Das könnte Ihnen auch gefallen

- Construction Contract Practice and ManagementDokument89 SeitenConstruction Contract Practice and ManagementArifNoch keine Bewertungen

- Cost AccntgDokument36 SeitenCost AccntgRoselynne GatbontonNoch keine Bewertungen

- ITC Product MixDokument47 SeitenITC Product MixMohit Malviya67% (3)

- Cost AccountingDokument14 SeitenCost Accountingkiros100% (1)

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageVon EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageBewertung: 5 von 5 Sternen5/5 (1)

- Modul Akuntansi Manajemen (TM2)Dokument12 SeitenModul Akuntansi Manajemen (TM2)Aurelique NatalieNoch keine Bewertungen

- Unit 2 Basic Cost Concepts: StructureDokument29 SeitenUnit 2 Basic Cost Concepts: StructureTushar SharmaNoch keine Bewertungen

- Unit 2 (Complete)Dokument16 SeitenUnit 2 (Complete)Tushar BhattacharyyaNoch keine Bewertungen

- BBA Management AccountingDokument8 SeitenBBA Management AccountingMohamaad SihatthNoch keine Bewertungen

- Cost Chapter4Dokument12 SeitenCost Chapter4Vishnu PrasathNoch keine Bewertungen

- Unit 1 Cost AccountingDokument20 SeitenUnit 1 Cost AccountingCollins NyendwaNoch keine Bewertungen

- Cost - Accounting 04122022-1Dokument30 SeitenCost - Accounting 04122022-1Mohamed SamerNoch keine Bewertungen

- Accounting CostingDokument156 SeitenAccounting CostingMorning32100% (1)

- Basic Concepts of Cost AccountingDokument14 SeitenBasic Concepts of Cost AccountinghellokittysaranghaeNoch keine Bewertungen

- Chapter 2 Cost IDokument13 SeitenChapter 2 Cost IHussen AbdulkadirNoch keine Bewertungen

- Cost 3Dokument17 SeitenCost 3Nandan Kumar JenaNoch keine Bewertungen

- Chap 2 CostDokument22 SeitenChap 2 CostAjinkya NaikNoch keine Bewertungen

- Overhead Cost Cost Accounting T. Y. B. Com. Sem V 1644476600Dokument37 SeitenOverhead Cost Cost Accounting T. Y. B. Com. Sem V 1644476600प्रभात सिंहNoch keine Bewertungen

- Atp 106 LPM Accounting - Topic 6 - Costing and BudgetingDokument17 SeitenAtp 106 LPM Accounting - Topic 6 - Costing and BudgetingTwain JonesNoch keine Bewertungen

- Cost AccountingDokument35 SeitenCost AccountingShubham LankaNoch keine Bewertungen

- Managerial Accounting - Chapter3Dokument27 SeitenManagerial Accounting - Chapter3Nazia AdeelNoch keine Bewertungen

- Management AccountingDokument7 SeitenManagement AccountingKhushal SainiNoch keine Bewertungen

- Elements of Cost: Management Accounting Costs Profitability GaapDokument8 SeitenElements of Cost: Management Accounting Costs Profitability GaapstefdrocksNoch keine Bewertungen

- Module 1 - Understanding ExpensesDokument14 SeitenModule 1 - Understanding Expensesjudith magsinoNoch keine Bewertungen

- P&C Module 1Dokument5 SeitenP&C Module 1Joe DomarsNoch keine Bewertungen

- Chapter Two: Cost Terminology and Classification: Learning OutcomesDokument8 SeitenChapter Two: Cost Terminology and Classification: Learning OutcomesKanbiro Orkaido100% (1)

- Cost Accounting - Meaning and ScopeDokument27 SeitenCost Accounting - Meaning and ScopemenakaNoch keine Bewertungen

- Unit 4 Allocation of Overhead CostDokument27 SeitenUnit 4 Allocation of Overhead CostTanishq KambojNoch keine Bewertungen

- Cost Accounting Cost Accounting: Presented ByDokument35 SeitenCost Accounting Cost Accounting: Presented BySusan Tagara-MukuzeNoch keine Bewertungen

- Elements of Cost in Overheads and Labor Rates and Their SignificanceDokument15 SeitenElements of Cost in Overheads and Labor Rates and Their SignificanceBrandy SangurahNoch keine Bewertungen

