Das könnte Ihnen auch gefallen

- Shubbar - 2023 - The Political Economy of UAE Defense IndustryDokument11 SeitenShubbar - 2023 - The Political Economy of UAE Defense IndustryMartín AlbertoNoch keine Bewertungen

- Turkey's Offset Policy Development and Case StudiesDokument129 SeitenTurkey's Offset Policy Development and Case StudiesMartín AlbertoNoch keine Bewertungen

- Albert Vidal - A New Chapter For UAE Defense Procurement - 01-12-22Dokument4 SeitenAlbert Vidal - A New Chapter For UAE Defense Procurement - 01-12-22Martín AlbertoNoch keine Bewertungen

- EDGE Group Continues Stellar International Growth, Consolidating Its Position As An Industry Leader - Defense Here - 30-11-23Dokument7 SeitenEDGE Group Continues Stellar International Growth, Consolidating Its Position As An Industry Leader - Defense Here - 30-11-23Martín AlbertoNoch keine Bewertungen

- Vinculos Entre España e Israel en DefensaDokument138 SeitenVinculos Entre España e Israel en DefensaMartín AlbertoNoch keine Bewertungen

- Military-Economic Structure in TurkeyDokument38 SeitenMilitary-Economic Structure in TurkeyMartín AlbertoNoch keine Bewertungen

- Donatas Palavenis - 2020 - Israel Defense Industry, What We Can Learn From ItDokument19 SeitenDonatas Palavenis - 2020 - Israel Defense Industry, What We Can Learn From ItMartín AlbertoNoch keine Bewertungen

- Military-Industrial Aspects of Turkish Defence Policy - Wisniewzki - 2015Dokument14 SeitenMilitary-Industrial Aspects of Turkish Defence Policy - Wisniewzki - 2015Martín Alberto100% (1)

- Jeffrey Clarke - 1977 - The Nationalization of War Industries in France - 1936-1937Dokument21 SeitenJeffrey Clarke - 1977 - The Nationalization of War Industries in France - 1936-1937Martín AlbertoNoch keine Bewertungen

- Defence Industries in The 21st Century A Comparative Analysis - Kurc & Neuman - 2017Dokument10 SeitenDefence Industries in The 21st Century A Comparative Analysis - Kurc & Neuman - 2017Martín AlbertoNoch keine Bewertungen

- The Defense Industry in Brasil - Characteristics and Involvement of Supplier Firms - IPEA - 2014Dokument60 SeitenThe Defense Industry in Brasil - Characteristics and Involvement of Supplier Firms - IPEA - 2014Martín AlbertoNoch keine Bewertungen

- Kemal Topcu, Et Al - 2015 - A Study On Defense Acquisition Models With Emerging Market Perspective - The Case of TurkeyDokument8 SeitenKemal Topcu, Et Al - 2015 - A Study On Defense Acquisition Models With Emerging Market Perspective - The Case of TurkeyMartín AlbertoNoch keine Bewertungen

- The Influence of Innovation On Firm Size - Bosma - 2002Dokument12 SeitenThe Influence of Innovation On Firm Size - Bosma - 2002Martín AlbertoNoch keine Bewertungen

- Ciampi Et Al - 2019 - Engineering Offshoring in The Defense Industry - Perspectives On Manufacturing IndustriesDokument5 SeitenCiampi Et Al - 2019 - Engineering Offshoring in The Defense Industry - Perspectives On Manufacturing IndustriesMartín AlbertoNoch keine Bewertungen

- Saksonova, Svetlana - Approaches To Improving Asset Structure ManagementDokument9 SeitenSaksonova, Svetlana - Approaches To Improving Asset Structure ManagementMartín AlbertoNoch keine Bewertungen

- Colfer y Baldwin - 2016 - The Mirroring Hypothesis Theory, Evidence, and ExDokument31 SeitenColfer y Baldwin - 2016 - The Mirroring Hypothesis Theory, Evidence, and ExMartín AlbertoNoch keine Bewertungen

