Das könnte Ihnen auch gefallen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- Pharmaceutical Business PlanDokument23 SeitenPharmaceutical Business PlanMohan KrishnaNoch keine Bewertungen

- A User's Guide To The CDM: (Clean Development Mechanism)Dokument89 SeitenA User's Guide To The CDM: (Clean Development Mechanism)Mohan KrishnaNoch keine Bewertungen

- 1.2c&3bAditionalityMorocco ElkhamlichiDokument21 Seiten1.2c&3bAditionalityMorocco ElkhamlichiMohan KrishnaNoch keine Bewertungen

- AEC Course Content PDFDokument11 SeitenAEC Course Content PDFMohan KrishnaNoch keine Bewertungen

- Umpp Greener Future121015 PDFDokument68 SeitenUmpp Greener Future121015 PDFMohan KrishnaNoch keine Bewertungen

- ETABS-Example-RC Building Seismic Load - Time HistoryDokument59 SeitenETABS-Example-RC Building Seismic Load - Time HistoryMauricio_Vera_5259100% (15)

- STAAD Pro 2006 Getting Started TutorialsDokument575 SeitenSTAAD Pro 2006 Getting Started TutorialsAhmed AdelNoch keine Bewertungen

- Solarpv ChecklistDokument6 SeitenSolarpv ChecklistMohan KrishnaNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- AQAP-2105 (E) (NATO Req For Quality Plans)Dokument13 SeitenAQAP-2105 (E) (NATO Req For Quality Plans)Bahadır HarmancıNoch keine Bewertungen

- DOJ OIG Audit of The Bureau of Alcohol, Tobacco, Firearms and Explosives Controls Over Weapons, Munitions, and ExplosivesDokument42 SeitenDOJ OIG Audit of The Bureau of Alcohol, Tobacco, Firearms and Explosives Controls Over Weapons, Munitions, and ExplosivesBeverly TranNoch keine Bewertungen

- Human Resources Specialist Administrator in Washington DC Resume Hirut ThompsonDokument2 SeitenHuman Resources Specialist Administrator in Washington DC Resume Hirut ThompsonHirutThompsonNoch keine Bewertungen

- Chapter 6 - Test BankDokument64 SeitenChapter 6 - Test Bankjuan80% (5)

- 2014 Kroll ABC ReportDokument32 Seiten2014 Kroll ABC ReportAnonymous Hnv6u54HNoch keine Bewertungen

- Feliciano v. Commission On Audit - Full TextDokument8 SeitenFeliciano v. Commission On Audit - Full TextDino Bernard LapitanNoch keine Bewertungen

- RIBA Quality Management System - Procedures ManualDokument94 SeitenRIBA Quality Management System - Procedures ManualbrunoNoch keine Bewertungen

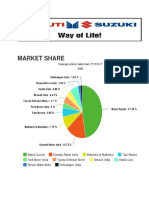

- Maruti Suzuki India LimitedDokument17 SeitenMaruti Suzuki India LimitedDinesh KumarNoch keine Bewertungen

- Dustin Howard ResumeDokument2 SeitenDustin Howard Resumeapi-270856726Noch keine Bewertungen

- UL Refresher Course in Accountancy Auditing - Module 2.3.1: PSA 330 The Auditor'S Responses To Assessed RisksDokument13 SeitenUL Refresher Course in Accountancy Auditing - Module 2.3.1: PSA 330 The Auditor'S Responses To Assessed RisksLOUISE ELIJAH GACUANNoch keine Bewertungen

- Alvin A.arens - Chapter 16Dokument40 SeitenAlvin A.arens - Chapter 16Nhung Kiều100% (1)

- Acctg 17nd-Final Exam ADokument14 SeitenAcctg 17nd-Final Exam AKristinelle AragoNoch keine Bewertungen

- Vessel Performance: Technical Solutions For Operational ChallengesDokument8 SeitenVessel Performance: Technical Solutions For Operational Challengesshahjada100% (1)

- SBD Works (ICB) - November-FinalDokument154 SeitenSBD Works (ICB) - November-FinalHabtamu Desalegn75% (4)

- CA. Sarthak Jain: CARO, 2020Dokument3 SeitenCA. Sarthak Jain: CARO, 2020Kushagra BurmanNoch keine Bewertungen

- Quiz Bowlers' Society Auditing TheoryDokument8 SeitenQuiz Bowlers' Society Auditing TheorysarahbeeNoch keine Bewertungen

- Basic Overview of Various Aspects of An IT ProjectDokument65 SeitenBasic Overview of Various Aspects of An IT ProjectAbhijit Khare0% (1)

- Aqap 2110 2016 Eng DataDokument32 SeitenAqap 2110 2016 Eng DataOTK Micro-FixNoch keine Bewertungen

- Asn 2 736 FinalDokument23 SeitenAsn 2 736 Finalqh11022003Noch keine Bewertungen

- Ias Ac-98 Accreditation Criteria For Inspection AgenciesDokument4 SeitenIas Ac-98 Accreditation Criteria For Inspection AgenciesMario RodriguezNoch keine Bewertungen

- Chapter 26 FinalDokument3 SeitenChapter 26 FinalLenlen VersozaNoch keine Bewertungen

- Internal Audit Charter PDFDokument4 SeitenInternal Audit Charter PDFAishah Al NahyanNoch keine Bewertungen

- Analysis of Global Non-OIC Best Cases Customs Risk ManagementDokument26 SeitenAnalysis of Global Non-OIC Best Cases Customs Risk ManagementRio Jalu PamungkasNoch keine Bewertungen

- Audit Manual Part1Dokument250 SeitenAudit Manual Part1Romer Lesondato100% (2)

- RSP21Dokument8 SeitenRSP21gueridiNoch keine Bewertungen

- Wilmington HA - Audit March 2018Dokument92 SeitenWilmington HA - Audit March 2018Ben SchachtmanNoch keine Bewertungen

- Accounting Thesis ExamplesDokument8 SeitenAccounting Thesis ExamplesWriteMyMathPaperSingapore100% (2)

- Risks Due To Convergence of Physical Security SystemsDokument5 SeitenRisks Due To Convergence of Physical Security SystemsMuhammad Dawood Abu AnasNoch keine Bewertungen

- Audit Programme For Accounts ReceivableDokument5 SeitenAudit Programme For Accounts ReceivableDaniela BulardaNoch keine Bewertungen

- FSC-PRO-20-001 V1-1 en Evaluation of FSC Values Health and Safety in CoCDokument10 SeitenFSC-PRO-20-001 V1-1 en Evaluation of FSC Values Health and Safety in CoCfcjr79Noch keine Bewertungen