- Purchasing Management Unit 3Dokument30 SeitenPurchasing Management Unit 3DEREJENoch keine Bewertungen

- CMS Activity Based CostingDokument18 SeitenCMS Activity Based CostingNikhila DoraNoch keine Bewertungen

- Introduction To Cost Accounting Final With PDFDokument19 SeitenIntroduction To Cost Accounting Final With PDFLemon EnvoyNoch keine Bewertungen

- Cost Classification Lecture NotesDokument7 SeitenCost Classification Lecture Notesmichellebaileylindsa100% (1)

- Jai Narayan Vyas University Jodhpur Faculty of LawDokument13 SeitenJai Narayan Vyas University Jodhpur Faculty of LawDilip JaniNoch keine Bewertungen

- Cost Accounting and Control Lecture NotesDokument11 SeitenCost Accounting and Control Lecture NotesAnalyn LafradezNoch keine Bewertungen

- Classification of CostDokument23 SeitenClassification of CostShohidul Islam SaykatNoch keine Bewertungen

- (2330) M Abdullah Amjad BCOM (B)Dokument9 Seiten(2330) M Abdullah Amjad BCOM (B)Amna Khan YousafzaiNoch keine Bewertungen

- AM UNIT-III MaterialDokument19 SeitenAM UNIT-III MaterialVINAY BETHANoch keine Bewertungen

- Account 203Dokument1 SeiteAccount 203RAVI KISHANNoch keine Bewertungen

- Cost Capter FourDokument11 SeitenCost Capter FourAbayineh MesenbetNoch keine Bewertungen

- Cost ConceptDokument6 SeitenCost ConceptDeepti KumariNoch keine Bewertungen

- 7 - Understanding CostDokument18 Seiten7 - Understanding CostBhagaban DasNoch keine Bewertungen

- Module 1 - Overview of Cost AccountingDokument7 SeitenModule 1 - Overview of Cost AccountingMae JessaNoch keine Bewertungen

- W 4-5 Cost and ManagementDokument12 SeitenW 4-5 Cost and ManagementMelvinNoch keine Bewertungen

- Cost Accounting and Control: Cagayan State UniversityDokument74 SeitenCost Accounting and Control: Cagayan State UniversityAntonNoch keine Bewertungen

- Cost CH 3Dokument20 SeitenCost CH 3Yonas AyeleNoch keine Bewertungen

- Accounting For Management - Unit IVDokument87 SeitenAccounting For Management - Unit IVSELVARAJ SNNoch keine Bewertungen

- Module 1Dokument14 SeitenModule 1sarojkumardasbsetNoch keine Bewertungen

- BBA 2003 Cost AccountingDokument26 SeitenBBA 2003 Cost AccountingVentusNoch keine Bewertungen

- Norhat1964 PDFDokument10 SeitenNorhat1964 PDFNORHAT ABDULJALILNoch keine Bewertungen

- Shukrullah Assignment No 2Dokument4 SeitenShukrullah Assignment No 2Shukrullah JanNoch keine Bewertungen

- Coursematerial mmzg511 MOML15Dokument6 SeitenCoursematerial mmzg511 MOML15srikanth_bhairiNoch keine Bewertungen

- Chapter 5Dokument13 SeitenChapter 5abraha gebruNoch keine Bewertungen

- Chapter One: Cost Terms and ClassificationsDokument11 SeitenChapter One: Cost Terms and ClassificationsAkkamaNoch keine Bewertungen

- Accounting 202 Exam 1 Study Guide: Chapter 1: Managerial Accounting and Cost Concepts (12 Questions)Dokument4 SeitenAccounting 202 Exam 1 Study Guide: Chapter 1: Managerial Accounting and Cost Concepts (12 Questions)zoedmoleNoch keine Bewertungen

- Unit 2Dokument17 SeitenUnit 2DeepakNoch keine Bewertungen

- Chapter2 - Cost Classification and ConceptsDokument11 SeitenChapter2 - Cost Classification and ConceptsshubhNoch keine Bewertungen

- Costs: Reference For BusinessDokument8 SeitenCosts: Reference For BusinessPummy JainNoch keine Bewertungen

- Chap 003Dokument5 SeitenChap 003abhinaypradhanNoch keine Bewertungen

- Management Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesVon EverandManagement Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesNoch keine Bewertungen

