Das könnte Ihnen auch gefallen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1091)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Certified Credit Professionals PDFDokument204 SeitenCertified Credit Professionals PDFAbhinav Purty0% (1)

- Dejan Kilibarda EWCM-2Dokument12 SeitenDejan Kilibarda EWCM-2almirb7Noch keine Bewertungen

- Introduction To Financial ManagementDokument20 SeitenIntroduction To Financial ManagementAVINANDANKUMARNoch keine Bewertungen

- Shubham Gupta 47 Sec ADokument102 SeitenShubham Gupta 47 Sec AAshutosh KumarNoch keine Bewertungen

- Fiber Optic Cable Production-823233 PDFDokument67 SeitenFiber Optic Cable Production-823233 PDFravikkotaNoch keine Bewertungen

- Concor ProjectDokument51 SeitenConcor ProjectAashish AnandNoch keine Bewertungen

- Sales Presentation Method: Contd: - Need - Satisfaction Method (FAB)Dokument33 SeitenSales Presentation Method: Contd: - Need - Satisfaction Method (FAB)Ayush GargNoch keine Bewertungen

- Anandam Company Case 1Dokument11 SeitenAnandam Company Case 1Mark Vendolf Kong0% (2)

- Project Report On Operations at RetailDokument50 SeitenProject Report On Operations at RetailVamsi96% (105)

- Mintzberg's 5 Ps For StrategyDokument2 SeitenMintzberg's 5 Ps For StrategyAyush GargNoch keine Bewertungen

- CC CC CCC CCC CCCC: CC CC C C CC CDokument76 SeitenCC CC CCC CCC CCCC: CC CC C C CC CAyush GargNoch keine Bewertungen

- Personality of The Salesman: - Personal QualitiesDokument26 SeitenPersonality of The Salesman: - Personal QualitiesAyush GargNoch keine Bewertungen

- Knowledge of CustomersDokument24 SeitenKnowledge of CustomersAyush GargNoch keine Bewertungen

- Why Sales Territories ?Dokument54 SeitenWhy Sales Territories ?Ayush GargNoch keine Bewertungen

- Types of Sales QuotasDokument51 SeitenTypes of Sales QuotasAyush GargNoch keine Bewertungen

- Presentation and DemonstrationDokument35 SeitenPresentation and DemonstrationAyush GargNoch keine Bewertungen

- Handling ObjectionsDokument31 SeitenHandling ObjectionsAyush GargNoch keine Bewertungen

- Factors / Considerations: - Sales - Driving Distance - Lead Management - WorkloadDokument53 SeitenFactors / Considerations: - Sales - Driving Distance - Lead Management - WorkloadAyush GargNoch keine Bewertungen

- CloseDokument29 SeitenCloseAyush GargNoch keine Bewertungen

- Sales Management ProcessDokument58 SeitenSales Management ProcessAyush GargNoch keine Bewertungen

- Sales TerritoriesDokument55 SeitenSales TerritoriesAyush GargNoch keine Bewertungen

- Steps in Sales ForecastingDokument56 SeitenSteps in Sales ForecastingAyush GargNoch keine Bewertungen

- Quasi ContractDokument12 SeitenQuasi ContractAyush GargNoch keine Bewertungen

- 7Dokument59 Seiten7Ayush GargNoch keine Bewertungen

- Sales Management: Definition: " The Planning, Direction and Control of PersonalDokument69 SeitenSales Management: Definition: " The Planning, Direction and Control of PersonalAyush GargNoch keine Bewertungen

- Quasi ContractDokument12 SeitenQuasi ContractAyush GargNoch keine Bewertungen

- 2 Contract Act 1872Dokument43 Seiten2 Contract Act 1872Ayush GargNoch keine Bewertungen

- Jaipuria Institute of ManagementDokument1 SeiteJaipuria Institute of ManagementAyush GargNoch keine Bewertungen

- Chuong 2Dokument27 SeitenChuong 2Huỳnh Hồng HanhNoch keine Bewertungen

- 7Dokument24 Seiten7JDNoch keine Bewertungen

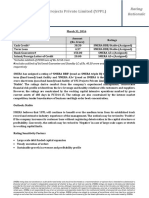

- YFC Projects Private Limited (YPPL) : Rating RationaleDokument2 SeitenYFC Projects Private Limited (YPPL) : Rating Rationalelalit rawatNoch keine Bewertungen

- Capital Budgeting - 01Dokument23 SeitenCapital Budgeting - 01ru4angelNoch keine Bewertungen

- DR Shivangee Sharma Financial Management-BBA-IBDokument68 SeitenDR Shivangee Sharma Financial Management-BBA-IBishan jainNoch keine Bewertungen

- 098060115Dokument75 Seiten098060115Sagar Paul'gNoch keine Bewertungen

- The Smithers Report: A News Digest of Activities in The Tire IndustryDokument4 SeitenThe Smithers Report: A News Digest of Activities in The Tire IndustryPrasannaNoch keine Bewertungen

- From Custumer To ValueDokument16 SeitenFrom Custumer To ValueIstiqlala AliaNoch keine Bewertungen

- Square Pharma & Beximco PharmaDokument22 SeitenSquare Pharma & Beximco PharmaSummaiya Barkat50% (2)

- Strategic Management and Business Policy Globalization Innovation and Sustainability 14th Edition Wheelen Solutions ManualDokument20 SeitenStrategic Management and Business Policy Globalization Innovation and Sustainability 14th Edition Wheelen Solutions Manualequally.ungown.q5sgg100% (15)

- Shri Mahila Griha Udyog Lijjat PapadDokument86 SeitenShri Mahila Griha Udyog Lijjat PapadpRiNcE DuDhAtRa60% (5)

- Research PaperDokument43 SeitenResearch PaperJankiNoch keine Bewertungen

- A Study On Working Capital Management With Reference To The India Cements LimitedDokument10 SeitenA Study On Working Capital Management With Reference To The India Cements LimitedEditor IJTSRDNoch keine Bewertungen

- Amazon Financial Statement Analysis PT 2 PaperDokument5 SeitenAmazon Financial Statement Analysis PT 2 Paperapi-242679288Noch keine Bewertungen

- IPO Profile of Robi Axiata Limited - PDFDokument7 SeitenIPO Profile of Robi Axiata Limited - PDFAshraf Uz ZamanNoch keine Bewertungen

- Granolite Vitrified Tiles Pvt. LTD Project Report-Prince DudhatraDokument59 SeitenGranolite Vitrified Tiles Pvt. LTD Project Report-Prince DudhatrapRiNcE DuDhAtRaNoch keine Bewertungen

- FINM CA2TabDokument27 SeitenFINM CA2TabTabrej AnsariNoch keine Bewertungen

- Anwar Physical Fitness CenterDokument32 SeitenAnwar Physical Fitness Centermuluken walelgn100% (2)

- Finals Requirement - Financial Management - Lazaro, Kate Irish MaeDokument10 SeitenFinals Requirement - Financial Management - Lazaro, Kate Irish MaeKATE IRISH MAE LAZARO0% (1)

- Cma-Vatsalya MineralsDokument13 SeitenCma-Vatsalya MineralsAtul BhandariNoch keine Bewertungen

- BKAL 1013 Chapter 7 Financial Statement AnalysisDokument67 SeitenBKAL 1013 Chapter 7 Financial Statement AnalysisWannaNoch keine Bewertungen

- Chapter 2 Working Capital ManagementDokument38 SeitenChapter 2 Working Capital Managementsuraj banNoch keine Bewertungen

- Hul Ratio AnalysisDokument14 SeitenHul Ratio Analysisvviek100% (1)