Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Assessment Formal AssessmentDokument7 SeitenAssessment Formal Assessmentashish100% (1)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- FGV Holding BHDDokument106 SeitenFGV Holding BHDNoor Syahidatul Fatimy90% (10)

- Excel Instructions CAUTION: Read Appendix A For Specific Instructions Relating To These TemplatesDokument40 SeitenExcel Instructions CAUTION: Read Appendix A For Specific Instructions Relating To These TemplatesEmily Cerney40% (5)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Printing of Case Form 0500Dokument2 SeitenPrinting of Case Form 0500Hanabishi RekkaNoch keine Bewertungen

- Practical Questions: Strategic Financial ManagementDokument50 SeitenPractical Questions: Strategic Financial ManagementRITZ BROWNNoch keine Bewertungen

- I 04.05studentDokument20 SeitenI 04.05studentKhánh Huyền0% (2)

- 450 499 PDFDokument44 Seiten450 499 PDFSamuelNoch keine Bewertungen

- Test Bank For Government and Not For Profit Accounting Concepts and Practices 5th Edition GranofDokument15 SeitenTest Bank For Government and Not For Profit Accounting Concepts and Practices 5th Edition Granofsamuel debebe100% (1)

- Basic Terminal ValueDokument4 SeitenBasic Terminal ValueVinNoch keine Bewertungen

- Cash Flow StatementDokument4 SeitenCash Flow StatementRavina Singh100% (1)

- Final Projact of Cost ButgetDokument35 SeitenFinal Projact of Cost ButgetDeepika KalimuthuNoch keine Bewertungen

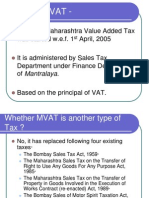

- Maharashtra Value Added Taxact, 2002 (Mvat) : Basic Concepts: Vivek College of CommerceDokument35 SeitenMaharashtra Value Added Taxact, 2002 (Mvat) : Basic Concepts: Vivek College of CommerceDeepika KalimuthuNoch keine Bewertungen

- University of Mumbai RM Sem 4Dokument5 SeitenUniversity of Mumbai RM Sem 4Deepika KalimuthuNoch keine Bewertungen

- University of Mumbai RM Sem 4Dokument5 SeitenUniversity of Mumbai RM Sem 4Deepika KalimuthuNoch keine Bewertungen

- Wipro's Audit Repo Add IntroDokument33 SeitenWipro's Audit Repo Add IntroDeepika KalimuthuNoch keine Bewertungen

- Financial 1Dokument41 SeitenFinancial 1Deepika KalimuthuNoch keine Bewertungen

- FM Ratio ProjectDokument39 SeitenFM Ratio ProjectDeepika KalimuthuNoch keine Bewertungen

- 634357469811641250Dokument23 Seiten634357469811641250Deepika KalimuthuNoch keine Bewertungen

- Projectonshampoo 101107134213 Phpapp01 DeepikaDokument30 SeitenProjectonshampoo 101107134213 Phpapp01 DeepikaDeepika KalimuthuNoch keine Bewertungen

- Projectonshampoo 101107134213 Phpapp01 DeepikaDokument30 SeitenProjectonshampoo 101107134213 Phpapp01 DeepikaDeepika KalimuthuNoch keine Bewertungen

- Indirect Taxes: Matushri Pushpaben Vinubhai Valia College of Commerce (Affiliated To University of Mumbai)Dokument20 SeitenIndirect Taxes: Matushri Pushpaben Vinubhai Valia College of Commerce (Affiliated To University of Mumbai)Deepika KalimuthuNoch keine Bewertungen

- Consumer Behaviour Towards Shampoos: Vivek College of CommersDokument37 SeitenConsumer Behaviour Towards Shampoos: Vivek College of CommersDeepika KalimuthuNoch keine Bewertungen

- Deepika ShampooDokument8 SeitenDeepika ShampooThilaga Senthilmurugan100% (1)

- FM Ratio ProjectDokument39 SeitenFM Ratio ProjectDeepika KalimuthuNoch keine Bewertungen

- 1Dokument1 Seite1Deepika KalimuthuNoch keine Bewertungen

- Consumer Behaviour: Business PurposeDokument30 SeitenConsumer Behaviour: Business PurposeDeepika KalimuthuNoch keine Bewertungen

