Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (894)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- India - Index of Industrial ProductionDokument1 SeiteIndia - Index of Industrial ProductionEduardo PetazzeNoch keine Bewertungen

- Turkey - Gross Domestic Product, Outlook 2016-2017Dokument1 SeiteTurkey - Gross Domestic Product, Outlook 2016-2017Eduardo PetazzeNoch keine Bewertungen

- China - Demand For Petroleum, Energy Efficiency and Consumption Per CapitaDokument1 SeiteChina - Demand For Petroleum, Energy Efficiency and Consumption Per CapitaEduardo PetazzeNoch keine Bewertungen

- U.S. Employment Situation - 2015 / 2017 OutlookDokument1 SeiteU.S. Employment Situation - 2015 / 2017 OutlookEduardo PetazzeNoch keine Bewertungen

- Highlights, Wednesday June 8, 2016Dokument1 SeiteHighlights, Wednesday June 8, 2016Eduardo PetazzeNoch keine Bewertungen

- U.S. New Home Sales and House Price IndexDokument1 SeiteU.S. New Home Sales and House Price IndexEduardo PetazzeNoch keine Bewertungen

- Analysis and Estimation of The US Oil ProductionDokument1 SeiteAnalysis and Estimation of The US Oil ProductionEduardo PetazzeNoch keine Bewertungen

- China - Price IndicesDokument1 SeiteChina - Price IndicesEduardo PetazzeNoch keine Bewertungen

- Germany - Renewable Energies ActDokument1 SeiteGermany - Renewable Energies ActEduardo PetazzeNoch keine Bewertungen

- WTI Spot PriceDokument4 SeitenWTI Spot PriceEduardo Petazze100% (1)

- Commitment of Traders - Futures Only Contracts - NYMEX (American)Dokument1 SeiteCommitment of Traders - Futures Only Contracts - NYMEX (American)Eduardo PetazzeNoch keine Bewertungen

- Reflections On The Greek Crisis and The Level of EmploymentDokument1 SeiteReflections On The Greek Crisis and The Level of EmploymentEduardo PetazzeNoch keine Bewertungen

- South Africa - 2015 GDP OutlookDokument1 SeiteSouth Africa - 2015 GDP OutlookEduardo PetazzeNoch keine Bewertungen

- India 2015 GDPDokument1 SeiteIndia 2015 GDPEduardo PetazzeNoch keine Bewertungen

- México, PBI 2015Dokument1 SeiteMéxico, PBI 2015Eduardo PetazzeNoch keine Bewertungen

- U.S. Federal Open Market Committee: Federal Funds RateDokument1 SeiteU.S. Federal Open Market Committee: Federal Funds RateEduardo PetazzeNoch keine Bewertungen

- US Mining Production IndexDokument1 SeiteUS Mining Production IndexEduardo PetazzeNoch keine Bewertungen

- Singapore - 2015 GDP OutlookDokument1 SeiteSingapore - 2015 GDP OutlookEduardo PetazzeNoch keine Bewertungen

- China - Power GenerationDokument1 SeiteChina - Power GenerationEduardo PetazzeNoch keine Bewertungen

- Mainland China - Interest Rates and InflationDokument1 SeiteMainland China - Interest Rates and InflationEduardo PetazzeNoch keine Bewertungen

- Highlights in Scribd, Updated in April 2015Dokument1 SeiteHighlights in Scribd, Updated in April 2015Eduardo PetazzeNoch keine Bewertungen

- USA - Oil and Gas Extraction - Estimated Impact by Low Prices On Economic AggregatesDokument1 SeiteUSA - Oil and Gas Extraction - Estimated Impact by Low Prices On Economic AggregatesEduardo PetazzeNoch keine Bewertungen

- US - Personal Income and Outlays - 2015-2016 OutlookDokument1 SeiteUS - Personal Income and Outlays - 2015-2016 OutlookEduardo PetazzeNoch keine Bewertungen

- European Commission, Spring 2015 Economic Forecast, Employment SituationDokument1 SeiteEuropean Commission, Spring 2015 Economic Forecast, Employment SituationEduardo PetazzeNoch keine Bewertungen

- Brazilian Foreign TradeDokument1 SeiteBrazilian Foreign TradeEduardo PetazzeNoch keine Bewertungen

- United States - Gross Domestic Product by IndustryDokument1 SeiteUnited States - Gross Domestic Product by IndustryEduardo PetazzeNoch keine Bewertungen

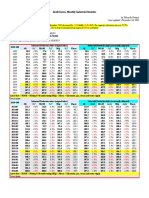

- Chile, Monthly Index of Economic Activity, IMACECDokument2 SeitenChile, Monthly Index of Economic Activity, IMACECEduardo PetazzeNoch keine Bewertungen

- Japan, Population and Labour Force - 2015-2017 OutlookDokument1 SeiteJapan, Population and Labour Force - 2015-2017 OutlookEduardo PetazzeNoch keine Bewertungen

- South Korea, Monthly Industrial StatisticsDokument1 SeiteSouth Korea, Monthly Industrial StatisticsEduardo PetazzeNoch keine Bewertungen

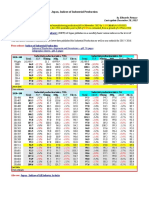

- Japan, Indices of Industrial ProductionDokument1 SeiteJapan, Indices of Industrial ProductionEduardo PetazzeNoch keine Bewertungen

