Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The State of e Wallets and Digital Payments in India 2018Dokument10 SeitenThe State of e Wallets and Digital Payments in India 2018Paridhi GolchhaNoch keine Bewertungen

- Clean N Clear AdjustedDokument41 SeitenClean N Clear AdjustedSami Hasan29% (7)

- ECS Holdings Limited Annual Report 2013Dokument56 SeitenECS Holdings Limited Annual Report 2013WeR1 Consultants Pte LtdNoch keine Bewertungen

- Chanel N5 INDIA Language Translations BriefDokument28 SeitenChanel N5 INDIA Language Translations BriefParidhi GolchhaNoch keine Bewertungen

- ALL IS WELL-Its Just The Beginning!!Dokument1 SeiteALL IS WELL-Its Just The Beginning!!Paridhi GolchhaNoch keine Bewertungen

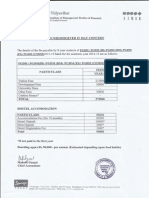

- Fees Structure 2014-15Dokument1 SeiteFees Structure 2014-15Paridhi GolchhaNoch keine Bewertungen

- Sunsilk 3dot Occidental Font CascadeDokument9 SeitenSunsilk 3dot Occidental Font CascadeParidhi GolchhaNoch keine Bewertungen

- Brand Wars: Rin V/S TideDokument9 SeitenBrand Wars: Rin V/S TideParidhi GolchhaNoch keine Bewertungen

- Ib WipDokument48 SeitenIb WipParidhi GolchhaNoch keine Bewertungen

- MM 2 ProjectDokument10 SeitenMM 2 ProjectParidhi GolchhaNoch keine Bewertungen

- McDonald Strategies.Dokument21 SeitenMcDonald Strategies.arslan_iqbal88100% (10)

- 44 Paridhi Golchha Bharti AirtelDokument19 Seiten44 Paridhi Golchha Bharti AirtelParidhi GolchhaNoch keine Bewertungen

- Extra ClassDokument2 SeitenExtra ClassParidhi GolchhaNoch keine Bewertungen

- PGDM-Comm 44 Paridhi GolchhaDokument20 SeitenPGDM-Comm 44 Paridhi GolchhaParidhi GolchhaNoch keine Bewertungen

- Business Communications SyllabusDokument2 SeitenBusiness Communications SyllabusParidhi GolchhaNoch keine Bewertungen

- Book 1Dokument3 SeitenBook 1Paridhi GolchhaNoch keine Bewertungen

- Display The Names and ContactDokument2 SeitenDisplay The Names and ContactParidhi GolchhaNoch keine Bewertungen

- BR For DummiesDokument16 SeitenBR For DummiesParidhi GolchhaNoch keine Bewertungen

- CommunicationDokument17 SeitenCommunicationParidhi GolchhaNoch keine Bewertungen

- Accounting PrinciplesDokument11 SeitenAccounting PrinciplesParidhi GolchhaNoch keine Bewertungen

- CVDokument1 SeiteCVParidhi GolchhaNoch keine Bewertungen

- CommunicationDokument17 SeitenCommunicationParidhi GolchhaNoch keine Bewertungen

- No More EscapeDokument1 SeiteNo More EscapeParidhi GolchhaNoch keine Bewertungen

- CommunicationDokument17 SeitenCommunicationParidhi GolchhaNoch keine Bewertungen

- CommunicationDokument17 SeitenCommunicationParidhi GolchhaNoch keine Bewertungen

- CommunicationDokument17 SeitenCommunicationParidhi GolchhaNoch keine Bewertungen

- QSPM Matrix (DELL)Dokument22 SeitenQSPM Matrix (DELL)Anu Sohail100% (3)

- FIN604 - HW03 - Farhan Zubair - 18164052Dokument9 SeitenFIN604 - HW03 - Farhan Zubair - 18164052ZNoch keine Bewertungen

- Term SheetDokument16 SeitenTerm SheetParesh DaveNoch keine Bewertungen

- Auditing and AssuranceDokument8 SeitenAuditing and Assurancebichngoc leNoch keine Bewertungen

