Das könnte Ihnen auch gefallen

- Form16Dokument5 SeitenForm16er_ved06Noch keine Bewertungen

- Tax Deducted at Source: - Presented By: CA Prabhat Kumar Tandon Fca, Disa (Icai)Dokument20 SeitenTax Deducted at Source: - Presented By: CA Prabhat Kumar Tandon Fca, Disa (Icai)shefalijais6491Noch keine Bewertungen

- TDS Rates and ReturnsDokument3 SeitenTDS Rates and ReturnsKashishKumarNoch keine Bewertungen

- Form 16: Wipro LimitedDokument5 SeitenForm 16: Wipro Limiteddeepak9976Noch keine Bewertungen

- Role of PAODokument29 SeitenRole of PAOAjay DhokeNoch keine Bewertungen

- Tax Deduction at SourceDokument5 SeitenTax Deduction at SourceSarayu BhardwajNoch keine Bewertungen

- Form 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Dokument4 SeitenForm 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Kamlesh PatelNoch keine Bewertungen

- Tdsincometax (210621)Dokument3 SeitenTdsincometax (210621)Pallavi SharmaNoch keine Bewertungen

- The Rigours of TDS - An OverviewDokument31 SeitenThe Rigours of TDS - An OverviewShaleenPatniNoch keine Bewertungen

- Session 5 TDSDokument67 SeitenSession 5 TDSsinthiakarim17Noch keine Bewertungen

- Wapda Taxmemo2013Dokument50 SeitenWapda Taxmemo2013Naveed ShaheenNoch keine Bewertungen

- Tds On Foreign Remittances: Surprises Continued.Dokument9 SeitenTds On Foreign Remittances: Surprises Continued.AdityaNoch keine Bewertungen

- TDS, TCS & Advance Payment of TaxDokument54 SeitenTDS, TCS & Advance Payment of TaxFalak GoyalNoch keine Bewertungen

- CA-Ashok-Mehta - PPT - Income TaxDokument88 SeitenCA-Ashok-Mehta - PPT - Income TaxAbinash DasNoch keine Bewertungen

- Intro of TdsDokument6 SeitenIntro of Tdsshivani singhNoch keine Bewertungen

- TDS - TCSDokument55 SeitenTDS - TCSBeing HumaneNoch keine Bewertungen

- Bhubaneswar 08112015 Session I PDFDokument42 SeitenBhubaneswar 08112015 Session I PDFsachin NegiNoch keine Bewertungen

- Consequences of Tds FailureDokument2 SeitenConsequences of Tds FailureMahaveer DhelariyaNoch keine Bewertungen

- Ca. Pathik B. Shah: Value Added Tax Act 2003Dokument36 SeitenCa. Pathik B. Shah: Value Added Tax Act 2003SanjayThakkarNoch keine Bewertungen

- Tar MRL Company PDFDokument18 SeitenTar MRL Company PDFrishi Kr.Noch keine Bewertungen

- Tds Law and Practice: Under Income Tax Act, 1961Dokument84 SeitenTds Law and Practice: Under Income Tax Act, 1961Vaibhav ChauhanNoch keine Bewertungen

- TDS ElaboratedDokument80 SeitenTDS ElaboratedAncyNoch keine Bewertungen

- 74802bos60498-Cp7 (1) - UnlockedDokument136 Seiten74802bos60498-Cp7 (1) - Unlockedsinghalrachit27Noch keine Bewertungen

- Efilling ProjectDokument22 SeitenEfilling ProjectTaiyab SiddiqueNoch keine Bewertungen

- TDS Rate Financial Year 13-14Dokument10 SeitenTDS Rate Financial Year 13-14Heena AgreNoch keine Bewertungen

- What Is Tax Deducted at SourceDokument6 SeitenWhat Is Tax Deducted at SourcejdonNoch keine Bewertungen

- Tax Deducted at Source IMPORTANT POINTSDokument2 SeitenTax Deducted at Source IMPORTANT POINTSnABSAMNNoch keine Bewertungen

- Presentation+ +Manish+ShahDokument106 SeitenPresentation+ +Manish+ShahAtul PatelNoch keine Bewertungen

