitenInfoKeshiva RamnathNoch keine Bewertungen

- Lecture 5 - Money and InflationDokument80 SeitenLecture 5 - Money and InflationLim Kok SeanNoch keine Bewertungen

- Princ Ch29 PresentationDokument36 SeitenPrinc Ch29 PresentationCresca Cuello CastroNoch keine Bewertungen

- The Monetary System LatestDokument31 SeitenThe Monetary System LatestDila OthmanNoch keine Bewertungen

- Chapter 29 PowerPoint StudentDokument33 SeitenChapter 29 PowerPoint StudentNhược NhượcNoch keine Bewertungen

- MACROECONOMICS, 7th. Edition N. Gregory Mankiw Mannig J. SimidianDokument21 SeitenMACROECONOMICS, 7th. Edition N. Gregory Mankiw Mannig J. SimidianAnsoy AvesNoch keine Bewertungen

- English WorksheetDokument31 SeitenEnglish WorksheetBinoy TrevadiaNoch keine Bewertungen

- Answer Key CH - Money & Banking, Government BudgetDokument11 SeitenAnswer Key CH - Money & Banking, Government Budgetrahaque01Noch keine Bewertungen

- The Money Supply Process and The Money MultipliersDokument18 SeitenThe Money Supply Process and The Money MultipliersLekhutla TFNoch keine Bewertungen

- Topic 4A-Money & BankingDokument37 SeitenTopic 4A-Money & BankingPradeep VarshneyNoch keine Bewertungen

- Money and BankingDokument7 SeitenMoney and BankingBishal GuptaNoch keine Bewertungen

- Answers To Quiz 10Dokument3 SeitenAnswers To Quiz 10Ahmad ZarwiNoch keine Bewertungen

- Slides Macroeconomics 1 - FTUDokument50 SeitenSlides Macroeconomics 1 - FTUK60 Nguyễn Ái Huyền TrangNoch keine Bewertungen

- Chapter SixDokument47 SeitenChapter SixAlmaz Getachew0% (1)

- Chapter SixDokument47 SeitenChapter SixAshenafi ZelekeNoch keine Bewertungen

- Money Supply and Money Demand: Chapter EighteenDokument16 SeitenMoney Supply and Money Demand: Chapter EighteenSharad Ranjan TyagiNoch keine Bewertungen

- Lesson 41 PDFDokument4 SeitenLesson 41 PDFSusheel KumarNoch keine Bewertungen

- Macro-C29 Monetary SystemDokument36 SeitenMacro-C29 Monetary SystemNguyen Thi Kim Ngan (K17 HCM)Noch keine Bewertungen

- Module 5Dokument65 SeitenModule 5SHIVAM SHARMANoch keine Bewertungen

- Mac 9&10Dokument51 SeitenMac 9&10Shubham DasNoch keine Bewertungen

- C4 - Money Market and Monetary PolicyDokument47 SeitenC4 - Money Market and Monetary PolicyAnh Ôn KimNoch keine Bewertungen

- Module 4 Monetary PolicyDokument29 SeitenModule 4 Monetary Policyg.prasanna saiNoch keine Bewertungen

- Lecture 7: Objectives: Topic: Investment Risk, Returns and The History of Capital MarketsDokument9 SeitenLecture 7: Objectives: Topic: Investment Risk, Returns and The History of Capital MarketsAAA820Noch keine Bewertungen

- FINS1613 S2 Yr 2013 WK 9 Cost of Capital 3 Per PageDokument9 SeitenFINS1613 S2 Yr 2013 WK 9 Cost of Capital 3 Per PageAAA820Noch keine Bewertungen

- ACCT3583 Week 10 Presentation 1Dokument19 SeitenACCT3583 Week 10 Presentation 1AAA820Noch keine Bewertungen

- IeTutorials2015s2 Ans UploadDokument34 SeitenIeTutorials2015s2 Ans UploadAAA820Noch keine Bewertungen

- Buseco Cover LetterDokument2 SeitenBuseco Cover LetterAAA820Noch keine Bewertungen

- (2013-S2) - FINS1613 - Week 09 Tutorial Solutions (From Chapter 11)Dokument9 Seiten(2013-S2) - FINS1613 - Week 09 Tutorial Solutions (From Chapter 11)AAA820Noch keine Bewertungen