- Salary IncomeDokument8 SeitenSalary IncomeAshis karmakarNoch keine Bewertungen

- Tax ProDokument34 SeitenTax ProDeepika KalimuthuNoch keine Bewertungen

- Business Strategy For ITC LTDDokument32 SeitenBusiness Strategy For ITC LTDDeepika KalimuthuNoch keine Bewertungen

- Finance PROJECT REPORT ON "COMPARATIVE STUDY OF TOP THREE BANKS OF INDIA"Dokument32 SeitenFinance PROJECT REPORT ON "COMPARATIVE STUDY OF TOP THREE BANKS OF INDIA"Deepika KalimuthuNoch keine Bewertungen

- Simple Numbers Presentation Slides 031815Dokument58 SeitenSimple Numbers Presentation Slides 031815Pablo HuescaNoch keine Bewertungen

- BIR Form No. 0901-D DividendsDokument2 SeitenBIR Form No. 0901-D DividendsKoji ZerofourNoch keine Bewertungen

- Diwali Picks: A Touch of Light To Your WealthDokument30 SeitenDiwali Picks: A Touch of Light To Your WealthADNoch keine Bewertungen

- Bonner Family Wealth BlueprintDokument7 SeitenBonner Family Wealth Blueprintmary welch100% (3)

- Responsibility Accounting and Transfer Pricing: Illustrative Problem 13.1 Evaluation of A Cost CenterDokument4 SeitenResponsibility Accounting and Transfer Pricing: Illustrative Problem 13.1 Evaluation of A Cost CenterTsundere DoradoNoch keine Bewertungen

- Vonovia 9M2021 Presentation 20211118Dokument76 SeitenVonovia 9M2021 Presentation 20211118LorenzoNoch keine Bewertungen

- Taxation of Income Earned From Selling SharesDokument5 SeitenTaxation of Income Earned From Selling Sharesphani raja kumarNoch keine Bewertungen

- TAX517 - Feb 2022Dokument14 SeitenTAX517 - Feb 2022IZZAH FAQIHAH AHMAD HARRISNoch keine Bewertungen

- Activity 1Dokument2 SeitenActivity 1Cristine Joy BenitezNoch keine Bewertungen

- CH 7Dokument41 SeitenCH 7Abdulrahman AlotaibiNoch keine Bewertungen

- Verification of Assets and Liabilities: Basic ConceptsDokument59 SeitenVerification of Assets and Liabilities: Basic ConceptsHarikrishnaNoch keine Bewertungen

- Leverage PPTDokument13 SeitenLeverage PPTamdNoch keine Bewertungen

- Completing The Accounting Cycle: © 2009 The Mcgraw-Hill Companies, Inc., All Rights ReservedDokument57 SeitenCompleting The Accounting Cycle: © 2009 The Mcgraw-Hill Companies, Inc., All Rights ReservedPham Thi Hoa (K14 DN)Noch keine Bewertungen

- Unit 18 Pricing of Bank Products and Services: ObjectivesDokument17 SeitenUnit 18 Pricing of Bank Products and Services: Objectivesrishabh_arora@live.comNoch keine Bewertungen

- Shree Renuka Sugars LTDDokument103 SeitenShree Renuka Sugars LTDsaikrishna858Noch keine Bewertungen

- Credit Statement (Form 26AS) OnlineDokument8 SeitenCredit Statement (Form 26AS) Onlinemevrick_guyNoch keine Bewertungen

- India Consumer: Wallet Watch - Vol 1/12Dokument6 SeitenIndia Consumer: Wallet Watch - Vol 1/12Rahul GanapathyNoch keine Bewertungen

- Financial Reporting and Analysis PDFDokument1 SeiteFinancial Reporting and Analysis PDFsaruyaNoch keine Bewertungen

- Factors Affecting Tax Compliance Behaviour in SelfDokument10 SeitenFactors Affecting Tax Compliance Behaviour in SelfZhakia IrianaNoch keine Bewertungen

- Module 4 Adjusting EntriesDokument41 SeitenModule 4 Adjusting EntriesXiavNoch keine Bewertungen