Das könnte Ihnen auch gefallen

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Case 2 - Revenue and Expense RecognitionDokument4 SeitenCase 2 - Revenue and Expense RecognitionRizwan MushtaqNoch keine Bewertungen

- Adjusting Entries Problems 2022 DahonogDokument2 SeitenAdjusting Entries Problems 2022 DahonogBaltazar JustinianoNoch keine Bewertungen

- Bir Tax ClearanceDokument95 SeitenBir Tax ClearanceJeline ReyesNoch keine Bewertungen

- Brooklyn Museum 2019 IRS Form 990Dokument64 SeitenBrooklyn Museum 2019 IRS Form 990Lee Rosenbaum, CultureGrrlNoch keine Bewertungen

- Payslip TemplateDokument1 SeitePayslip TemplateLeonardo GonzalezNoch keine Bewertungen

- Compliance Estimates For Earned Income Tax Credit Claimed On 1999 ReturnsDokument38 SeitenCompliance Estimates For Earned Income Tax Credit Claimed On 1999 ReturnsIRSNoch keine Bewertungen

- DOL Unemployment ReportDokument41 SeitenDOL Unemployment ReportJohn DodgeNoch keine Bewertungen

- Treasury Inspector General For Tax AdministrationDokument21 SeitenTreasury Inspector General For Tax AdministrationBecket AdamsNoch keine Bewertungen

- 2nd Q 2013final Report 08.19.13Dokument14 Seiten2nd Q 2013final Report 08.19.13Elliott AuerbachNoch keine Bewertungen

- Role Accounts OfficerssDokument43 SeitenRole Accounts OfficerssPryns Nii Nortey AddoNoch keine Bewertungen

- Waste Management: A Focus On General Computing ControlsDokument3 SeitenWaste Management: A Focus On General Computing ControlsCryptic LollNoch keine Bewertungen

- Final Alert Memo - States' Compliance With CARES Act UI RPT - 080222Dokument28 SeitenFinal Alert Memo - States' Compliance With CARES Act UI RPT - 080222Adam HarringtonNoch keine Bewertungen

- Irs Subject To FdcpaDokument5 SeitenIrs Subject To Fdcpaxlrider530Noch keine Bewertungen

- Commissionerof Incometax, Bangalorevs KRaheja Hotels EsDokument6 SeitenCommissionerof Incometax, Bangalorevs KRaheja Hotels EsKaran GannaNoch keine Bewertungen

- TITGADokument26 SeitenTITGAcorruptioncurrentsNoch keine Bewertungen

- Treasury Inspector General For Tax AdministrationDokument26 SeitenTreasury Inspector General For Tax AdministrationIRSNoch keine Bewertungen

- Annual Report On New York State Tax Expenditures 2013-14 State Fiscal YearDokument193 SeitenAnnual Report On New York State Tax Expenditures 2013-14 State Fiscal YearRick KarlinNoch keine Bewertungen

- Itr 1Dokument50 SeitenItr 1LightRINoch keine Bewertungen

- U1A OverviewDokument7 SeitenU1A Overview4mggxj68cyNoch keine Bewertungen

- Job Tax Credit AuditDokument63 SeitenJob Tax Credit AuditZachary HansenNoch keine Bewertungen

- IRS Free File ReportDokument106 SeitenIRS Free File ReportAustin DeneanNoch keine Bewertungen

- Chapter 2 - Tax On Sales Trade EtcDokument42 SeitenChapter 2 - Tax On Sales Trade EtcS Dharam SinghNoch keine Bewertungen

- Treasury Inspector General For Tax AdministrationDokument31 SeitenTreasury Inspector General For Tax AdministrationJeffrey DunetzNoch keine Bewertungen

- Audit Report On Sales TaxDokument27 SeitenAudit Report On Sales TaxharshNoch keine Bewertungen

- CAG Report On MNREGADokument344 SeitenCAG Report On MNREGACanary Trap100% (1)