- Form 15CA and CB A Complete GuideDokument55 SeitenForm 15CA and CB A Complete GuideKRISHNA GOPAL YADHUVANSINoch keine Bewertungen

- Instructions ItrDokument988 SeitenInstructions ItrBalasubramanian NatarajanNoch keine Bewertungen

- Samsung India Electronics Pvt. LTD.: Signature Not VerifiedDokument7 SeitenSamsung India Electronics Pvt. LTD.: Signature Not VerifiedGajendra Singh RaghavNoch keine Bewertungen

- All About Tax Deducted at Source (TDS) - Taxguru - inDokument11 SeitenAll About Tax Deducted at Source (TDS) - Taxguru - inwaqtkeebaatein12Noch keine Bewertungen

- Deduction, Collection & Recovery of TaxesDokument143 SeitenDeduction, Collection & Recovery of TaxesjyotiNoch keine Bewertungen

- TDS Return Forms 24Q, 26Q, 27Q, 27EQ: How To Download, Due DatesDokument6 SeitenTDS Return Forms 24Q, 26Q, 27Q, 27EQ: How To Download, Due DatesJayesh WaghNoch keine Bewertungen

- Instructions For Filling Out FORM ITR-2Dokument8 SeitenInstructions For Filling Out FORM ITR-2Ganesh KumarNoch keine Bewertungen

- OLD Income Tax Performa-2021-22Dokument13 SeitenOLD Income Tax Performa-2021-22Research AccountNoch keine Bewertungen

- Tax Deducted at SourceDokument29 SeitenTax Deducted at SourceAmbar Pratik MishraNoch keine Bewertungen

- Tax Rebate Claim Form-2019Dokument2 SeitenTax Rebate Claim Form-2019Muhammad Hanif SuchwaniNoch keine Bewertungen

- Tax Deduction at Source OR: Tds/TcsDokument29 SeitenTax Deduction at Source OR: Tds/TcsArka PramanikNoch keine Bewertungen

- Prerequisites in E-Filing Income Tax Returns: Dr. Kailash KalyaniDokument62 SeitenPrerequisites in E-Filing Income Tax Returns: Dr. Kailash KalyaniRicha KalyaniNoch keine Bewertungen

- Tax Audit ChecklistDokument3 SeitenTax Audit Checklisthemanth0% (1)

- SET 23 24 Detail Guide EDokument20 SeitenSET 23 24 Detail Guide ENishan MahanamaNoch keine Bewertungen

- Overview of TDS: by C.A. Manish JathliyaDokument21 SeitenOverview of TDS: by C.A. Manish JathliyaHasan Babu KothaNoch keine Bewertungen

- ITR1 - Part 3 (How To Download 26AS)Dokument8 SeitenITR1 - Part 3 (How To Download 26AS)gaurav gargNoch keine Bewertungen

- Income Tax Refund PDFDokument3 SeitenIncome Tax Refund PDFArunDaniel100% (1)

- TDS Return FilingDokument34 SeitenTDS Return FilingCABRAJJHANoch keine Bewertungen

- Tds ProvisionsDokument38 SeitenTds Provisionsglobalfreedom4Noch keine Bewertungen

- Income Tax Law & Practice Unit 4Dokument8 SeitenIncome Tax Law & Practice Unit 4MuskanNoch keine Bewertungen

- Requirements U/S 195: By: Ca Sanjay K. AgarwalDokument71 SeitenRequirements U/S 195: By: Ca Sanjay K. AgarwalHemanthKumarNoch keine Bewertungen

- FKMPS9021Q Q3 2016-17Dokument2 SeitenFKMPS9021Q Q3 2016-17Hannan SatopayNoch keine Bewertungen

- Instructions ITR5 AY2021 22Dokument196 SeitenInstructions ITR5 AY2021 22Nikhil KumarNoch keine Bewertungen

- TDS Rate Chart PDFDokument2 SeitenTDS Rate Chart PDFjdhamdeep07Noch keine Bewertungen

- Tds Rate Chart Fy 2014-15 Ay 2015-16Dokument26 SeitenTds Rate Chart Fy 2014-15 Ay 2015-16shivashankari86Noch keine Bewertungen

