Das könnte Ihnen auch gefallen

- CRFB JCT Response FINAL JS PDFDokument8 SeitenCRFB JCT Response FINAL JS PDFCommittee For a Responsible Federal BudgetNoch keine Bewertungen

- House Bills Would Add Billions To Debt Scuttle Medicare Cost Controls PDFDokument2 SeitenHouse Bills Would Add Billions To Debt Scuttle Medicare Cost Controls PDFCommittee For a Responsible Federal BudgetNoch keine Bewertungen

- CRFB On SGR Deal 3262014Dokument1 SeiteCRFB On SGR Deal 3262014Committee For a Responsible Federal BudgetNoch keine Bewertungen

- Prepplan PDFDokument12 SeitenPrepplan PDFCommittee For a Responsible Federal BudgetNoch keine Bewertungen

- CRFB JCT Response FINAL JS PDFDokument8 SeitenCRFB JCT Response FINAL JS PDFCommittee For a Responsible Federal BudgetNoch keine Bewertungen

- Fy16 Presidents Budget CRFB Slidedeck PDFDokument18 SeitenFy16 Presidents Budget CRFB Slidedeck PDFCommittee For a Responsible Federal BudgetNoch keine Bewertungen

- Goldwein 09-10Dokument3 SeitenGoldwein 09-10Committee For a Responsible Federal BudgetNoch keine Bewertungen

- CRFB JCT Response FINAL JS PDFDokument8 SeitenCRFB JCT Response FINAL JS PDFCommittee For a Responsible Federal BudgetNoch keine Bewertungen

- CRFB JCT Response FINAL JS PDFDokument8 SeitenCRFB JCT Response FINAL JS PDFCommittee For a Responsible Federal BudgetNoch keine Bewertungen

- Averting A Fiscal Crisis - Why America Needs Comprehensive Fiscal Reform Now 0 0 0 0 0 0 0 0Dokument53 SeitenAverting A Fiscal Crisis - Why America Needs Comprehensive Fiscal Reform Now 0 0 0 0 0 0 0 0Committee For a Responsible Federal BudgetNoch keine Bewertungen

- Reforming The Corporate Tax CodeDokument14 SeitenReforming The Corporate Tax CodeCommittee For a Responsible Federal BudgetNoch keine Bewertungen

- Americans Sign Debt Petition in One WeekDokument2 SeitenAmericans Sign Debt Petition in One WeekCommittee For a Responsible Federal BudgetNoch keine Bewertungen

- CRFB JCT Response FINAL JS PDFDokument8 SeitenCRFB JCT Response FINAL JS PDFCommittee For a Responsible Federal BudgetNoch keine Bewertungen

- Averting A Fiscal Crisis - Why America Needs Comprehensive Fiscal Reform Now 0 0 0 0 0 0 0Dokument60 SeitenAverting A Fiscal Crisis - Why America Needs Comprehensive Fiscal Reform Now 0 0 0 0 0 0 0Committee For a Responsible Federal Budget100% (1)

- Averting A Fiscal Crisis 0Dokument26 SeitenAverting A Fiscal Crisis 0Committee For a Responsible Federal BudgetNoch keine Bewertungen

- Averting A Fiscal Crisis - Why America Needs Comprehensive Fiscal Reform Now 0 0 0 0 0 0Dokument59 SeitenAverting A Fiscal Crisis - Why America Needs Comprehensive Fiscal Reform Now 0 0 0 0 0 0Committee For a Responsible Federal BudgetNoch keine Bewertungen

- Averting A Fiscal Crisis 0Dokument26 SeitenAverting A Fiscal Crisis 0Committee For a Responsible Federal BudgetNoch keine Bewertungen

- Politco Fiscal Cliff Ad FinalDokument1 SeitePolitco Fiscal Cliff Ad FinalCommittee For a Responsible Federal BudgetNoch keine Bewertungen

- CRFB Reacts To Six-Month Continuing Resolution 9-11-2012Dokument1 SeiteCRFB Reacts To Six-Month Continuing Resolution 9-11-2012Committee For a Responsible Federal BudgetNoch keine Bewertungen

- Averting A Fiscal Crisis - Why America Needs Comprehensive Fiscal Reform Now 0 0 0 0 0 0Dokument59 SeitenAverting A Fiscal Crisis - Why America Needs Comprehensive Fiscal Reform Now 0 0 0 0 0 0Committee For a Responsible Federal BudgetNoch keine Bewertungen

- Averting A Fiscal Crisis - Why America Needs Comprehensive Fiscal Reform Now 0 0 0 0 0 0Dokument59 SeitenAverting A Fiscal Crisis - Why America Needs Comprehensive Fiscal Reform Now 0 0 0 0 0 0Committee For a Responsible Federal BudgetNoch keine Bewertungen

- Averting A Fiscal Crisis 0Dokument25 SeitenAverting A Fiscal Crisis 0Committee For a Responsible Federal BudgetNoch keine Bewertungen

- CBO August 2012 Update 0Dokument6 SeitenCBO August 2012 Update 0René Guerieri WoodNoch keine Bewertungen

- CRFB Reacts To OMBs Report On The SequesterDokument1 SeiteCRFB Reacts To OMBs Report On The SequesterCommittee For a Responsible Federal BudgetNoch keine Bewertungen

- With Conventions Out of The Way Its Time For Leaders To LeadDokument1 SeiteWith Conventions Out of The Way Its Time For Leaders To LeadCommittee For a Responsible Federal BudgetNoch keine Bewertungen

- Paul Ryan TableDokument3 SeitenPaul Ryan TableCommittee For a Responsible Federal BudgetNoch keine Bewertungen