- 2 of 2014Dokument176 Seiten2 of 2014Aksh GandhiNoch keine Bewertungen

- Zimbabwe Third Quarter - Short Term Insurance ReportDokument31 SeitenZimbabwe Third Quarter - Short Term Insurance ReportKristi DuranNoch keine Bewertungen

- Meralco Co. Consolidated Financial Statement 2020Dokument155 SeitenMeralco Co. Consolidated Financial Statement 2020Lyca SorianoNoch keine Bewertungen

- Self Assessments SchemeDokument10 SeitenSelf Assessments SchemeRafae ShahidNoch keine Bewertungen

- Tib Vol35 No5Dokument43 SeitenTib Vol35 No5infoNoch keine Bewertungen

- 00 555Dokument129 Seiten00 555Giora RozmarinNoch keine Bewertungen

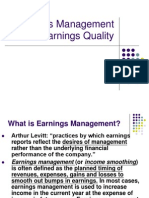

- Earnings Management and Earnings QualityDokument23 SeitenEarnings Management and Earnings QualityZa HanfiNoch keine Bewertungen

- 2020 CBO IRS Enforcement ReportDokument40 Seiten2020 CBO IRS Enforcement ReportStephen LoiaconiNoch keine Bewertungen

- Irs Audit SystemDokument30 SeitenIrs Audit SystemMcKenzieLawNoch keine Bewertungen

- Puspitari - PublishedDokument6 SeitenPuspitari - PublishedAzizah El FathNoch keine Bewertungen

- Direct Tax - 2011Dokument494 SeitenDirect Tax - 2011vinagoyaNoch keine Bewertungen

- Tax Reforms in India: Static DimensionsDokument11 SeitenTax Reforms in India: Static DimensionsLeela LazarNoch keine Bewertungen

- Key Energy Services, Inc.: United States Securities and Exchange Commission Form 10-QDokument61 SeitenKey Energy Services, Inc.: United States Securities and Exchange Commission Form 10-QAlok PatelNoch keine Bewertungen

- Internal Audit Report 202122 UpdateDokument29 SeitenInternal Audit Report 202122 Updateahmed khoudhiryNoch keine Bewertungen

- 10 3Q Results KoreanDokument11 Seiten10 3Q Results Korean김준섭Noch keine Bewertungen

- Oregon Secretary of State Audit of Oregon Employment DepartmentDokument47 SeitenOregon Secretary of State Audit of Oregon Employment DepartmentSinclair Broadcast Group - EugeneNoch keine Bewertungen

- Wpiea2020142 Print PDFDokument42 SeitenWpiea2020142 Print PDFDita ApriliaNoch keine Bewertungen

- LEITI 2nd Reconciliation ReportDokument112 SeitenLEITI 2nd Reconciliation ReportLiberiaEITINoch keine Bewertungen

- 23 IDES Unemployment Ins Prgms Perf FullDokument156 Seiten23 IDES Unemployment Ins Prgms Perf Full25 NewsNoch keine Bewertungen

- 226 CIR v. Sony Philippines, IncDokument4 Seiten226 CIR v. Sony Philippines, IncclarkorjaloNoch keine Bewertungen

- TARGET CORP 8-K (Events or Changes Between Quarterly Reports) 2009-02-24Dokument13 SeitenTARGET CORP 8-K (Events or Changes Between Quarterly Reports) 2009-02-24http://secwatch.comNoch keine Bewertungen

- sd13 Using Income Tax InformationDokument9 Seitensd13 Using Income Tax InformationAngela JoyceNoch keine Bewertungen

- Financial Results & Limited Review Report For Dec 31, 2015 (Standalone) (Result)Dokument3 SeitenFinancial Results & Limited Review Report For Dec 31, 2015 (Standalone) (Result)Shyam SunderNoch keine Bewertungen

- PandemicUIexpiration PaperDokument28 SeitenPandemicUIexpiration PaperWKRC Local 12Noch keine Bewertungen