- LEGT 1710 Business and The Law Assignment 2: Meaning of Property Real PropertyDokument12 SeitenLEGT 1710 Business and The Law Assignment 2: Meaning of Property Real PropertyAAA820Noch keine Bewertungen

- Week 10 Open Economy Macroeconomics: Exchange RatesDokument36 SeitenWeek 10 Open Economy Macroeconomics: Exchange RatesAAA820Noch keine Bewertungen

- Priss Compilation Macro Tute Test 2 AnswersDokument12 SeitenPriss Compilation Macro Tute Test 2 AnswersAAA820100% (1)

- FINS1613 S2 Yr 2013 WK 8 Risk Return CAPM3 Per PageDokument9 SeitenFINS1613 S2 Yr 2013 WK 8 Risk Return CAPM3 Per PageAAA820Noch keine Bewertungen

- Econ1102 Week 11Dokument21 SeitenEcon1102 Week 11AAA820Noch keine Bewertungen

- Econ1102 Week 9Dokument41 SeitenEcon1102 Week 9AAA820Noch keine Bewertungen

- Week 12 The Economy in The Long Run: Economic Growth: Reference: Bernanke, Olekalns and Frank - Chapter 10, 11Dokument30 SeitenWeek 12 The Economy in The Long Run: Economic Growth: Reference: Bernanke, Olekalns and Frank - Chapter 10, 11AAA820Noch keine Bewertungen

- Econ1102 Week 3Dokument42 SeitenEcon1102 Week 3AAA820Noch keine Bewertungen

- Econ1102 Week 2Dokument35 SeitenEcon1102 Week 2AAA820Noch keine Bewertungen

- Econ1102 Week 8Dokument46 SeitenEcon1102 Week 8AAA820100% (1)

- Econ1102 Week 4Dokument41 SeitenEcon1102 Week 4AAA820Noch keine Bewertungen

- Tute2 Sol StudentsDokument10 SeitenTute2 Sol StudentsAAA820Noch keine Bewertungen

- Econ1102 Week 5Dokument45 SeitenEcon1102 Week 5AAA820Noch keine Bewertungen

- Econ1102 Week 6Dokument53 SeitenEcon1102 Week 6AAA820Noch keine Bewertungen

- Econ1102 Week 4 (Part 2)Dokument65 SeitenEcon1102 Week 4 (Part 2)AAA820Noch keine Bewertungen

- Tut Sol Week12Dokument8 SeitenTut Sol Week12findheroNoch keine Bewertungen

- ECON1203/ECON2292 Business and Economic Statistics: Week 12Dokument10 SeitenECON1203/ECON2292 Business and Economic Statistics: Week 12AAA820Noch keine Bewertungen

- Tutorial Test Question PoolDokument6 SeitenTutorial Test Question PoolAAA820Noch keine Bewertungen

- 3 07-03-08QMB AssignmentDokument4 Seiten3 07-03-08QMB AssignmentJoseph YangNoch keine Bewertungen

- Econ1102 Week 1 RevisedDokument42 SeitenEcon1102 Week 1 RevisedAAA820Noch keine Bewertungen

- Microecon Game TheoryDokument21 SeitenMicroecon Game TheoryAAA820Noch keine Bewertungen

- Assignmenth. Hhvbjyu. GGDokument2 SeitenAssignmenth. Hhvbjyu. GGchetanphalak.instagramNoch keine Bewertungen

- Balance Confirmation Letter FD S SadushanDokument1 SeiteBalance Confirmation Letter FD S SadushanSomasundaram SadushanNoch keine Bewertungen

- Citibank N.A. - CEO Profile - Michael L. CorbatDokument1 SeiteCitibank N.A. - CEO Profile - Michael L. CorbatJ. F. El - All Rights ReservedNoch keine Bewertungen

- Spbu Note Oke DDokument6 SeitenSpbu Note Oke DrobbyNoch keine Bewertungen

- FNB Pay Slip Sep-1Dokument1 SeiteFNB Pay Slip Sep-1Arnoldz WaldemarNoch keine Bewertungen