- Turkey Officially Launches Competition For TF-X Fighter EngineDokument7 SeitenTurkey Officially Launches Competition For TF-X Fighter EngineMartín AlbertoNoch keine Bewertungen

- Tee - 2019 - Benefiting From Modularity Within and Across FirmDokument18 SeitenTee - 2019 - Benefiting From Modularity Within and Across FirmMartín AlbertoNoch keine Bewertungen

- Hall and Gingerich (2009) - Varieties of Capitalism and Institutional Complementarities in The Political EconomyDokument67 SeitenHall and Gingerich (2009) - Varieties of Capitalism and Institutional Complementarities in The Political EconomyMartín AlbertoNoch keine Bewertungen

- The - Building - Blocks - of - Economic - Complexity - Hidalgo y HausmanDokument7 SeitenThe - Building - Blocks - of - Economic - Complexity - Hidalgo y HausmanMartín AlbertoNoch keine Bewertungen

- Brown (2020) - Mission-Oriented or Mission AdriftDokument24 SeitenBrown (2020) - Mission-Oriented or Mission AdriftMartín AlbertoNoch keine Bewertungen

- Cellin & Lambertini - 2005 - Betrand Competition and InnovationDokument6 SeitenCellin & Lambertini - 2005 - Betrand Competition and InnovationMartín AlbertoNoch keine Bewertungen

- Beraud-Sudreau and Nouwens - 2019 - Weighing Giants - Taking Stock of The Expansion of Chinas Defense IndustryDokument28 SeitenBeraud-Sudreau and Nouwens - 2019 - Weighing Giants - Taking Stock of The Expansion of Chinas Defense IndustryMartín AlbertoNoch keine Bewertungen

- Industrial Policy Debate: Rationales, Evidence and ConclusionsDokument51 SeitenIndustrial Policy Debate: Rationales, Evidence and ConclusionsMartín AlbertoNoch keine Bewertungen

- Global Supply Chains and Intangible Assets in The Automotive and Aeronautical Industries - Serfati & Sauviat - 2019Dokument27 SeitenGlobal Supply Chains and Intangible Assets in The Automotive and Aeronautical Industries - Serfati & Sauviat - 2019Martín AlbertoNoch keine Bewertungen

- 2016 - Reforming Chinas Defense IndustryDokument29 Seiten2016 - Reforming Chinas Defense IndustryMartín AlbertoNoch keine Bewertungen

- CHina WHite Paper On DefenceDokument52 SeitenCHina WHite Paper On DefenceAkshay RanadeNoch keine Bewertungen

- Another Strong Year For China's Defence CompaniesDokument8 SeitenAnother Strong Year For China's Defence CompaniesMartín AlbertoNoch keine Bewertungen

- Architectural Innovation The Reconfiguration of ExDokument24 SeitenArchitectural Innovation The Reconfiguration of ExRaisa CardosoNoch keine Bewertungen

- Government R&D Drives Innovation in AsiaDokument27 SeitenGovernment R&D Drives Innovation in AsiaMartín AlbertoNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5782)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (72)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Records: Collierville Schools Removed Hundreds of LGBTQ+ Books From ShelvesDokument328 SeitenRecords: Collierville Schools Removed Hundreds of LGBTQ+ Books From ShelvesUSA TODAY NetworkNoch keine Bewertungen

- Human ExceptionalityDokument3 SeitenHuman ExceptionalityVergel LearningcenterNoch keine Bewertungen

- SPE 55631 Practical Issues With Field Injection Well Gel TreatmentsDokument9 SeitenSPE 55631 Practical Issues With Field Injection Well Gel TreatmentsAngy Carolina Taborda VelasquezNoch keine Bewertungen

- PMAI Sample ReportDokument6 SeitenPMAI Sample ReportchidambaraNoch keine Bewertungen

- Daily Lesson Plan English Language Year 5Dokument5 SeitenDaily Lesson Plan English Language Year 5muhammadNoch keine Bewertungen

- National Income MCQsDokument6 SeitenNational Income MCQsZeeshan AfzalNoch keine Bewertungen