- MSRD Manila Electric Company Sec 17c 2023 Consolidated Afs 29 Feb 2024Dokument159 SeitenMSRD Manila Electric Company Sec 17c 2023 Consolidated Afs 29 Feb 2024Walen JosefNoch keine Bewertungen

- U.S. Securities and Exchange Commission - Fiscal Year 2013 Agency Financial ReportDokument156 SeitenU.S. Securities and Exchange Commission - Fiscal Year 2013 Agency Financial ReportVanessa SchoenthalerNoch keine Bewertungen

- Case of The DayDokument29 SeitenCase of The DayToni Gabrielle Ang EspinaNoch keine Bewertungen

- Commissioner of Internal Revenue vs. Systems Technology Institute, Inc., 833 SCRA 285, July 26, 2017Dokument16 SeitenCommissioner of Internal Revenue vs. Systems Technology Institute, Inc., 833 SCRA 285, July 26, 2017j0d3Noch keine Bewertungen

- Vangent, Inc. Announces Second Quarter 2010 Financial ResultsDokument10 SeitenVangent, Inc. Announces Second Quarter 2010 Financial ResultsChetan VyasNoch keine Bewertungen

- EPIQ SYSTEMS INC 8-K (Events or Changes Between Quarterly Reports) 2009-02-24Dokument11 SeitenEPIQ SYSTEMS INC 8-K (Events or Changes Between Quarterly Reports) 2009-02-24http://secwatch.comNoch keine Bewertungen

- Secretary of State Audit ReportDokument20 SeitenSecretary of State Audit ReportStatesman JournalNoch keine Bewertungen

- CBO Reid Letter HR3590Dokument28 SeitenCBO Reid Letter HR3590clyde2400Noch keine Bewertungen

- United States Securities and Exchange CommissionDokument233 SeitenUnited States Securities and Exchange CommissionjsvrolykNoch keine Bewertungen

- 12 19 Reid Letter ManagersDokument38 Seiten12 19 Reid Letter Managersclyde2400Noch keine Bewertungen

- Cta 2D CV 07000 D 2008jan09 RefDokument14 SeitenCta 2D CV 07000 D 2008jan09 RefSharon AgapuyanNoch keine Bewertungen

- Tool Kit for Tax Administration Management Information SystemVon EverandTool Kit for Tax Administration Management Information SystemBewertung: 1 von 5 Sternen1/5 (1)

- Textbook of Urgent Care Management: Chapter 38, Audits by Managed-Care Organizations and Regulatory AgenciesVon EverandTextbook of Urgent Care Management: Chapter 38, Audits by Managed-Care Organizations and Regulatory AgenciesNoch keine Bewertungen

- Department of Labor: Aces CPDokument36 SeitenDepartment of Labor: Aces CPUSA_DepartmentOfLabor100% (2)

- Department of Labor: Stop2sticker6Dokument1 SeiteDepartment of Labor: Stop2sticker6USA_DepartmentOfLaborNoch keine Bewertungen

- Department of Labor: Dst-Aces-Cps-V20040123Dokument121 SeitenDepartment of Labor: Dst-Aces-Cps-V20040123USA_DepartmentOfLaborNoch keine Bewertungen

- Department of Labor: Generalprovision 6 28 07Dokument6 SeitenDepartment of Labor: Generalprovision 6 28 07USA_DepartmentOfLaborNoch keine Bewertungen

- Department of Labor: Dst-Aces-Cps-V20040617Dokument121 SeitenDepartment of Labor: Dst-Aces-Cps-V20040617USA_DepartmentOfLaborNoch keine Bewertungen

- Department of Labor: YouthworkerDokument1 SeiteDepartment of Labor: YouthworkerUSA_DepartmentOfLaborNoch keine Bewertungen

- Department of Labor: Stop2stickerDokument1 SeiteDepartment of Labor: Stop2stickerUSA_DepartmentOfLaborNoch keine Bewertungen

- Department of Labor: Stop1sticker6Dokument1 SeiteDepartment of Labor: Stop1sticker6USA_DepartmentOfLaborNoch keine Bewertungen