- Paul Ryan Comparison TableDokument3 SeitenPaul Ryan Comparison TableCommittee For a Responsible Federal BudgetNoch keine Bewertungen

- Dont Put The Extenders On The Nations Credit CardDokument1 SeiteDont Put The Extenders On The Nations Credit CardCommittee For a Responsible Federal BudgetNoch keine Bewertungen

- Press Clips For Fix The Debt 8-13-2012Dokument7 SeitenPress Clips For Fix The Debt 8-13-2012Committee For a Responsible Federal BudgetNoch keine Bewertungen

- Davis Steele Rendell Gregg Call For Debates On Debt ReductionDokument3 SeitenDavis Steele Rendell Gregg Call For Debates On Debt ReductionCommittee For a Responsible Federal BudgetNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (120)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- ExxonMobil Final DraftDokument10 SeitenExxonMobil Final DraftJohn CooganNoch keine Bewertungen

- Comprehension Questions: 1. What Are Minimum Lease Payments'?Dokument13 SeitenComprehension Questions: 1. What Are Minimum Lease Payments'?Amit ShuklaNoch keine Bewertungen

- Southwest Airlines Co.: Investor Booklet - April 2019Dokument34 SeitenSouthwest Airlines Co.: Investor Booklet - April 2019theredcornerNoch keine Bewertungen

- Jawaban CH 3 (2) Problem 3-43 AKB ASLABDokument5 SeitenJawaban CH 3 (2) Problem 3-43 AKB ASLABRantiyaniNoch keine Bewertungen

- Check - Chapter 10 - She Part 1Dokument4 SeitenCheck - Chapter 10 - She Part 1ARNEL CALUBAGNoch keine Bewertungen

- Wood FSDokument117 SeitenWood FSAnton SocoNoch keine Bewertungen

- Types of GST ReturnsDokument5 SeitenTypes of GST ReturnsParvathy MNoch keine Bewertungen

- Service Tax Refund - RansaDokument1 SeiteService Tax Refund - RansaservervcnewNoch keine Bewertungen

- Solid Waste Management DPRDokument200 SeitenSolid Waste Management DPRshweta bhavsarNoch keine Bewertungen

- Uniform Format of Accounts For Central Automnomous Bodies PDFDokument46 SeitenUniform Format of Accounts For Central Automnomous Bodies PDFsgirishri4044Noch keine Bewertungen

- ATW108 Chapter 28 TutorialDokument3 SeitenATW108 Chapter 28 TutorialShuhada ShamsuddinNoch keine Bewertungen

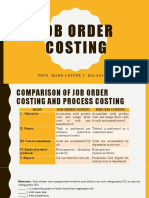

- Job Order Costing: Prof. Mark Lester T. Balasa, CpaDokument24 SeitenJob Order Costing: Prof. Mark Lester T. Balasa, CpaNah HamzaNoch keine Bewertungen

- 327-329 Plaridel Surety & Insurance v. CIR Collector v. Goodrich International Rubber Co.Dokument2 Seiten327-329 Plaridel Surety & Insurance v. CIR Collector v. Goodrich International Rubber Co.Eloise Coleen Sulla PerezNoch keine Bewertungen

- Co Op Business Plan Template PDFDokument15 SeitenCo Op Business Plan Template PDFIngle Satish100% (1)

- The Independent Issue 515Dokument44 SeitenThe Independent Issue 515The Independent MagazineNoch keine Bewertungen

- Chap 012Dokument17 SeitenChap 012Ahmed A HakimNoch keine Bewertungen

- Auto-Payslip Sample 2017Dokument14 SeitenAuto-Payslip Sample 2017Matthew NiñoNoch keine Bewertungen

- Logical Ability For XATDokument52 SeitenLogical Ability For XATBharat BajajNoch keine Bewertungen

- DAVAO v. APHIDokument2 SeitenDAVAO v. APHIEnverga Law School Corporation Law SC Division100% (1)

- Winfield Refuse Management Inc. Raising Debt vs. EquityDokument13 SeitenWinfield Refuse Management Inc. Raising Debt vs. EquitynmenalopezNoch keine Bewertungen

- (TB) II CHii07Dokument22 Seiten(TB) II CHii07Dina Adel DawoodNoch keine Bewertungen

- Case 5 - 32Dokument5 SeitenCase 5 - 32ashu140350% (2)

- Quiz National Y AccountingDokument2 SeitenQuiz National Y AccountingAngeline Maquiso SumaoyNoch keine Bewertungen

- Brown-Forman Initiating CoverageDokument96 SeitenBrown-Forman Initiating CoverageRestructuring100% (1)

- Sports Bar Business PlanDokument33 SeitenSports Bar Business PlanNathaniel MadugaNoch keine Bewertungen

- El Teck Magnetic Advacnes Planning DocumentDokument4 SeitenEl Teck Magnetic Advacnes Planning DocumentStephanie Ng100% (1)

- Tugas 6 - Aulia KhairaniDokument3 SeitenTugas 6 - Aulia KhairaniadvokesmahmmbNoch keine Bewertungen

- A Young Engineer Applied For A Position That Was To Last Six MonthsDokument6 SeitenA Young Engineer Applied For A Position That Was To Last Six MonthsNeco Carlo PalNoch keine Bewertungen

- IFM Chapter 01Dokument33 SeitenIFM Chapter 01Mahbub TalukderNoch keine Bewertungen

- Ldce - Fasp - 08 PDFDokument9 SeitenLdce - Fasp - 08 PDFDinesh Talele86% (7)