- 2017 Book TheBusinessOfBankingDokument253 Seiten2017 Book TheBusinessOfBankingMohamed HendawyNoch keine Bewertungen

- 1-Macroeconomics - Overview and Study FieldDokument29 Seiten1-Macroeconomics - Overview and Study Fieldrichard tocaNoch keine Bewertungen

- The European Union Lesson 1Dokument17 SeitenThe European Union Lesson 1api-53255207Noch keine Bewertungen

- Good Newspapers ArticlesDokument151 SeitenGood Newspapers ArticlesManish YadavNoch keine Bewertungen

- New Left Review, Volume 324 (November - December 2014)Dokument150 SeitenNew Left Review, Volume 324 (November - December 2014)GrahamAustinNoch keine Bewertungen

- Progression of FERA To FEMADokument49 SeitenProgression of FERA To FEMAMoaaz AhmedNoch keine Bewertungen

- Foreign Exchange Consensus Forecasts by Consensus Economics Inc.Dokument36 SeitenForeign Exchange Consensus Forecasts by Consensus Economics Inc.Consensus EconomicsNoch keine Bewertungen

- Financial Times USA 28 July 2023Dokument16 SeitenFinancial Times USA 28 July 2023Nikolai LazarovNoch keine Bewertungen

- Who Moved My Interest Rate - Leading The Reserve Bank of India Through Five Turbulent Years (PDFDrive)Dokument294 SeitenWho Moved My Interest Rate - Leading The Reserve Bank of India Through Five Turbulent Years (PDFDrive)dev guptaNoch keine Bewertungen

- EcbDokument210 SeitenEcbhnkyNoch keine Bewertungen

- Wallstreetjournaleurope 20160307 The Wall Street Journal EuropeDokument22 SeitenWallstreetjournaleurope 20160307 The Wall Street Journal EuropestefanoNoch keine Bewertungen

- Fmi - Part 4 - Chap 10 - Conduct of Monetary PolicyDokument65 SeitenFmi - Part 4 - Chap 10 - Conduct of Monetary PolicyTouseef Rizvi100% (1)

- Flash Note: Euro Area: ECB Monetary PolicyDokument6 SeitenFlash Note: Euro Area: ECB Monetary Policyapi-309425623Noch keine Bewertungen

- Barclays Capital Tuesday Credit Call 20 September 2011Dokument22 SeitenBarclays Capital Tuesday Credit Call 20 September 2011poitrenacNoch keine Bewertungen

- Case Study of RelianceDokument3 SeitenCase Study of RelianceClementFernandesNoch keine Bewertungen

- Declaratie de Conformitate Ce: Cu Seria Produs de La LaDokument3 SeitenDeclaratie de Conformitate Ce: Cu Seria Produs de La LaVasile Marian AdrianNoch keine Bewertungen

- Delloit Research On ILAAPDokument16 SeitenDelloit Research On ILAAPATISHAY JAINNoch keine Bewertungen

- Pulling The Plug On The Car Industry The Dismal State of Germany's Army Debt On The Nile How To Conduct A Sex SurveyDokument88 SeitenPulling The Plug On The Car Industry The Dismal State of Germany's Army Debt On The Nile How To Conduct A Sex SurveyEconomist MagazineNoch keine Bewertungen

- JPM U S Year Ahead 2012 2011 12 10 738272Dokument156 SeitenJPM U S Year Ahead 2012 2011 12 10 738272apache05Noch keine Bewertungen

- The Relationship Between Money, Identity, and European IntegrationDokument28 SeitenThe Relationship Between Money, Identity, and European IntegrationreniestessNoch keine Bewertungen

- Survival of the euro requires fiscal decentralization and financial centralizationDokument57 SeitenSurvival of the euro requires fiscal decentralization and financial centralizationAdrianaNoch keine Bewertungen

- Occasional Paper Series: ECB Economy-Wide Climate Stress TestDokument91 SeitenOccasional Paper Series: ECB Economy-Wide Climate Stress TestAparnaNoch keine Bewertungen

- Geojit Insights October 2019 PDFDokument52 SeitenGeojit Insights October 2019 PDFMauryanNoch keine Bewertungen

- Material Didactic Engleza FABBVDokument6 SeitenMaterial Didactic Engleza FABBVMarius-Mihai DUMITRACHENoch keine Bewertungen

- Reith 2020 Lecture 2 TranscriptDokument17 SeitenReith 2020 Lecture 2 TranscriptHuy BuiNoch keine Bewertungen

- Presented by Piyush Chawala Sukant Prusty Anurag Nath Satish Naik Manjushaa Hemanth KumarDokument63 SeitenPresented by Piyush Chawala Sukant Prusty Anurag Nath Satish Naik Manjushaa Hemanth Kumarsalonid17Noch keine Bewertungen

- The Markets in Crypto-Assets Regulation (MICA)Dokument33 SeitenThe Markets in Crypto-Assets Regulation (MICA)Eve AthanasekouNoch keine Bewertungen

- Eur To Usd Trading Basics XDokument3 SeitenEur To Usd Trading Basics XVeljko KerčevićNoch keine Bewertungen

- David Einhorn Grant's ConferenceDokument89 SeitenDavid Einhorn Grant's ConferenceCanadianValueNoch keine Bewertungen