- Solved Hahn Flooring Company S Perpetual Inventory Records Indicate That 1 333 150 ofDokument1 SeiteSolved Hahn Flooring Company S Perpetual Inventory Records Indicate That 1 333 150 ofAnbu jaromiaNoch keine Bewertungen

- Cpa Review School of The Philippines Manila Advanced Financial Accounting and Reporting First Preboard Examination SolutionsDokument12 SeitenCpa Review School of The Philippines Manila Advanced Financial Accounting and Reporting First Preboard Examination SolutionsSophia PerezNoch keine Bewertungen

- Msniaga Annualreport2009 (2.4mb)Dokument115 SeitenMsniaga Annualreport2009 (2.4mb)ArifTapoosiNoch keine Bewertungen

- Calzado en España StatistaDokument65 SeitenCalzado en España StatistaPaula Calvo ZaragozanoNoch keine Bewertungen

- Financial Analysis Steel Authority of India Limited (SAIL)Dokument86 SeitenFinancial Analysis Steel Authority of India Limited (SAIL)Saurabh Marwah33% (6)

- Final Business PlanDokument16 SeitenFinal Business PlanMariae JalandoonNoch keine Bewertungen

- 1Dokument13 Seiten1gamalbedNoch keine Bewertungen

- ADVACC3 ATsDokument5 SeitenADVACC3 ATsgazer beam100% (1)

- Lesson 3 Financing PDFDokument20 SeitenLesson 3 Financing PDFAngelita Dela cruzNoch keine Bewertungen

- Chapter # 2 Financial AnalysisDokument94 SeitenChapter # 2 Financial Analysiswondosen birhanuNoch keine Bewertungen

- January 31: Birendra Mahato Adjusting Entries and WorksheetDokument17 SeitenJanuary 31: Birendra Mahato Adjusting Entries and WorksheetAjit UpretyNoch keine Bewertungen

- Discontinued OperationsDokument2 SeitenDiscontinued OperationsBwwwiiiiiNoch keine Bewertungen

- Question and Answer FOR JUNE 2018Dokument86 SeitenQuestion and Answer FOR JUNE 2018Simbarashe ChigwendeNoch keine Bewertungen

- Analyzing Operating ActivitiesDokument38 SeitenAnalyzing Operating ActivitiesindahmuliasariNoch keine Bewertungen

- Ud Mardelco ExcelDokument1 SeiteUd Mardelco Excelfaid sugiartoNoch keine Bewertungen

- Chapter 9Dokument26 SeitenChapter 9Maha BashirNoch keine Bewertungen

- Mgt401solvedsubjectivefinalterm PDFDokument13 SeitenMgt401solvedsubjectivefinalterm PDFengr_alihussain02Noch keine Bewertungen

- MCS-Transfer Pricing - FinalDokument74 SeitenMCS-Transfer Pricing - FinalHarsh N. DhruvaNoch keine Bewertungen

- Confidence CementDokument17 SeitenConfidence Cementnahidul202Noch keine Bewertungen

- Practice Problem 2Dokument5 SeitenPractice Problem 2panda 1Noch keine Bewertungen

- Financial Analysis - HotstarDokument5 SeitenFinancial Analysis - Hotstarabhi vermaNoch keine Bewertungen

- Port Folio Number - 2007-MASDokument8 SeitenPort Folio Number - 2007-MASAndreaNoch keine Bewertungen

- Financial Statement Analysis & Security Valuation (Fifth Edition)Dokument46 SeitenFinancial Statement Analysis & Security Valuation (Fifth Edition)arunjangra566Noch keine Bewertungen

- The Role of Related Party Transactions in Fraudulent Financial ReportingDokument39 SeitenThe Role of Related Party Transactions in Fraudulent Financial ReportingFelipe Augusto CuryNoch keine Bewertungen

- Taxflash: Tax Indonesia / June 2018 / No.07Dokument3 SeitenTaxflash: Tax Indonesia / June 2018 / No.07Daisy Anita SusiloNoch keine Bewertungen