- Macatangay Bsn-g4b - Business Model CanvasDokument3 SeitenMacatangay Bsn-g4b - Business Model CanvasGaea Angela MACATANGAYNoch keine Bewertungen

- Oral Hygiene Autis PDFDokument7 SeitenOral Hygiene Autis PDFNoviyana Idrus DgmapatoNoch keine Bewertungen

- How To Install A Siemens Mag MeterDokument10 SeitenHow To Install A Siemens Mag MeterBabiker ElrasheedNoch keine Bewertungen

- Business Administration Core: Sample Exam QuestionsDokument6 SeitenBusiness Administration Core: Sample Exam QuestionsBernard Vincent Guitan MineroNoch keine Bewertungen

- Fuel - in Tank Fuel Pump Replacement PDFDokument14 SeitenFuel - in Tank Fuel Pump Replacement PDFBeniamin KowollNoch keine Bewertungen

- Netflix in 2012 Can It Recover From Its Strategy MissteptsDokument1 SeiteNetflix in 2012 Can It Recover From Its Strategy MissteptsShubham GoelNoch keine Bewertungen

- Flowsheet WWT IKPPDokument5 SeitenFlowsheet WWT IKPPDiffa achmadNoch keine Bewertungen

- Foundation Engineering2Dokument8 SeitenFoundation Engineering2mahmoud alawnehNoch keine Bewertungen

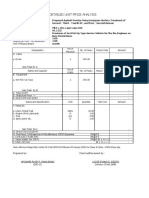

- DETAILED UNIT PRICE ANALYSIS FOR PROPOSED ASPHALT OVERLAYDokument7 SeitenDETAILED UNIT PRICE ANALYSIS FOR PROPOSED ASPHALT OVERLAYreynoldNoch keine Bewertungen

- Harvard RP1Dokument7 SeitenHarvard RP1Ajay NegiNoch keine Bewertungen

- Big Book AlphabetDokument53 SeitenBig Book Alphabetallrounder crazy thingsNoch keine Bewertungen

- Plant Your Wisdom Tree: Define CurriculumDokument1 SeitePlant Your Wisdom Tree: Define CurriculumBon Jaime TangcoNoch keine Bewertungen

- Hope-4 Activity-Sheet MountaineeringDokument2 SeitenHope-4 Activity-Sheet MountaineeringKristine MirasolNoch keine Bewertungen

- Castration Procedure in Farm AnimalsDokument70 SeitenCastration Procedure in Farm AnimalsIgor GaloskiNoch keine Bewertungen

- Pesachim 45Dokument42 SeitenPesachim 45Julian Ungar-SargonNoch keine Bewertungen

- Gradeup's comprehensive guide to teaching and learningDokument6 SeitenGradeup's comprehensive guide to teaching and learningRJNoch keine Bewertungen

- Projection of points and lines engineeringDokument38 SeitenProjection of points and lines engineeringBharat SinghNoch keine Bewertungen

- English Vocabulary Exercises For B2 - It Drives Me Crazy! - English Practice OnlineDokument16 SeitenEnglish Vocabulary Exercises For B2 - It Drives Me Crazy! - English Practice Onlineსოფი 'აNoch keine Bewertungen

- Midheaven in Taurus Meaning & Careers - AstrologyDokument1 SeiteMidheaven in Taurus Meaning & Careers - AstrologyGlithc hNoch keine Bewertungen

- Kindred IntroductionDokument18 SeitenKindred IntroductionMarionNoch keine Bewertungen

- Request Letter For Payment Features & SampleDokument3 SeitenRequest Letter For Payment Features & SamplemindnbooksNoch keine Bewertungen

- 10 Commandments - For Effective Email Communication (1) .PpsDokument13 Seiten10 Commandments - For Effective Email Communication (1) .Ppshima_bindu_89Noch keine Bewertungen

- Presentation On Programming Language: Name IDDokument9 SeitenPresentation On Programming Language: Name IDAjay GhoshNoch keine Bewertungen

- Sist en 12390 3 2019Dokument10 SeitenSist en 12390 3 2019Francois UWIMBABAZINoch keine Bewertungen