Das könnte Ihnen auch gefallen

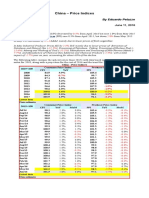

- China - Price IndicesDokument1 SeiteChina - Price IndicesEduardo PetazzeNoch keine Bewertungen

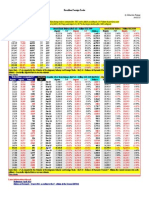

- WTI Spot PriceDokument4 SeitenWTI Spot PriceEduardo Petazze100% (1)

- México, PBI 2015Dokument1 SeiteMéxico, PBI 2015Eduardo PetazzeNoch keine Bewertungen

- Brazilian Foreign TradeDokument1 SeiteBrazilian Foreign TradeEduardo PetazzeNoch keine Bewertungen

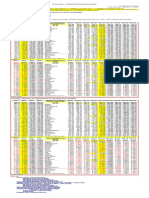

- Retail Sales in The UKDokument1 SeiteRetail Sales in The UKEduardo PetazzeNoch keine Bewertungen

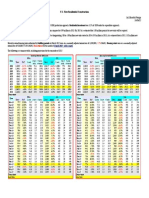

- U.S. New Residential ConstructionDokument1 SeiteU.S. New Residential ConstructionEduardo PetazzeNoch keine Bewertungen

- Euro Area - Industrial Production IndexDokument1 SeiteEuro Area - Industrial Production IndexEduardo PetazzeNoch keine Bewertungen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Economics AssignmentDokument6 SeitenEconomics Assignmenturoosa vayaniNoch keine Bewertungen

- Starbucks Coffee-In Bangladesh-MarketingDokument22 SeitenStarbucks Coffee-In Bangladesh-MarketingNusrat SharminNoch keine Bewertungen

- Local Working Instruction On Pricing GovernanceDokument16 SeitenLocal Working Instruction On Pricing GovernancemukiwanNoch keine Bewertungen

- HEALTH ECONOMICS Supply & Demand, Market EquilibriumDokument10 SeitenHEALTH ECONOMICS Supply & Demand, Market EquilibriumPao C Espi100% (1)

- 2010-2011 Q2. Compute The Following Financial Ratios For Merck's and Company Inc (December 2008)Dokument5 Seiten2010-2011 Q2. Compute The Following Financial Ratios For Merck's and Company Inc (December 2008)royaviNoch keine Bewertungen

- Boeing Market Outlook 2005Dokument39 SeitenBoeing Market Outlook 2005mdshoppNoch keine Bewertungen

- Chapter 4 Nominal and Effective Interest RateDokument42 SeitenChapter 4 Nominal and Effective Interest RateRama Krishna100% (1)

- Century: at The Right Time. at The Right PlaceDokument252 SeitenCentury: at The Right Time. at The Right PlaceGrishma JainNoch keine Bewertungen

- C37FF Week 2 Financial Statements 201617Dokument30 SeitenC37FF Week 2 Financial Statements 201617GamatNoch keine Bewertungen

- Bukit Mertajam 2014 (A)Dokument7 SeitenBukit Mertajam 2014 (A)STPMmathsNoch keine Bewertungen

- Purchase Order: Napco Modern Plastic Products Co. - Sack DivisionDokument1 SeitePurchase Order: Napco Modern Plastic Products Co. - Sack Divisionمحمد اصدNoch keine Bewertungen

- Financial Ratios NestleDokument23 SeitenFinancial Ratios NestleSehrash SashaNoch keine Bewertungen

- Assignment On InflationDokument7 SeitenAssignment On InflationKhalid Mahmood100% (4)

- Ripple V SwiftDokument10 SeitenRipple V SwiftcaiocvmNoch keine Bewertungen

- Cannon Ball Review With Exercises Part 3 PDFDokument20 SeitenCannon Ball Review With Exercises Part 3 PDFTroisNoch keine Bewertungen

- Decision AnalysisDokument2 SeitenDecision AnalysisNatalie O'Beefe LamNoch keine Bewertungen

- Ey Global Ipo Trends 2023 q3 v1Dokument17 SeitenEy Global Ipo Trends 2023 q3 v1bodnartiNoch keine Bewertungen

- 2c.purchasing Power Parity TheoryDokument9 Seiten2c.purchasing Power Parity Theoryamitkmundra100% (1)

- Retail Business Plan: Get Bagged .. .Tag A Bag..!Dokument13 SeitenRetail Business Plan: Get Bagged .. .Tag A Bag..!gurpreet gillNoch keine Bewertungen

- Market Value Appraisal: Property Exhibited To Us by The Located inDokument12 SeitenMarket Value Appraisal: Property Exhibited To Us by The Located inJennaNoch keine Bewertungen

- FINA 615 Islamic Financial Contracts - Istisna&SalamDokument17 SeitenFINA 615 Islamic Financial Contracts - Istisna&SalamFBusinessNoch keine Bewertungen

- Bcom MGKVP SlybusDokument30 SeitenBcom MGKVP SlybusHoney SrivastavaNoch keine Bewertungen

- M 14 IPCC Cost FM Guideline AnswersDokument12 SeitenM 14 IPCC Cost FM Guideline Answerssantosh barkiNoch keine Bewertungen

- Production Planning LPP CaseDokument2 SeitenProduction Planning LPP Caserinkirola7576Noch keine Bewertungen

- Forex Calendar at Forex Factory PDFDokument7 SeitenForex Calendar at Forex Factory PDFRamalingam Rathinasabapathy EllappanNoch keine Bewertungen

- Demand Estimation and ForecastingDokument31 SeitenDemand Estimation and ForecastingAnuruddha RajasuriyaNoch keine Bewertungen

- Indian Weekender Vol 6 Issue 03Dokument40 SeitenIndian Weekender Vol 6 Issue 03Indian WeekenderNoch keine Bewertungen

- 16BSP0677 Chirag Goyal OM Case Study SolutionDokument2 Seiten16BSP0677 Chirag Goyal OM Case Study SolutionChirag GoyalNoch keine Bewertungen

- EY Global Oil and Gas Reserves Study 2013Dokument112 SeitenEY Global Oil and Gas Reserves Study 2013Joao Carlos DrumondNoch keine Bewertungen

- Final Exam Set A MafDokument6 SeitenFinal Exam Set A MafZeyad Tareq Al SaroriNoch keine Bewertungen