- Department of Labor: Yr English GuideDokument1 SeiteDepartment of Labor: Yr English GuideUSA_DepartmentOfLaborNoch keine Bewertungen

- Department of Labor: ForkliftstickerDokument1 SeiteDepartment of Labor: ForkliftstickerUSA_DepartmentOfLaborNoch keine Bewertungen

- Department of Labor: ln61003Dokument2 SeitenDepartment of Labor: ln61003USA_DepartmentOfLaborNoch keine Bewertungen

- Department of Labor: YouthRulesBrochureDokument12 SeitenDepartment of Labor: YouthRulesBrochureUSA_DepartmentOfLaborNoch keine Bewertungen

- Department of Labor: Niosh Recs To Dol 050302Dokument198 SeitenDepartment of Labor: Niosh Recs To Dol 050302USA_DepartmentOfLaborNoch keine Bewertungen

- Department of Labor: Forkliftsticker6Dokument1 SeiteDepartment of Labor: Forkliftsticker6USA_DepartmentOfLaborNoch keine Bewertungen

- Department of Labor: Stop1stickerDokument1 SeiteDepartment of Labor: Stop1stickerUSA_DepartmentOfLaborNoch keine Bewertungen

- Department of Labor: Niosh Letter FinalDokument3 SeitenDepartment of Labor: Niosh Letter FinalUSA_DepartmentOfLaborNoch keine Bewertungen

- Department of Labor: BookmarkDokument2 SeitenDepartment of Labor: BookmarkUSA_DepartmentOfLaborNoch keine Bewertungen

- Department of Labor: KonstaDokument1 SeiteDepartment of Labor: KonstaUSA_DepartmentOfLaborNoch keine Bewertungen

- Department of Labor: LindseyDokument1 SeiteDepartment of Labor: LindseyUSA_DepartmentOfLaborNoch keine Bewertungen

- Department of Labor: 20040422 YouthrulesDokument1 SeiteDepartment of Labor: 20040422 YouthrulesUSA_DepartmentOfLaborNoch keine Bewertungen

- Department of Labor: Final ReportDokument37 SeitenDepartment of Labor: Final ReportUSA_DepartmentOfLaborNoch keine Bewertungen

- Department of Labor: YouthConstructDokument1 SeiteDepartment of Labor: YouthConstructUSA_DepartmentOfLaborNoch keine Bewertungen

- Department of Labor: JYMP 8x11 2Dokument1 SeiteDepartment of Labor: JYMP 8x11 2USA_DepartmentOfLaborNoch keine Bewertungen

- Department of Labor: JYMP 8x11 3Dokument1 SeiteDepartment of Labor: JYMP 8x11 3USA_DepartmentOfLaborNoch keine Bewertungen

- Department of Labor: JYMP 11x17 1Dokument1 SeiteDepartment of Labor: JYMP 11x17 1USA_DepartmentOfLaborNoch keine Bewertungen

- Department of Labor: JYMP 11x17 3Dokument1 SeiteDepartment of Labor: JYMP 11x17 3USA_DepartmentOfLaborNoch keine Bewertungen

- Department of Labor: JYMP 11x17 2Dokument1 SeiteDepartment of Labor: JYMP 11x17 2USA_DepartmentOfLaborNoch keine Bewertungen

- Department of Labor: JYMP 8x11 1Dokument1 SeiteDepartment of Labor: JYMP 8x11 1USA_DepartmentOfLaborNoch keine Bewertungen

- Boodmo Invoice SPDokument1 SeiteBoodmo Invoice SPDilip MishraNoch keine Bewertungen

- G.R. No. L-26911, L-26924 - Atlas Consolidated Mining & Development Corp. v. Commissioner of Internal RevenueDokument6 SeitenG.R. No. L-26911, L-26924 - Atlas Consolidated Mining & Development Corp. v. Commissioner of Internal RevenueMegan AglauaNoch keine Bewertungen