- Form No. 16A: From ToDokument2 SeitenForm No. 16A: From ToAstro Shalleneder GoyalNoch keine Bewertungen

- Tax Planning and ManagementDokument12 SeitenTax Planning and Managementayushi chandraNoch keine Bewertungen

- Instructions ITR2 AY2021 22Dokument125 SeitenInstructions ITR2 AY2021 22Help Tubestar CrewNoch keine Bewertungen

- Presentation On Taxation To The Construction Industry Federation of Zimbabwe (Cifoz)Dokument44 SeitenPresentation On Taxation To The Construction Industry Federation of Zimbabwe (Cifoz)Franco DurantNoch keine Bewertungen

- Form 16 ADokument23 SeitenForm 16 Amlkhantwal8404Noch keine Bewertungen

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineVon EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNoch keine Bewertungen

- TDS Presentation Taxguru - inDokument35 SeitenTDS Presentation Taxguru - inBj Thivagar0% (2)

- TDS Presentation Taxguru - inDokument35 SeitenTDS Presentation Taxguru - inBj Thivagar0% (2)

- Name of The Economists and Their ContributionDokument4 SeitenName of The Economists and Their ContributionBj Thivagar100% (1)

- ISRO Exam Paper-2006-Paper-1Dokument9 SeitenISRO Exam Paper-2006-Paper-1sukesh564Noch keine Bewertungen

- April AndhimazhaiDokument68 SeitenApril AndhimazhaiBj ThivagarNoch keine Bewertungen

- Pipeline Sales KolDokument3 SeitenPipeline Sales KolBj ThivagarNoch keine Bewertungen

- The Origins of OpennessDokument7 SeitenThe Origins of Opennesssree harshaNoch keine Bewertungen

- April AndhimazhaiDokument68 SeitenApril AndhimazhaiBj ThivagarNoch keine Bewertungen

- RRCMASDokument1 SeiteRRCMASBj ThivagarNoch keine Bewertungen

- Timber Rate Feb 13Dokument6 SeitenTimber Rate Feb 13Bj ThivagarNoch keine Bewertungen

- New Office Agreement1Dokument6 SeitenNew Office Agreement1Bj ThivagarNoch keine Bewertungen

- WB00114IDokument1 SeiteWB00114IBj ThivagarNoch keine Bewertungen

- How To Prepare Group1 Group2Dokument16 SeitenHow To Prepare Group1 Group2eshwariee100% (1)

- IF Function in ExcelDokument3 SeitenIF Function in ExcelBj ThivagarNoch keine Bewertungen

- About CCCLDokument2 SeitenAbout CCCLBj ThivagarNoch keine Bewertungen

- Yanai Doctor FinalDokument49 SeitenYanai Doctor FinalBj Thivagar100% (1)

- Admission FormDokument2 SeitenAdmission FormBj ThivagarNoch keine Bewertungen

- Jayakanthan Sirukathaigal - Part3Dokument83 SeitenJayakanthan Sirukathaigal - Part3முரளி கிருஷ்ணன் alias முகி100% (5)

- Admission FormDokument2 SeitenAdmission FormBj ThivagarNoch keine Bewertungen

- ScienceDokument6 SeitenSciencejyuvarajeeeNoch keine Bewertungen

- Trial BalanceDokument1 SeiteTrial BalanceBj ThivagarNoch keine Bewertungen

- Tally QuestionDokument1 SeiteTally QuestionBj ThivagarNoch keine Bewertungen

- Factoring 101 - An Introduction To Factoring - The Basics You Need To Know (US)Dokument18 SeitenFactoring 101 - An Introduction To Factoring - The Basics You Need To Know (US)timlea50100% (5)

- Ch05 TB Hoggetta8eDokument18 SeitenCh05 TB Hoggetta8eAlex Schuldiner100% (2)

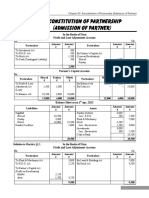

- 03 Reconstitution of Partnership Admission of Partner PDFDokument24 Seiten03 Reconstitution of Partnership Admission of Partner PDFBrawler Stars100% (3)

- QGEP Investor Presentation NDR Dez17 VFDokument25 SeitenQGEP Investor Presentation NDR Dez17 VFkarlGGNoch keine Bewertungen