- Case Jonah Creighton: Ethics and Value Based LeadershipDokument16 SeitenCase Jonah Creighton: Ethics and Value Based Leadershiprammar147Noch keine Bewertungen

- WCPT9 Scientific Program Madrid 2022Dokument52 SeitenWCPT9 Scientific Program Madrid 2022rammar147Noch keine Bewertungen

- Investment Scenario - : (A) FDI EQUITY INFLOWS (Equity Capital Components)Dokument1 SeiteInvestment Scenario - : (A) FDI EQUITY INFLOWS (Equity Capital Components)rammar147Noch keine Bewertungen

- A Coupled CFD Monte Carlo Method For Simulating Complex Aerosol Dynamics in Turbulent FlowsDokument14 SeitenA Coupled CFD Monte Carlo Method For Simulating Complex Aerosol Dynamics in Turbulent Flowsrammar147Noch keine Bewertungen

- Commercial Vehicles - February 2018Dokument3 SeitenCommercial Vehicles - February 2018rammar147Noch keine Bewertungen

- 2022 Rent Receipt 2Dokument1 Seite2022 Rent Receipt 2rammar147Noch keine Bewertungen

- Case Study 1Dokument11 SeitenCase Study 1Jaspal Singh100% (1)

- Leveraging: Case StudyDokument1 SeiteLeveraging: Case Studyrammar147Noch keine Bewertungen

- Financing:: 1. Role of Shareholders As StakeholdersDokument2 SeitenFinancing:: 1. Role of Shareholders As Stakeholdersrammar147Noch keine Bewertungen

- Financing:: 1. Role of Shareholders As StakeholdersDokument2 SeitenFinancing:: 1. Role of Shareholders As Stakeholdersrammar147Noch keine Bewertungen

- Volume 5 Issue 4 Paper 3Dokument6 SeitenVolume 5 Issue 4 Paper 3Niku BandiNoch keine Bewertungen

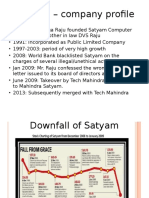

- Satyam CaseDokument4 SeitenSatyam Caserammar147Noch keine Bewertungen

- Flux Calculation Due To Non Uniform SourceDokument4 SeitenFlux Calculation Due To Non Uniform Sourcerammar147Noch keine Bewertungen

- Case Study 1Dokument11 SeitenCase Study 1Jaspal Singh100% (1)

- Volume 5 Issue 4 Paper 3Dokument6 SeitenVolume 5 Issue 4 Paper 3Niku BandiNoch keine Bewertungen

- Dose Due To Cylindrical SourceDokument9 SeitenDose Due To Cylindrical Sourcerammar147Noch keine Bewertungen

- Dose Due To Cylindrical SourceDokument9 SeitenDose Due To Cylindrical Sourcerammar147Noch keine Bewertungen

- 13 PPTGGDokument78 Seiten13 PPTGGأحمدآلزهوNoch keine Bewertungen

- Shielding CalculationDokument17 SeitenShielding Calculationrammar147Noch keine Bewertungen

- Special RelativityDokument53 SeitenSpecial RelativityAndrew Florit100% (2)

- Supersymmetry ReportDokument49 SeitenSupersymmetry Reportrammar147Noch keine Bewertungen

- Flux Calculation Due To Non Uniform SourceDokument4 SeitenFlux Calculation Due To Non Uniform Sourcerammar147Noch keine Bewertungen

- Dose Due To Cylindrical SourceDokument9 SeitenDose Due To Cylindrical Sourcerammar147Noch keine Bewertungen

- Fmradio 1111 PDFDokument7 SeitenFmradio 1111 PDFVikiVikiNoch keine Bewertungen

- Semiconductor PN JunctionDokument19 SeitenSemiconductor PN Junctionrammar147Noch keine Bewertungen

- 1 - 0 Answers Progress: To Check YourDokument26 Seiten1 - 0 Answers Progress: To Check YourvimalbakshiNoch keine Bewertungen

- Mco 07Dokument4 SeitenMco 07rammar147Noch keine Bewertungen

- Introduction To MarketingDokument18 SeitenIntroduction To Marketingsabyasachi samalNoch keine Bewertungen

- Solutions GuideDokument10 SeitenSolutions Guidepalak32Noch keine Bewertungen

- ECS Mandate FormDokument2 SeitenECS Mandate FormManoj PatiyalNoch keine Bewertungen