- GHA Term 3 - 2019-2020 School Fees StructureDokument1 SeiteGHA Term 3 - 2019-2020 School Fees StructureGilbert Kamanzi100% (1)

- Promissory Note - Katherine Rose Frias - April 20, 2021Dokument5 SeitenPromissory Note - Katherine Rose Frias - April 20, 2021khate friasNoch keine Bewertungen

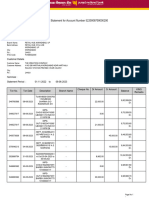

- Banking StatementDokument18 SeitenBanking StatementAshwani KumarNoch keine Bewertungen

- User StoriesDokument6 SeitenUser StoriesNextorNoch keine Bewertungen

- Viviana Power Tech PVT - Ltd.-GUJARAT: Particulars Credit DebitDokument2 SeitenViviana Power Tech PVT - Ltd.-GUJARAT: Particulars Credit DebitDhruv ParekhNoch keine Bewertungen

- Tugas AKM II Kel. 1 (Ch. 13 Current Liablities & Contigencies)Dokument7 SeitenTugas AKM II Kel. 1 (Ch. 13 Current Liablities & Contigencies)Rafika RizkiaNoch keine Bewertungen

- Acct Statement - XX9928 - 22122021Dokument49 SeitenAcct Statement - XX9928 - 22122021viveknaikNoch keine Bewertungen

- NCERT Solutions PDFDokument9 SeitenNCERT Solutions PDFShri RamNoch keine Bewertungen

- Checking AccountDokument7 SeitenChecking Accountapi-312903607Noch keine Bewertungen

- 04 BELL, Stephanie e Wray, L. Randall. Fiscal Effects On Reserves and The In-Dependence of The FedDokument11 Seiten04 BELL, Stephanie e Wray, L. Randall. Fiscal Effects On Reserves and The In-Dependence of The FedGuilherme UchimuraNoch keine Bewertungen

- Examination Question and Answers, Set C (Multiple Choice), Chapter 6 - Accounting For Merchandising BusinessDokument2 SeitenExamination Question and Answers, Set C (Multiple Choice), Chapter 6 - Accounting For Merchandising BusinessJohn Carlos Doringo100% (2)

- Project ReportDokument51 SeitenProject ReporttanmayNoch keine Bewertungen

- BankingDokument4 SeitenBankingKhatrine AtienzaNoch keine Bewertungen

- 18.arrears Interest CalculationDokument3 Seiten18.arrears Interest CalculationKingpinNoch keine Bewertungen

- Quizzes - Chapter 6 - Business Transactions & Their AnalysisDokument6 SeitenQuizzes - Chapter 6 - Business Transactions & Their AnalysisAmie Jane MirandaNoch keine Bewertungen

- ABS Market MakersDokument4 SeitenABS Market Makerschuff6675Noch keine Bewertungen

- Brihanmumbai Mahanagarpalika: Assessment and Collection Dept.Dokument7 SeitenBrihanmumbai Mahanagarpalika: Assessment and Collection Dept.Tanya GhaiNoch keine Bewertungen

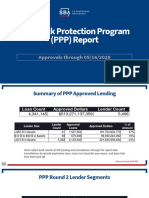

- PPP ReportDokument7 SeitenPPP ReportBrittany EtheridgeNoch keine Bewertungen

- Truth in Lending Act SlidesDokument6 SeitenTruth in Lending Act SlidesSherine Vizconde100% (1)

- SN 112105Dokument8 SeitenSN 112105wduslnNoch keine Bewertungen

- Ijrpr2769 Rural Customer Perception Towards Banking ServiceDokument6 SeitenIjrpr2769 Rural Customer Perception Towards Banking ServiceraisehellNoch keine Bewertungen

- CardsDokument17 SeitenCardsPriyal Shah100% (1)

- Solnik & McLeavey - Global Investment 6th EdDokument5 SeitenSolnik & McLeavey - Global Investment 6th Edhotmail13Noch keine Bewertungen

- HSBC London Corporate Refund Undertaking LetterDokument1 SeiteHSBC London Corporate Refund Undertaking LetterHelge Sandoy100% (3)

- ES 1 - General Guidelines On Gold LoanDokument3 SeitenES 1 - General Guidelines On Gold LoanVishnu AppuNoch keine Bewertungen