Das könnte Ihnen auch gefallen

- Consulting Diagrams and Design Templates SampleDokument96 SeitenConsulting Diagrams and Design Templates SampleSTRATICX100% (1)

- Issue-Based Work Planning and Hypothesis Problem SolvingDokument13 SeitenIssue-Based Work Planning and Hypothesis Problem SolvingSTRATICXNoch keine Bewertungen

- Organizational Velocity - Improving Speed, Efficiency & Effectiveness of Business SampleDokument24 SeitenOrganizational Velocity - Improving Speed, Efficiency & Effectiveness of Business SampleSTRATICXNoch keine Bewertungen

- Complete Toolkit For Improving MeetingsDokument16 SeitenComplete Toolkit For Improving MeetingsSTRATICXNoch keine Bewertungen

- Complete Resource For Consulting Frameworks and Design TemplatesDokument180 SeitenComplete Resource For Consulting Frameworks and Design TemplatesSTRATICXNoch keine Bewertungen

- Complete Guide To Business Strategy DesignDokument26 SeitenComplete Guide To Business Strategy DesignSTRATICX100% (2)

- Building A Market Model and Market SizingDokument12 SeitenBuilding A Market Model and Market SizingSTRATICXNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- RSA CASES I To IIDokument215 SeitenRSA CASES I To IICrest PedrosaNoch keine Bewertungen

- Management Advisory ServicesDokument4 SeitenManagement Advisory ServicesYaj CruzadaNoch keine Bewertungen

- IDirect KalpataruPower Q2FY20Dokument10 SeitenIDirect KalpataruPower Q2FY20QuestAviatorNoch keine Bewertungen

- Warren Buffett and GEICO Case StudyDokument18 SeitenWarren Buffett and GEICO Case StudyReymond Jude PagcoNoch keine Bewertungen

- Financial Reporting Financial Statement Analysis and Valuation 8th Edition Wahlen Solutions Manual 1Dokument36 SeitenFinancial Reporting Financial Statement Analysis and Valuation 8th Edition Wahlen Solutions Manual 1ericsuttonybmqwiorsa100% (24)

- Investment and Portfolio Management: ACFN 3201Dokument16 SeitenInvestment and Portfolio Management: ACFN 3201Bantamkak FikaduNoch keine Bewertungen

- Manila Electric Co Vs Province of Laguna - G.R. No. 131359. May 5, 1999Dokument6 SeitenManila Electric Co Vs Province of Laguna - G.R. No. 131359. May 5, 1999Ebbe DyNoch keine Bewertungen

- Fis - Micro Finance NotesDokument5 SeitenFis - Micro Finance NotesDr. MURALI KRISHNA VELAVETINoch keine Bewertungen

- Module 7 CVP Analysis SolutionsDokument12 SeitenModule 7 CVP Analysis SolutionsChiran AdhikariNoch keine Bewertungen

- Residential Status: Project Report OnDokument6 SeitenResidential Status: Project Report OnTarun Inder KaurNoch keine Bewertungen

- Chapter - 8Dokument17 SeitenChapter - 8Maruf AhmedNoch keine Bewertungen

- Book Value Assets Realizable Value: Nama: Firda Arfianti NIM: 2301949596Dokument2 SeitenBook Value Assets Realizable Value: Nama: Firda Arfianti NIM: 2301949596FirdaNoch keine Bewertungen

- PolicyDokument5 SeitenPolicyRichard WijayaNoch keine Bewertungen

- 10 - G.R. No. 181845 - City of Manila V Coca-Cola PDFDokument7 Seiten10 - G.R. No. 181845 - City of Manila V Coca-Cola PDFRenz Francis LimNoch keine Bewertungen

- Chapter 5: Investment Companies: DefinitionDokument16 SeitenChapter 5: Investment Companies: Definitiontjarnob13100% (1)

- DA Case WriteupDokument2 SeitenDA Case WriteupHaseebAshfaqNoch keine Bewertungen

- Wacc and MMDokument2 SeitenWacc and MMThảo NguyễnNoch keine Bewertungen

- Turkish Tax SystemDokument3 SeitenTurkish Tax Systemapi-3835399Noch keine Bewertungen

- Control AccountsDokument1 SeiteControl AccountsFalak MuscatiNoch keine Bewertungen

- A Pair Trade With Some Sparkle - Long Signet Jewelers (SIG) /short Blue Nile (NILE)Dokument20 SeitenA Pair Trade With Some Sparkle - Long Signet Jewelers (SIG) /short Blue Nile (NILE)PAA researchNoch keine Bewertungen

- BCOM Syllabus MBB and Ram ThakurDokument4 SeitenBCOM Syllabus MBB and Ram ThakurAnimeshSahaNoch keine Bewertungen

- Multiple ChoiceDokument18 SeitenMultiple ChoiceJonnel Samaniego100% (1)

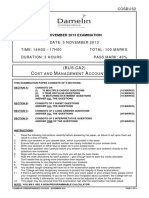

- (COSBUS2) (BUS-CA2) Cost and Management Accounting 2 (Nov2013) v5Dokument8 Seiten(COSBUS2) (BUS-CA2) Cost and Management Accounting 2 (Nov2013) v5FarrukhsgNoch keine Bewertungen

- CorpLiq Draft (Recovered)Dokument9 SeitenCorpLiq Draft (Recovered)Via Samantha de AustriaNoch keine Bewertungen

- Rumus Perhitungan KeekonomianDokument1 SeiteRumus Perhitungan KeekonomianihsansepalmaNoch keine Bewertungen

- Internship Report On The Bank of PunjabDokument91 SeitenInternship Report On The Bank of PunjabArslan73% (22)

- Ais Quiz 5Dokument5 SeitenAis Quiz 5Annieka PascualNoch keine Bewertungen

- IFRS16 - Lease Standard SAP Solution Through Real Estate Management - SAP BlogsDokument12 SeitenIFRS16 - Lease Standard SAP Solution Through Real Estate Management - SAP BlogsFranki Giassi MeurerNoch keine Bewertungen

- Rhombus Energy vs. CIRDokument7 SeitenRhombus Energy vs. CIREmNoch keine Bewertungen

- Sample by LawsDokument11 SeitenSample by Lawsgilberthufana446877Noch keine Bewertungen