- Presentation (Aurobindo Pharma)Dokument20 SeitenPresentation (Aurobindo Pharma)SuhailNoch keine Bewertungen

- TaxDokument13 SeitenTaxPinky SalvadorNoch keine Bewertungen

- Manila Electric Company vs. Central Board of Assessment Appeals, Et Al. - Case DigestDokument1 SeiteManila Electric Company vs. Central Board of Assessment Appeals, Et Al. - Case DigestAbigail TolabingNoch keine Bewertungen

- Pre-Sanction Visit Report For Retail LendingDokument5 SeitenPre-Sanction Visit Report For Retail Lendingneeraj guptaNoch keine Bewertungen

- Tax Planning and ManagementDokument12 SeitenTax Planning and ManagementPalash BairagiNoch keine Bewertungen

- Detailed Unit Price Analysis (DUPA) FORM POW-2015-01D-00Dokument1 SeiteDetailed Unit Price Analysis (DUPA) FORM POW-2015-01D-00Engineer ZaldyNoch keine Bewertungen

- Performa Indemnity BondDokument2 SeitenPerforma Indemnity BondNamita Puri0% (1)

- 10 CIR v. Toledo Power CompanyDokument47 Seiten10 CIR v. Toledo Power Companyada mae santoniaNoch keine Bewertungen

- Remission of Duties & Taxes On Exported Products (Rodtep) SchemeDokument21 SeitenRemission of Duties & Taxes On Exported Products (Rodtep) SchemeAnupam BaliNoch keine Bewertungen

- Cost of Capital Solved Problems - Cost of Capital - Capital StructureDokument1 SeiteCost of Capital Solved Problems - Cost of Capital - Capital StructureAnonymous qOdzTznKE100% (1)

- Updated Information On Use of Form W-8Eci (Revision Date February 2006) Before January 1, 2015Dokument2 SeitenUpdated Information On Use of Form W-8Eci (Revision Date February 2006) Before January 1, 2015Criss RojasNoch keine Bewertungen

- Cia15 Study Guide 4 Bac 103 Taxation Income Taxation SfernandoDokument23 SeitenCia15 Study Guide 4 Bac 103 Taxation Income Taxation Sfernando5555-899341Noch keine Bewertungen

- CIR Vs General FoodsDokument12 SeitenCIR Vs General FoodsVictor LimNoch keine Bewertungen

- Goods & Services Tax (GST) - User DashboardDokument3 SeitenGoods & Services Tax (GST) - User Dashboarddurgpalsingh2023Noch keine Bewertungen

- Goods and Services Tax (GST) in IndiaDokument30 SeitenGoods and Services Tax (GST) in IndiarupalNoch keine Bewertungen

- Toa03 05 SBC BC GG Dividends Beps and DepsDokument2 SeitenToa03 05 SBC BC GG Dividends Beps and DepsMerliza JusayanNoch keine Bewertungen

- EOCh 1 Self TestDokument9 SeitenEOCh 1 Self TestHannah valdeNoch keine Bewertungen

- TAXATIONDokument23 SeitenTAXATIONJessica AragonNoch keine Bewertungen

- Buy or Rent House - CalculatorDokument1 SeiteBuy or Rent House - CalculatorRahul VermaNoch keine Bewertungen

- RR 10-98 - FcduDokument6 SeitenRR 10-98 - FcduCkey ArNoch keine Bewertungen

- Corner Brook Furniture Co Makes Bookstands and Expects Sales AnDokument2 SeitenCorner Brook Furniture Co Makes Bookstands and Expects Sales AnAmit PandeyNoch keine Bewertungen

- Taxation Law MCQsDokument17 SeitenTaxation Law MCQsNoemi Hill100% (1)

- Solution Tax667 - Dec 2016Dokument7 SeitenSolution Tax667 - Dec 2016Zahiratul QamarinaNoch keine Bewertungen

- BLO2206 S2 2020 Sample Letter of AdviceDokument11 SeitenBLO2206 S2 2020 Sample Letter of AdviceRuby LeeNoch keine Bewertungen