- Partnership FirmDokument9 SeitenPartnership FirmLowlyLutfur100% (1)

- Managing Finance in Health and Social CareDokument26 SeitenManaging Finance in Health and Social CareShaji Viswanathan. Mcom, MBA (U.K)Noch keine Bewertungen

- Trucking Operations in IndiaDokument290 SeitenTrucking Operations in IndiaRahul AGJNoch keine Bewertungen

- Ignou Bright Future For YouDokument22 SeitenIgnou Bright Future For YouAnshooman RayNoch keine Bewertungen

- HDFC Bank ProfileDokument6 SeitenHDFC Bank ProfileARDRA VASUDEVNoch keine Bewertungen

- Master Circular - Disbursement of Government Pension by Agency BanksDokument12 SeitenMaster Circular - Disbursement of Government Pension by Agency BanksSrinivaasNoch keine Bewertungen

- What Do Banks Do - What Should They Do - and What Policies Are Needed To Ensure Best Results For The Real EconomyDokument31 SeitenWhat Do Banks Do - What Should They Do - and What Policies Are Needed To Ensure Best Results For The Real EconomyjoebloggsscribdNoch keine Bewertungen

- SALES - BAR EXAM Q&A SelectedDokument24 SeitenSALES - BAR EXAM Q&A Selectedian clark MarinduqueNoch keine Bewertungen

- PDFDokument1 SeitePDFJohn BatorNoch keine Bewertungen

- Plants, Property and EquipmentDokument21 SeitenPlants, Property and EquipmentAna Mae HernandezNoch keine Bewertungen

- Century Properties Group, Inc ReportDokument38 SeitenCentury Properties Group, Inc Reportカイ みゆきNoch keine Bewertungen

- Free Elective Exercise No. 1-BalancedDokument17 SeitenFree Elective Exercise No. 1-BalancedLoi PanlaquiNoch keine Bewertungen

- NPA NotesDokument33 SeitenNPA NotesAdv Sheetal SaylekarNoch keine Bewertungen

- KIM Cum Appln Form Reliance Fixed Horizon Fund XXXX Series 15 PDFDokument24 SeitenKIM Cum Appln Form Reliance Fixed Horizon Fund XXXX Series 15 PDFarvind gaikwadNoch keine Bewertungen

- Making The Law Work For Everyone Vol IDokument106 SeitenMaking The Law Work For Everyone Vol IStefanos VazakasNoch keine Bewertungen

- Mba I Accounting For Management (14mba13) NotesDokument58 SeitenMba I Accounting For Management (14mba13) NotesAnonymous 4lXDgDUkQ100% (2)

- Corporate Tax ProblemsDokument21 SeitenCorporate Tax Problemsnavtej02Noch keine Bewertungen

- CIR Vs Filinvest DigestDokument17 SeitenCIR Vs Filinvest DigestJImlan Sahipa IsmaelNoch keine Bewertungen

- GlossaryDokument45 SeitenGlossarysilvi88Noch keine Bewertungen

- Article 1177 - ObliconDokument11 SeitenArticle 1177 - ObliconJaysonMahilumQuilbanNoch keine Bewertungen

- Valuation CA Final Financial Reporting JNPPJTL4Dokument1.266 SeitenValuation CA Final Financial Reporting JNPPJTL4rahulNoch keine Bewertungen

- Business Junior CertDokument9 SeitenBusiness Junior CertCathal O' GaraNoch keine Bewertungen

- Question For Manager Test in KsfeDokument11 SeitenQuestion For Manager Test in KsfeVimalKumar50% (2)

- WRX Body and Paint, Inc.Dokument4 SeitenWRX Body and Paint, Inc.makelipaNoch keine Bewertungen

- Standalone & Consolidated Financial Results, Auditors Report For March 31, 2016 (Result)Dokument16 SeitenStandalone & Consolidated Financial Results, Auditors Report For March 31, 2016 (Result)Shyam SunderNoch keine Bewertungen

- HP 17bII+ Financial Calculator ManualDokument309 SeitenHP 17bII+ Financial Calculator ManualBrooks KincaidNoch keine Bewertungen