- About Ibm Food Trust - 89017389USENDokument17 SeitenAbout Ibm Food Trust - 89017389USENMatheus SpartalisNoch keine Bewertungen

- What Is Economics?Dokument2 SeitenWhat Is Economics?Lupan DumitruNoch keine Bewertungen

- 24-Hour Call Center: 16221 For Overseas Callers: +880 2 55668056Dokument8 Seiten24-Hour Call Center: 16221 For Overseas Callers: +880 2 55668056Number ButNoch keine Bewertungen

- Full Question Bank by Ravi Taori 201025122739Dokument345 SeitenFull Question Bank by Ravi Taori 201025122739Mr. RetrospectorNoch keine Bewertungen

- Women EnterprenuershipDokument3 SeitenWomen EnterprenuershipMehul MehtaNoch keine Bewertungen

- AFAR04-10 Business Combination Date of AcquisitionDokument3 SeitenAFAR04-10 Business Combination Date of AcquisitioneildeeNoch keine Bewertungen

- CertAlarm Certificate FC460P FireClass Photoelectric DetectorDokument3 SeitenCertAlarm Certificate FC460P FireClass Photoelectric DetectortbelayinehNoch keine Bewertungen

- Submitted By: Dela Cruz, Janella T. Masters in Business AdministrationDokument21 SeitenSubmitted By: Dela Cruz, Janella T. Masters in Business AdministrationAngelica AnneNoch keine Bewertungen

- Operational Plan SampleDokument5 SeitenOperational Plan Sampletaylor swiftyyyNoch keine Bewertungen

- Aprds Safety ValveDokument2 SeitenAprds Safety ValveMandeep SinghNoch keine Bewertungen

- Midterm Test EthicsDokument9 SeitenMidterm Test EthicsAzwimar PutranusaNoch keine Bewertungen

- The First Annual Report of Farz FoundationDokument62 SeitenThe First Annual Report of Farz FoundationFarhat Abbas ShahNoch keine Bewertungen

- How You Know Rural IndiaDokument78 SeitenHow You Know Rural IndiaAadil KakarNoch keine Bewertungen

- Mutula - Effect of Electronic Accounting On The Financial Performance of Commercial State Corporations in KenyaDokument73 SeitenMutula - Effect of Electronic Accounting On The Financial Performance of Commercial State Corporations in KenyaaliNoch keine Bewertungen

- DME NEET UG 2022 Institute Fee Paymet User ManualDokument9 SeitenDME NEET UG 2022 Institute Fee Paymet User ManualYash AdhauliaNoch keine Bewertungen

- Cocacola Term PaperDokument6 SeitenCocacola Term PaperJanak UpadhyayNoch keine Bewertungen

- Kumar Mangalam Birla Committee - Docxkumar Mangalam Birla CommitteeDokument3 SeitenKumar Mangalam Birla Committee - Docxkumar Mangalam Birla CommitteeVanessa HernandezNoch keine Bewertungen

- Invitation Letter ERI-CEFE Training LPANDokument2 SeitenInvitation Letter ERI-CEFE Training LPANJoy VisitacionNoch keine Bewertungen

- Cost Estimating: Microsoft ProjectDokument3 SeitenCost Estimating: Microsoft Projectain_ykbNoch keine Bewertungen

- Contract Administration Works-Sbd 1Dokument200 SeitenContract Administration Works-Sbd 1Rajaratnam TharakanNoch keine Bewertungen

- Wheel of StrategyDokument7 SeitenWheel of StrategyKalpesh Singh SinghNoch keine Bewertungen

- Principles of BankingDokument33 SeitenPrinciples of BankingMANAN MEHTANoch keine Bewertungen

- 0450 Y15 SM 1Dokument10 Seiten0450 Y15 SM 1nouraNoch keine Bewertungen

- Assessment Task 3 - BSBHRM513Dokument40 SeitenAssessment Task 3 - BSBHRM513Xavar Xan50% (2)

- Aggregate Planning and MRPDokument68 SeitenAggregate Planning and MRPJanarthanan Siva KumarNoch keine Bewertungen

- Organization ProfileDokument2 SeitenOrganization ProfilebalasudhakarNoch keine Bewertungen

- Seminar 4Dokument5 SeitenSeminar 4Ethel OgirriNoch keine Bewertungen